Nvidia shares pop as analysts dismiss AI bubble concerns

Introduction & Market Context

Griffon Corporation (NYSE:GFF) presented its fourth quarter and full-year 2025 results on November 19, 2025, showcasing strong financial performance that exceeded analyst expectations. The company’s shares responded positively, rising 3.29% to $69.06 following the earnings release, with pre-market trading showing initial gains of 3.19%.

The building products and consumer goods manufacturer highlighted its successful portfolio transformation and margin expansion strategies across its two main operating segments. Griffon’s performance comes amid a resilient repair and remodel market, which continues to see elevated activity levels exceeding $510 billion in annual spend.

Financial Performance Highlights

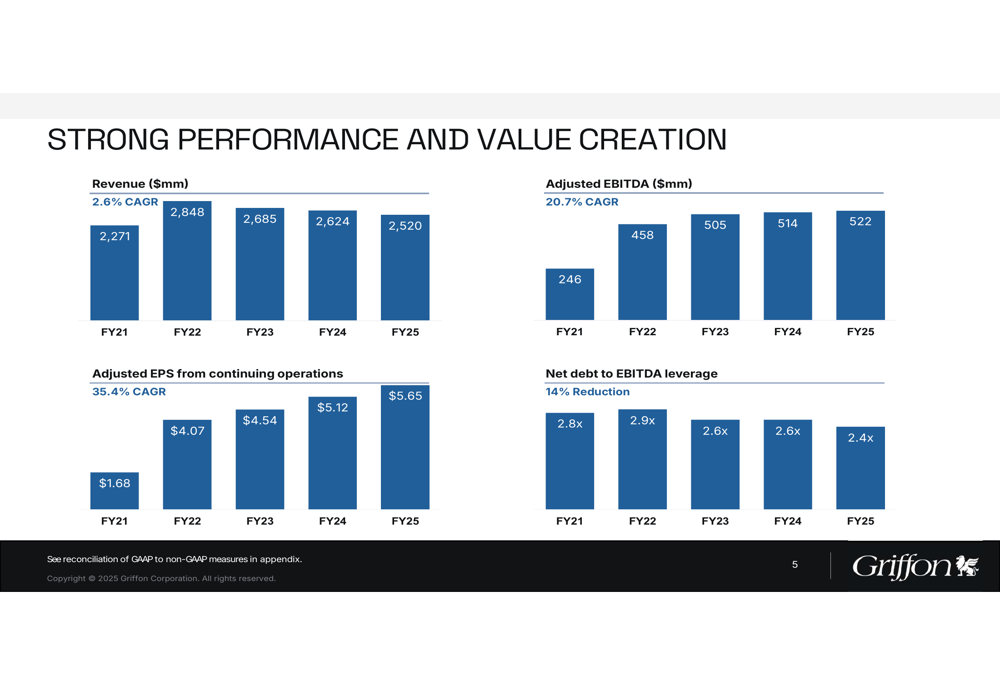

Griffon reported full-year revenue of $2.52 billion for fiscal 2025, maintaining consistent performance with the previous year while significantly improving profitability metrics. The company’s adjusted EBITDA reached $522 million, representing a 21% margin and demonstrating substantial improvement over the past four years.

As shown in the following chart of financial performance:

The company has achieved impressive compound annual growth rates (CAGR) from FY21 to FY25, including 2.6% for revenue, 20.7% for adjusted EBITDA, and a remarkable 35.4% for adjusted earnings per share. Adjusted EPS increased from $1.68 in FY21 to $5.65 in FY25, while net debt to EBITDA leverage improved from 2.8x to 2.4x during the same period.

For the fourth quarter specifically, Griffon reported revenue of $662.2 million, exceeding analyst expectations of $631.41 million. Quarterly earnings per share came in at $1.54, surpassing the forecasted $1.51 and contributing to the positive market reaction.

