U.S. stocks lower as investors rotate out of tech ahead of Jackson Hole

Introduction & Market Context

Grupa KĘTY SA (WSE:KTY) reported strong second-quarter results on July 31, 2025, with revenue growing 11% year-over-year despite mixed economic indicators across its key markets. The company’s stock rose 0.44% to 904.5 PLN following the presentation, continuing its upward trajectory from the 900.5 PLN closing price the previous day.

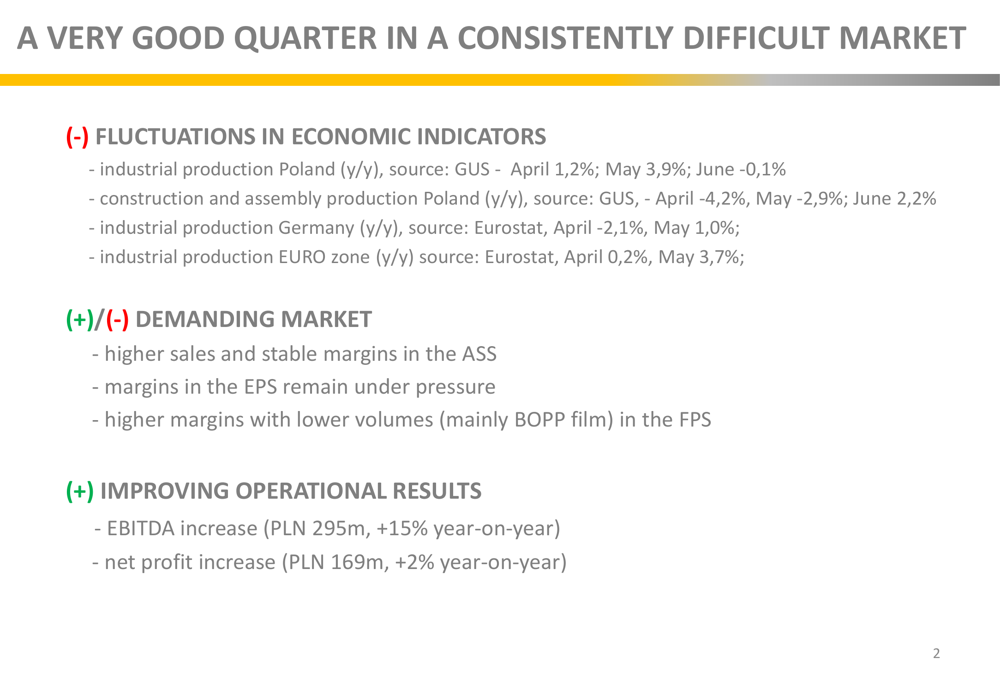

The Polish aluminum processing leader delivered these results against a backdrop of fluctuating industrial production in Poland, Germany, and the broader Eurozone. While industrial production in Poland showed volatility (April +1.2%, May +3.9%, June -0.1%), construction and assembly production demonstrated improvement toward the end of the quarter (April -4.2%, May -2.9%, June +2.2%).

As shown in the following economic indicators overview:

Quarterly Performance Highlights

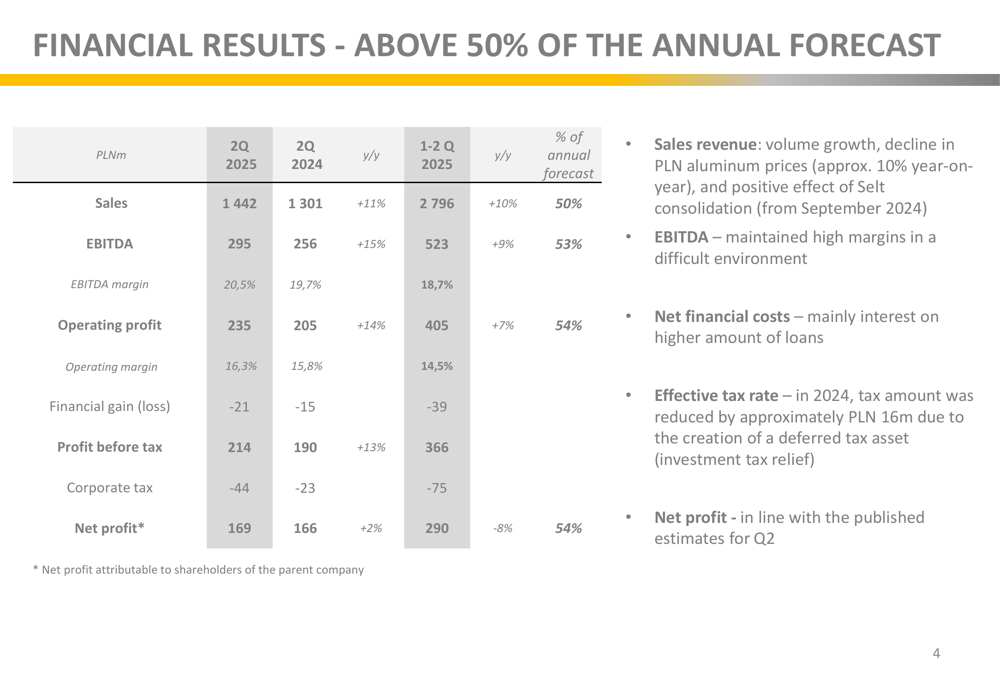

Grupa KĘTY achieved consolidated sales of 1,442 million PLN in Q2 2025, representing an 11% increase year-over-year. More impressively, EBITDA grew 15% to 295 million PLN, maintaining a strong 20.5% margin. Net profit increased by 2% to 169 million PLN, with growth limited by higher financial costs related to increased debt levels.

For the first half of 2025, the company reported sales of 2,796 million PLN (+10% y/y) and EBITDA of 523 million PLN (+9% y/y). The company has already achieved over 50% of its annual forecast in the first six months of the year, positioning it well to meet or exceed full-year targets.

The detailed financial results show volume growth across segments, with the Selt acquisition contributing significantly to revenue:

Segment Analysis

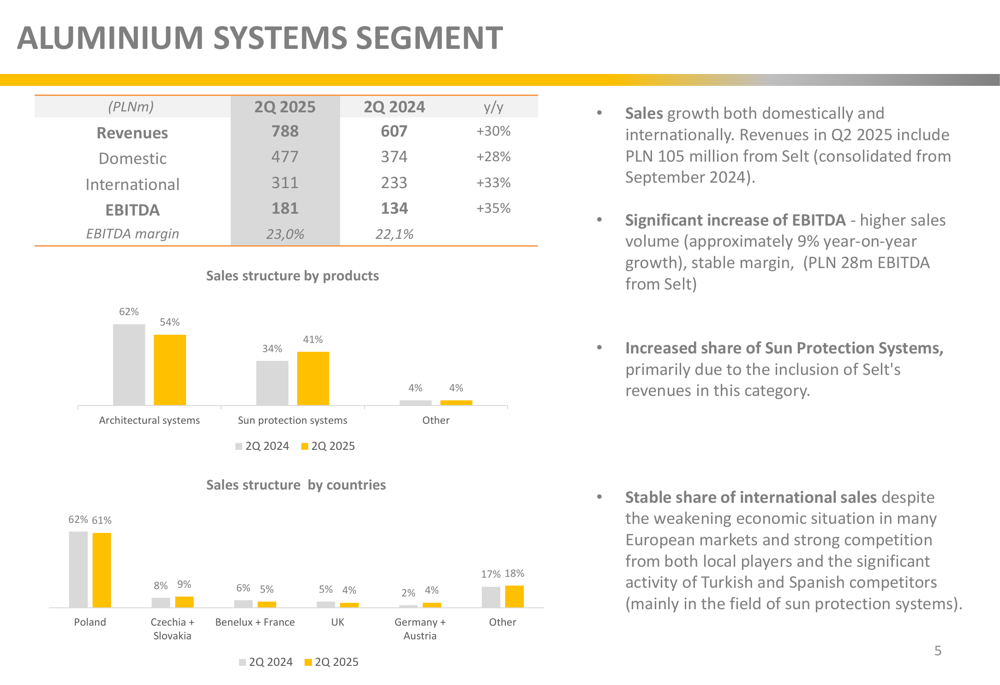

The Aluminium Systems Segment (ASS) was the standout performer, with revenues surging 30% year-over-year to 788 million PLN in Q2 2025. This growth was driven by both domestic (+28%) and international (+33%) sales, with the recently acquired Selt contributing 105 million PLN. The segment’s EBITDA jumped 35% to 181 million PLN, achieving an impressive 23.0% margin.

