Cardiff Oncology shares plunge after Q2 earnings miss

Introduction & Market Context

Hagerty Inc. (NYSE:HGTY) presented its Q1 2025 financial results on May 7, revealing substantial growth across all business segments and significant profitability improvements. The specialty automotive insurer and enthusiast brand reported total revenue of $320 million, an 18% increase year-over-year, while net income more than tripled to $27 million.

Despite these strong results, Hagerty’s stock has faced pressure in recent months, trading at $8.88 as of May 6, down from its 52-week high of $12.35. The company’s shares showed signs of recovery in premarket trading on May 7, up 3.04% to $9.15.

Quarterly Performance Highlights

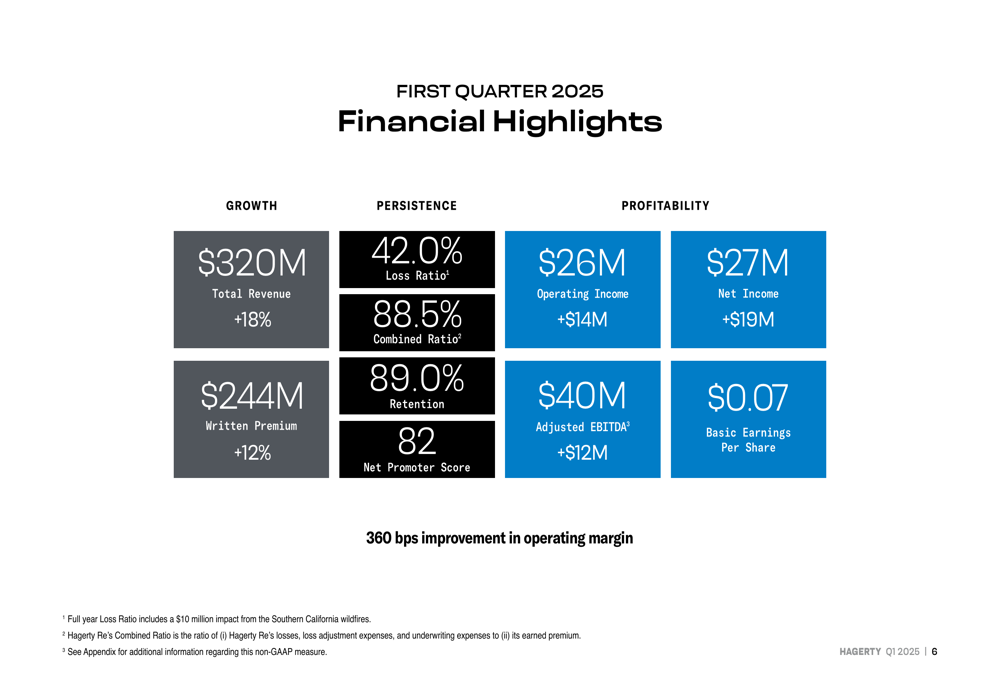

Hagerty delivered impressive financial results for Q1 2025, with total revenue reaching $320 million, up 18% compared to the same period last year. The company reported written premium growth of 12%, adding 55,000 new members during the quarter.

The most dramatic improvement came in profitability metrics, with operating income surging 110% to $26 million and operating margin expanding by 360 basis points. Net income reached $27 million, a 233% increase from $8 million in Q1 2024, while adjusted EBITDA grew 45% to $40 million.

As shown in the following financial highlights chart:

The company maintained strong operational metrics with a loss ratio of 42.0%, combined ratio of 88.5%, and policy retention rate of 89.0%. Customer satisfaction remained exceptional with a Net Promoter Score of 82, reflecting Hagerty’s strong relationship with its enthusiast customer base.