Segment Analysis

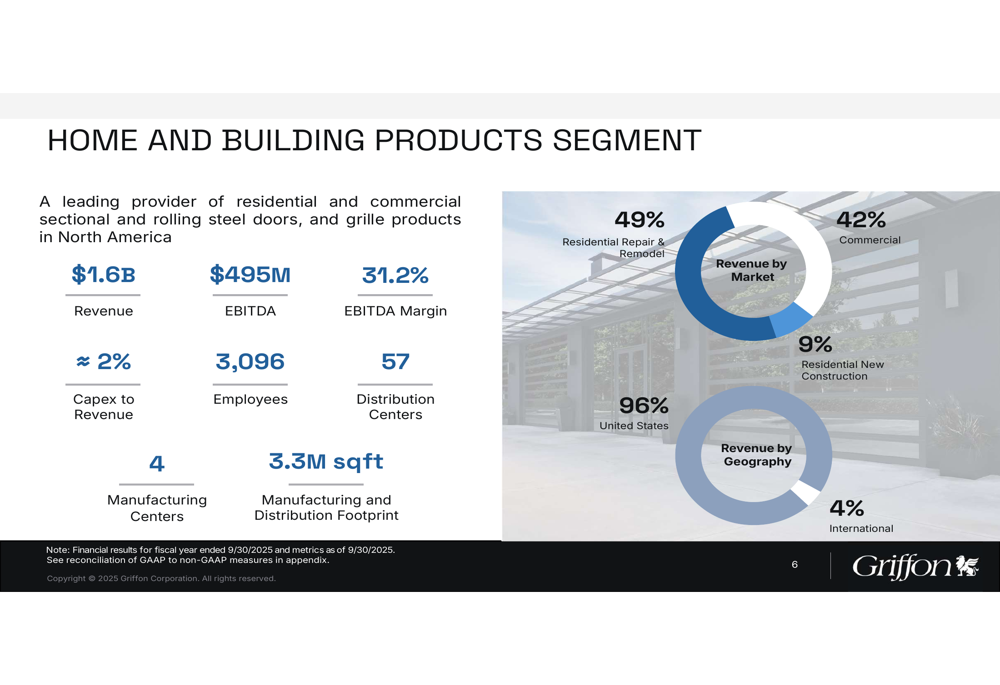

Griffon’s business is divided into two primary segments: Home and Building Products (HBP) and Consumer and Professional Products (CPP). The performance disparity between these segments highlights both strengths and opportunities within the company’s portfolio.

The Home and Building Products segment, which accounts for 63% of total revenue, has demonstrated exceptional profitability with an EBITDA of $495 million and a 31.2% EBITDA margin. This segment’s revenue breakdown is illustrated below:

HBP’s revenue is primarily derived from residential repair and remodel activities (49%) and commercial applications (42%), with residential new construction representing just 9%. Geographically, the segment remains heavily concentrated in the United States (96%).

