Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

Hancock Whitney Corporation (NASDAQ:HWC) presented its second quarter 2025 earnings results on July 15, 2025, highlighting the return of loan growth and continued net interest margin expansion. The regional bank, which operates across six southern states with a $35.2 billion asset base, reported solid performance metrics despite a challenging interest rate environment.

The company’s stock closed at $60.49 following the earnings release, representing a 1.6% increase, reflecting positive investor sentiment toward the quarterly results. With a market capitalization of $4.9 billion, Hancock Whitney continues to position itself as a stable regional banking player with a 125-year operating history.

Quarterly Performance Highlights

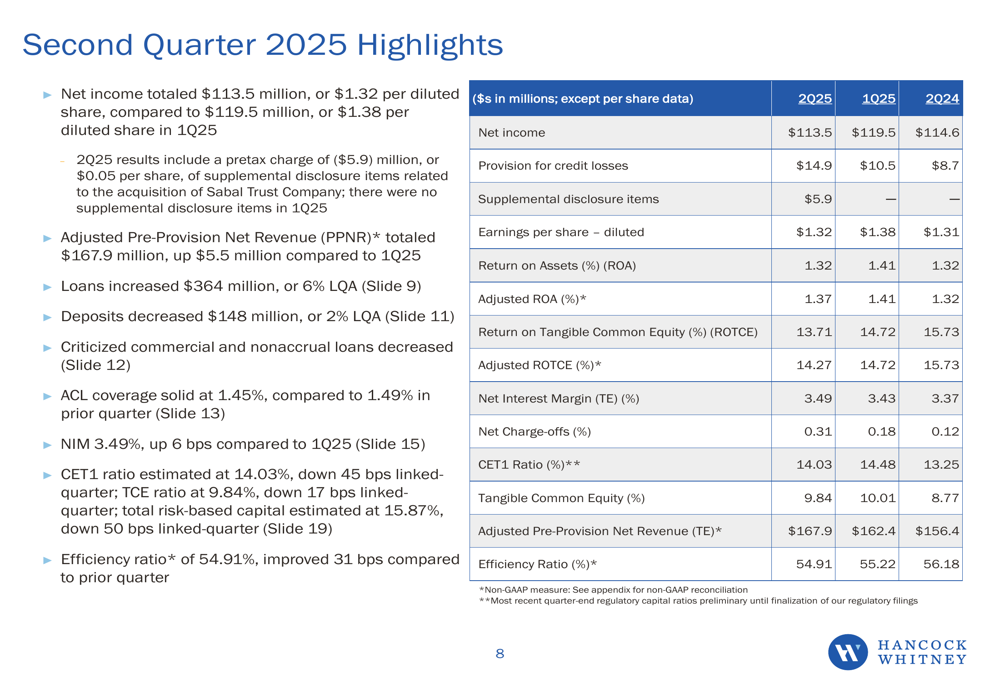

Hancock Whitney reported net income of $113.5 million, or $1.32 per diluted share for the second quarter of 2025. The company’s adjusted Pre-Provision Net Revenue (PPNR) totaled $167.9 million, while the efficiency ratio improved to 54.91%.

The bank maintained strong capital levels with a Common Equity Tier 1 (CET1) ratio of 14.03% and a Tangible Common Equity (TCE) ratio of 9.84%, positioning it well above regulatory requirements and providing flexibility for continued growth and capital return to shareholders.

As shown in the following summary of quarterly performance metrics:

