Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

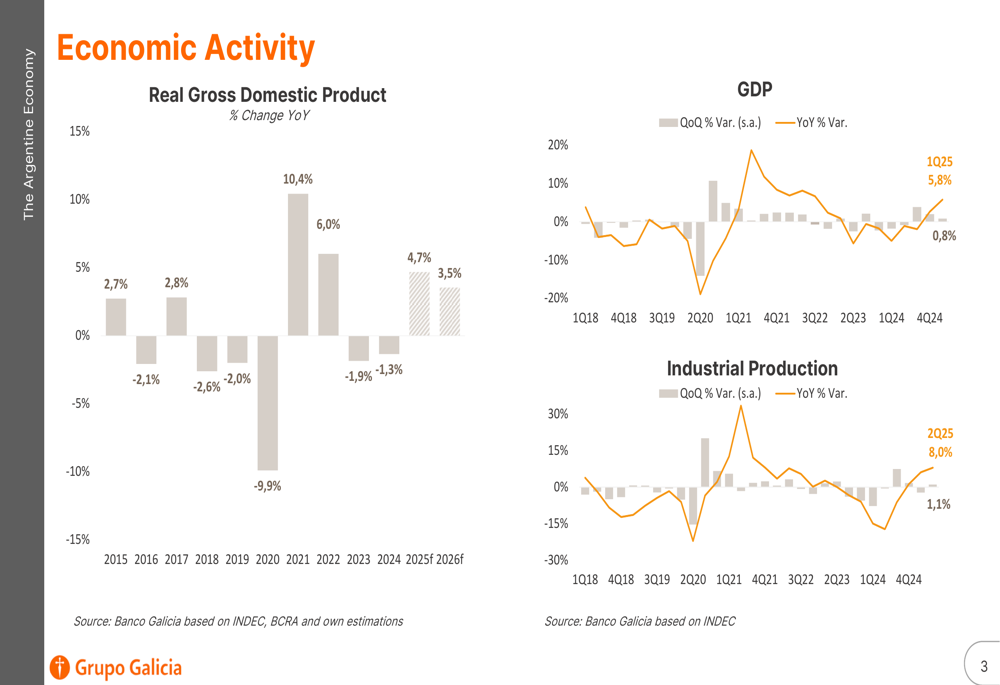

Grupo Financiero Galicia (NASDAQ:GGAL) presented its Q2 2025 investor slides on August 27, 2025, showcasing the company’s performance against the backdrop of Argentina’s ongoing economic recovery. The presentation highlighted how the financial group is navigating the improving but still challenging Argentine economic environment, where GDP growth has rebounded to 4.7% in 2024 and is projected to stabilize at 3.5% for 2025-2026.

As shown in the following chart of Argentina’s economic activity, the country is experiencing a significant recovery after several years of contraction, providing a more favorable operating environment for financial institutions:

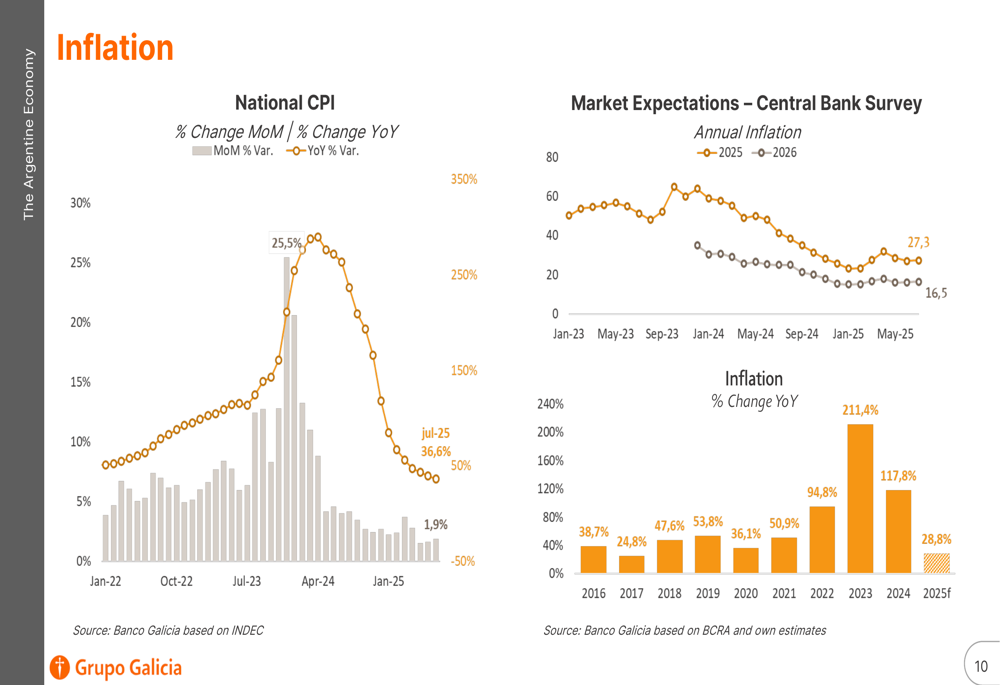

A key macroeconomic factor influencing the banking sector has been Argentina’s declining inflation rate, which has fallen dramatically from 211.4% in 2023 to a projected 28.8% in 2025. This disinflationary trend has created a more stable environment for financial planning and credit expansion.

As illustrated in the following inflation data, market expectations from the Central Bank survey indicate continued improvement in the inflation outlook:

Quarterly Performance Highlights

Grupo Financiero Galicia reported a return on equity (ROE) of 9.5% for Q2 2025 and 9.1% for the full fiscal year 2025, with a return on assets (ROA) of 1.9% and 1.8% respectively. The company maintained a solid financial margin of 20.9% in Q2 and demonstrated strong operational efficiency at 43.1%.

The following summary highlights the group’s key financial metrics:

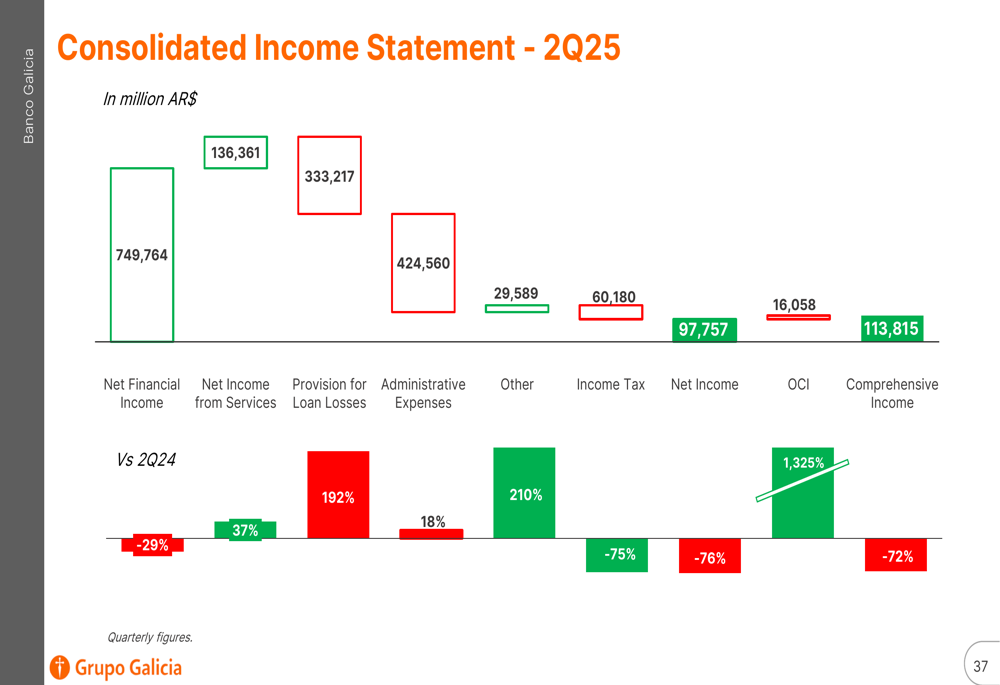

Despite these positive metrics presented in the slides, it’s worth noting that according to recent earnings reports, Grupo Financiero Galicia’s net income actually dropped 70% year-over-year, even as its earnings per share of 107.48 dramatically exceeded forecasts of 1.13. This discrepancy suggests potential one-time accounting factors at play that weren’t fully addressed in the presentation.