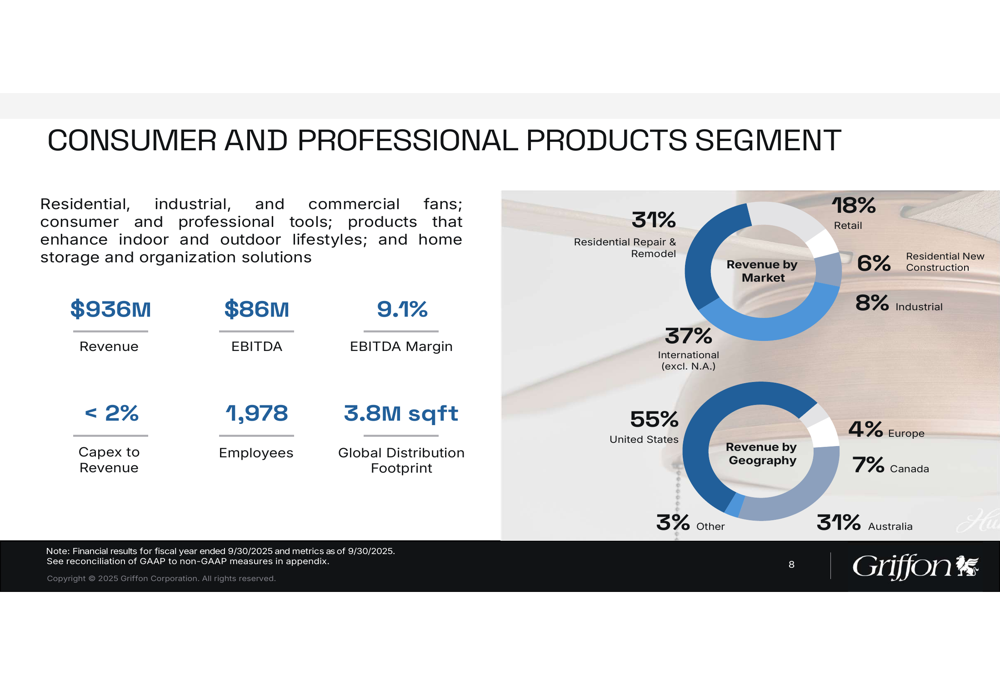

In contrast, the Consumer and Professional Products segment, contributing 37% of revenue, reported an EBITDA of $86 million with a 9.1% margin. The segment’s revenue sources and geographic distribution show greater diversification:

CPP’s revenue is more balanced across residential repair and remodel (31%), retail (18%), residential new construction (6%), and industrial applications (8%). Internationally, the segment generates 45% of its revenue outside the United States, with Australia representing a significant 31% of the total.

Capital Allocation & Strategic Initiatives

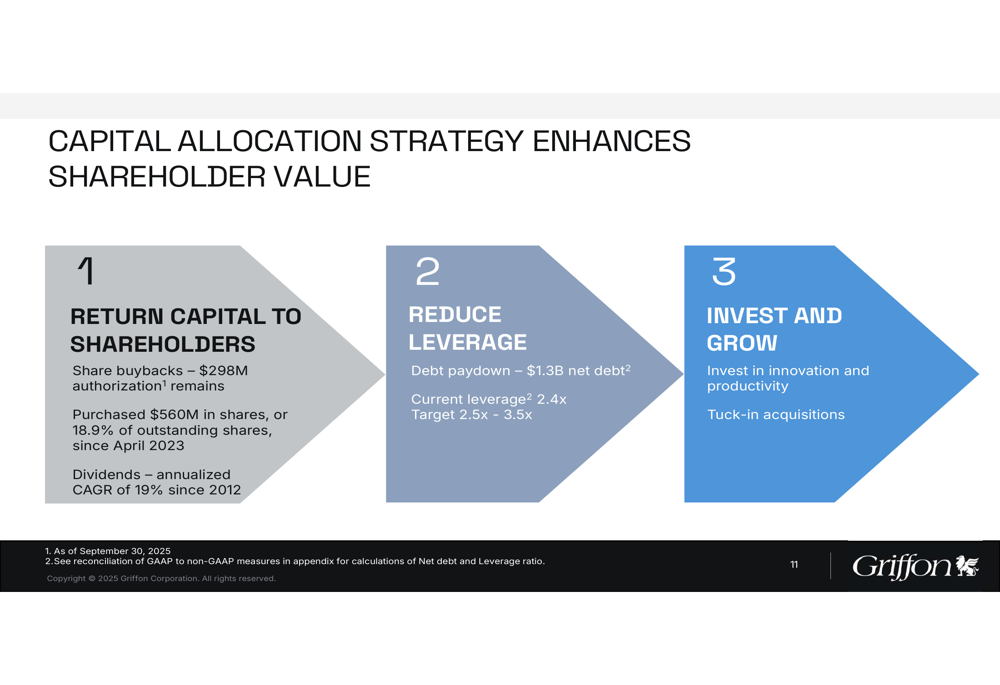

Griffon’s capital allocation strategy emphasizes shareholder returns while maintaining financial discipline, as detailed in the following slide:

The company has aggressively returned capital to shareholders, purchasing $560 million in shares (representing 18.9% of outstanding shares) since April 2023, with $298 million remaining in its authorization. Dividend growth has been substantial, with an annualized CAGR of 19% since 2012.

