Asia tech stocks slide tracking Wall St losses amid AI doubts, govt. uncertainty

Introduction & Market Context

Grupa KĘTY SA (WSE:KTY) presented its first quarter 2025 results on April 23, revealing a 9% year-over-year revenue increase despite persistent challenging market conditions across Europe. The Polish aluminum products manufacturer characterized the period as a "Good Quarter in a Consistently Difficult Market," highlighting its ability to maintain growth momentum against a backdrop of weak industrial production indicators in both domestic and key export markets.

The company’s stock closed at PLN 818.5 on April 22, 2025, showing a 1.17% gain ahead of the earnings presentation. Year-to-date, the stock has traded between PLN 658.5 and PLN 918, reflecting market volatility amid uncertain economic conditions.

Quarterly Performance Highlights

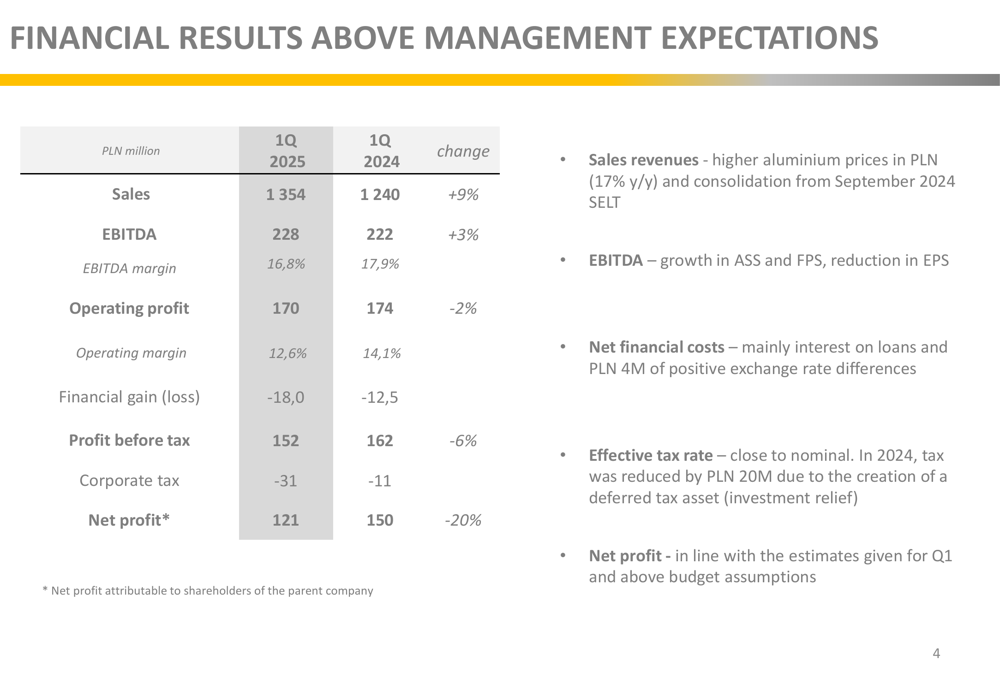

Grupa KĘTY reported Q1 2025 sales of PLN 1,354 million, a 9% increase from PLN 1,240 million in Q1 2024. EBITDA grew by 3% to PLN 228 million, though EBITDA margin contracted to 16.8% from 17.9% in the comparable period. Net profit declined 20% to PLN 121 million, primarily due to the absence of a PLN 20 million tax benefit from the creation of a deferred tax asset in the previous year.

The company noted that its Q1 performance exceeded budget assumptions, with sales growth driven by higher aluminum prices in PLN terms (up 17% year-over-year) and the consolidation of SELT, acquired in September 2024.

