LIVE UPDATES: Fed Chair Jerome Powell to deliver major speech at Jackson Hole

Introduction & Market Context

Grupo Supervielle SA (NYSE:SUPV) presented its first quarter 2025 results on May 28, revealing a strategic shift toward higher-yielding retail loans amid Argentina’s challenging macroeconomic environment. The Argentine bank reported mixed results, with strong loan and deposit growth contrasting with declining profitability metrics. Grupo Supervielle’s stock closed down 6.31% at $14.71 on the reporting day, suggesting investors remain cautious despite the company’s growth narrative.

The bank is navigating what it describes as a "transitional macro environment" characterized by precautionary consumer behavior, heightened FX volatility, and limited peso liquidity. However, management highlighted several supportive structural conditions, including Argentina’s fiscal surplus, lifted FX restrictions, decelerating inflation, and strengthened foreign exchange reserves.

Quarterly Performance Highlights

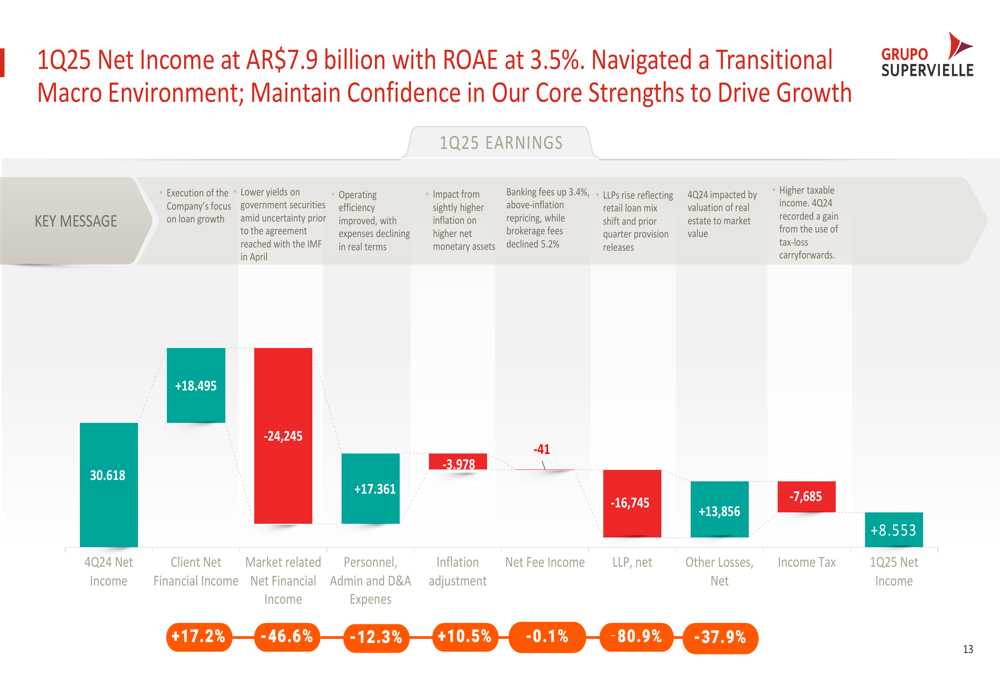

Grupo Supervielle reported net income of Ps.8.5 billion for Q1 2025, a significant decrease from Ps.30.6 billion in the previous quarter. The company achieved a return on equity (ROE) of 4% in real terms, while maintaining solid capital ratios with a CET1 ratio of 15.3%.

As shown in the following detailed earnings analysis, several factors contributed to the quarter-over-quarter decline in net income:

The bank’s client net financial income increased by 17% quarter-over-quarter, while operating expenses decreased by 12% QoQ and 17% year-over-year, reflecting ongoing efficiency initiatives. However, these positive developments were offset by a Ps.24.2 billion decrease in market-related net financial income and a Ps.16.7 billion increase in loan loss provisions.

