Bitcoin price today: dips below $112k, near 6-wk low despite Fed cut bets

Introduction & Market Context

HarborOne Bancorp (NASDAQ:HONE) released its Q1 2025 investor presentation on April 24, 2025, showcasing steady financial performance alongside a major announcement of a definitive merger agreement with Eastern Bankshares, Inc. The stock responded positively to the news, jumping 11.33% to $11.20 in premarket trading following the announcement.

The New England-based bank, with $5.7 billion in assets, reported modest improvements in key metrics while simultaneously unveiling a transformative merger that would create the largest mid-sized bank in the Boston area.

Quarterly Performance Highlights

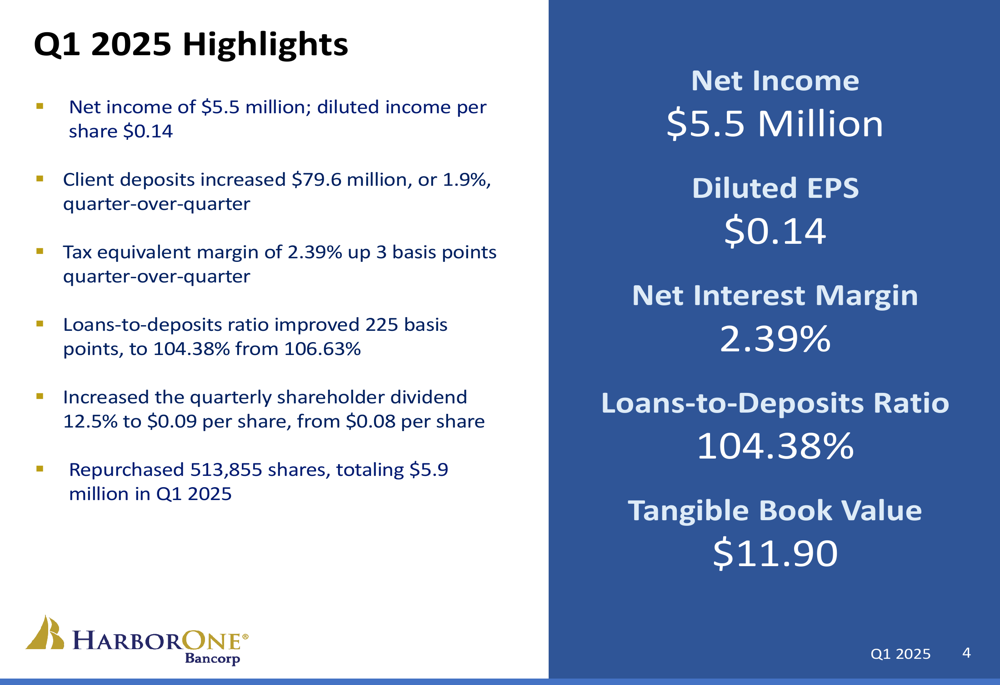

HarborOne reported net income of $5.5 million for Q1 2025, translating to diluted earnings per share of $0.14. While this represents a decrease from the $0.21 EPS in Q4 2024 and $0.17 in the year-ago quarter, the bank showed improvement in several operational metrics.

As shown in the following quarterly financial highlights:

Net interest margin improved to 2.39%, up 3 basis points quarter-over-quarter, continuing a positive trend that has seen the metric steadily increase from 2.25% in Q1 2024. Client deposits increased by $79.6 million (1.9%) from the previous quarter, while the loans-to-deposits ratio improved to 104.38% from 106.63%.

The company also returned value to shareholders through an increased quarterly dividend of $0.09 per share, up 12.5% from the previous $0.08, and repurchased 513,855 shares totaling $5.9 million during the quarter.