Loan Growth and Portfolio Composition

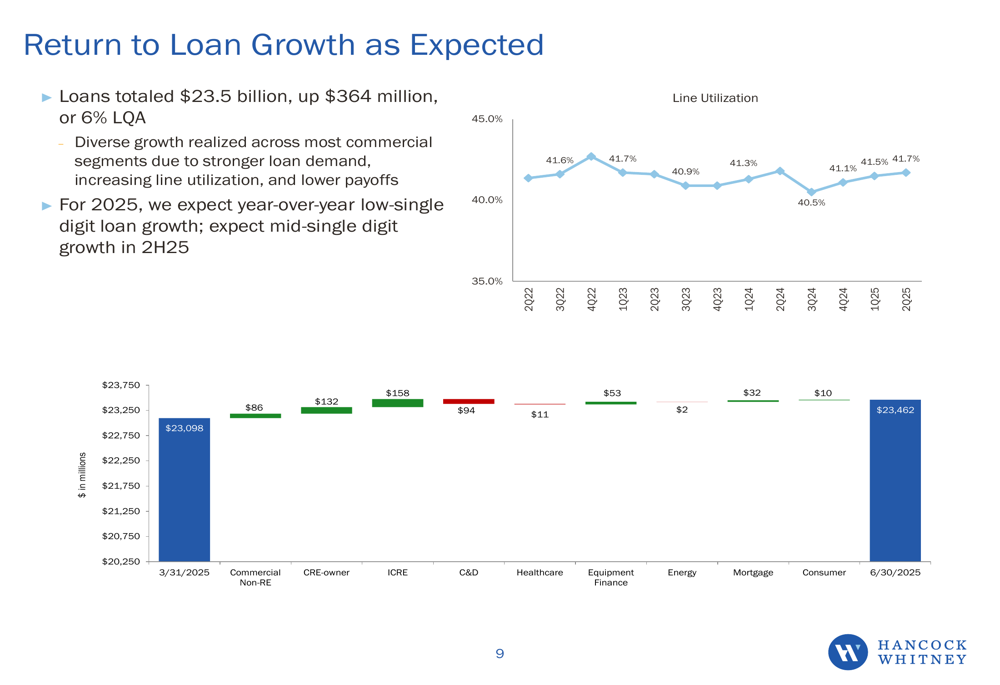

After a period of muted expansion, Hancock Whitney reported the return of loan growth in Q2 2025. Total loans increased by $364 million to $23.5 billion, representing a 6% linked-quarter annualized growth rate. The company indicated that diverse growth was realized across most commercial segments, with expectations for low single-digit year-over-year loan growth and mid-single digit growth in the second half of 2025.

The following chart illustrates the loan growth by segment and line utilization trends:

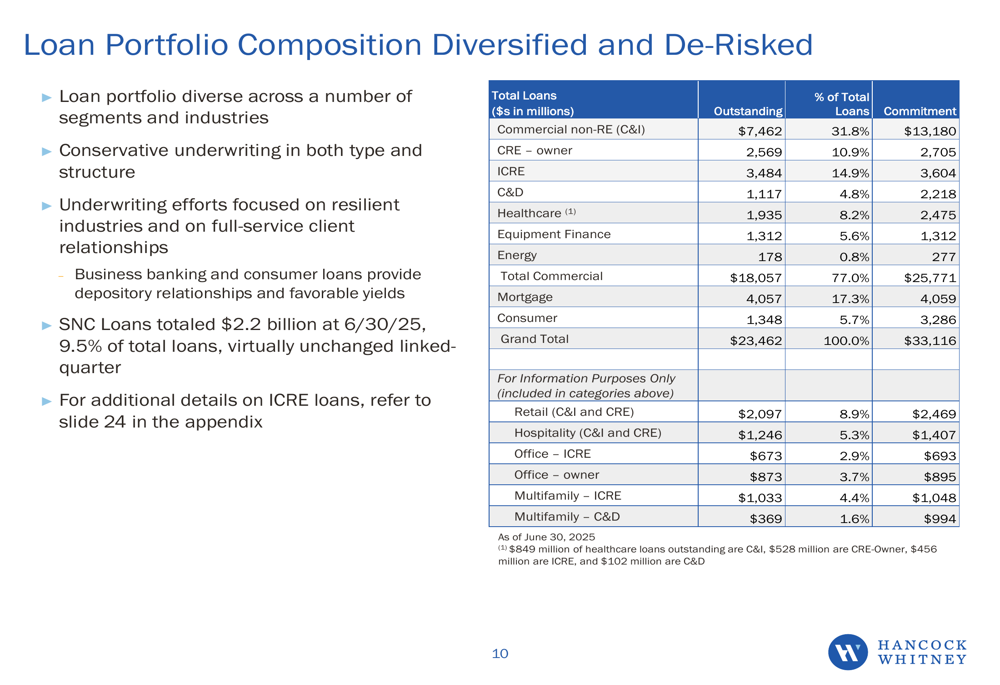

Hancock Whitney’s loan portfolio remains well-diversified across multiple segments and industries, reflecting the company’s de-risking strategy. Commercial non-real estate loans constitute the largest segment at $7.46 billion, followed by mortgage loans at $4.06 billion and income-producing commercial real estate at $3.48 billion.

