Trump administration authorizes CIA for covert action in Venezuela - Bloomberg

Introduction & Market Context

Grong Sparebank (GRONG) reported its first quarter 2025 results on May 13, showing mixed performance with strong loan growth offset by rising loan losses and compressed interest margins. The Norwegian regional bank continues its expansion strategy despite challenging market conditions, including high competition and geopolitical uncertainties.

The bank’s stock closed at NOK 150 before the presentation, up 0.64% for the day, and has traded between NOK 134.98 and NOK 159 over the past 52 weeks.

Quarterly Performance Highlights

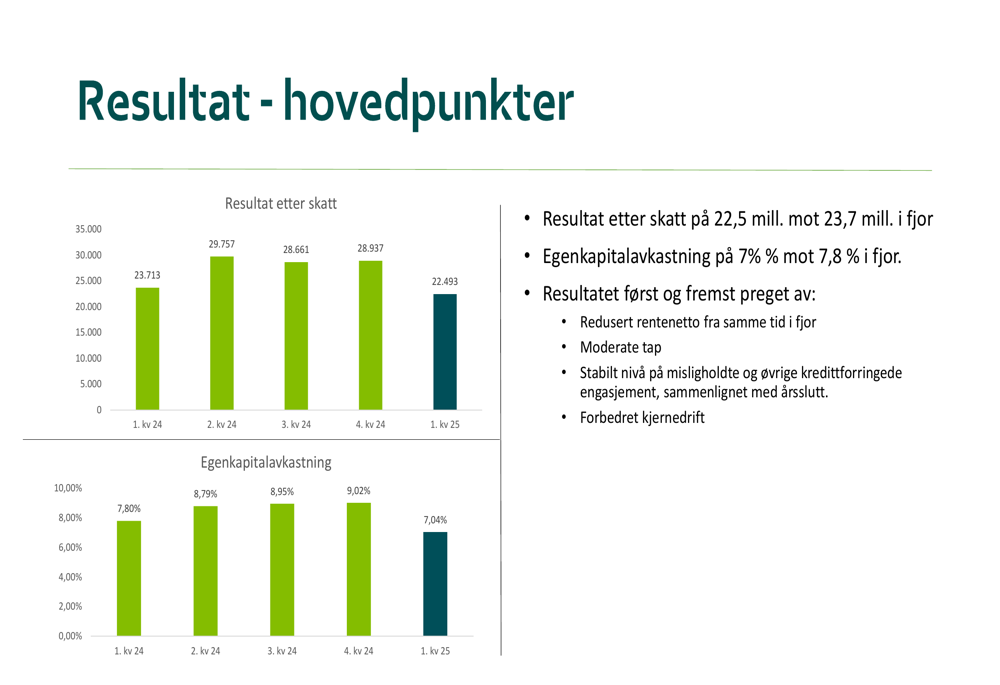

Grong Sparebank reported a profit after tax of NOK 22.493 million for Q1 2025, down from NOK 23.713 million in the same period last year. Return on equity declined to 7.04% from 7.8% in Q1 2024, falling short of the bank’s long-term target of at least 9%.

As shown in the following chart of quarterly results and return on equity:

The bank’s performance was primarily affected by reduced net interest income, moderate losses, and stable levels of non-performing loans compared to year-end. However, management highlighted improved core operations as a positive factor.