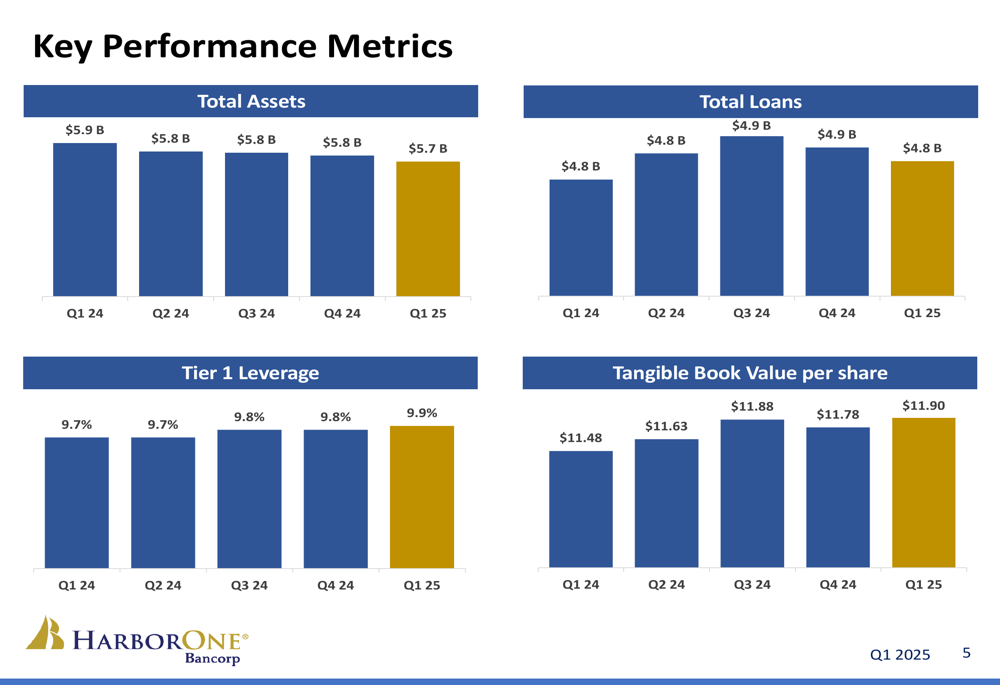

The following chart illustrates the bank’s consistent performance across key metrics over the past five quarters:

Asset Quality and Loan Portfolio

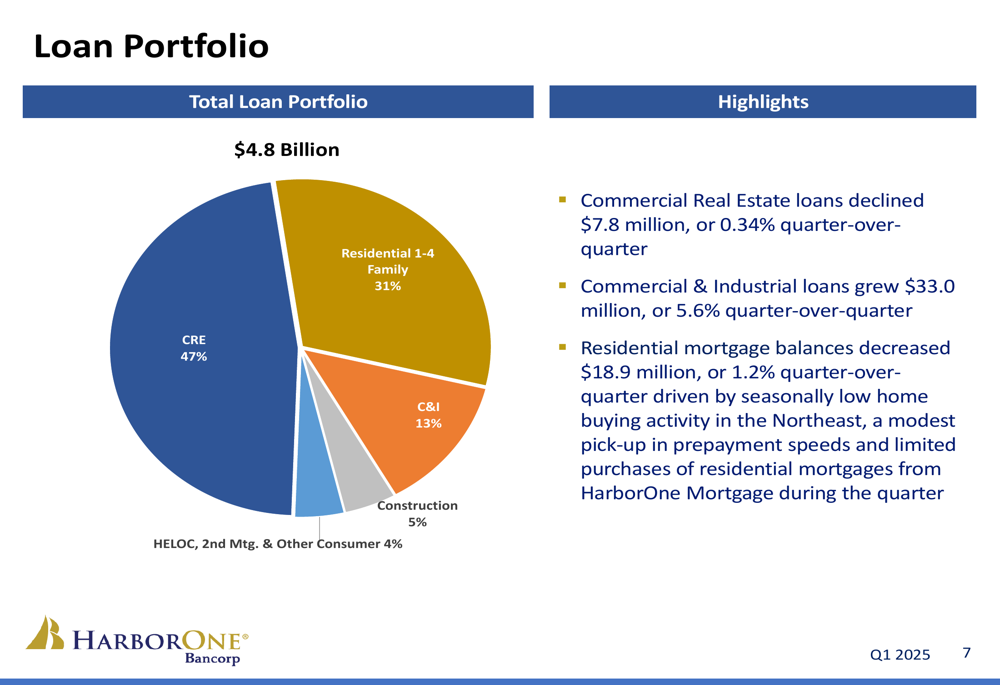

HarborOne’s loan portfolio totaled $4.8 billion at quarter-end, with commercial real estate (CRE) loans representing the largest segment at 47%, followed by residential 1-4 family loans at 31%, and commercial and industrial (C&I) loans at 13%.