The segment’s product mix has evolved, with sun protection systems gaining share following the Selt acquisition:

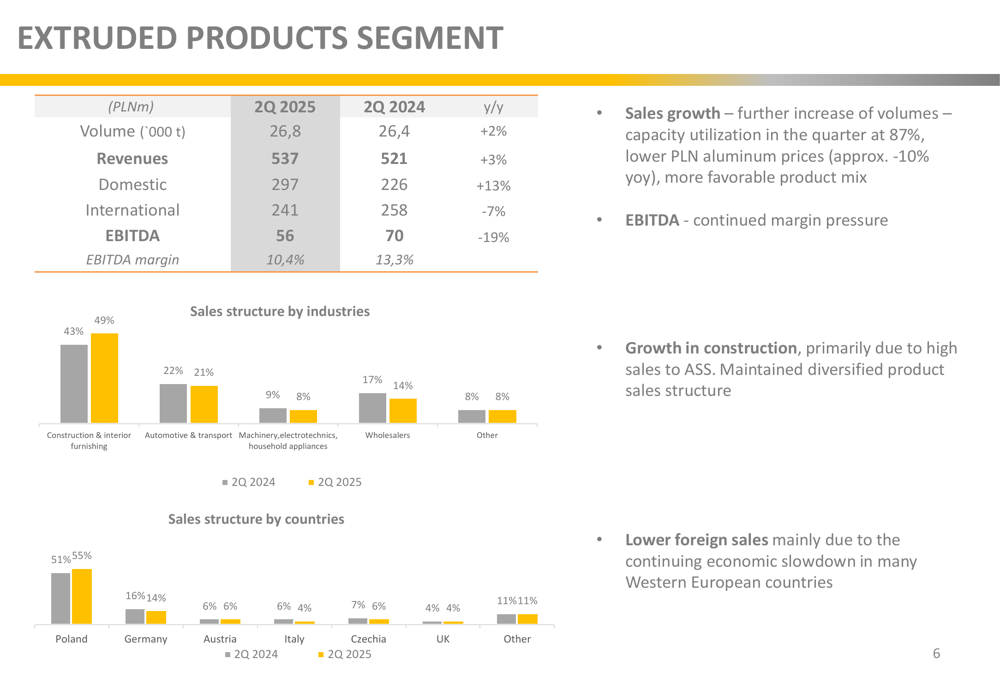

The Extruded Products Segment showed more modest growth, with revenues increasing 3% to 537 million PLN despite a 2% volume increase. While domestic sales grew 13%, international sales declined by 7%. More concerning was the 19% drop in EBITDA to 56 million PLN, reducing the segment’s margin to 10.4% as it continued to face pricing pressure.

The segment’s sales structure shows growth in construction applications but weakness in international markets:

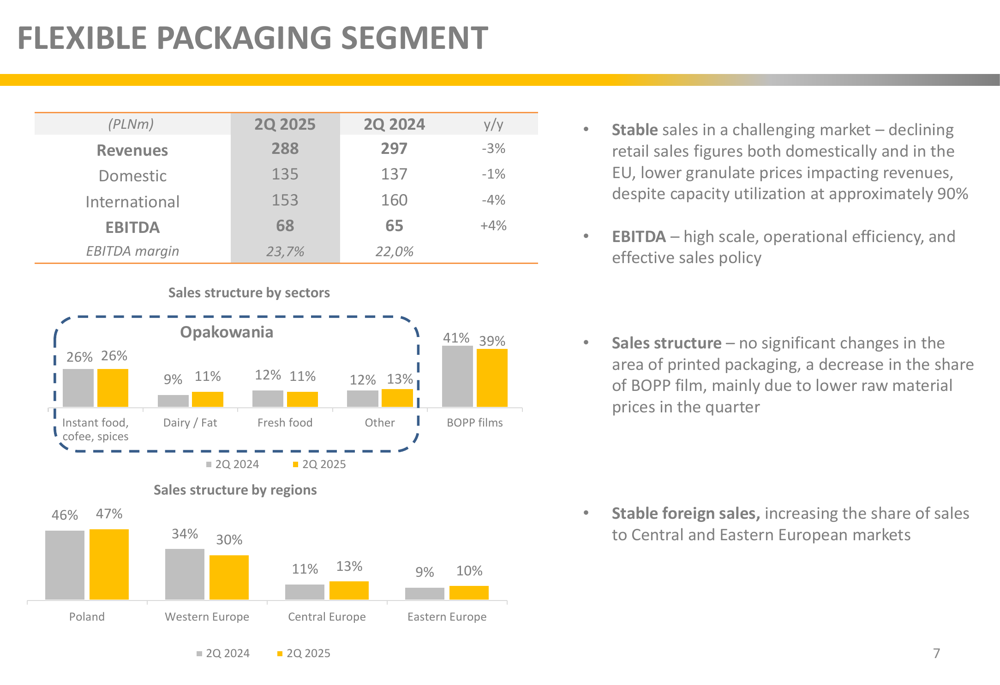

The Flexible Packaging (NYSE:PKG) Segment demonstrated resilience despite challenging market conditions. While revenues declined slightly by 3% to 288 million PLN, EBITDA increased by 4% to 68 million PLN, improving margins to an impressive 23.7%. The segment maintained stable sales in printed packaging while experiencing some weakness in BOPP films.

