How are energy investors positioned?

Groupe Dynamite Inc. (TSX:GRGD) shared its Q1 2025 investor presentation on June 17, highlighting strong quarterly performance and raising its full-year outlook. The company reported 20% year-over-year revenue growth and a 13% increase in comparable store sales, building on momentum from its successful fiscal 2024 results.

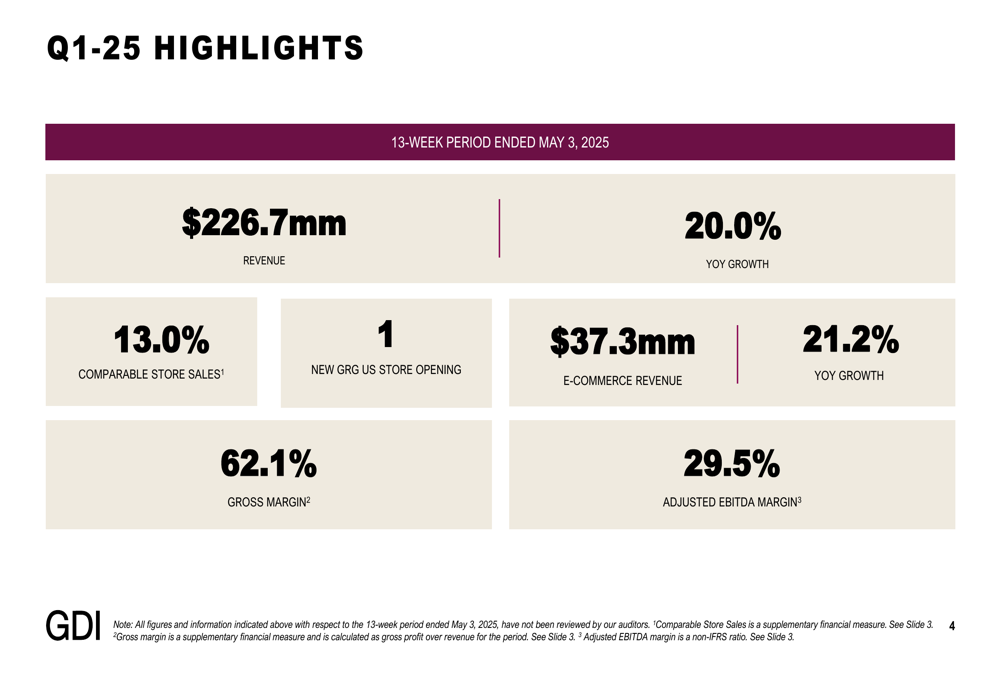

Q1-25 Performance Highlights

For the first quarter ended May 3, 2025, Groupe Dynamite delivered revenue of $226.7 million, representing 20.0% year-over-year growth. Comparable store sales increased by 13.0%, while e-commerce revenue reached $37.3 million, growing 21.2% compared to the same period last year. The company maintained strong profitability with a gross margin of 62.1% and adjusted EBITDA margin of 29.5%.

As shown in the following quarterly performance summary:

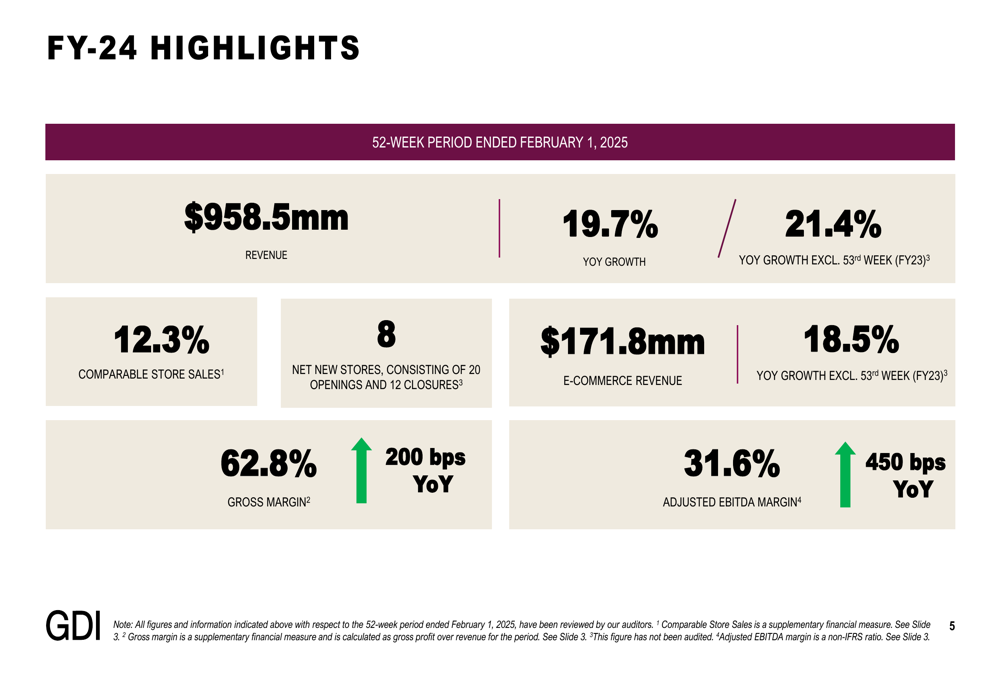

These results follow a strong fiscal 2024, which ended February 1, 2025, where the company achieved revenue of $958.5 million, representing 19.7% year-over-year growth (21.4% excluding the 53rd week in FY23). Comparable store sales for FY24 increased by 12.3%, while e-commerce revenue reached $171.8 million, growing 18.5% year-over-year excluding the 53rd week. Gross margin expanded to 62.8%, up 200 basis points, and adjusted EBITDA margin reached 31.6%, up 450 basis points from the previous year.

The company’s fiscal 2024 performance is illustrated here:

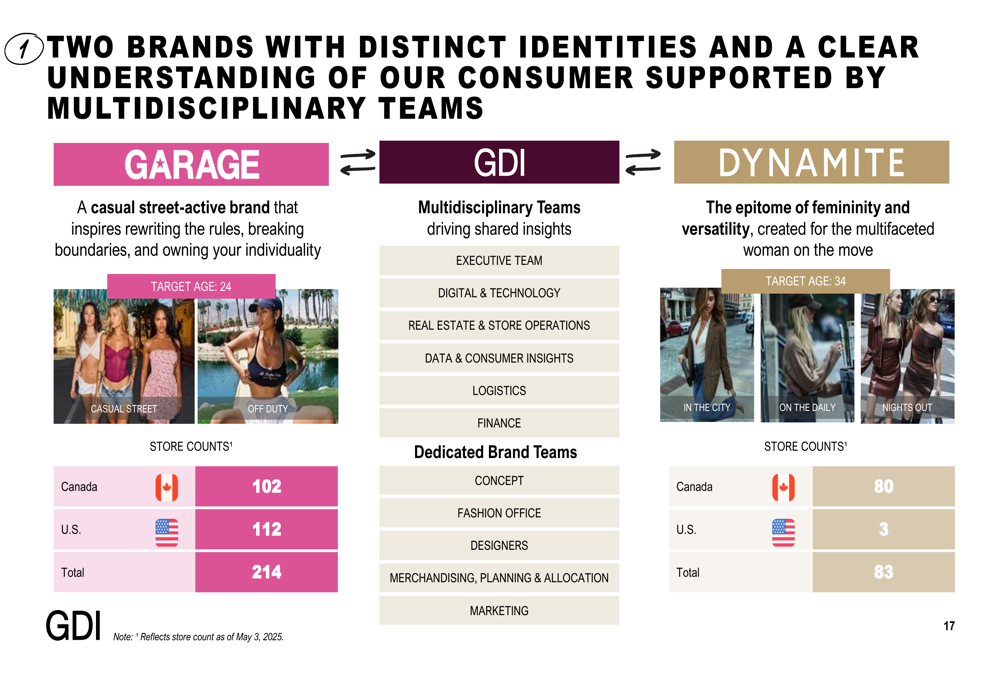

Strategic Initiatives & Growth Levers

Groupe Dynamite operates two distinct brands targeting different demographic segments: GARAGE, targeting 24-year-old women with a casual street-active aesthetic, and DYNAMITE, targeting 34-year-old women with a focus on femininity and versatility. As of May 3, 2025, GARAGE operated 102 stores in Canada and 112 in the U.S., while DYNAMITE had 80 stores in Canada and 3 in the U.S.