While focusing on shareholder returns, Griffon has simultaneously reduced its leverage to 2.4x net debt to EBITDA, within its target range of 2.5x to 3.5x. The company’s total net debt stands at $1.3 billion.

The presentation also highlighted Griffon’s strategic portfolio reshaping since 2018, including the acquisitions of ClosetMaid, CornellCookson, and Hunter Fan. These moves have positioned the company to capitalize on secular market trends, particularly in the repair and remodel sector.

Forward Outlook

Looking ahead to fiscal 2026, Griffon provided guidance that reflects confidence in its operational strategy while acknowledging market challenges. The company expects stable revenue of approximately $2.5 billion, with adjusted EBITDA projected between $580 million and $600 million.

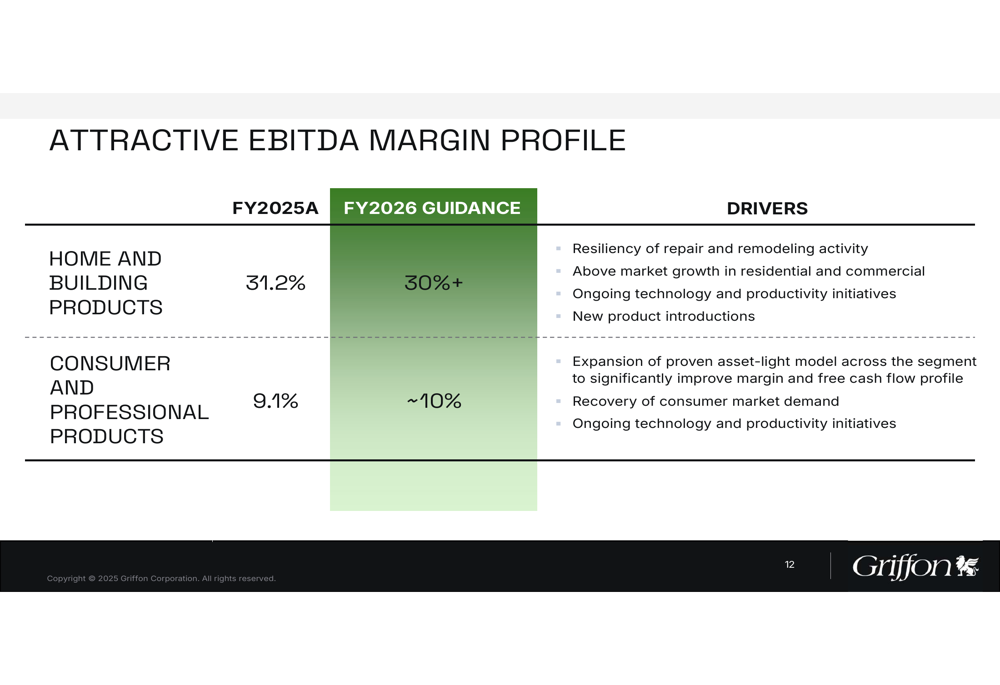

The segment-specific margin outlook reveals Griffon’s priorities for the coming year:

The HBP segment is expected to maintain its strong EBITDA margin above 30%, driven by the resiliency of repair and remodeling activity, above-market growth in both residential and commercial sectors, and ongoing technology and productivity initiatives.

For the CPP segment, Griffon targets margin improvement to approximately 10%, primarily through the expansion of its asset-light model across the segment. This approach aims to significantly enhance both margin and free cash flow profiles while positioning the business for recovery in consumer market demand.

During the earnings call, CEO Ron Kramer expressed confidence in the company’s strategic positioning, stating, "We are well positioned as we enter fiscal 2026 and are confident in our ability to continue to generate strong financial performance." He emphasized the importance of brand strength and product quality in driving sustained growth.

Griffon’s performance and outlook reflect its ability to navigate challenging macroeconomic conditions while delivering value to shareholders through operational excellence and strategic capital allocation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.