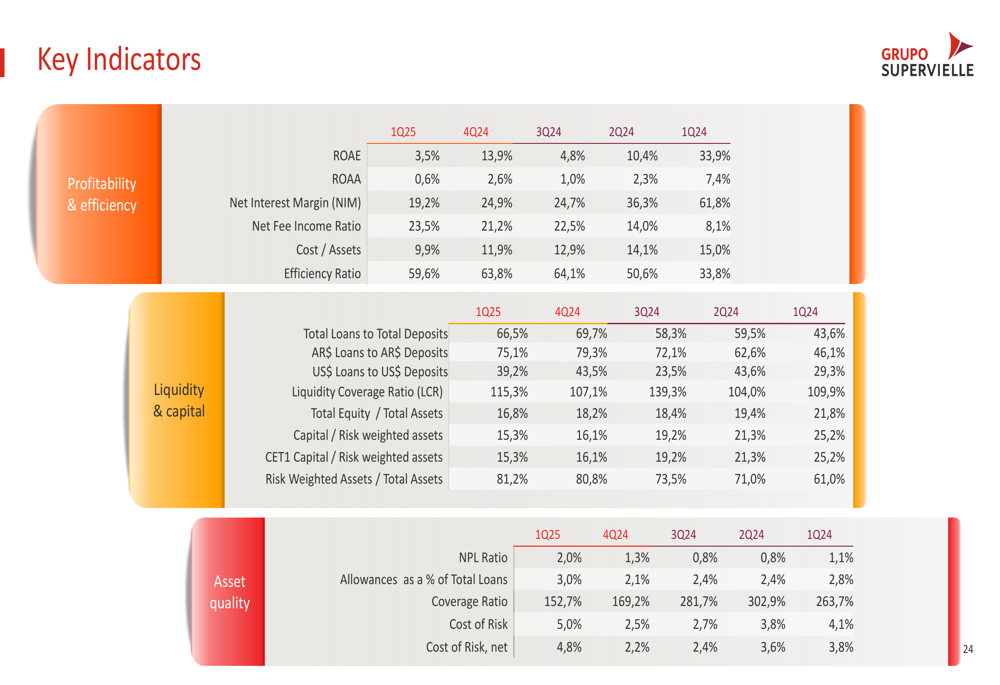

Key performance indicators show a mixed picture across profitability, efficiency, liquidity, and asset quality:

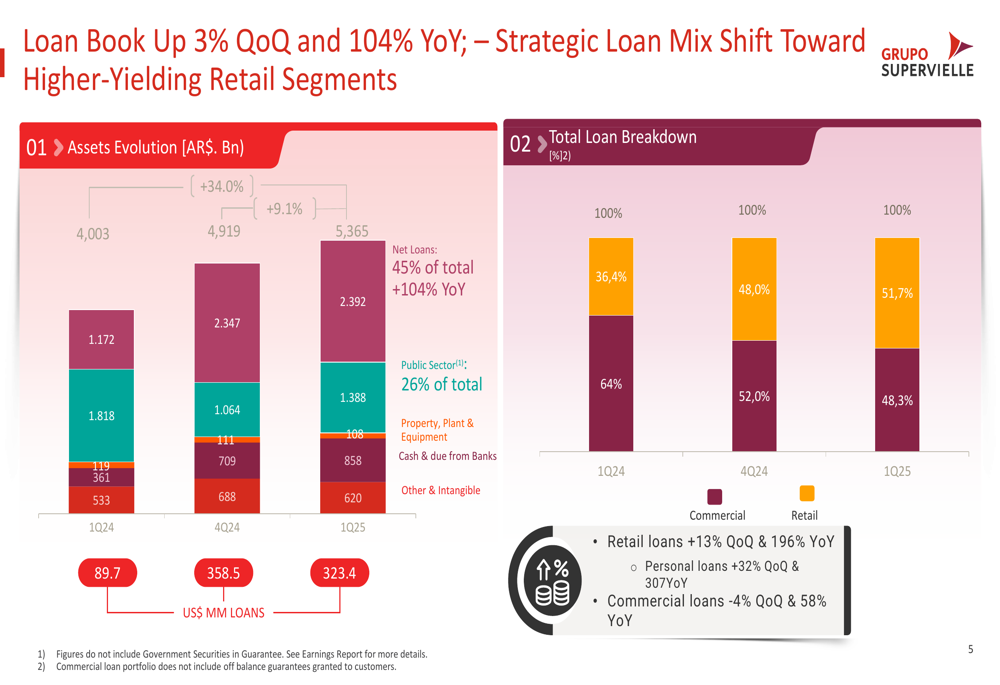

Loan Portfolio Transformation

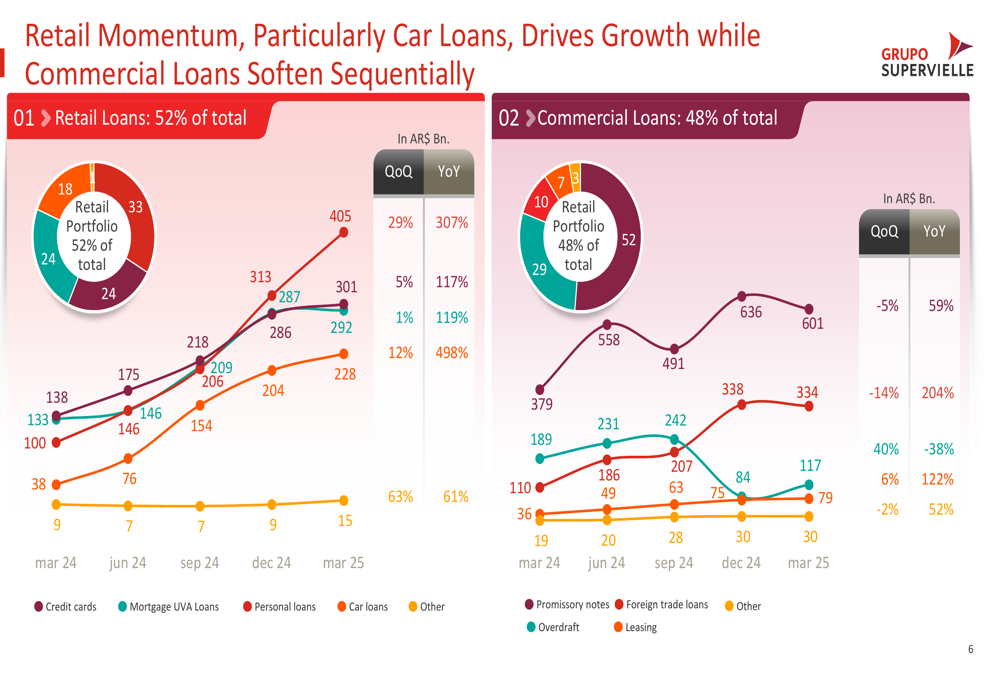

A central element of Grupo Supervielle’s strategy is the ongoing transformation of its loan portfolio, with a decisive shift toward higher-yielding retail segments. The loan book increased by 3% quarter-over-quarter and 104% year-over-year, with retail loans growing by 13% QoQ and now representing 52% of the total loan portfolio, up from 48% in Q4 2024.

The following chart illustrates this strategic pivot from commercial to retail lending:

Breaking down the retail loan growth, personal loans showed particularly strong momentum with a 32% increase quarter-over-quarter and 307% year-over-year. The bank has strategically focused on payroll lending, with 53% of loans to individuals going to payroll and pension clients, and 88% of personal loans granted to payroll customers.

