Can anything shut down the Gold rally?

Introduction & Market Context

Gaztransport et Technigaz SA (EN:GTT (EPA:GTT)) reported strong financial results for the first half of 2025, with significant growth in both revenue and profitability. The company, which specializes in containment systems for liquefied natural gas (LNG) transportation and storage, presented its H1 2025 results on July 30, 2025. Despite the positive results, GTT ’s stock closed down 0.69% at €159.6 on the day of the announcement.

The company’s performance comes amid a complex geopolitical landscape for LNG, with both tailwinds (strengthened US LNG momentum after the end of DoE permit freeze) and headwinds (geopolitical tensions and US tariffs). Nevertheless, GTT has capitalized on strong long-term market fundamentals to deliver impressive growth.

Financial Performance Highlights

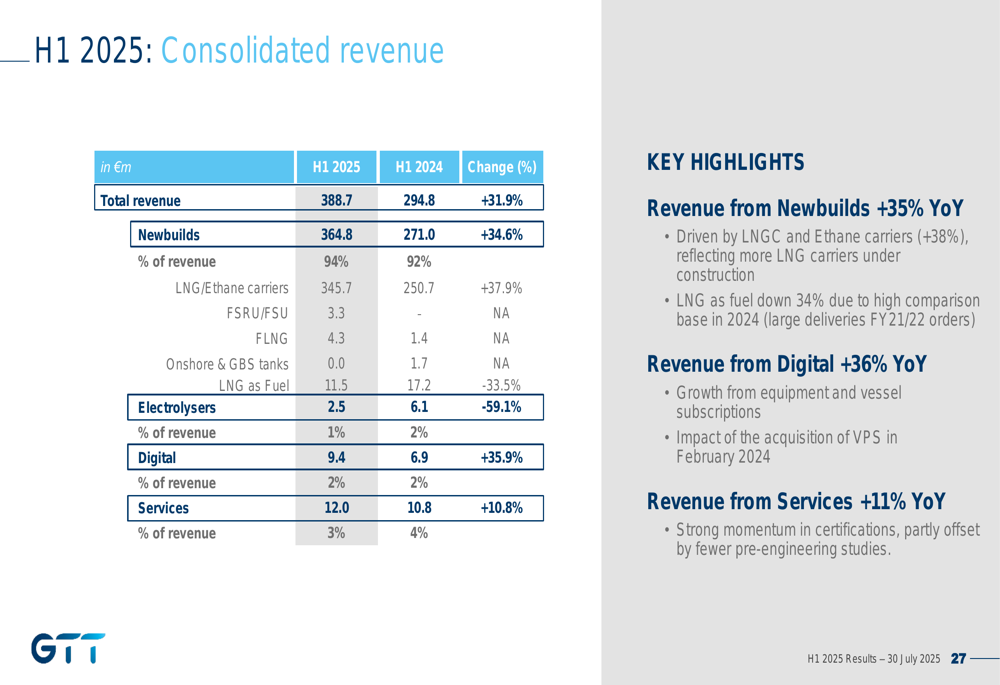

GTT reported consolidated revenue of €388.7 million for H1 2025, representing a 31.9% increase compared to the same period last year. This growth was primarily driven by the company’s core newbuilds business, which grew by 34.6% to €364.8 million.

As shown in the following consolidated revenue breakdown:

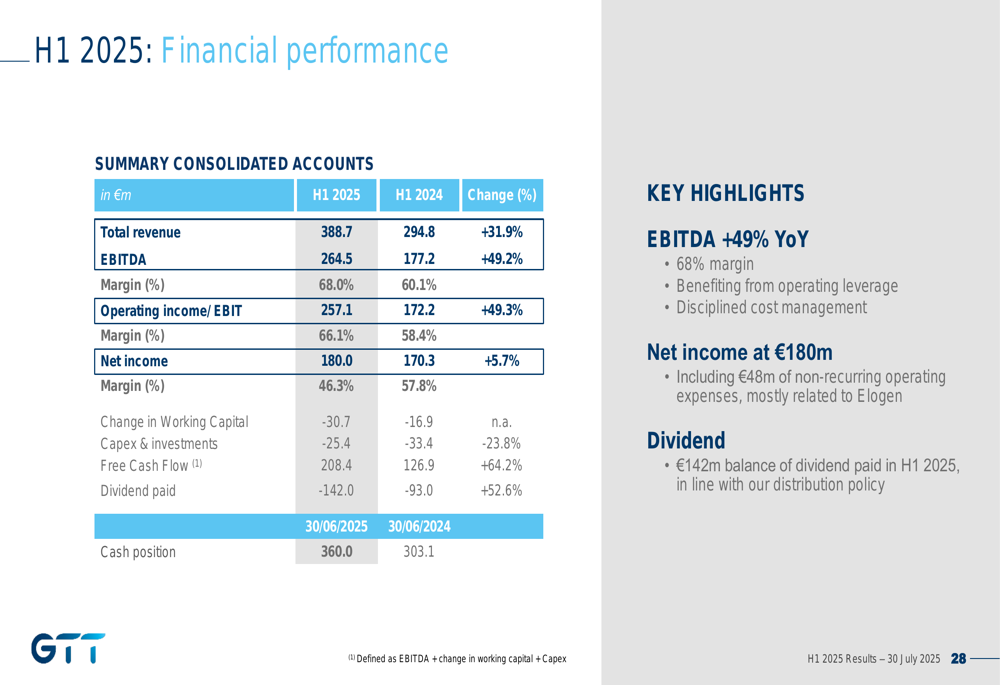

The company’s EBITDA surged by 49.2% year-over-year to €264.5 million, resulting in an impressive EBITDA margin of 68%. This significant margin expansion reflects GTT’s operating leverage and disciplined cost management. Net income increased by 5.7% to €180 million, and the company maintained a strong cash position of €360 million, even after paying €142 million in dividends during the first half of the year.

The following financial performance summary illustrates the company’s strong profitability metrics:

Core Business Strength

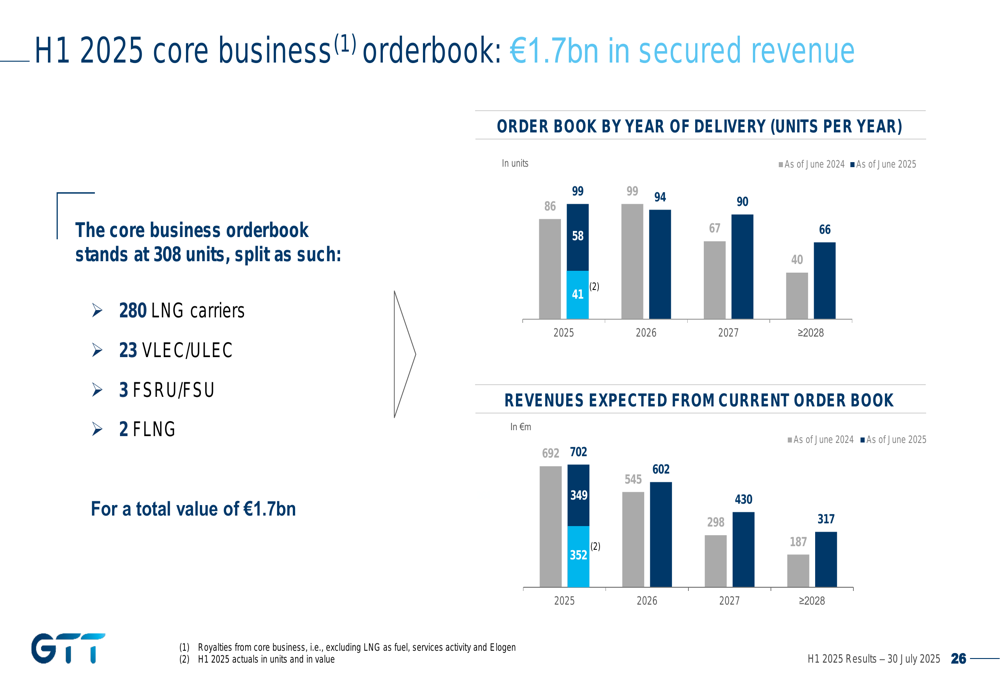

GTT’s core business continues to show robust performance, with 17 new orders received in H1 2025. The company’s orderbook stood at 308 units as of June 30, 2025, representing €1.7 billion in secured revenue. This includes 280 LNG carriers, 23 VLEC/ULEC (Very Large/Ultra Large Ethane Carriers), 3 FSRU/FSU (Floating Storage and Regasification Units/Floating Storage Units), and 2 FLNG (OL:FLNG) (Floating Liquefied Natural Gas (OTC:LNGLF)) units.

The following chart illustrates the composition and timeline of GTT’s orderbook:

The LNG market fundamentals remain strong, with exceptional Sales and Purchase Agreement (SPA) activity in Q2 2025, particularly for US pre-FID (Final Investment Decision) projects. Approximately 38 Mtpa (million tonnes per annum) of new liquefaction capacity was sanctioned in 2025 so far, mainly in the US, including projects like Woodside (OTC:WOPEY) Louisiana, CP2 Phase 1, and Corpus Christi.

GTT also highlighted that new proposed IMO (International Maritime Organization) regulations could significantly increase compliance costs for older LNG carriers, potentially accelerating the replacement cycle. According to the company, over 350 vessels could be impacted as early as 2028, creating additional demand for GTT’s technologies.

Strategic Expansion

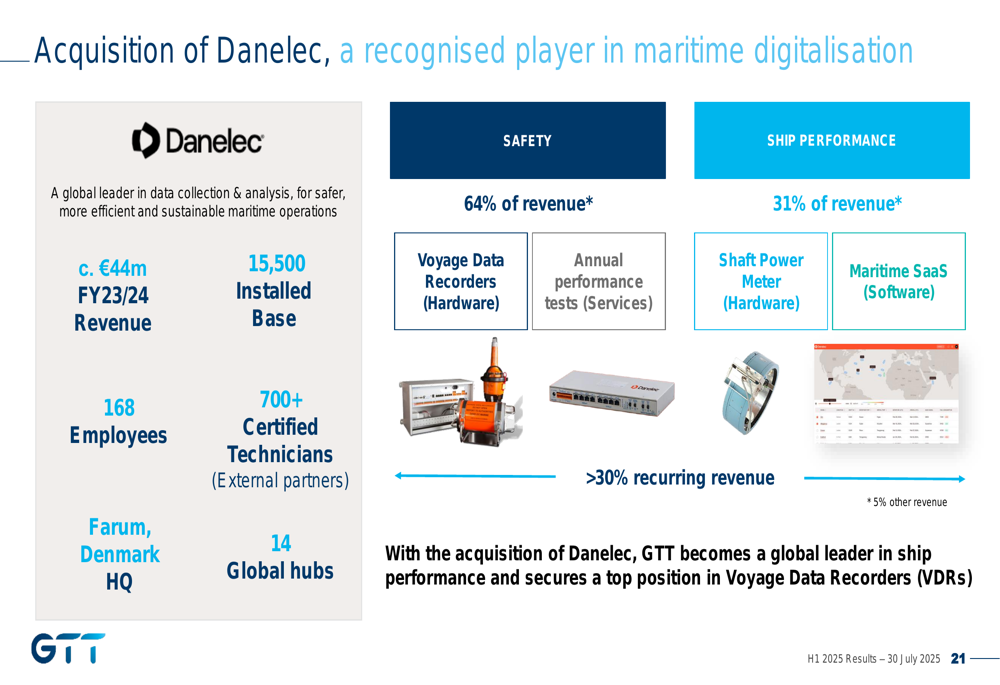

A major strategic development in H1 2025 was GTT’s acquisition of Danelec, a recognized player in maritime digitalization. Danelec generated approximately €44 million in revenue in FY23/24 and has an installed base of 15,500 units. The company specializes in data collection and analysis for safer, more efficient, and sustainable maritime operations, with 64% of its revenue coming from safety products and 31% from ship performance solutions.