As shown in the following comprehensive financial results table:

Segment Analysis

The company’s performance varied across its three main business segments, with each facing different market dynamics:

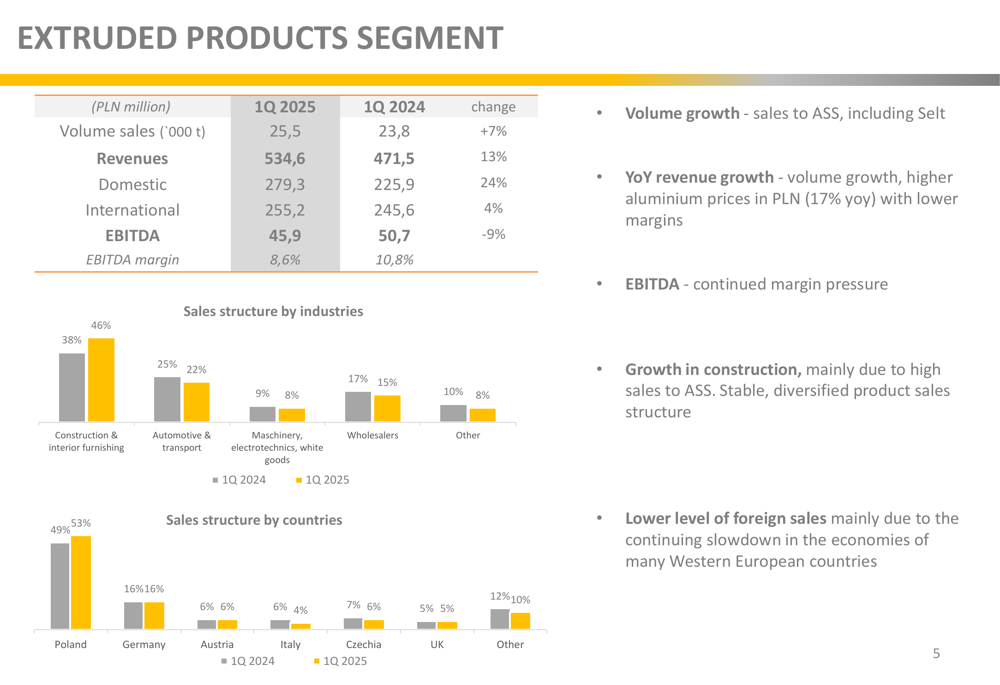

Extruded Products Segment

The Extruded Products Segment reported a 7% increase in volume sales to 25,500 tons and a 13% revenue increase to PLN 534.6 million. However, EBITDA declined 9% to PLN 45.9 million, with margin falling to 8.6% from 10.8% in Q1 2024. Domestic sales grew significantly (+24%), while international sales increased modestly (+4%), reflecting the continued slowdown in Western European economies.

The segment’s performance details are illustrated in the following chart:

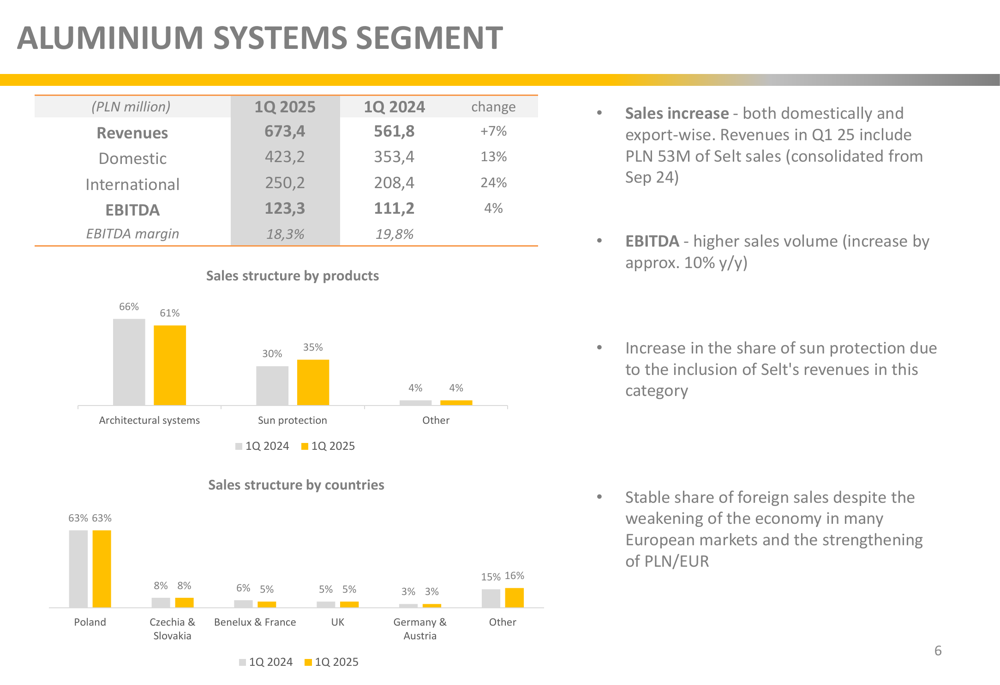

Aluminium Systems Segment

The Aluminium Systems Segment delivered strong results with revenues increasing to PLN 673.4 million (+7% year-over-year) and EBITDA growing to PLN 123.3 million (+4%). The segment’s performance was boosted by the inclusion of PLN 53 million in sales from SELT, which was consolidated from September 2024. Sales volume increased by approximately 10% year-over-year, though EBITDA margin slightly decreased to 18.3% from 19.8%.

The segment maintained a stable share of foreign sales despite economic weakening in many European markets and the strengthening of the PLN/EUR exchange rate, as shown in the following breakdown:

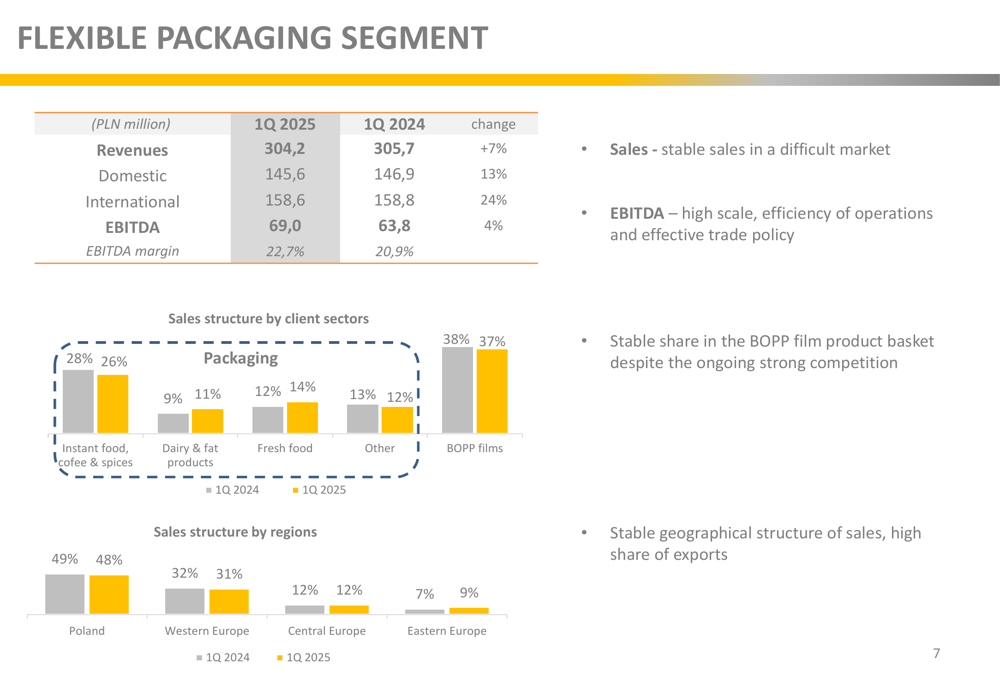

Flexible Packaging (NYSE:PKG) Segment

The Flexible Packaging Segment demonstrated resilience with stable revenues of PLN 304.2 million (-0.5% year-over-year) and improved profitability, with EBITDA increasing 8.2% to PLN 69.0 million. The segment achieved an impressive EBITDA margin of 22.7%, up from 20.9% in Q1 2024, attributed to operational efficiency and effective trade policy despite ongoing strong competition in the BOPP film market.