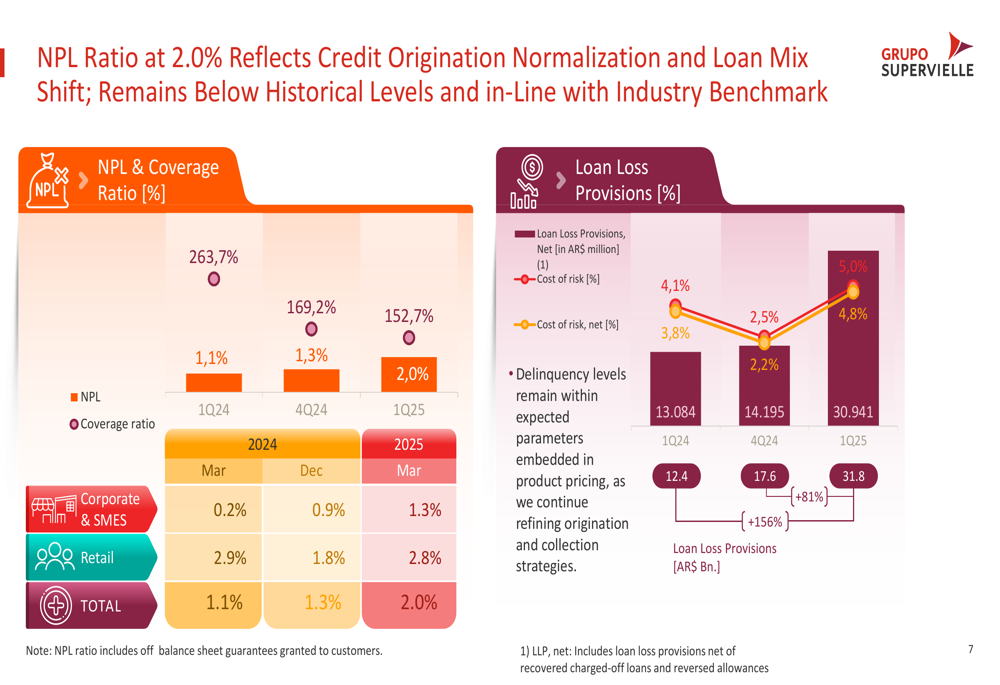

Despite the rapid loan growth, asset quality has remained relatively stable. The non-performing loan (NPL) ratio stands at 2.0%, which the company describes as "consistent with credit normalization and within expected levels." The coverage ratio remains robust at 153%, providing a cushion against potential loan losses.