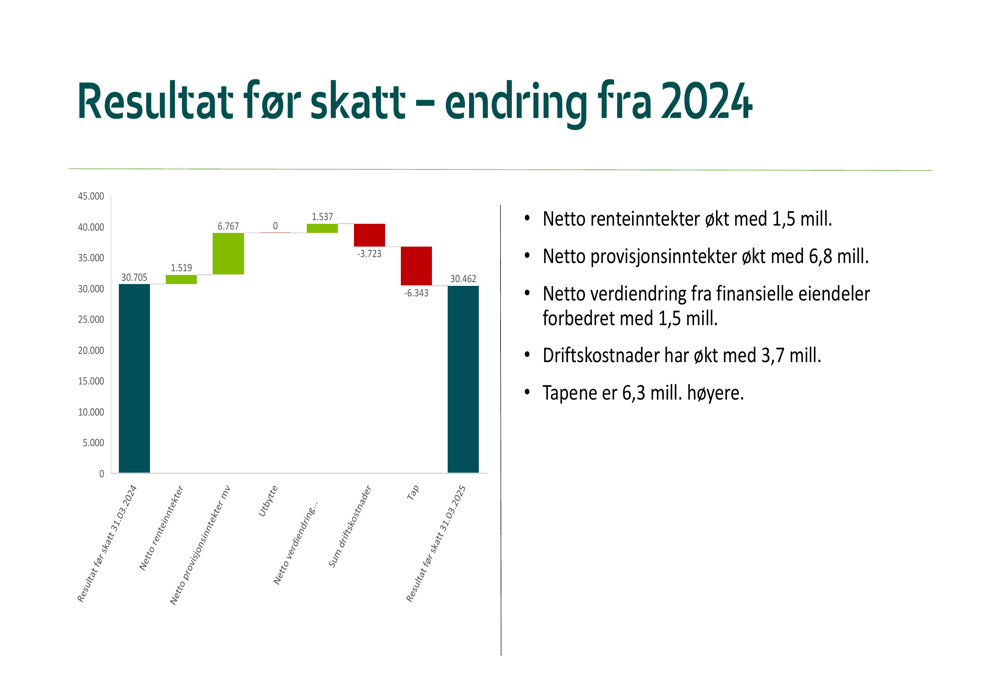

The waterfall chart below illustrates the key factors influencing the change in profit before tax from Q1 2024 to Q1 2025:

Detailed Financial Analysis

Net Interest Income and Margins

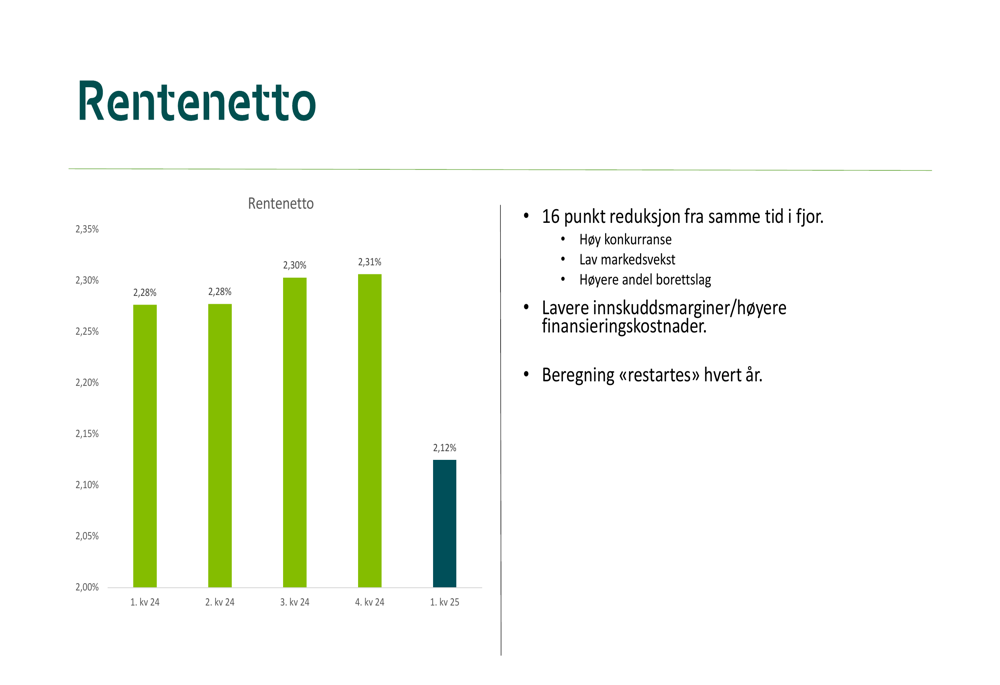

Net interest income declined to 2.12% in Q1 2025 from 2.30% in the same period last year, representing a 16 basis point reduction. Management attributed this compression to high competition, low market growth, a higher proportion of housing cooperative loans, lower deposit margins, and higher financing costs.

The following chart shows the declining trend in net interest income over the past five quarters:

Commission Income and Operating Costs

In contrast to the pressure on interest income, net commission income showed significant improvement, reaching NOK 24.3 million in Q1 2025 compared to NOK 17.5 million in Q1 2024. This 38.9% increase was primarily driven by higher commission income from Eika Boligkreditt, increased insurance commissions, and growth in payment services and securities management.

The cost index excluding securities improved slightly to 53.04% in Q1 2025 from 53.94% in the same period last year, though still above the bank’s long-term target of less than 52%. Higher personnel costs were cited as a factor, likely due to the opening of new branch offices in Verdal and Mo i Rana.