The company’s brand positioning and store distribution strategy is shown below:

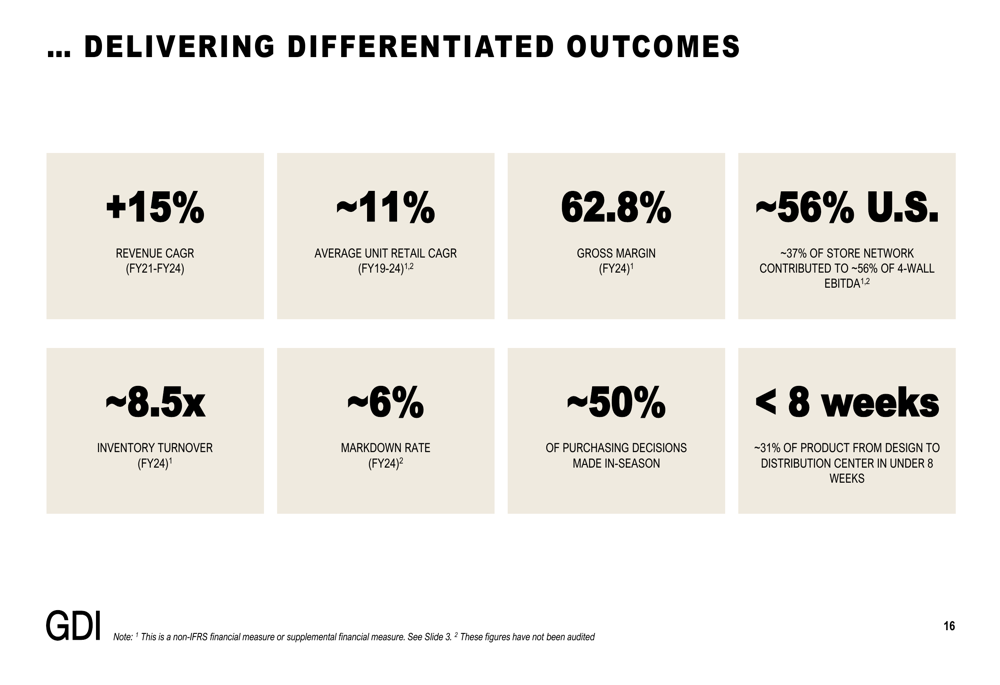

The presentation highlighted several competitive advantages driving the company’s success, including a proprietary inventory management system called "The Brain," which optimizes order fulfillment and reduces markdowns. The company’s de-risked fashion model allows approximately 50% of purchasing decisions to be made in-season, enabling quick response to emerging trends.

These strategic advantages have delivered impressive operational metrics, including an 11% compound annual growth rate in average unit retail from FY19 to FY24, approximately 8.5x inventory turnover in FY24, and a markdown rate of only about 6% in FY24.

The company’s differentiated outcomes are detailed in this slide:

Groupe Dynamite’s omnichannel strategy is showing strong results, with approximately 20% of identifiable customers shopping across both physical and digital channels, generating about 40% of revenue from identifiable customers. The company views its physical and digital channels as complementary, with stores driving brand awareness and traffic to digital platforms, while also serving as fulfillment centers for online orders.