Deposit Growth and Funding

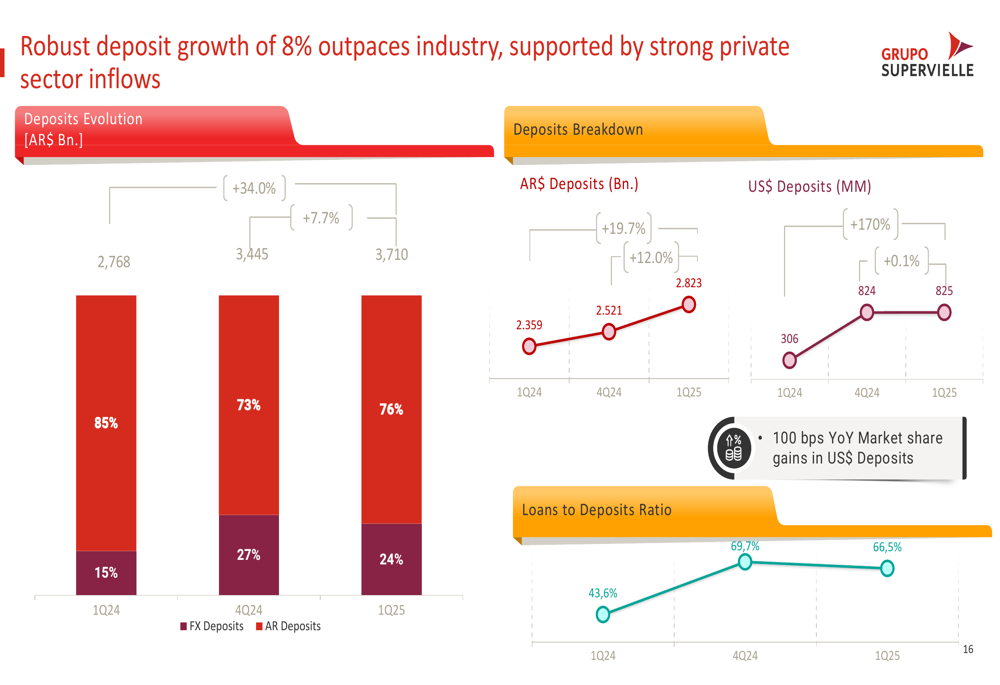

Grupo Supervielle reported strong deposit growth, with its total deposit base increasing by 8% quarter-over-quarter. Argentine peso deposits grew by 12% QoQ, while US dollar deposits reached record levels, up 170% year-over-year, outpacing industry growth. The bank gained 100 basis points in market share year-over-year and 30 basis points quarter-over-quarter.

The following chart shows the evolution of the bank’s deposit base:

The growth in US dollar deposits is particularly noteworthy, increasing from $306 million in Q1 2024 to $825 million in Q1 2025. This shift in deposit composition reflects changing customer preferences in Argentina’s volatile currency environment and provides the bank with more stable funding sources.

Profitability Challenges

Despite the growth in loans and deposits, Grupo Supervielle faces profitability challenges. The bank’s net interest margin (NIM) has declined, with the Argentine peso interest spread decreasing from approximately 123% in Q1 2024 to below 40% in Q1 2025, reflecting the country’s declining interest rate environment.

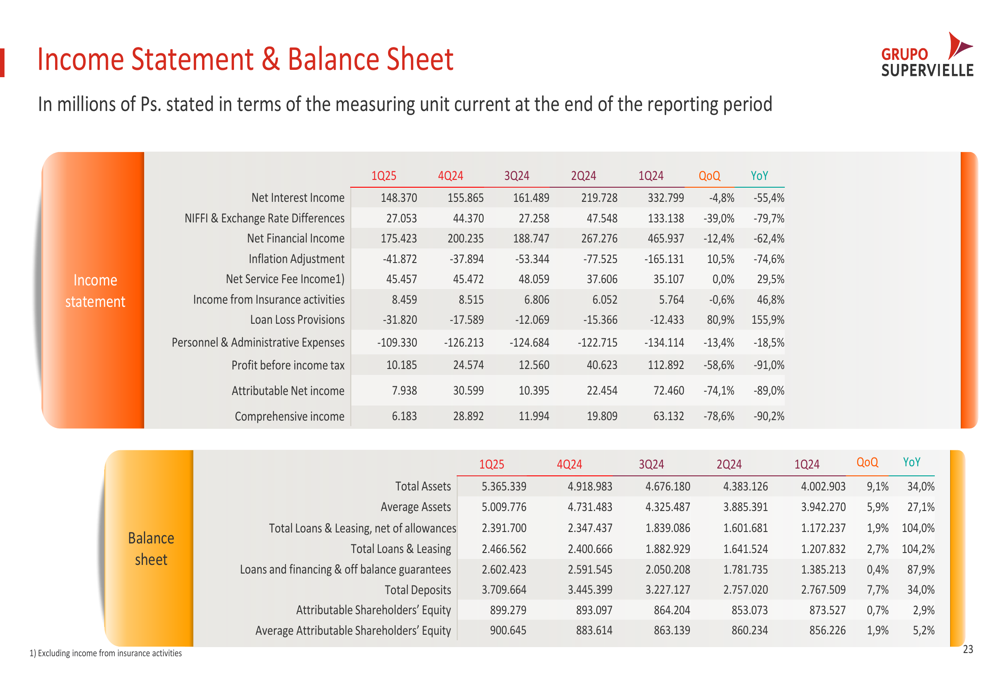

The company’s return on average equity (ROAE) and return on average assets (ROAA) have both shown a steady decline through Q1 2025. Profit before income tax decreased from Ps.112.9 billion to Ps.10.2 billion, while attributable net income fell from Ps.72.5 billion to Ps.7.9 billion.