Detailed Financial Analysis

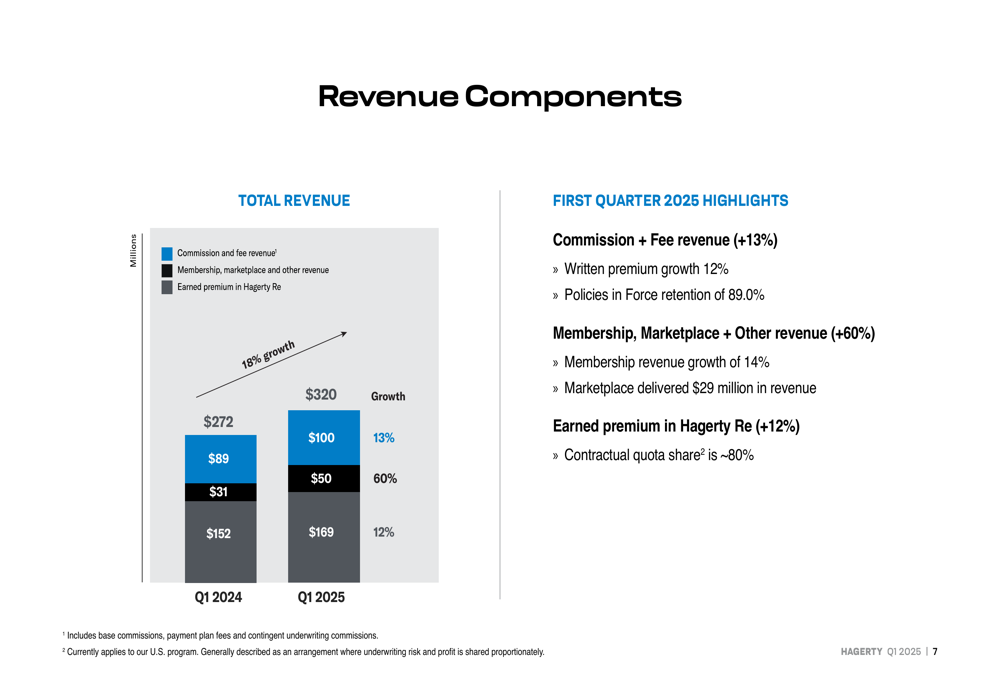

Revenue growth was broad-based across all segments. Commission and fee revenue increased 13% to $100 million, while earned premium in Hagerty Re grew 12% to $169 million. The standout performer was the Membership, Marketplace, and Other revenue category, which surged 60% to $50 million, driven primarily by a 176% increase in Marketplace revenue due to higher inventory sales.

The following chart illustrates the revenue component breakdown:

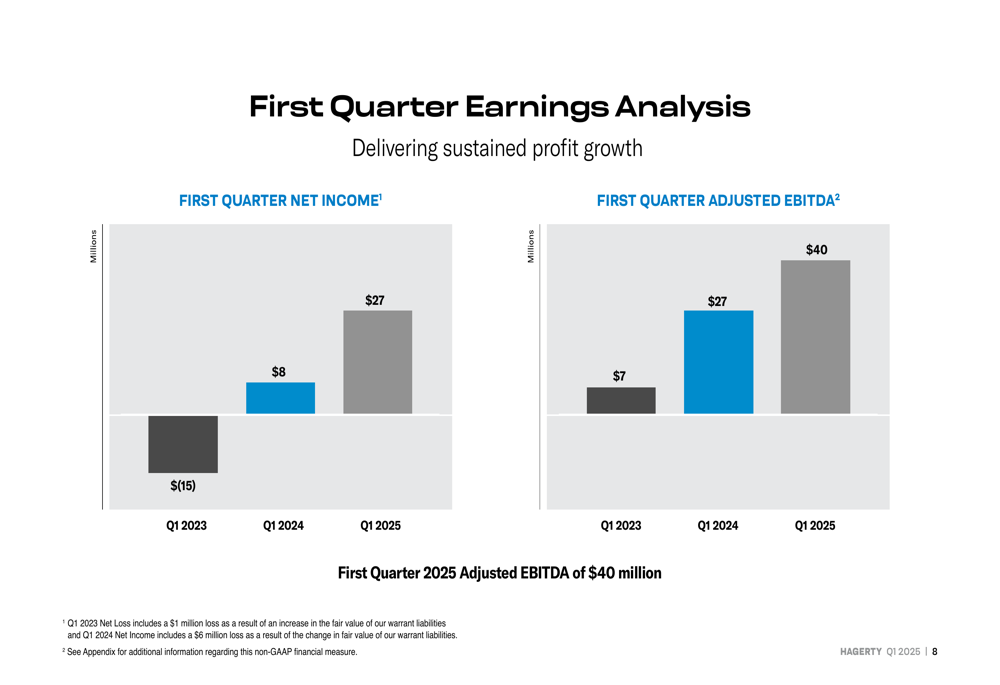

Hagerty’s earnings trajectory shows consistent improvement over the past two years, with Q1 2025 representing the continuation of strong momentum from 2024. The company has transformed from a net loss position in Q1 2023 to substantial profitability in Q1 2025.