The composition of the loan portfolio is illustrated in the following chart:

The bank reported mixed trends in its loan segments. Commercial real estate loans declined by $7.8 million (0.34%) quarter-over-quarter, while commercial and industrial loans grew by $33.0 million (5.6%). Residential mortgage balances decreased by $18.9 million (1.2%), which the company attributed to seasonally low home buying activity in the Northeast, modest increases in prepayment speeds, and limited purchases from HarborOne Mortgage.

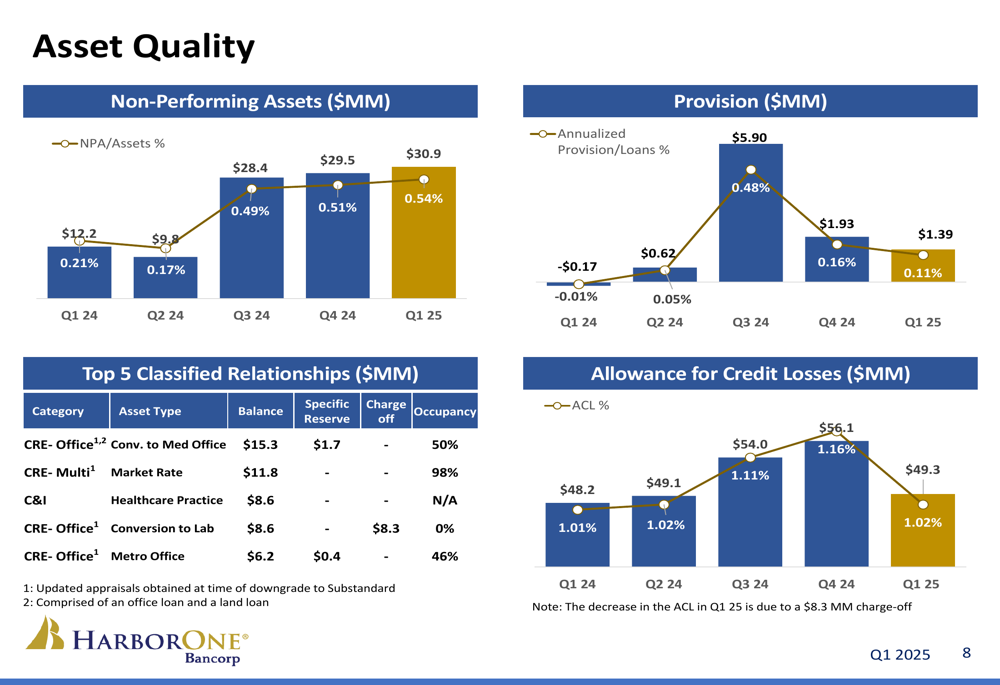

Asset quality metrics showed some deterioration, with non-performing assets increasing to $30.9 million from $12.2 million a year earlier. The bank also reported a significant $8.3 million charge-off on one office credit during the quarter.

The following chart details the asset quality metrics:

Given the ongoing concerns about commercial real estate, particularly office properties, HarborOne provided a detailed breakdown of its office exposure, which totals $212 million or approximately 8% of its CRE and construction portfolio. The bank noted that a classified Class A office loan required an additional $3.6 million specific reserve on top of an existing $4.7 million reserve, with the aggregate $8.3 million subsequently charged off during the quarter.