The income statement and balance sheet highlights provide a comprehensive overview of the bank’s financial performance:

Forward-Looking Statements

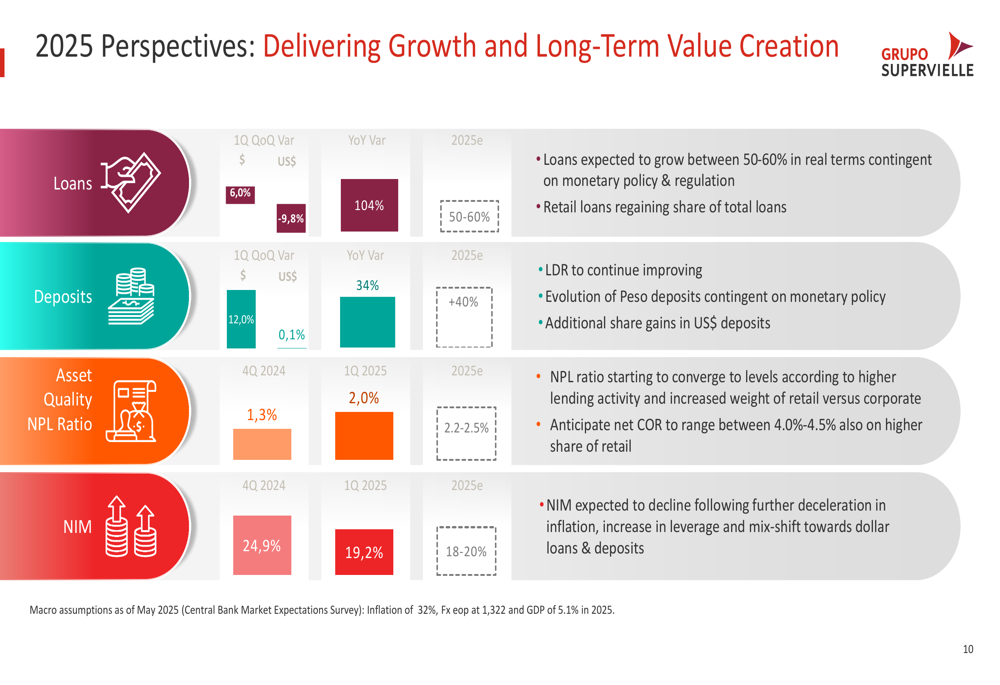

Looking ahead to the remainder of 2025, Grupo Supervielle provided guidance on several key metrics. The bank expects loans to grow between 50-60% in real terms, with deposits projected to increase by more than 40%. The NPL ratio is anticipated to range between 2.2-2.5%, while the net interest margin is expected to be between 18-20%.

The bank also expects to see improvements in fee income, with bank net fees projected to grow on higher income and lower expenses, while asset management fees are anticipated to follow growth in assets under management. Operating expenses are expected to continue declining in real terms, reflecting efficiencies in headcount and other areas.

Management anticipates that return on average equity will improve gradually quarter-over-quarter as the loan portfolio and leverage increase, combined with cost reductions and fee income growth. The bank’s risk-weighted assets are expected to increase following loan growth and regulatory changes implemented in Q1 2025.

Grupo Supervielle is also focusing on innovation initiatives to deepen customer engagement and accelerate growth, including a new remunerated account, an official online store hosted on Mercado Libre, AI-powered interactions via WhatsApp, and investment transactions through the bank’s app.

As Argentina’s economic stabilization continues, Grupo Supervielle appears positioned to benefit from its strategic shift toward higher-yielding retail loans and strong deposit growth, though investors will be watching closely for signs of improvement in the bank’s profitability metrics in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.