Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

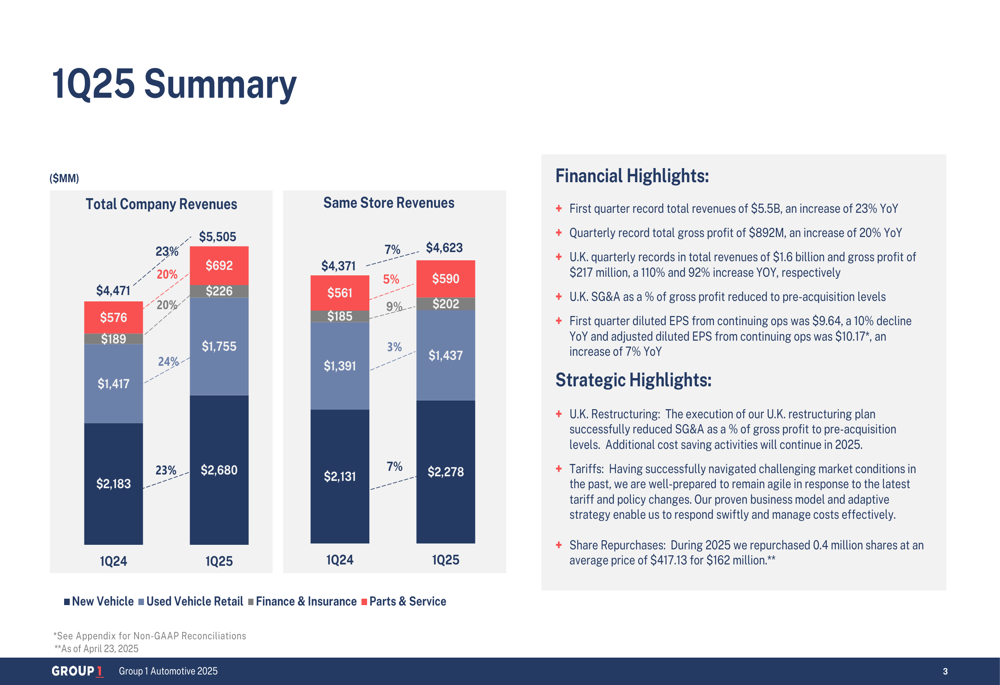

Group 1 Automotive Inc (NYSE:GPI) reported strong first-quarter 2025 results on April 24, showcasing significant revenue growth and continued progress on its UK restructuring initiatives. The automotive retailer, which operates 260 dealerships across the US and UK, posted record total revenues of $5.5 billion, representing a 23% year-over-year increase.

Despite the company’s solid performance, GPI’s stock has seen some pressure recently, closing at $398.65 on April 23, down 0.79% for the day. The stock is currently trading well below its 52-week high of $490.09, though significantly above its 52-week low of $279.86.

Quarterly Performance Highlights

Group 1’s first quarter results demonstrated robust growth across key financial metrics. Total (EPA:TTEF) company revenues reached $5.5 billion, a 23% increase from $4.47 billion in Q1 2024. This growth was driven by strong performance across all business segments, with new vehicle sales up 23%, used vehicle retail sales up 24%, and finance & insurance revenue up 20%.

As shown in the following comprehensive financial summary:

The company reported quarterly record total gross profit of $892 million, representing a 20% increase year-over-year. However, first quarter diluted EPS from continuing operations was $9.64, a 10% decline compared to the same period last year. On an adjusted basis, diluted EPS was $10.17, showing a 7% improvement year-over-year.

Same-store revenues also showed healthy growth at 7% year-over-year, reaching $4.62 billion. This performance indicates organic growth beyond the company’s acquisition strategy, with particularly strong results in new vehicle sales (up 7%) and parts & service (up 7%).