The detailed breakdown of the loan portfolio demonstrates the bank’s balanced approach to credit risk:

Deposit Trends and Funding

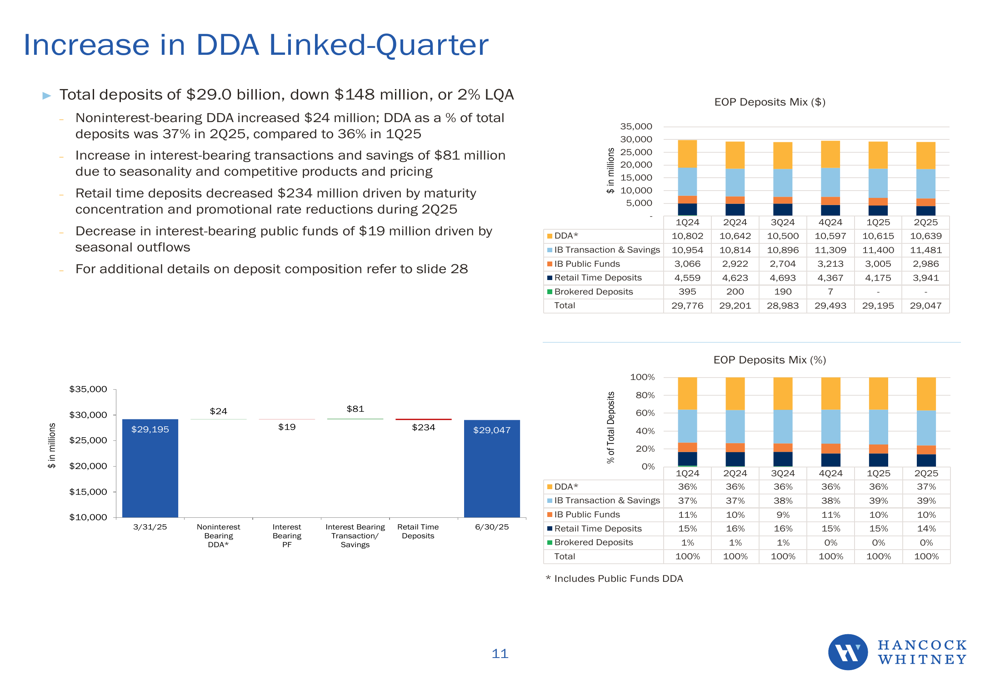

Total deposits decreased slightly by $148 million to $29.0 billion, representing a 2% linked-quarter annualized decline. However, the bank reported an encouraging increase in noninterest-bearing demand deposit accounts (DDA), which grew by $24 million during the quarter. DDA as a percentage of total deposits improved to 37% in Q2 2025 from 36% in the previous quarter, helping to manage the bank’s overall cost of funds.

The following chart shows the deposit mix evolution:

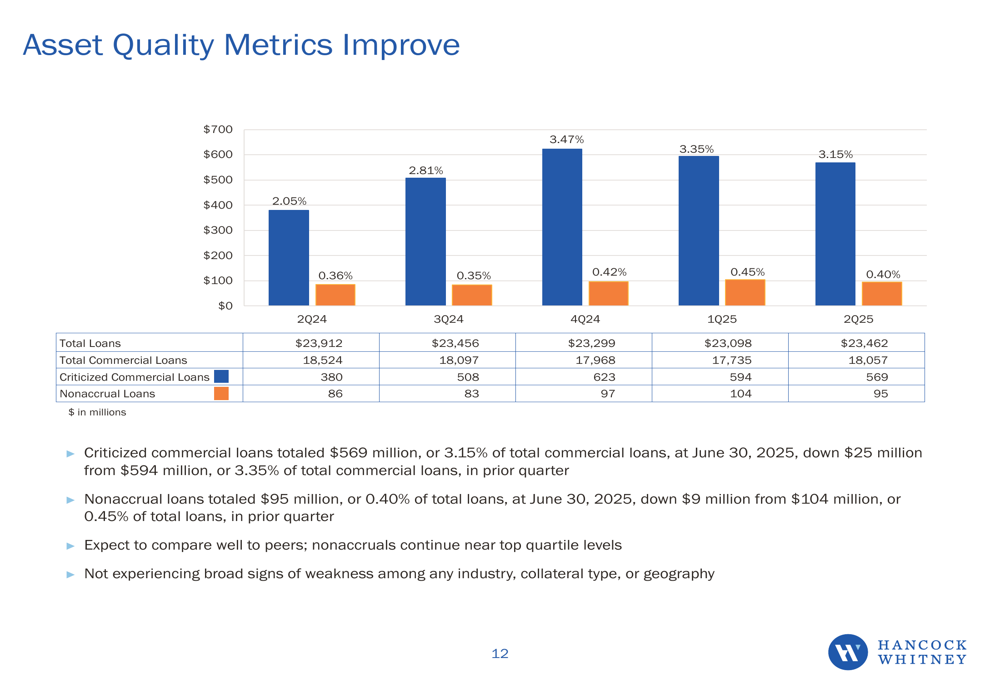

Asset Quality and Reserves

Hancock Whitney reported improving asset quality metrics in the second quarter. Criticized commercial loans totaled $569 million, or 3.15% of total commercial loans, showing improvement from previous quarters. Nonaccrual loans totaled $95 million, or 0.40% of total loans, also reflecting positive trends in credit quality.

The following chart demonstrates the improvement in asset quality metrics:

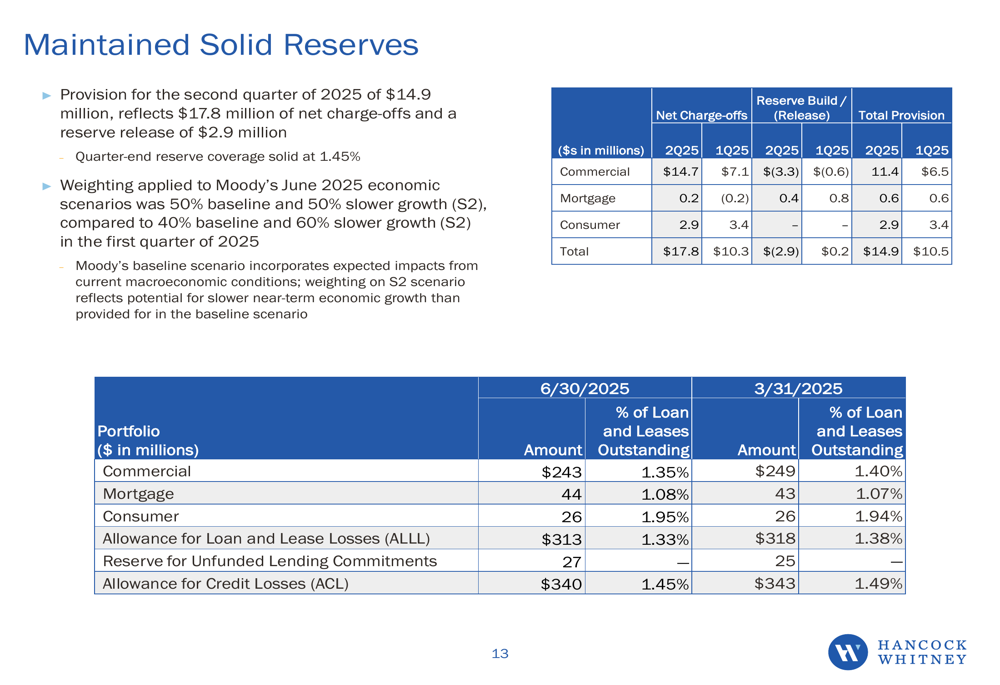

The bank maintained solid reserves with an allowance for credit losses (ACL) at 1.45% of total loans. The provision for credit losses in Q2 2025 was $14.9 million, reflecting $17.8 million of net charge-offs and a reserve release of $2.9 million. The company’s economic scenario weighting applied to its reserve modeling was 50% baseline and 50% slower growth, indicating a cautious approach to potential economic headwinds.