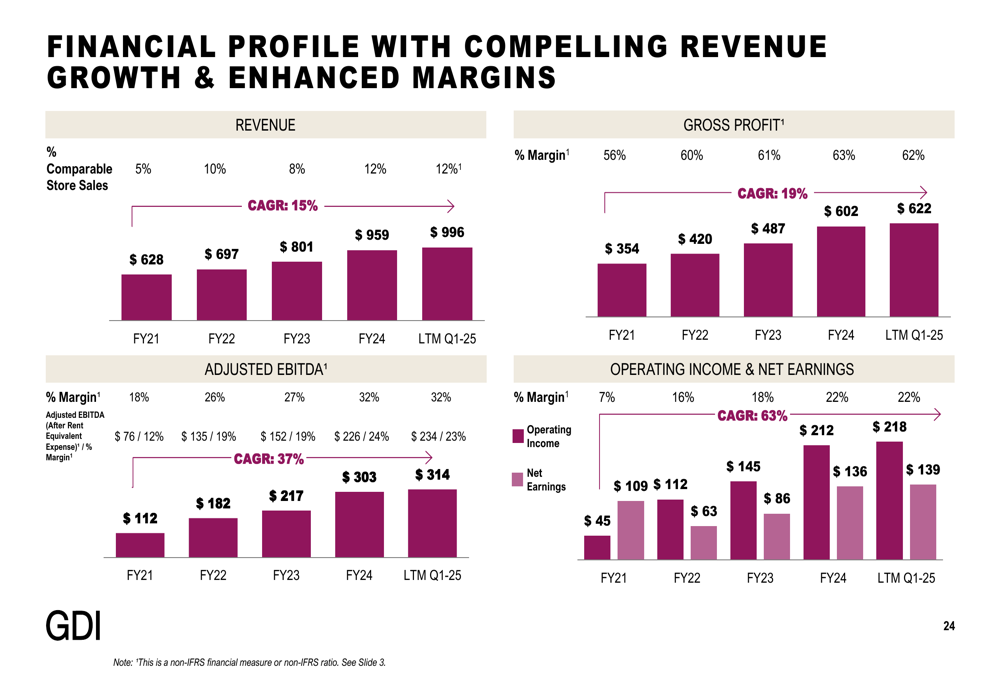

Financial Profile & Margin Expansion

The company has demonstrated consistent financial improvement over recent years, with revenue growing from $628 million in FY21 to $996 million in the last twelve months ending Q1-25. Adjusted EBITDA has shown even stronger growth, increasing from $112 million to $314 million over the same period.

The financial progression is illustrated in this chart:

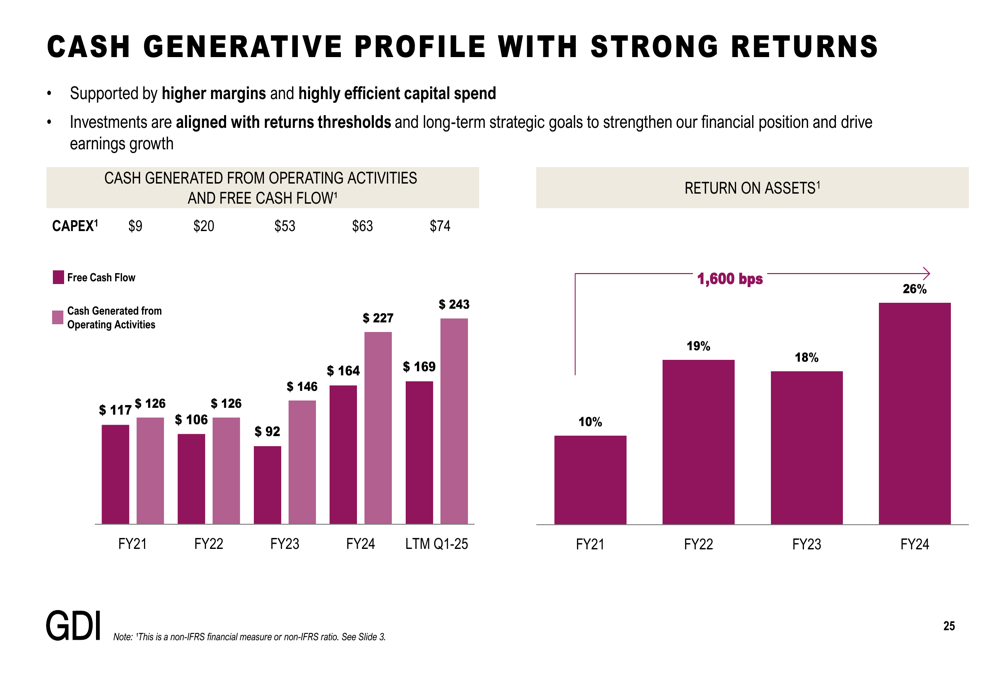

Groupe Dynamite maintains a capital-light business model with strong cash generation. The company has achieved approximately 60% free cash flow to adjusted EBITDA conversion from FY21 to FY24, and reported a 26.0% return on assets as of February 1, 2025.