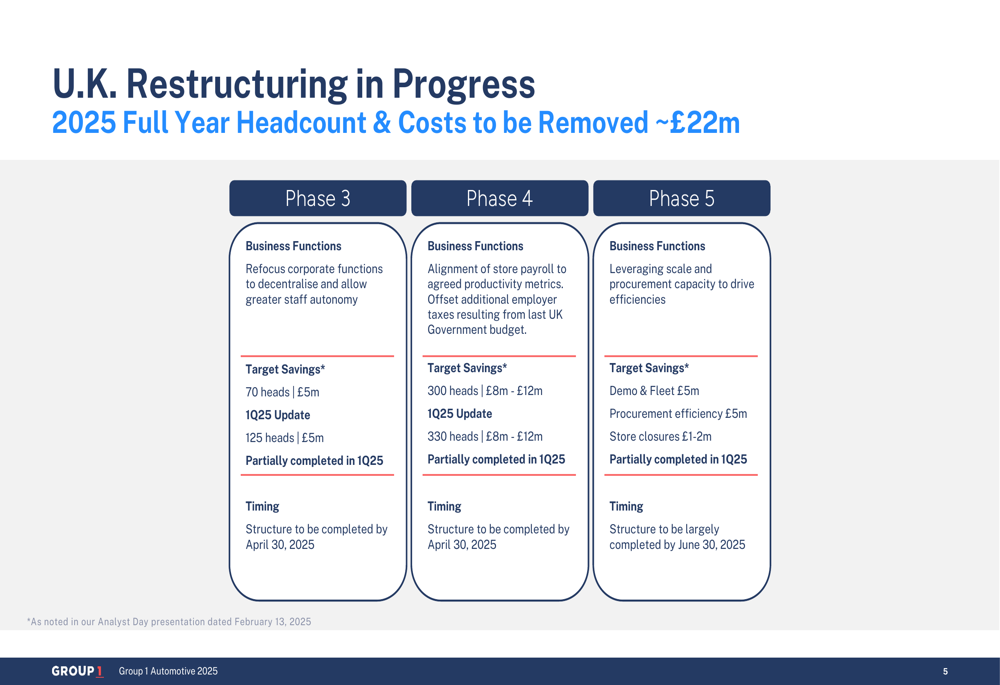

UK Restructuring Progress

A significant focus of Group 1’s presentation was the ongoing restructuring of its UK operations, which has already yielded substantial cost savings. The company has completed several phases of its restructuring plan, resulting in £15 million in cost savings through headcount reductions and operational efficiencies.

The restructuring initiatives included streamlining the executive team, eliminating duplicated corporate functions, onshoring shared services, and strategically closing underperforming used car locations. These efforts have successfully reduced SG&A as a percentage of gross profit to pre-acquisition levels.

Looking ahead, Group 1 outlined its ongoing UK restructuring plans, which are expected to deliver an additional £22 million in cost savings during 2025:

The company is making significant progress on these initiatives, with partial completion already achieved in Q1 2025. The restructuring is focused on decentralizing corporate functions, aligning store payroll to productivity metrics, and leveraging scale for procurement efficiencies.

Strategic Initiatives

Group 1’s presentation highlighted several strategic advantages that position the company for continued success. These include strong earnings and cash flow generation, portfolio optimization through M&A and share repurchases, Parts & Service growth, and building local scale in key markets.

The company’s strategic approach is clearly illustrated in this overview:

Portfolio optimization remains a key focus, with Group 1 having acquired $8.5 billion in revenues since the beginning of 2021. The company has also repurchased approximately 5.8 million shares during this period, representing 32% of its share count. In Q1 2025 alone, the company repurchased 0.4 million shares at an average price of $417.13 for a total of $162 million.

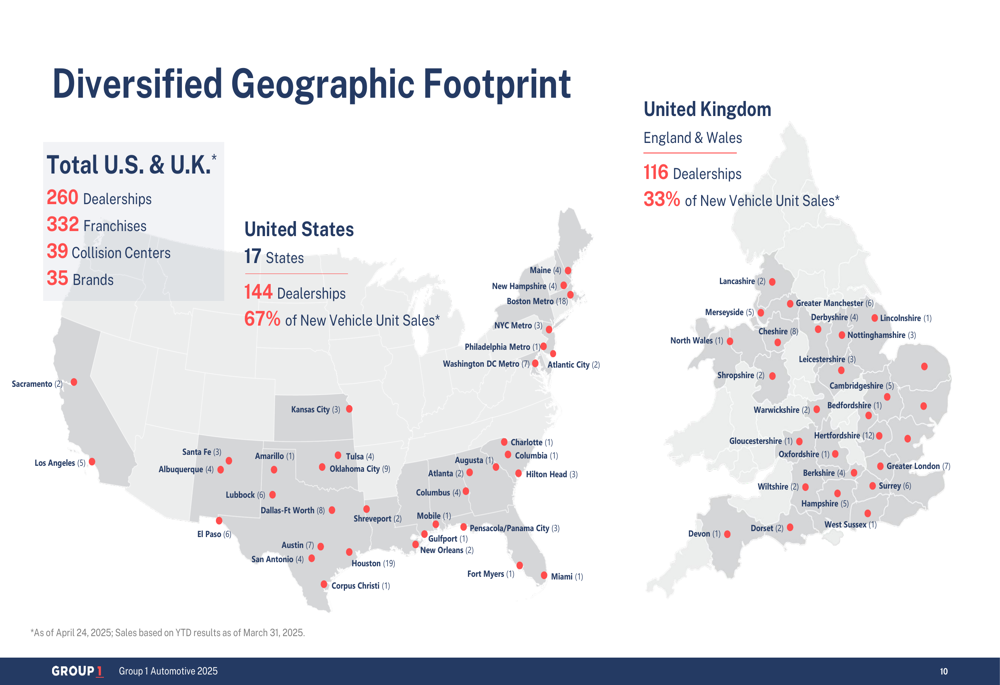

Group 1’s geographic diversification provides stability and growth opportunities across multiple markets. The company operates 144 dealerships across 17 states in the US and 116 dealerships in the UK, as shown in this comprehensive footprint overview:

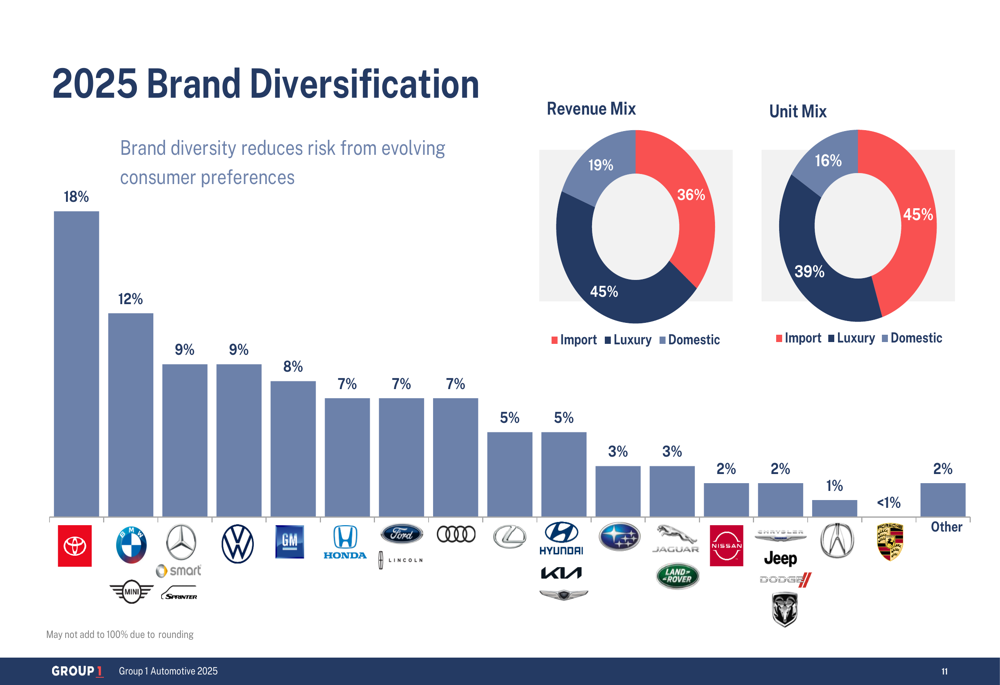

The company’s brand portfolio is also well-diversified, with a balanced mix of import, luxury, and domestic brands. This diversification helps mitigate risks associated with any single manufacturer or market segment:

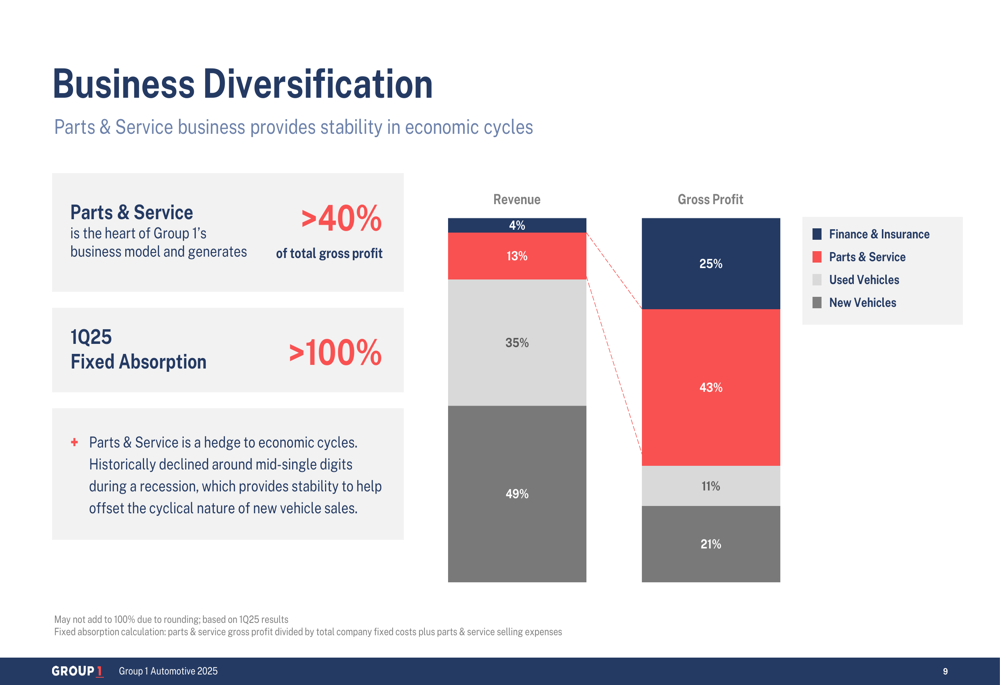

Business Model Resilience

A key strength of Group 1’s business model is the stability provided by its Parts & Service segment, which generates over 40% of total gross profit despite representing only 13% of revenue. This segment provides consistent cash flow and helps offset the cyclical nature of vehicle sales.