The following breakdown shows the composition of the bank’s reserves:

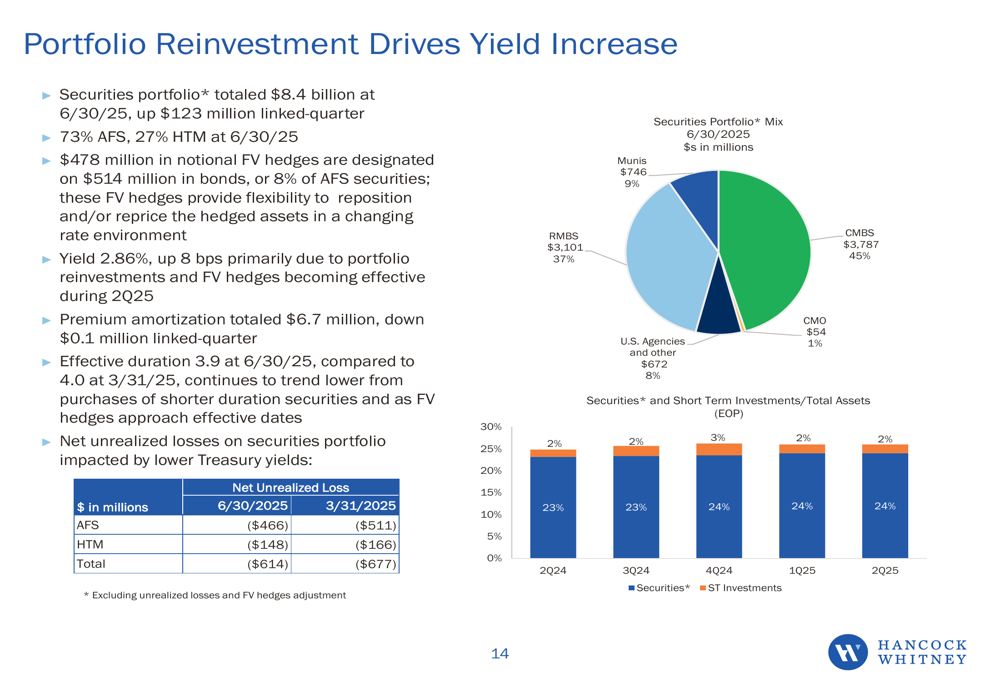

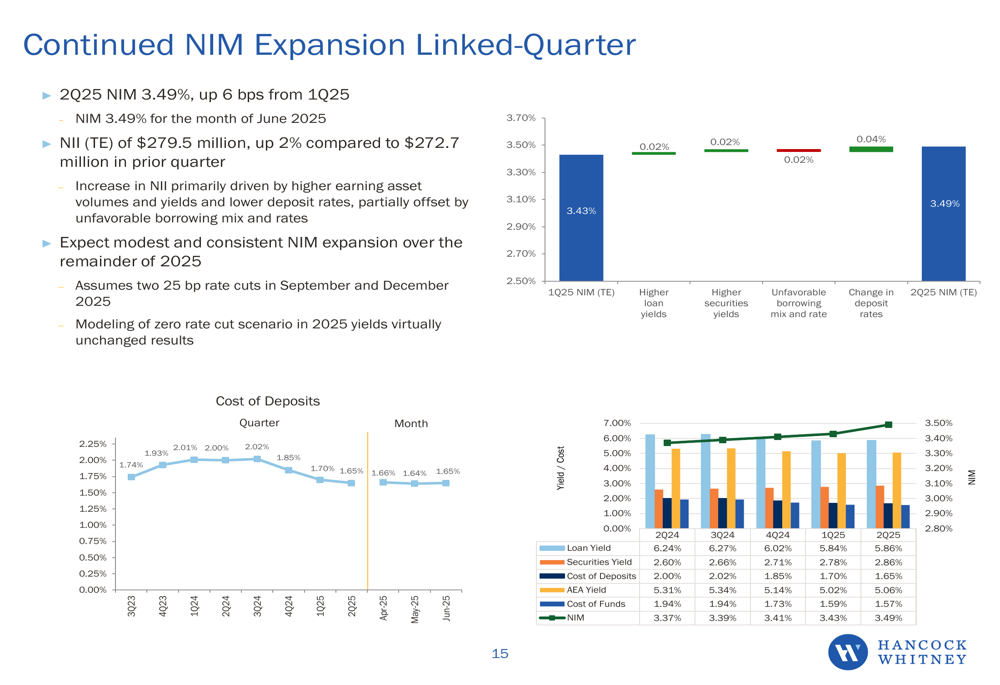

Net Interest Margin and Income

Hancock Whitney reported continued expansion in its net interest margin (NIM), which increased to 3.49% in Q2 2025, up 6 basis points from the previous quarter. Net interest income (NII) grew to $279.5 million, representing a 2% increase compared to the prior quarter.