Deposit and Liquidity Position

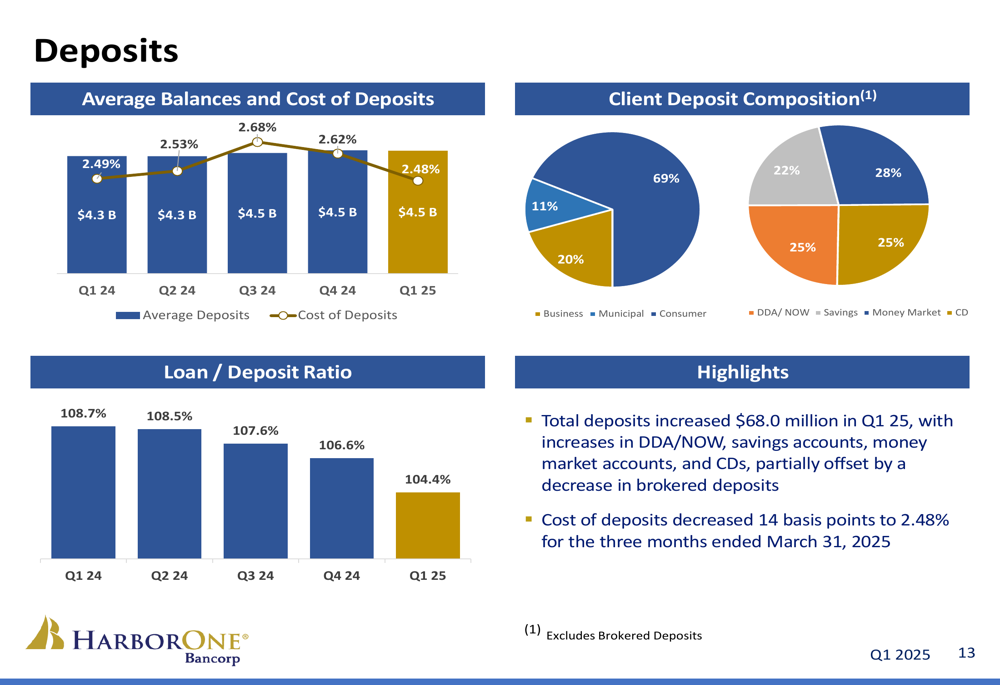

HarborOne maintained a solid liquidity position with uninsured deposits of $942 million representing 20.4% of total deposits. The bank reported 212% coverage of uninsured deposits with immediately available liquidity, highlighting its strong financial foundation.

The following chart illustrates the bank’s deposit composition and trends:

Total (EPA:TTEF) deposits increased by $68 million in Q1 2025, with growth across demand deposits, savings accounts, money market accounts, and CDs, partially offset by a decrease in brokered deposits. The cost of deposits decreased by 14 basis points to 2.48% for the quarter ended March 31, 2025.

Merger with Eastern Bankshares

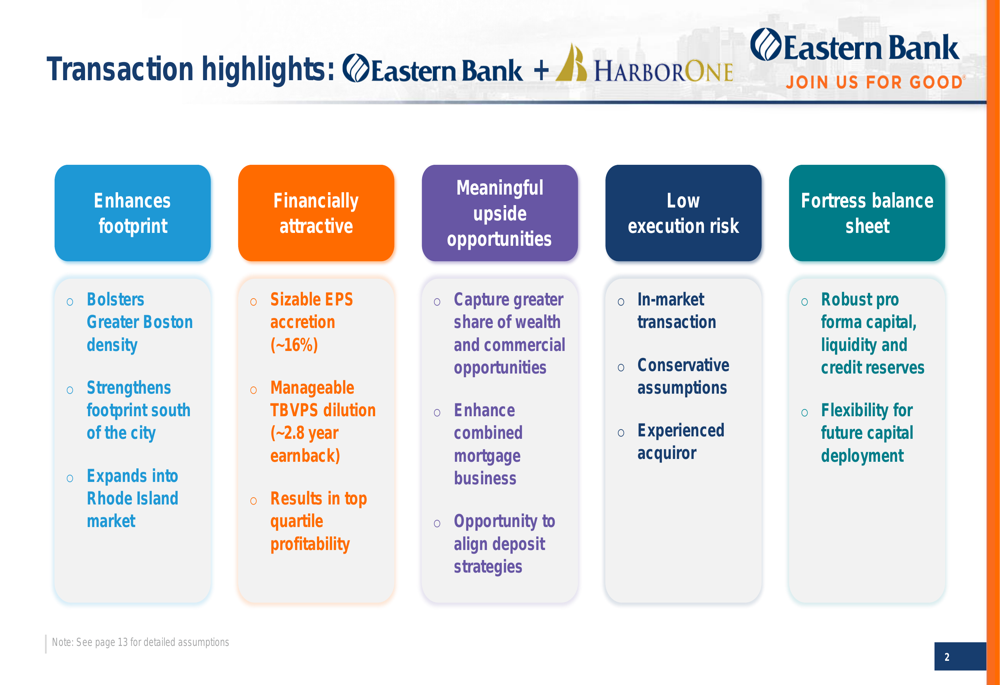

The most significant announcement in the presentation was HarborOne’s agreement to merge with Eastern Bankshares, Inc. Under the terms of the deal, HarborOne shareholders can elect to receive either $12.00 in cash or 0.765 shares of Eastern stock for each HarborOne share, subject to proration, with the overall consideration mix expected to be 75-85% stock.

