Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Group 1 Automotive (NYSE:GPI) presented its second quarter 2025 financial results on July 24, 2025, highlighting record revenues and the successful implementation of strategic initiatives. The automotive retailer, which operates 258 dealerships across the United States and United Kingdom (TADAWUL:4280), continues to demonstrate resilience in a changing automotive landscape characterized by tariff concerns and the ongoing transition to electric vehicles.

The company’s stock has shown stability amid these industry shifts, trading at $417.35 as of July 23, 2025, within its 52-week range of $321.55 to $490.09. This performance follows a strong first quarter where GPI exceeded market expectations with adjusted EPS of $10.17 against a forecast of $9.56.

Quarterly Performance Highlights

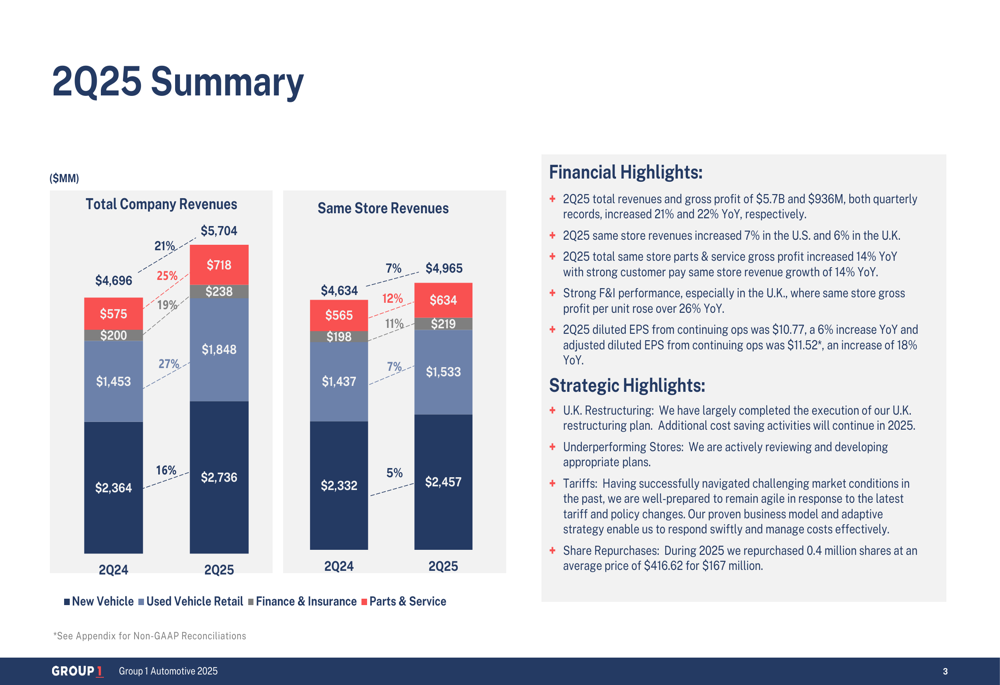

Group 1 reported record total revenues of $5,704 million for Q2 2025, representing a 21% increase compared to $4,696 million in Q2 2024. Same store revenues grew by 7% to $4,965 million. This growth was consistent across all business segments, with particularly strong performance in used vehicle retail (27% increase) and finance & insurance (25% increase).

As shown in the following chart detailing revenue growth across segments:

The company’s profitability remained strong, with diluted earnings per share from continuing operations at $10.77 and adjusted diluted EPS at $11.52. This performance builds on the company’s track record of consistent earnings growth, which has seen a 29% CAGR in EPS from 2019 to 2024.

Group 1’s U.S. operations outperformed the broader market, with same store new vehicle retail unit sales increasing by 6% year-over-year, compared to the overall U.S. market growth of 3%. Used vehicle retail unit sales grew by 4%, in line with the overall market.