Loan Quality and Provisions

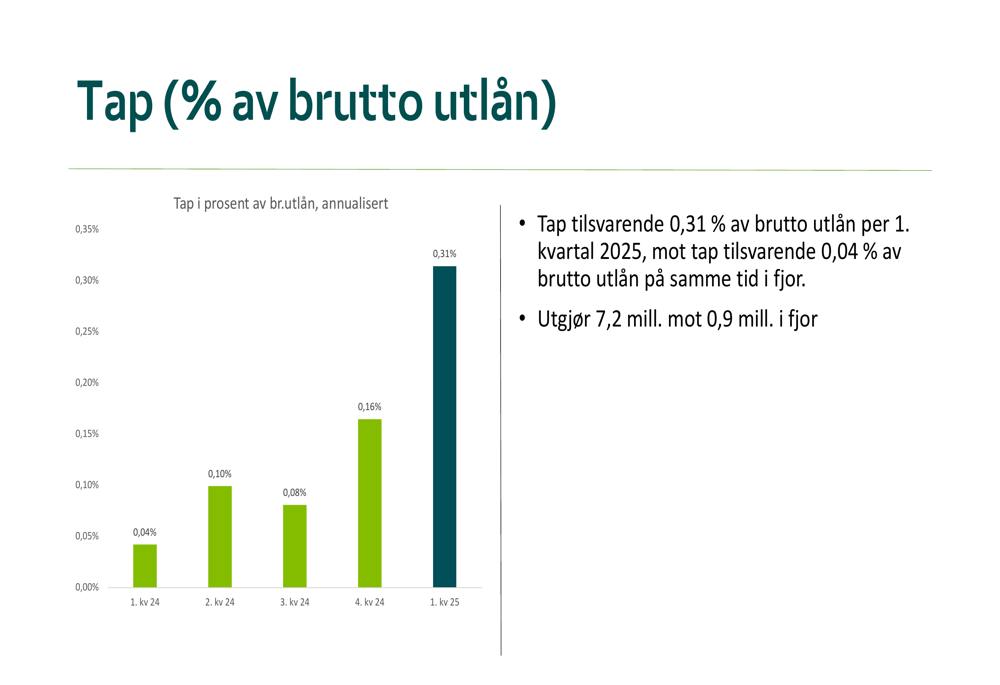

Loan losses increased substantially to 0.31% of gross loans in Q1 2025, compared to just 0.04% in Q1 2024. This represents NOK 7.2 million in losses, up from NOK 0.9 million in the same period last year.

The following chart illustrates the concerning upward trend in loan losses over the past five quarters:

Non-performing loans over 90 days stood at 0.55% of gross loans at the end of Q1 2025, down from 0.66% at year-end 2024 but up significantly from 0.15% in Q1 2024. Other loss-affected commitments increased to 1.16% from 0.24% a year earlier. Combined, non-performing and other loss-affected commitments totaled 1.71%, unchanged from year-end.

