Aston Martin cuts 2025 volume and profit guidance amid weak demand, tariff risks

Introduction & Market Context

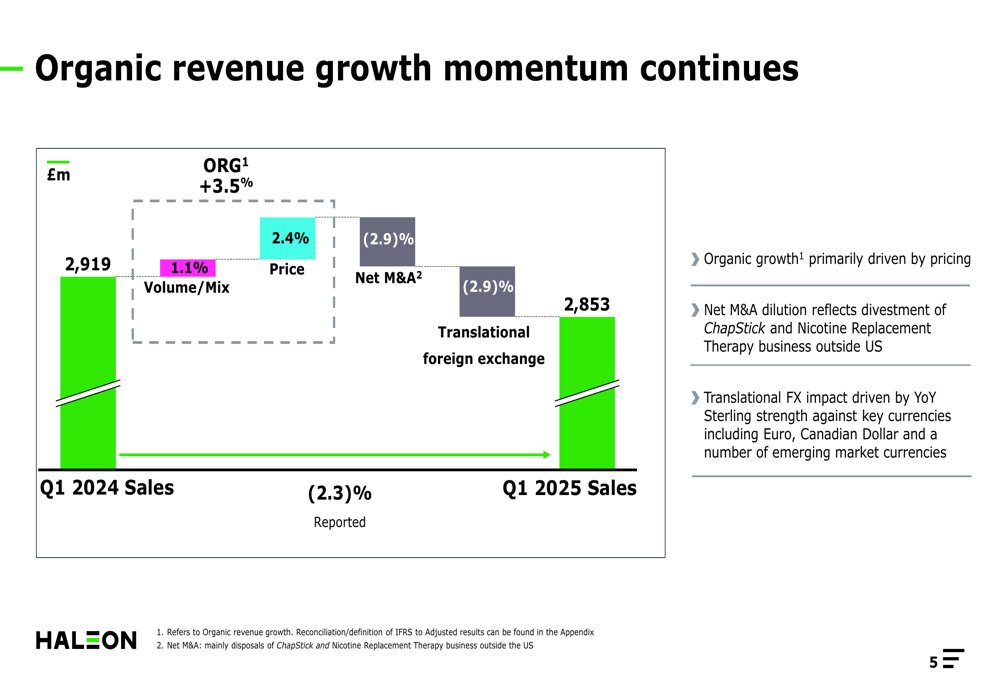

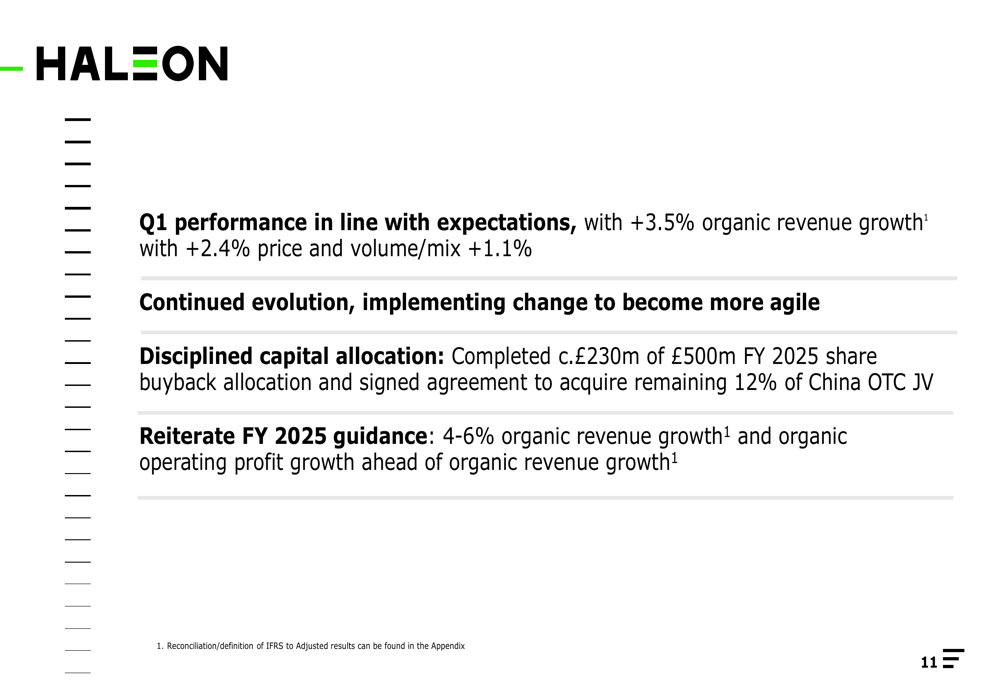

Haleon PLC (NYSE:HLN), the global consumer healthcare company, reported its first quarter 2025 results on April 30, showing organic revenue growth of 3.5% and reaffirming its full-year guidance. The company generated £2.9 billion in revenue during the quarter, with growth primarily driven by pricing actions (2.4%) complemented by positive volume/mix contribution (1.1%).

The results come as Haleon continues to navigate a challenging macroeconomic environment, with currency headwinds and the impact of recent divestments affecting reported figures. Despite these challenges, the company’s performance remained in line with management expectations, supporting their confidence in delivering on full-year targets.

Quarterly Performance Highlights