Strategic Initiatives

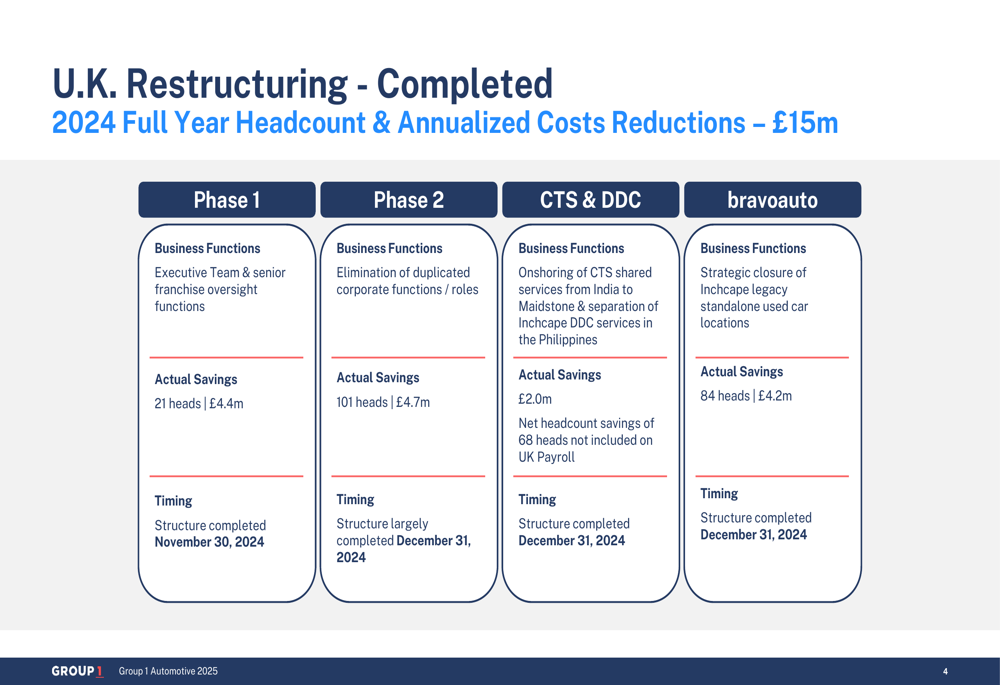

A key focus of Group 1’s presentation was its comprehensive UK restructuring plan, which has already delivered significant cost savings. The completed phases of the restructuring in 2024 resulted in £15 million in annualized cost reductions through headcount reductions and operational efficiencies.

The detailed breakdown of these completed initiatives shows:

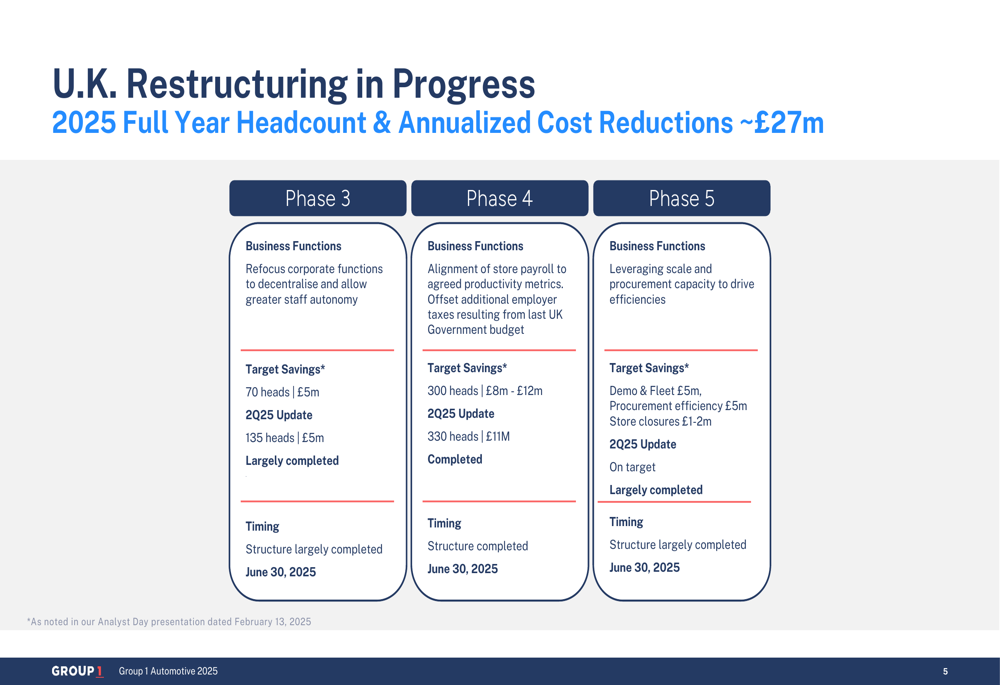

The restructuring continues in 2025, with additional phases targeting approximately £27 million in further annualized cost reductions. As of Q2 2025, the company reported being largely on target with these initiatives, which include refocusing corporate functions, aligning store payroll to productivity metrics, and leveraging scale for procurement efficiencies.