Financial Position & Investment

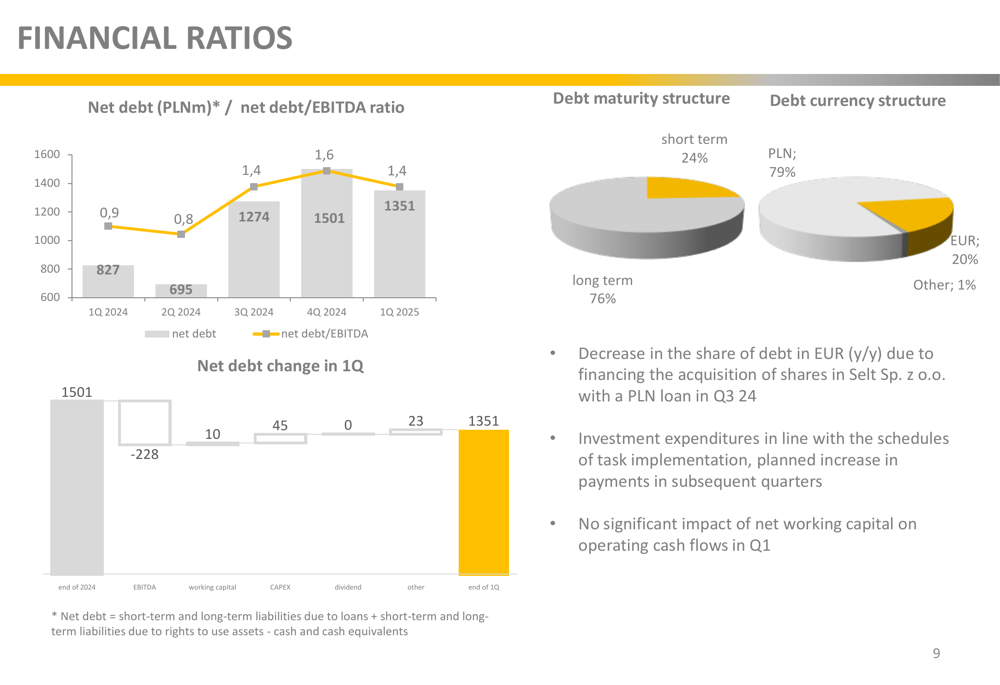

Grupa KĘTY reduced its net debt to PLN 1,351 million at the end of Q1 2025, down from PLN 1,501 million at the end of 2024. The company’s debt structure remains predominantly long-term (76%) and PLN-denominated (79%), with a decreased share of EUR debt following the SELT acquisition financing.

Capital expenditures in Q1 2025 totaled PLN 45 million, representing 13% of the annual investment forecast. The CAPEX was distributed across segments, with PLN 24 million allocated to the Extruded Products Segment, PLN 14 million to the Aluminium Systems Segment, and PLN 6 million to the Flexible Packaging Segment.

The following chart illustrates the company’s net debt trends and debt structure:

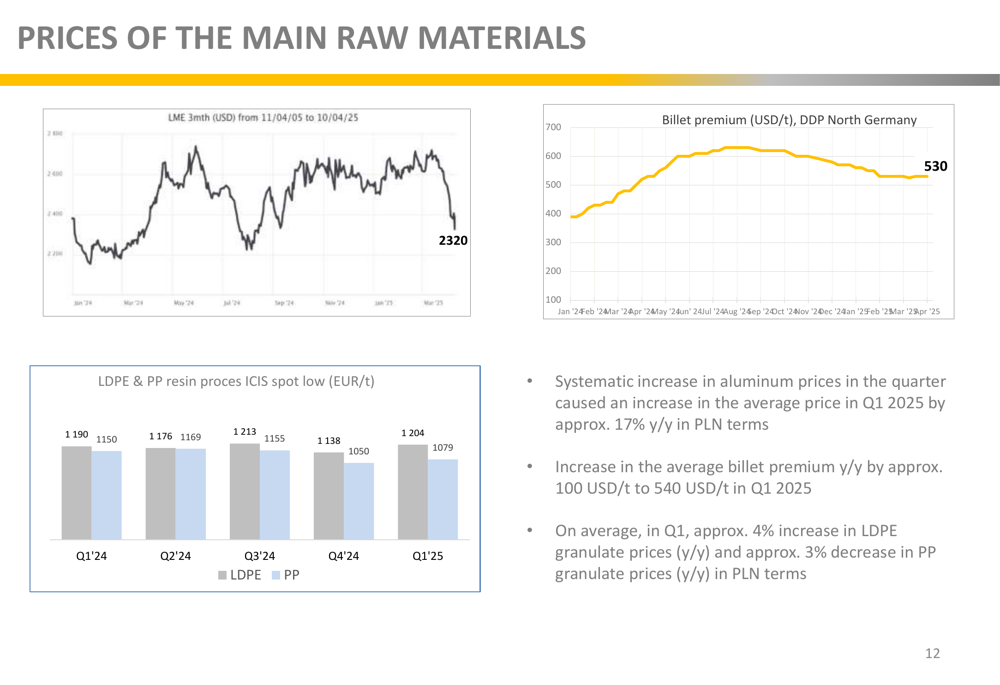

Raw material prices significantly impacted the company’s performance, with aluminum prices increasing systematically throughout the quarter, resulting in an average price increase of approximately 17% year-over-year in PLN terms. The billet premium also increased by approximately 100 USD/t year-over-year to 540 USD/t in Q1 2025.

The company has recommended a dividend of PLN 48.78 per share, reflecting its commitment to shareholder returns despite challenging market conditions.

Outlook & Strategy

Looking ahead to Q2 2025, Grupa KĘTY expects no significant changes in market conditions, while acknowledging uncertainty about the impact of higher tariffs on various sectors of the European economy. The company noted significant price fluctuations of some commodities in response to US tariff actions.

Operationally, the company plans to maintain high production capacity utilization while continuing the integration of SELT. It is also beginning implementation of its new strategy for 2025-2029, though specific details were not elaborated in the presentation.

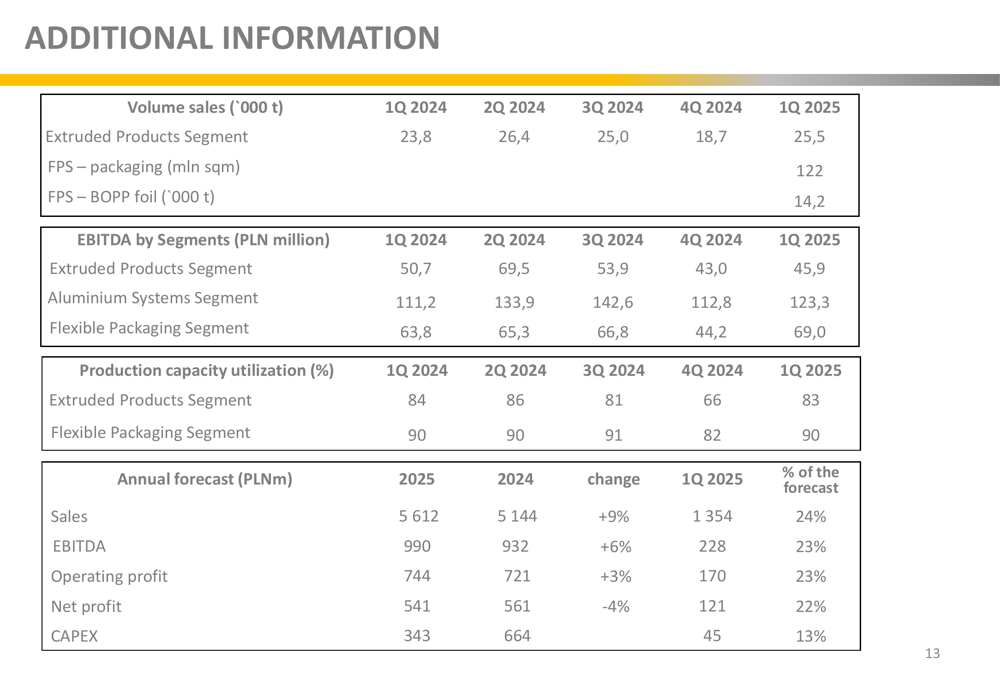

The company’s volume sales data and annual forecast provide additional context for its operational outlook:

Despite the challenging market environment, Grupa KĘTY’s Q1 2025 results demonstrate its ability to generate revenue growth and maintain relatively stable margins through operational efficiency and strategic acquisitions. However, the company faces ongoing headwinds from weak industrial production in key markets and potential disruptions from changing trade policies.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.