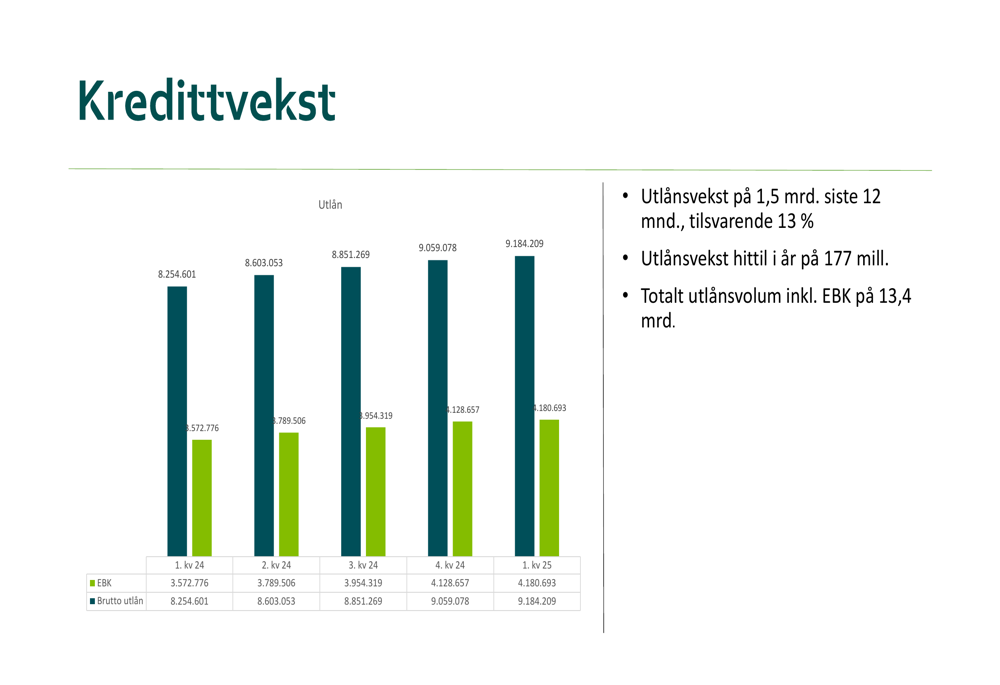

Balance Sheet Growth

Grong Sparebank continued to demonstrate strong growth in its loan portfolio, with total loans increasing by NOK 1.5 billion or 13% over the past 12 months. Total (EPA:TTEF) loan volume including Eika Boligkreditt reached NOK 13.4 billion, with NOK 177 million in growth so far this year.

The chart below shows the consistent growth in both gross loans and loans through Eika Boligkreditt (EBK):

Deposits also showed healthy growth, reaching NOK 8 billion, an increase of NOK 649 million or 8.8% year-over-year. However, deposit coverage declined to 87.4% from 89.3% last year, indicating that loan growth outpaced deposit growth.

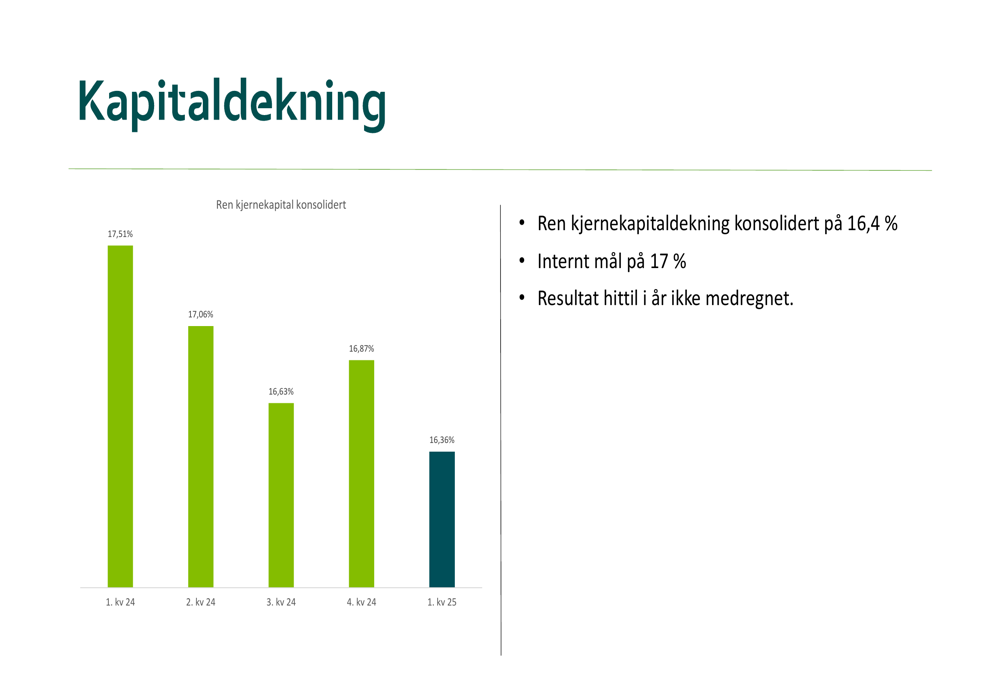

Capital Position

The bank’s consolidated core capital adequacy ratio declined to 16.36% in Q1 2025 from 17.51% in Q1 2024, falling below the internal target of 17%. Management noted that the result year-to-date is not included in this calculation.

Strategic Initiatives and Outlook

Grong Sparebank outlined several forward-looking initiatives and market factors that will impact its performance:

1. A more risk-sensitive standard method for capital calculations will be introduced in Q2 2025, which management expects will provide more equal competitive conditions between small, medium, and large banks. For Grong Sparebank, this is anticipated to result in capital easing and continued opportunity for growth.

2. The bank plans to open a new branch office in Mo i Rana in Q2 2025, continuing its expansion strategy despite challenging market conditions.

3. Management highlighted ongoing geopolitical and market turmoil as external factors that could impact performance.

Despite the mixed results, Grong Sparebank continues to pursue growth opportunities while managing increasing loan losses. The bank’s ability to improve commission income partially offsets the pressure on interest margins, but the rising trend in loan losses will require careful monitoring in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.