Haleon’s Q1 2025 performance showed resilience with organic growth of 3.5%, though reported revenue declined by 2.3% due to negative impacts from net M&A activities (-2.9%) and translational foreign exchange (-2.9%).

As shown in the following revenue growth breakdown:

The company’s CFO, Dawn Allen, noted that organic growth was primarily driven by pricing, while the net M&A dilution reflected the divestment of ChapStick and Nicotine Replacement Therapy business outside the US. The translational foreign exchange impact was driven by year-over-year Sterling strength against key currencies including the Euro, Canadian Dollar, and several emerging market currencies.

Segment and Regional Analysis

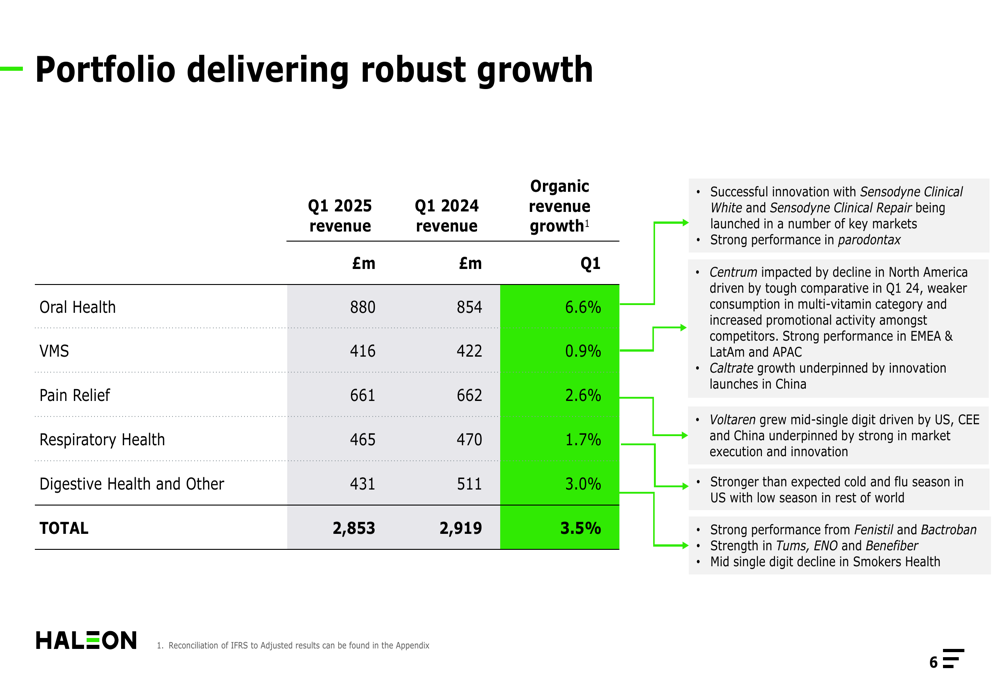

Haleon’s portfolio delivered varied performance across its five product categories. Oral Health emerged as the standout performer with 6.6% organic growth, driven by successful innovation including the launch of Sensodyne Clinical White and Sensodyne Clinical Repair in key markets.