The following slide outlines the key transaction highlights:

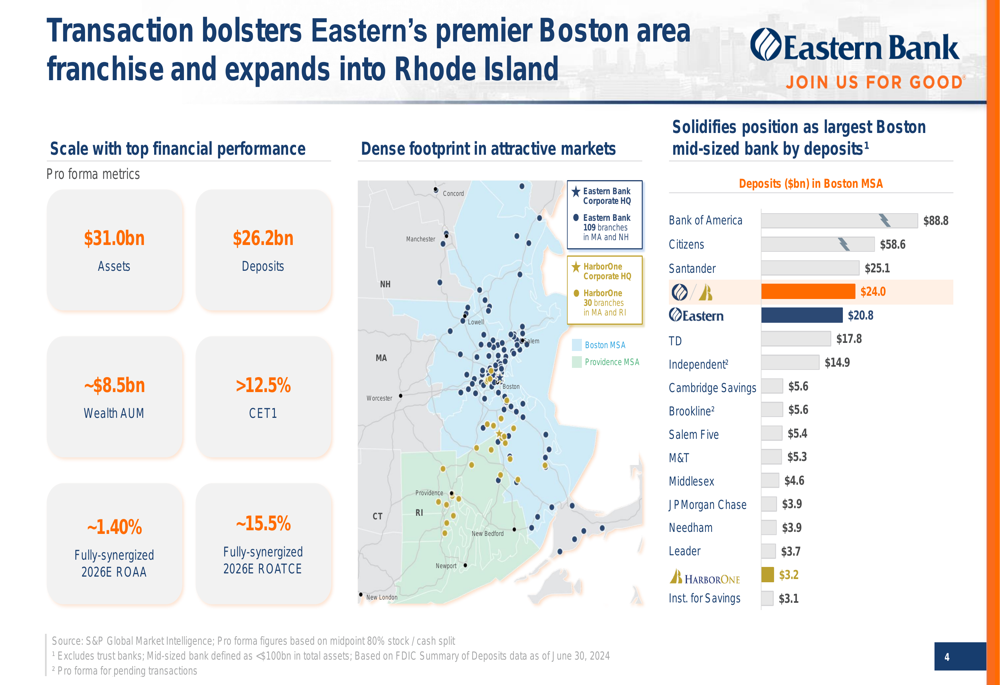

The merger will create a combined entity with approximately $31 billion in assets and $26.2 billion in deposits, positioning it as the largest mid-sized bank in the Boston area. The transaction is expected to be highly accretive, with projected EPS accretion of approximately 16% and an internal rate of return of around 18%.

The geographic footprint of the combined entity will strengthen Eastern’s presence in the Boston area while providing entry into the Rhode Island market, as illustrated in this map:

The merger is expected to unlock significant earnings potential, with fully-synergized net income projected to reach $440 million, up from $335 million. Cost savings are anticipated to be approximately 35% of HarborOne’s non-interest expense base, with one-time merger charges estimated at $115 million pre-tax.

Forward Outlook

Following the merger, the combined entity is projected to achieve enhanced profitability metrics, including a net interest margin of approximately 3.70% and an operating return on average tangible common equity of around 15.5%. These figures would place the bank in the top quartile of its peer group.

The transaction is subject to regulatory approvals and the approval of HarborOne shareholders, with closing expected in the fourth quarter of 2025. Eastern has demonstrated success with previous acquisitions, having delivered on stated financial targets in its mergers with Century and Cambridge.

While HarborOne’s Q1 2025 results showed some pressure on earnings and asset quality, the merger with Eastern represents a strategic move that could provide scale advantages and enhanced returns for shareholders. The significant premium implied by the merger terms (approximately 19% based on pre-announcement prices) suggests confidence in the combined entity’s future prospects despite the challenges in certain loan segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.