The progress on these ongoing initiatives is detailed below:

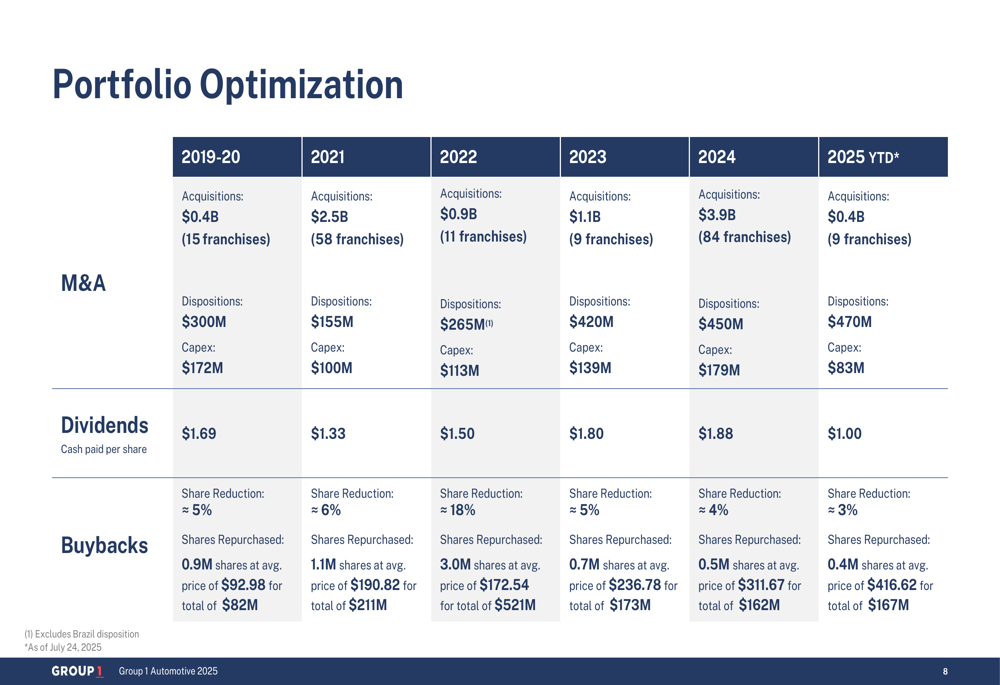

Group 1 also highlighted its portfolio optimization strategy, which balances acquisitions, dispositions, and shareholder returns. Since the beginning of 2021, the company has acquired $8.8 billion in revenues through strategic acquisitions while also disposing of smaller, less profitable stores. In 2025 year-to-date, GPI has completed acquisitions representing $0.4 billion in expected annual revenues and dispositions totaling $470 million.

The company’s acquisition and disposition activity over recent years demonstrates this balanced approach:

Business Diversification and Segment Performance

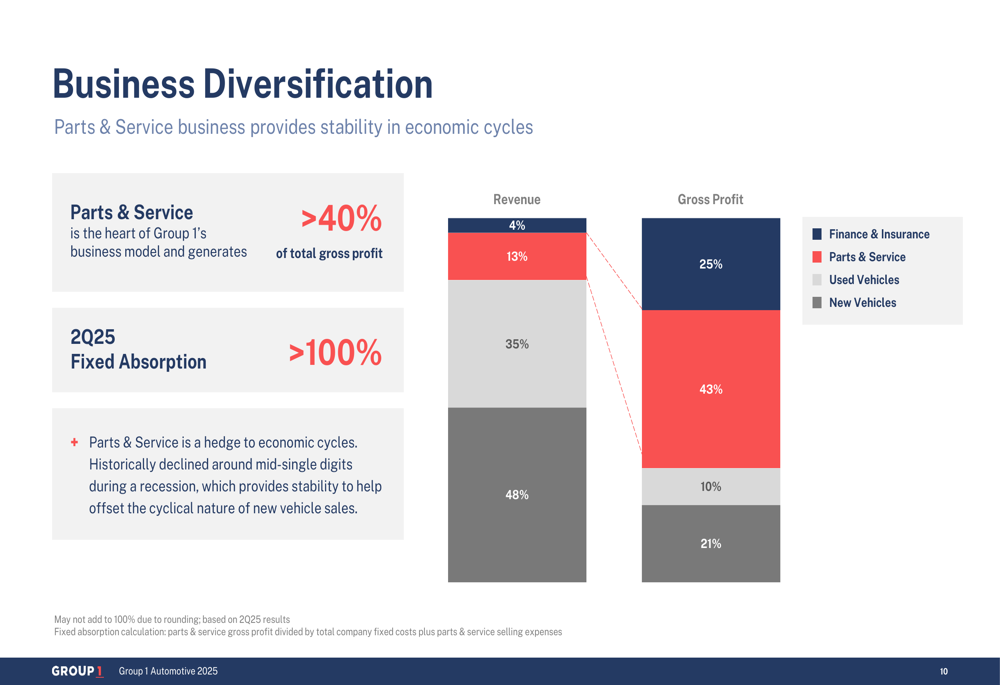

Group 1 emphasized the importance of its diversified business model in providing stability and resilience. While new vehicles represented 48% of total revenues in Q2 2025, they contributed only 21% of gross profit. In contrast, the Parts & Service segment generated 13% of revenues but accounted for 43% of gross profit, highlighting its significance as a profit center.