The company’s business diversification is clearly illustrated in the following breakdown:

Group 1 has also positioned itself well to navigate potential tariff impacts on the automotive industry. CEO Daryl Kenningham noted, "Our U.S. business performed well in the current quarter, as we continued to execute while navigating the uncertainty that has arisen from ongoing tariff and trade policy changes. We are monitoring these developments and are prepared to be operationally nimble in the face of the changing landscape."

The company’s exposure to potential tariffs is mitigated by its diversified vehicle sourcing, with 51% of new vehicle unit sales coming from US-manufactured vehicles. Group 1 has also stress-tested its business model against various macroeconomic scenarios and remains confident in its ability to maintain profitability and reasonable leverage.

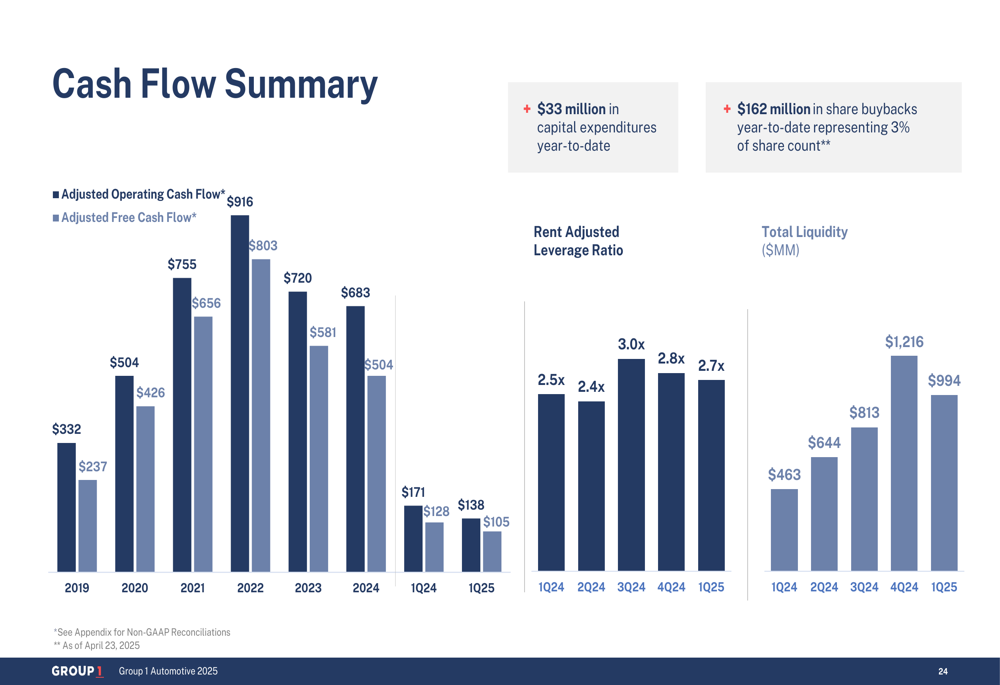

Financial Strength and Liquidity

Group 1 maintains a strong financial position with solid cash flow generation and ample liquidity. The company’s cash flow summary shows consistent performance and increasing total liquidity:

As of March 31, 2025, Group 1 had total liquidity of $1.22 billion, a significant increase from $463 million in Q1 2024. The company’s rent-adjusted leverage ratio stood at 2.7x, providing flexibility for continued strategic investments and shareholder returns.

Forward-Looking Statements

Looking ahead, Group 1 remains focused on completing its UK restructuring initiatives, which are expected to be largely finished by June 30, 2025. The company continues to monitor potential impacts from tariff and trade policy changes but believes it is well-positioned to adapt to changing market conditions.

The company’s strong earnings trajectory, with a 29% CAGR in adjusted EPS from 2019 to 2024, provides a solid foundation for future growth. Group 1’s strategic focus on portfolio optimization, Parts & Service growth, and building local scale should continue to drive long-term shareholder value.

With its diversified business model, geographic footprint, and brand portfolio, Group 1 Automotive appears well-positioned to navigate potential challenges while capitalizing on growth opportunities in both the US and UK markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.