The earnings progression is clearly visualized in this chart:

The company also strengthened its financial position by entering into a $375 million unsecured credit agreement, adding BMO to the upsized facility with lower borrowing costs and extending maturity to March 2030.

Strategic Initiatives

Hagerty outlined several strategic priorities for 2025, centered around its goal to double policies in force to 3.0 million by 2030. Key initiatives include the State Farm rollout and launch of Enthusiast Plus insurance products, integrated membership with authentic delivery of products and services, and global expansion in live and digital auctions.

The company is making significant technology investments to support its growth ambitions, including the implementation of a new insurance IT platform, Duck Creek. Management noted that technology spend is expected to moderate as a percentage of revenue in 2026 as these investments begin to yield operational efficiencies.

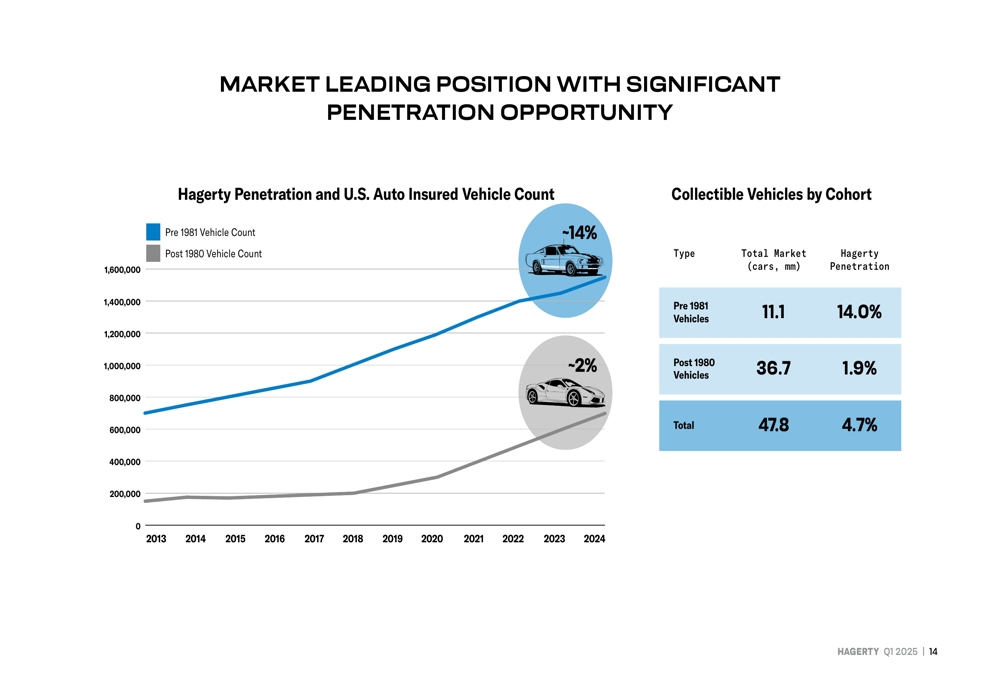

Hagerty maintains a market-leading position in the collectible vehicle insurance space, though significant penetration opportunities remain. The company has achieved 14% penetration in pre-1981 vehicles but only 1.9% in post-1980 vehicles, suggesting substantial growth potential in the newer collectible segment.

As illustrated in this market penetration chart:

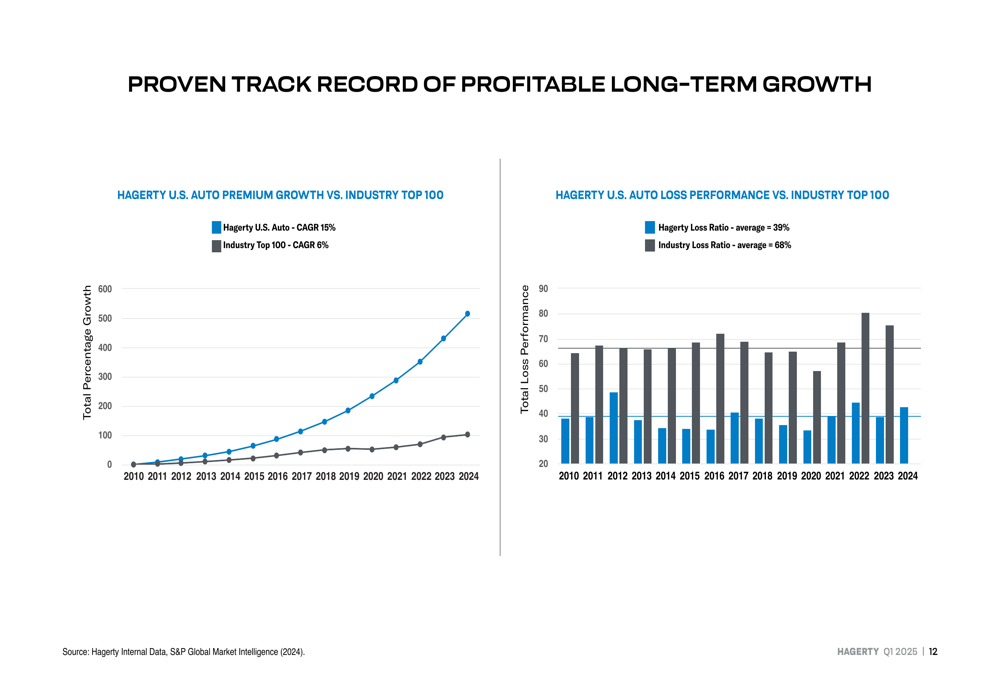

The company’s growth has consistently outpaced the broader insurance industry, with Hagerty’s U.S. auto premium growth achieving a 15% CAGR compared to just 6% for the industry top 100. Similarly, Hagerty’s loss ratio has averaged 39%, substantially better than the industry average of 68%.

This competitive advantage is clearly demonstrated in the following chart:

Forward-Looking Statements

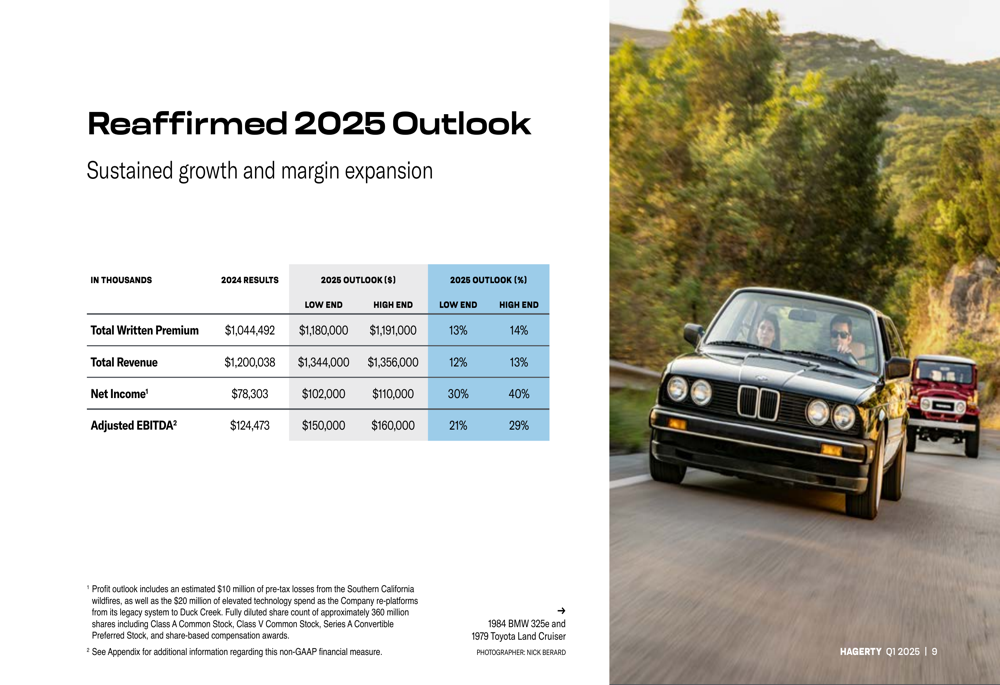

Hagerty reaffirmed its 2025 outlook, projecting total written premium of $1,180-1,191 million, total revenue of $1,344-1,356 million, net income of $102-110 million, and adjusted EBITDA of $150-160 million.

The company’s full-year guidance is visualized here:

These projections represent continued strong growth from 2024, when the company reported Q4 EPS of $0.02 (double the forecast) and full-year revenue growth of 19%. Management remains confident in its ability to execute its growth strategy while improving profitability, with net income expected to grow 30-40% for the full year 2025.

CEO McKeel Hagerty and CFO Patrick McClymont emphasized the company’s focus on technology investments to create a scalable platform for future growth, particularly as Hagerty pursues its ambitious goal of doubling its policy count by 2030. The management team highlighted that these investments, while significant in the near term, are expected to drive operational efficiencies and margin expansion in 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.