This diversification is illustrated in the following breakdown of revenue and gross profit mix:

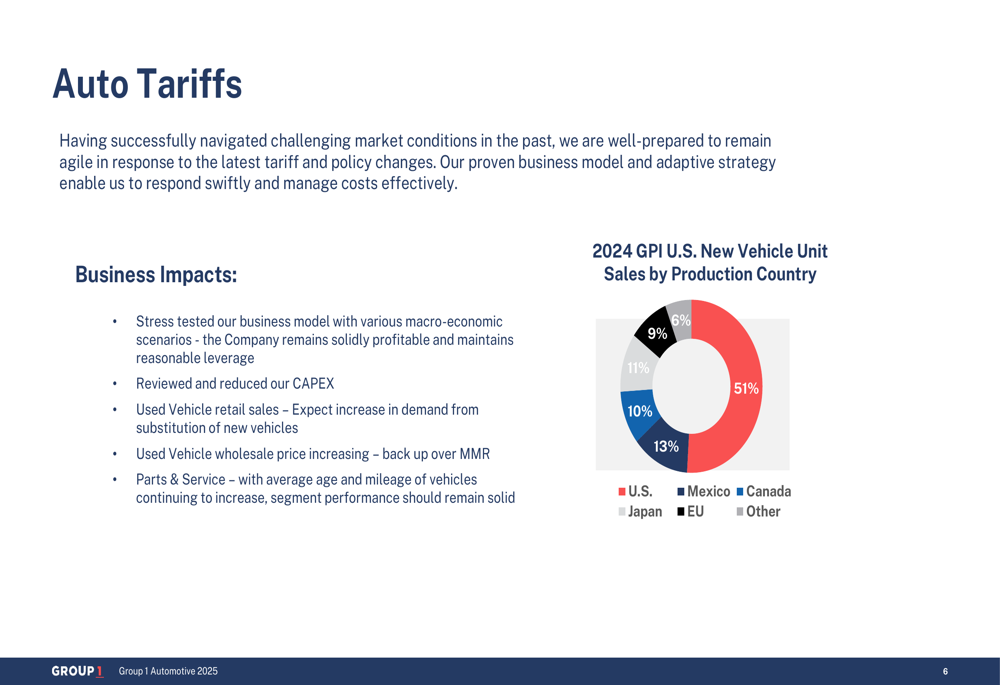

The company is also well-positioned to navigate potential challenges from auto tariffs, with 51% of its U.S. new vehicle unit sales coming from U.S.-produced vehicles. The remainder is diversified across vehicles produced in Mexico (9%), Canada (11%), Japan (10%), the EU (13%), and other countries (6%).

Group 1’s approach to potential tariff impacts includes:

The Finance & Insurance segment continues to be a strong performer, with U.S. same store F&I gross profit per retail unit increasing by 4% year-over-year in Q2 2025. The company has achieved this through optimized financing strategies with OEM partners and consolidated lender relationships, as well as growth in product penetration rates.

Forward-Looking Statements

Looking ahead, Group 1 remains focused on several strategic priorities, including completing its UK restructuring, optimizing its dealership portfolio, and continuing to grow its high-margin Parts & Service business. The company is also preparing for the ongoing transition to electric vehicles, investing in technician training and equipment for all powertrain types.

The company noted that its business model has been stress-tested and remains solidly profitable in the face of potential tariff and policy changes. Management expects increased demand for used vehicles as a substitution for new vehicles if tariffs impact pricing, and anticipates that the Parts & Service segment will remain solid due to the increasing average age and mileage of vehicles on the road.

Group 1’s strong cash flow generation continues to support its balanced capital allocation strategy. In Q2 2025 year-to-date, the company generated $267 million in adjusted free cash flow and repurchased 0.4 million shares for $167 million. This financial strength, combined with a total liquidity position of $1,112 million as of Q2 2025, provides flexibility for future strategic investments and shareholder returns.

The company’s real estate strategy also continues to evolve, with ownership of dealership locations increasing to 71% as of June 2025, up from 62% in 2019. This shift toward ownership provides greater flexibility and lower costs over the long term, with approximately $2.6 billion of gross real estate currently owned and financed through approximately $1.2 billion of mortgage debt.

Group 1 Automotive’s Q2 2025 presentation demonstrates a company executing effectively on its strategic initiatives while delivering strong financial results in a dynamic automotive retail environment. With its diversified business model, geographic footprint, and focus on operational efficiency, GPI appears well-positioned to navigate industry challenges and continue its growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.