Strategic Initiatives & Investments

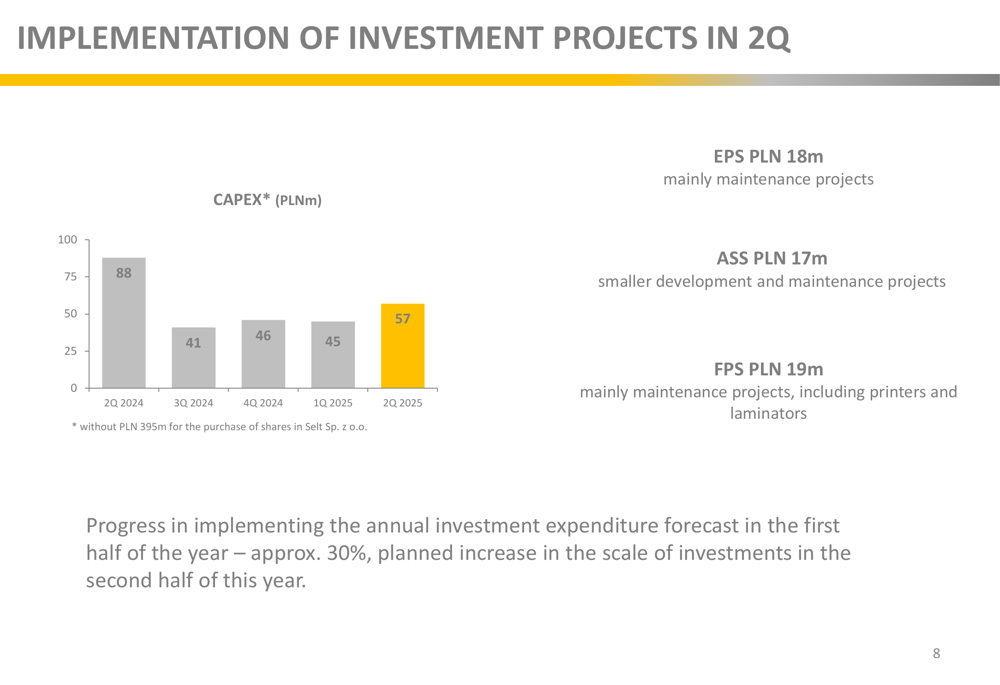

Capital expenditures reached 57 million PLN in Q2 2025, up from 45 million PLN in Q1 but below the 88 million PLN invested in Q2 2024. The company has completed approximately 30% of its planned annual investments in the first half of the year, with increased investment activity expected in the second half.

The CAPEX distribution was relatively balanced across segments, with 18 million PLN in Extruded Products, 17 million PLN in Aluminium Systems, and 19 million PLN in Flexible Packaging, primarily for maintenance projects.

The following chart illustrates the quarterly CAPEX trend:

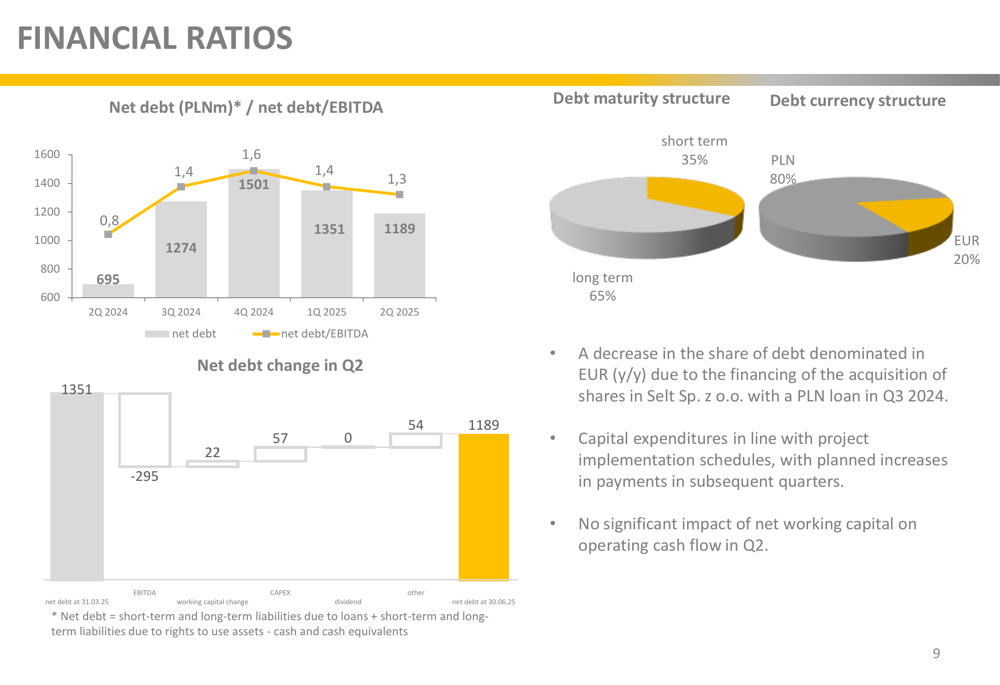

The company’s financial position remains solid, with net debt under control despite recent acquisitions. The debt structure has shifted toward more PLN-denominated debt (80%) versus EUR (20%), primarily due to the financing of the Selt acquisition with a PLN loan. The debt maturity profile shows a healthy balance between short-term (35%) and long-term (65%) obligations.

As illustrated in the following debt structure overview:

Forward-Looking Statements

Looking ahead to Q3 2025, Grupa KĘTY expects stable market conditions with no significant changes in the economic environment. The company anticipates continued fluctuations in commodity prices but expects to maintain high production capacity utilization across segments.

On the financial front, the company has paid the first dividend tranche of 16.70 PLN per share, in line with its commitment to shareholder returns. This continues the trend highlighted in the Q1 earnings call, where management emphasized maintaining an 85% profit dividend policy with projected 6-7% dividend yields.

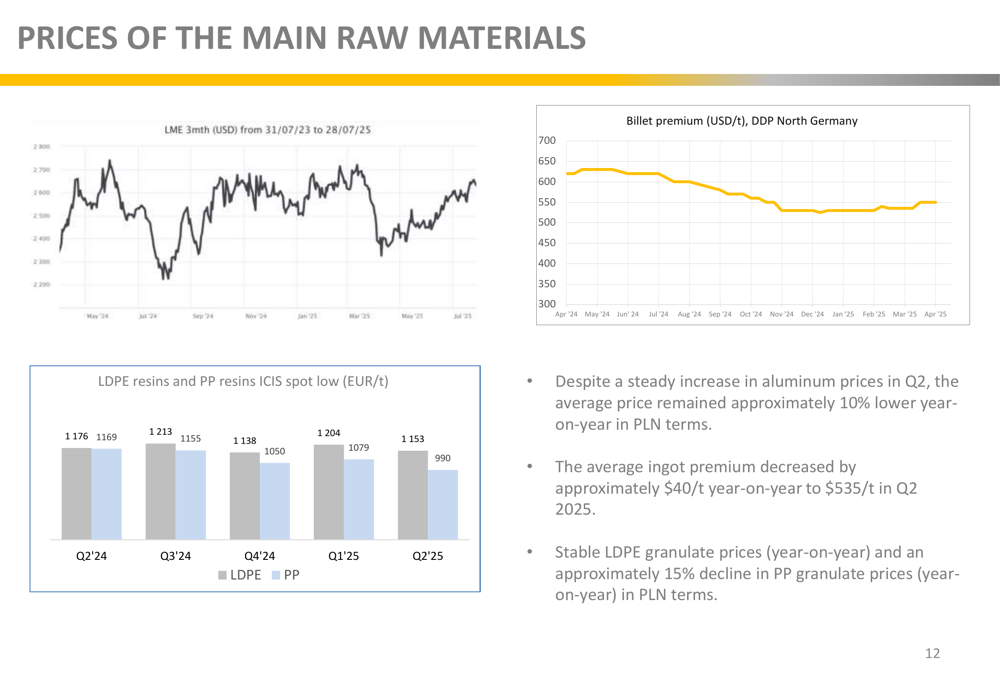

The raw materials outlook shows some stabilization after earlier volatility. Despite steady increases in aluminum prices during Q2, average prices remained approximately 10% lower year-on-year in PLN terms. Similarly, the average ingot premium decreased by approximately $40/t year-on-year to $535/t in Q2 2025, while polymer prices showed mixed trends with stable LDPE prices and declining PP prices.

The following chart illustrates key raw material price trends:

Grupa KĘTY’s Q2 2025 results demonstrate continued execution of the strategy outlined in previous communications, including the goal of transitioning to a leading European player in aluminum processing. The company’s focus on export growth is evident in the strong international performance of the Aluminium Systems Segment, aligning with the previously stated goal of increasing export sales from 50% to nearly 55%.

With half of 2025 now complete, the company appears well-positioned to achieve its annual targets while continuing to navigate market volatility through operational excellence and strategic acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.