The following table illustrates the performance across all segments:

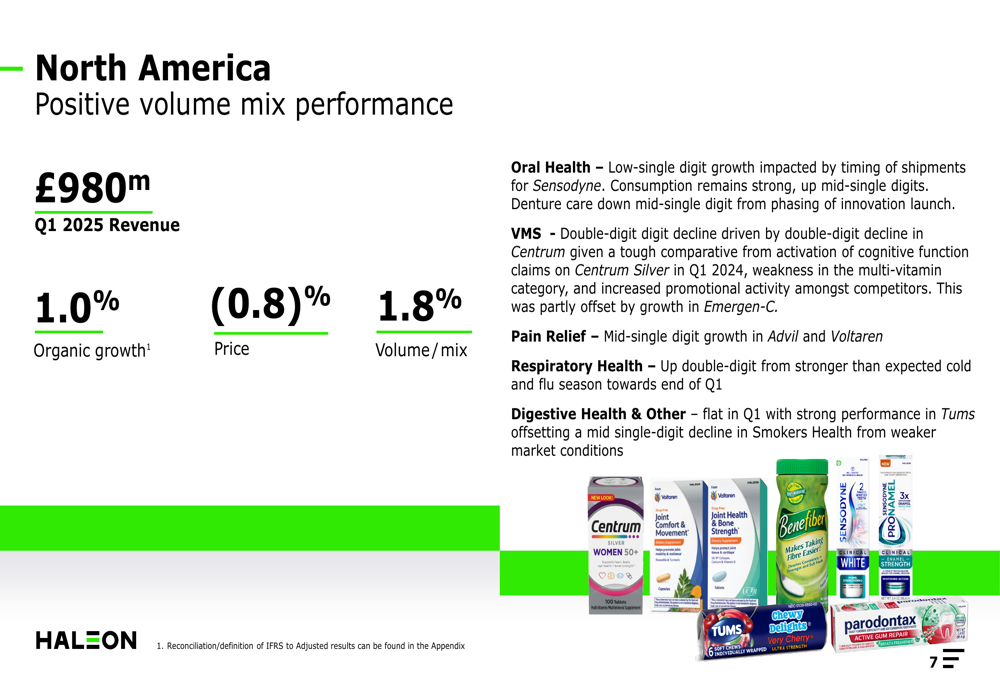

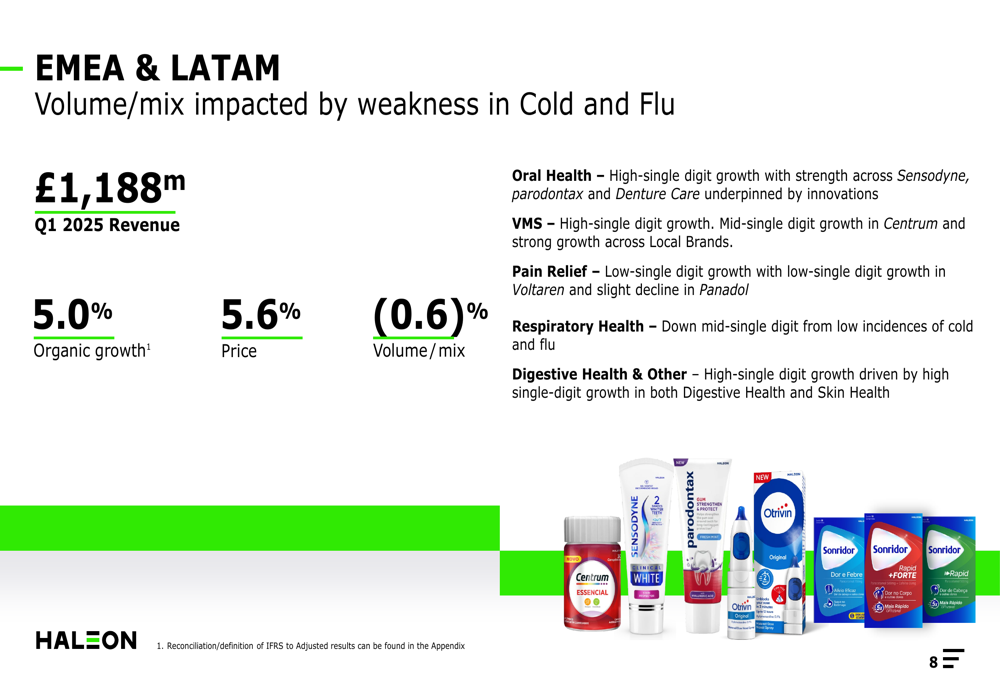

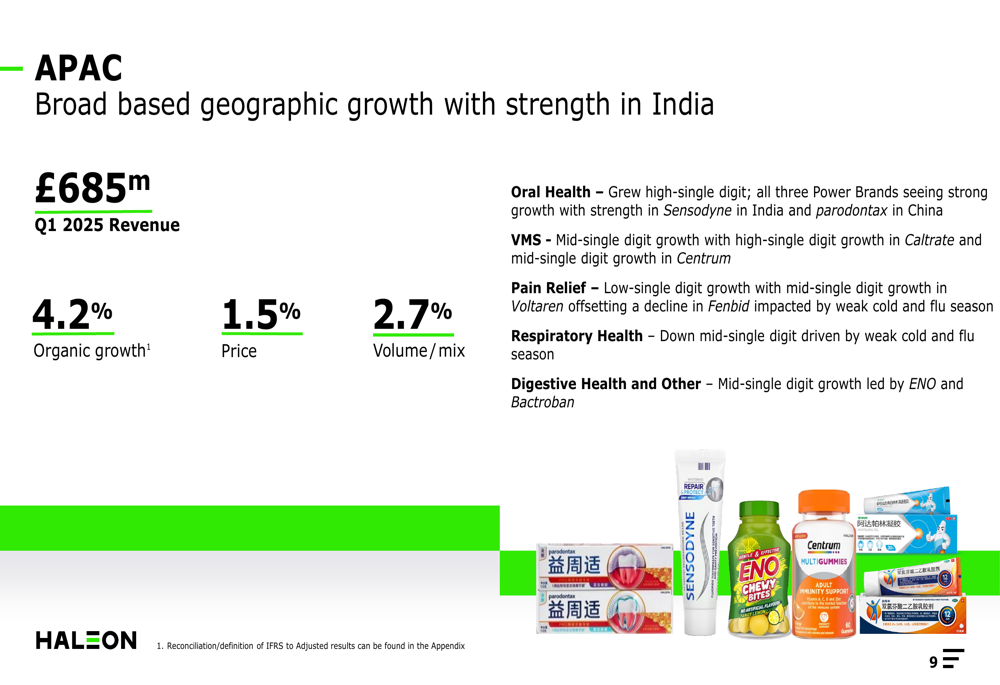

Regional performance showed significant variations, with North America delivering the slowest growth at 1.0%, while EMEA & LATAM led with 5.0% organic growth, followed by APAC at 4.2%.

North America’s modest performance was attributed to a mixed segment performance, with respiratory health benefiting from a stronger-than-expected cold and flu season toward the end of Q1, while the VMS category experienced a double-digit decline driven by Centrum:

By contrast, EMEA & LATAM showed robust growth with strong pricing contribution (5.6%), though slightly offset by negative volume/mix (-0.6%):

The APAC region delivered balanced growth with positive contributions from both pricing (1.5%) and volume/mix (2.7%), with particular strength in Oral Health:

Strategic Initiatives and Capital Allocation

Haleon continued to execute on its capital allocation priorities during Q1 2025. The company acquired approximately £170 million in shares from Pfizer (NYSE:PFE) in March 2025 and progressed on its share buyback program, which is expected to complete approximately £330 million of the total £500 million planned for 2025.

In a strategic move to strengthen its position in the important Chinese market, Haleon announced an agreement to acquire the remaining stake in its China joint venture for approximately £0.2 billion. This acquisition aligns with the company’s focus on expanding its presence in key growth markets.