The company’s consolidated income statement for Q2 2025 shows a remarkable 1,325% increase in comprehensive income compared to Q2 2024:

Business Unit Performance

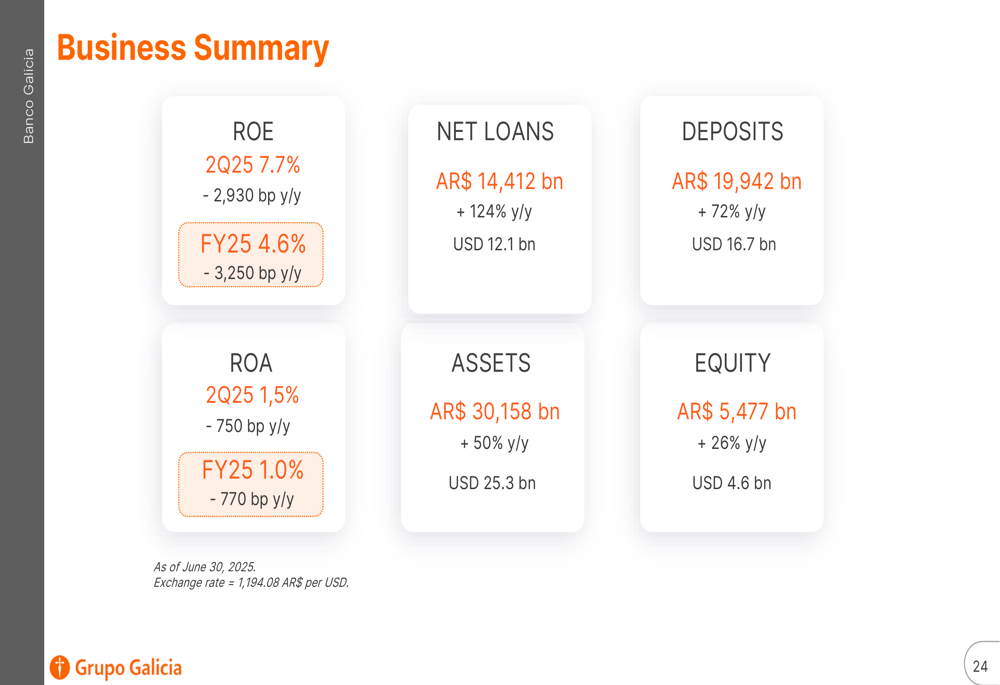

Banco Galicia, the group’s main banking operation, reported an ROE of 7.7% for Q2 2025 and 4.6% for the full fiscal year. With assets of AR$ 30,158 billion (USD 25.3 billion) and a loan portfolio of AR$ 14,412 billion (USD 12.1 billion), the bank maintains a strong position in the Argentine financial system.

The following business summary provides a comprehensive overview of Banco Galicia’s key metrics:

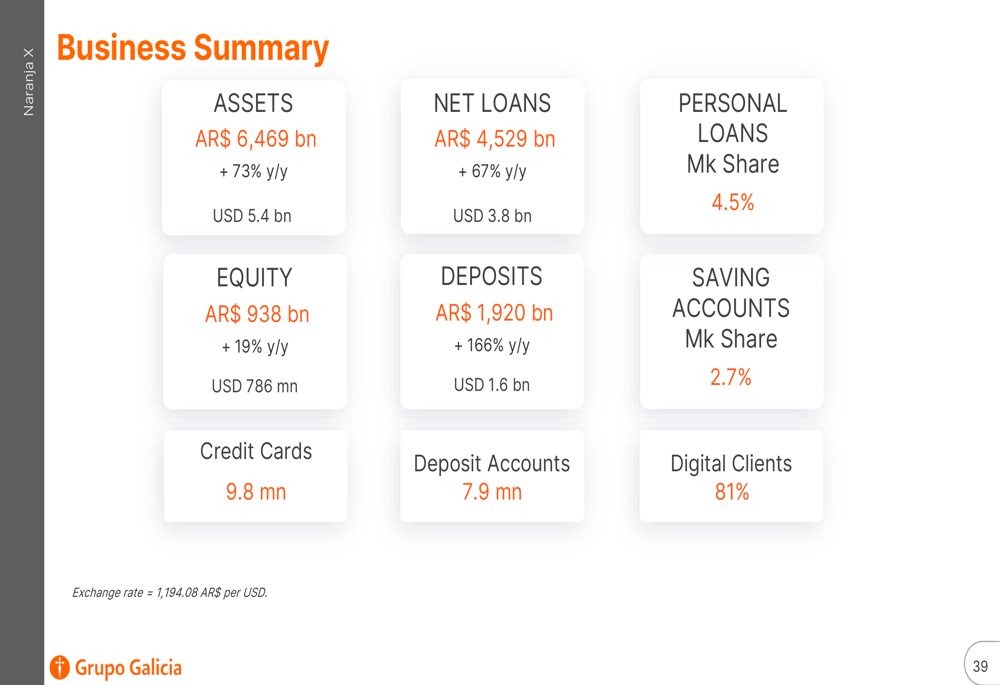

Naranja X, the group’s fintech and consumer finance arm, has emerged as a significant growth driver with an impressive ROE of 13.8% for Q2 2025 and a projected 21.6% for the full fiscal year. With 9.8 million credit cards and 7.9 million deposit accounts, Naranja X has established itself as a major player in Argentina’s digital banking space, with 81% of its clients using digital channels.

As shown in the following business summary, Naranja X contributes significantly to the group’s diversified revenue streams:

Strategic Positioning

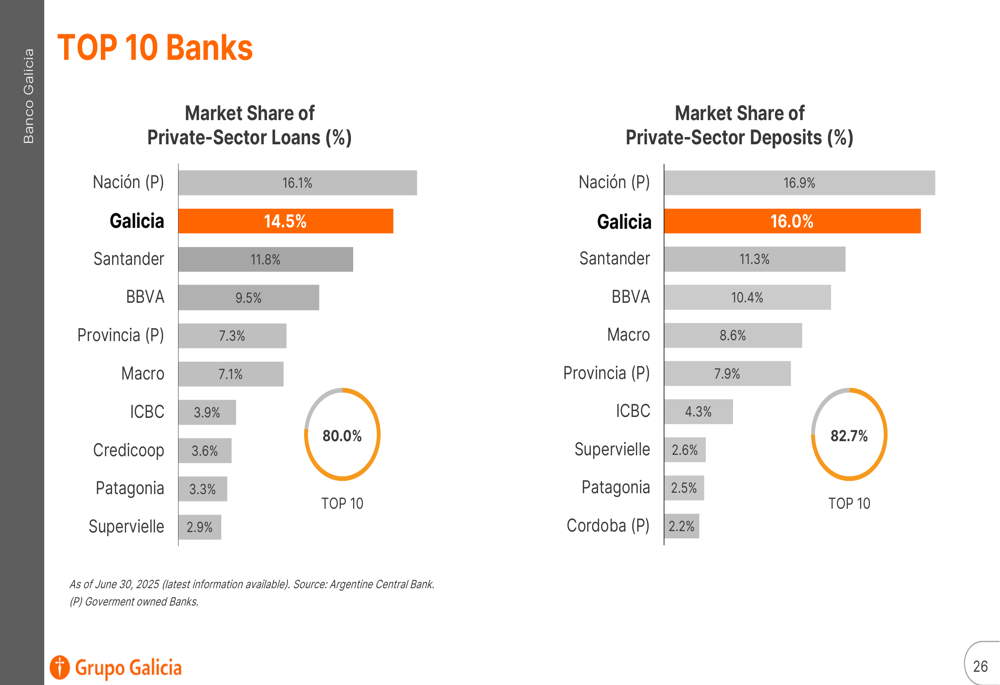

Grupo Financiero Galicia maintains a strong competitive position in the Argentine banking sector, holding a 14.5% market share in loans and 16.0% in deposits. This places the bank among the top institutions in the country, competing closely with Santander and Banco Macro.