The cash flow profile is shown here:

Forward-Looking Statements & Guidance

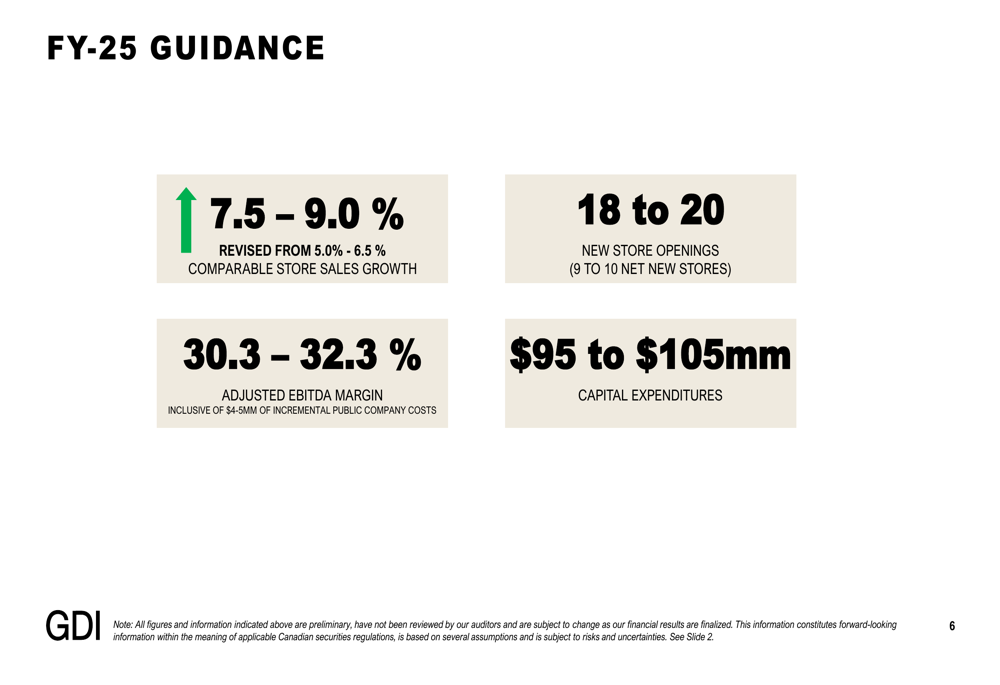

Based on strong Q1 performance, Groupe Dynamite has raised its FY25 guidance for comparable store sales growth to 7.5-9.0%, up from the previous guidance of 5.0-6.5%. The company plans to open 18 to 20 new stores (9 to 10 net new stores) during the fiscal year. Adjusted EBITDA margin is expected to be 30.3-32.3%, inclusive of $4-5 million of incremental public company costs. Capital expenditures are projected at $95 to $105 million.

The updated guidance is detailed in this slide:

Looking further ahead, Groupe Dynamite outlined ambitious growth plans, including expanding its store network to approximately 350 locations by the end of FY28 (from the current 297), growing e-commerce to approximately 25% penetration over the long term, and entering the UK market in FY26.

The company’s growth strategy is summarized here:

Groupe Dynamite’s stock closed at $16.51 on June 16, 2025, down 2.25% for the day. The stock has traded between $10.35 and $21.48 over the past 52 weeks. Following the company’s Q4 2025 earnings report in February, which exceeded expectations with EPS of $0.33 versus forecasted $0.26, the stock had seen a significant rally, though it has since pulled back from those highs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.