The company also highlighted its continued focus on innovation, particularly in the Oral Health category, which has been a consistent growth driver. The successful launches of Sensodyne Clinical White and Sensodyne Clinical Repair in key markets underscore Haleon’s commitment to product development and market expansion.

Forward Guidance and Outlook

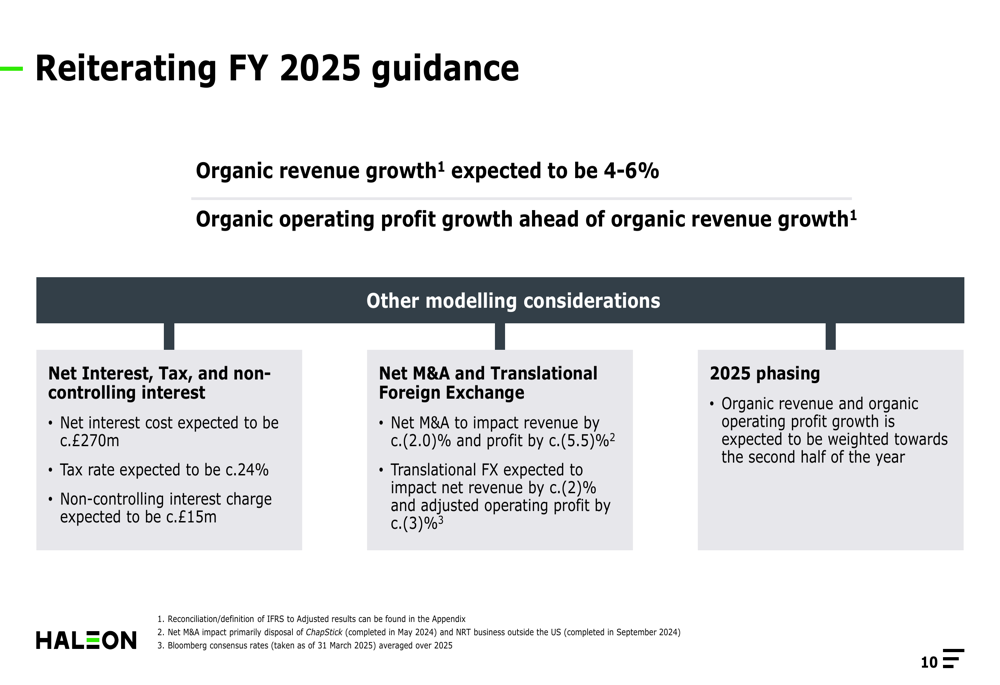

Haleon reaffirmed its full-year 2025 guidance, projecting organic revenue growth of 4-6% and organic operating profit growth ahead of organic revenue growth. Management noted that growth is expected to be weighted toward the second half of the year, consistent with their previous communication patterns.

The following slide details the company’s guidance and additional modeling considerations:

For modeling purposes, Haleon provided several key expectations, including a net interest cost of approximately £270 million, a tax rate of approximately 24%, and a non-controlling interest charge of approximately £15 million. The company also expects net M&A to impact revenue by approximately -2.0% and profit by approximately -5.5%, while translational foreign exchange is anticipated to impact net revenue by approximately -2% and adjusted operating profit by approximately -3%.

Summary and Market Reaction

Haleon’s Q1 2025 performance demonstrates the company’s ability to deliver moderate growth in a challenging environment, with particular strength in its Oral Health segment and EMEA & LATAM region. The company’s focus on innovation, strategic acquisitions, and disciplined capital allocation positions it well for the remainder of the year.

As summarized in the company’s key points:

Market reaction to the results was mixed, with Haleon’s stock closing at $10.28 on April 29, 2025, representing a 0.49% increase on the day. However, in extended trading following the release, the stock declined by 2.34% to $10.01, suggesting some investor caution regarding the company’s performance and outlook.

Investors will likely focus on Haleon’s ability to accelerate growth in the second half of the year as projected, particularly in the North American market where performance has been more subdued. The company’s progress on integrating the remaining stake in its China joint venture and the impact of its ongoing share buyback program will also be key areas to watch in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.