The following slide details the strategic rationale and potential synergies from the Danelec acquisition:

GTT’s digital segment showed strong growth in H1 2025, with revenue increasing by 35.9% year-over-year to €9.4 million. The gross margin for this segment improved to 57%, compared to 48% in FY 2024. Key achievements in the digital business included the expansion of the Fleet Centre in Vancouver and a contract with TMS Group to equip its entire fleet of 130+ ships with Ascenz Marorka solutions.

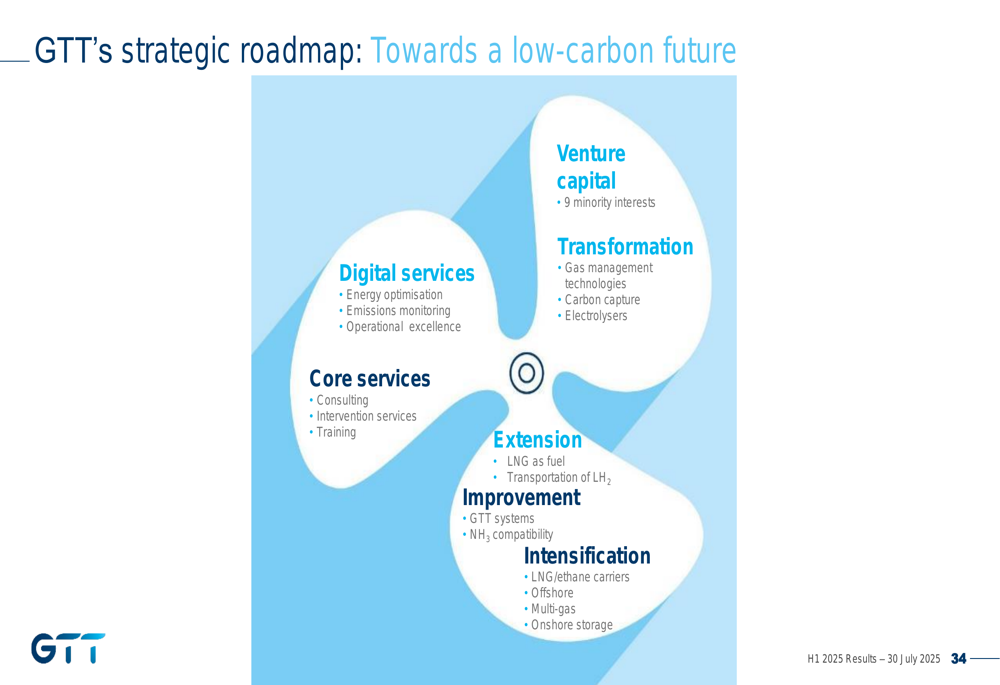

The company’s strategic roadmap continues to focus on diversification toward a low-carbon future, as illustrated in this comprehensive overview:

Market Outlook & Forward Guidance

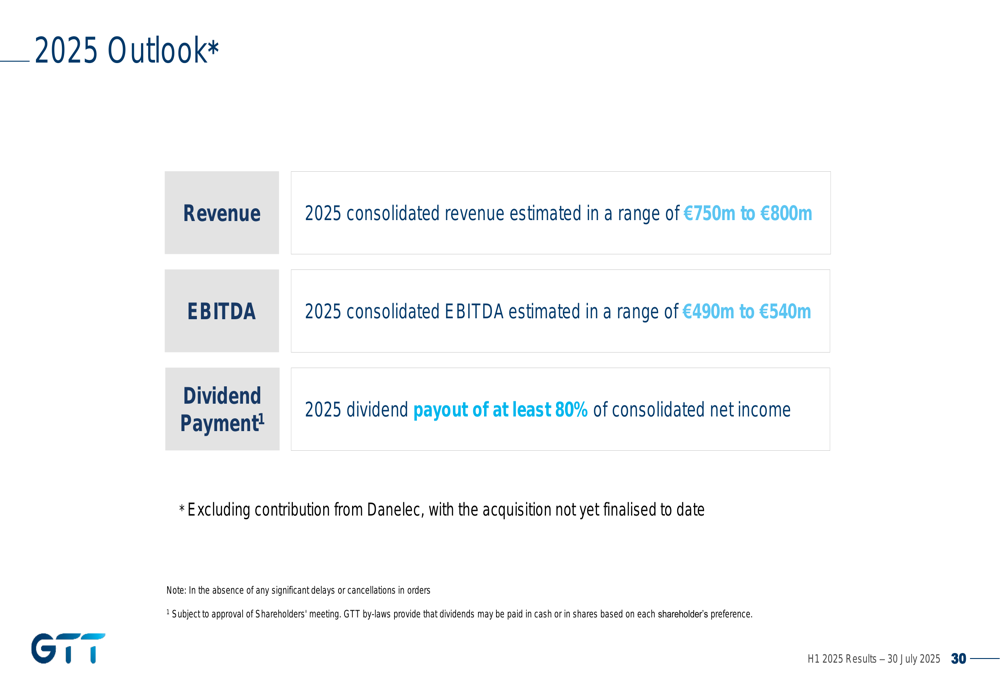

GTT confirmed its full-year 2025 guidance, projecting consolidated revenue between €750 million and €800 million and EBITDA between €490 million and €540 million. The company plans to maintain its dividend policy with a payout of at least 80% of consolidated net income. It’s worth noting that these projections exclude the contribution from the recently acquired Danelec.

As shown in the company’s outlook slide:

Looking beyond 2025, GTT provided long-term estimates for cumulated orders over the 2025-2034 period, including more than 450 LNG carriers, 25-40 ULEC/VLEC units, up to 10 FSRUs, up to 10 FLNGs, and 25-30 onshore and GBS (Gravity Based Structure) tanks.

The company also highlighted the continued adoption of LNG as a marine fuel, with LNG confirming its position as the leading alternative fuel with over 60% market share compared to methanol. GTT’s membrane system has secured 129 LNG fuel orders in total, including 18 new orders in H1 2025.

Challenges and Strategic Adjustments

Despite the overall positive performance, GTT’s Elogen subsidiary, which focuses on hydrogen electrolyzers, continues to face challenges. The company has implemented a strategic review resulting in a new business model focused on R&D and high-power stacks production at its Les Ulis facility. This restructuring includes a workforce reduction plan that was implemented in early July.

Elogen reported revenue of €2.5 million in H1 2025, with an EBITDA loss of €9.2 million. The subsidiary incurred non-recurring costs of €45 million related to the restructuring. Its order book stood at €3.0 million at the end of the period.

The company is also navigating geopolitical challenges in the LNG market, including US tariffs and a focus on domestic production in the United States. However, GTT remains confident in the strong long-term fundamentals of the LNG market, with ship-owners assessing timing for new orders amid these dynamics.

Conclusion

GTT’s H1 2025 results demonstrate the company’s ability to capitalize on strong demand for LNG transportation and storage solutions, while also successfully expanding into adjacent markets through strategic acquisitions and investments. The robust orderbook provides good visibility for future revenue, and the company’s high margins reflect its technological leadership and operational efficiency.

While challenges remain, particularly in the hydrogen business and amid geopolitical uncertainties, GTT’s diversified strategy and strong market position in its core business segment position the company well for continued growth. The confirmation of full-year guidance suggests management confidence in maintaining this positive momentum through the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.