The company’s securities portfolio totaled $8.4 billion, with 73% classified as available for sale (AFS). Portfolio reinvestment has been a key driver of yield increases, as illustrated in the following chart:

The bank anticipates modest and consistent NIM expansion over the remainder of 2025, assuming two 25 basis point rate cuts by the Federal Reserve in September and December 2025. This outlook reflects management’s confidence in navigating the changing interest rate environment.

The following chart shows the NIM expansion trend and cost of deposits:

Strategic Growth Initiatives

Hancock Whitney outlined its multi-year organic growth plan focused on two key areas: revenue producers and facility expansion. The bank is actively hiring additional wholesale, business, and wealth management revenue producers, primarily in Texas and Florida markets, with an expected ongoing annual expense of $8.5 million.

For facility expansion, the company plans to open five additional financial centers in the Dallas metropolitan statistical area (MSA), with phased openings scheduled for Q4 2025 and 2026. This expansion represents an expected ongoing annual expense of $6.2 million.

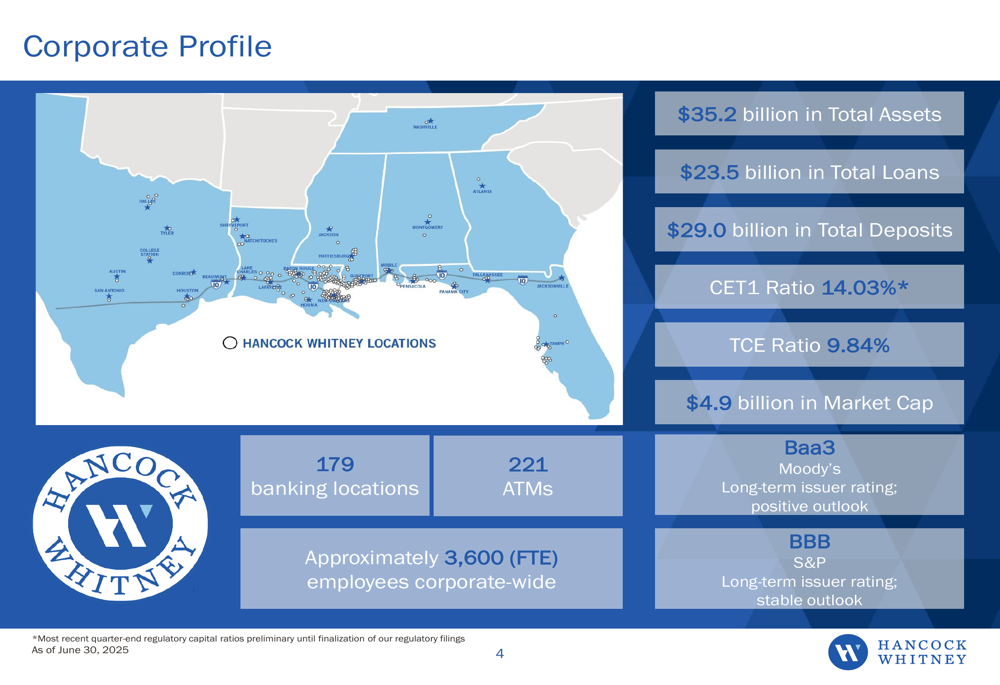

The bank’s corporate profile highlights its current footprint across six southern states, with 179 banking locations and 221 ATMs, serving customers through approximately 3,600 full-time equivalent employees:

Forward Outlook

Looking ahead, Hancock Whitney expects to maintain its momentum with low single-digit loan growth for the full year 2025, accelerating to mid-single digit growth in the second half. The company anticipates modest and consistent NIM expansion through year-end, even with projected Federal Reserve rate cuts.

The bank’s strong capital position, with a CET1 ratio of 14.03%, provides flexibility for continued organic growth, potential acquisitions, and capital returns to shareholders. Management emphasized its commitment to a de-risked balance sheet, proactive expense management, and ongoing technology investments as key elements of its long-term strategy.

With credit ratings of Baa3 (positive outlook) from Moody’s and BBB (stable outlook) from S&P, Hancock Whitney appears well-positioned to navigate the evolving economic landscape while pursuing strategic growth opportunities in its core markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.