The following chart illustrates Galicia’s market position relative to its main competitors:

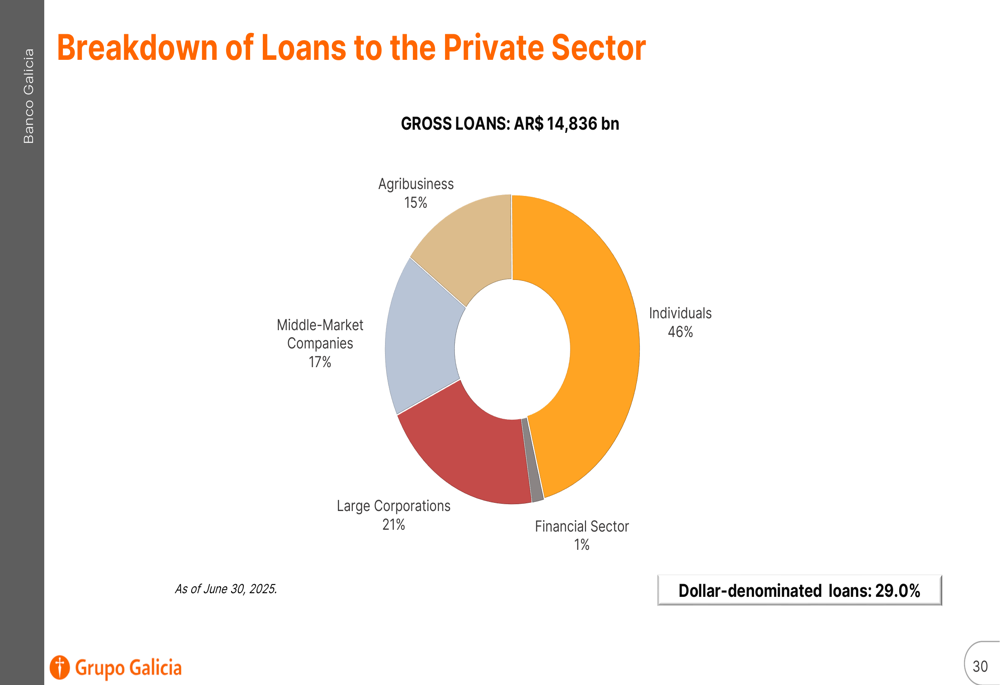

The group’s loan portfolio is well-diversified across various sectors, with 46% allocated to individuals, 21% to large corporations, 17% to middle-market companies, 15% to agribusiness, and 1% to the financial sector. Additionally, 29% of the loan portfolio is denominated in US dollars, providing some hedge against currency fluctuations.

Forward-Looking Statements

Looking ahead, Grupo Financiero Galicia projects continued growth and profitability improvement. According to the earnings call, the company expects a return on equity of 9-11% for 2025, with loan growth of 30-40% and deposit growth of approximately 35%.

The integration of Galicia Mas (formerly HSBC Argentina) is expected to contribute to further market share gains, though restructuring costs may temporarily impact profitability. The company anticipates non-performing loans to stabilize by the end of Q3 or early Q4 2025.

Despite the strong operational metrics presented in the slides, investors appear cautious, with the stock trading at $39.79 as of August 29, 2025, near its 52-week low of $38.39. This suggests ongoing market concerns about Argentina’s economic stability and potential challenges in the financial sector, despite the improving macroeconomic indicators highlighted in the presentation.

The company’s ability to maintain its market leadership position while navigating Argentina’s economic recovery will be crucial for its performance in the coming quarters, particularly as inflation continues to moderate and credit demand potentially increases.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.