Gold prices edge higher on raised Fed rate cut hopes

Introduction & Market Context

Harmonic Inc . (NASDAQ:HLIT) presented its second quarter 2025 earnings results on July 28, 2025, revealing a mixed financial performance as the company navigates short-term challenges while positioning for future growth. The telecommunications equipment provider reported slight revenue declines year-over-year but demonstrated strength in bookings, cash position, and its Video segment.

Despite beating earnings expectations in Q1 2025, Harmonic’s stock experienced a modest 1.67% increase on the day of the Q2 earnings release, closing at $9.00, with an additional 1.78% gain in after-hours trading. The company’s shares remain well within their 52-week range of $7.91 to $15.46.

Quarterly Performance Highlights

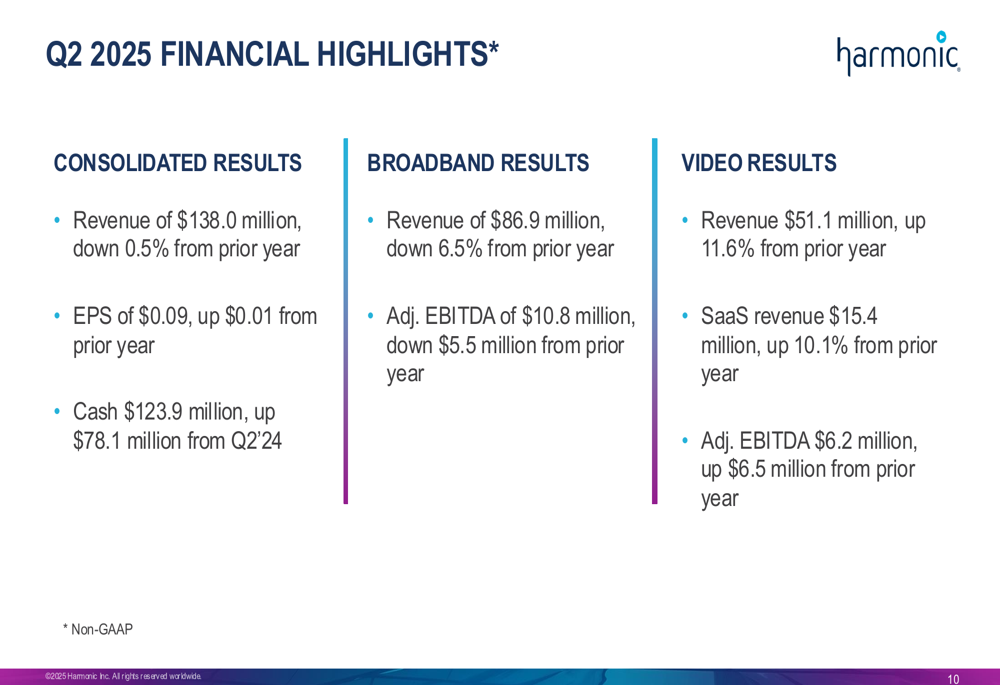

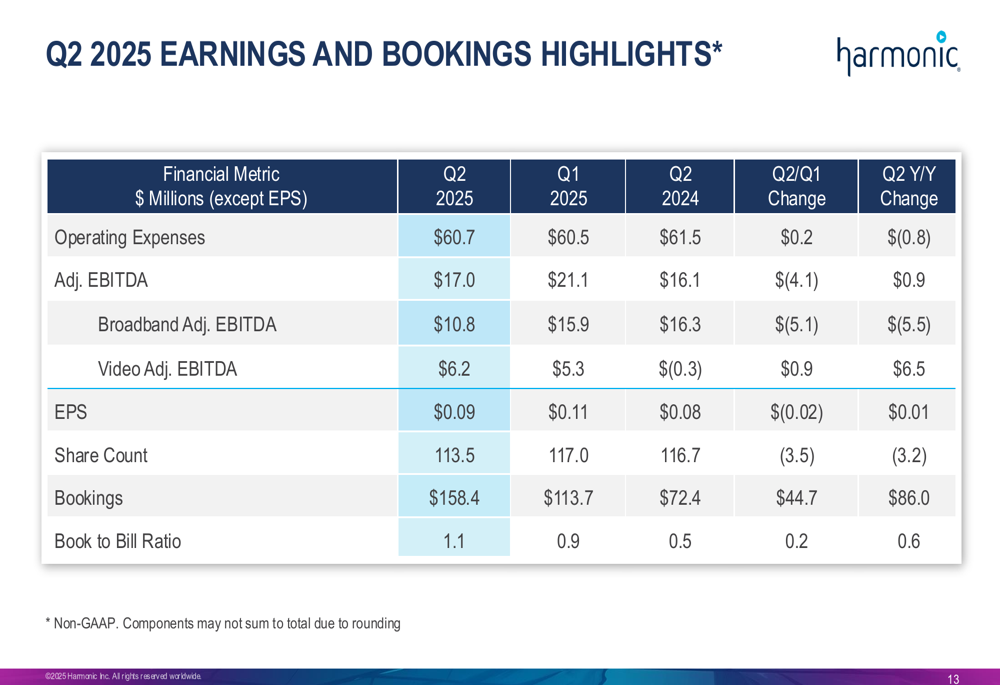

Harmonic reported Q2 2025 revenue of $138.0 million, representing a slight decrease of 0.5% compared to the same period last year, but a 3.7% improvement from Q1 2025. Earnings per share came in at $0.09, up $0.01 year-over-year but down from $0.11 in the previous quarter.

As shown in the following comprehensive financial overview, the company demonstrated improved profitability metrics despite the revenue challenges:

A particularly encouraging sign was the significant improvement in bookings, which reached $158.4 million in Q2 2025, more than double the $72.4 million recorded in Q2 2024. This resulted in a book-to-bill ratio of 1.1, indicating strong future revenue potential.

The detailed quarterly comparison below highlights these trends across key financial metrics:

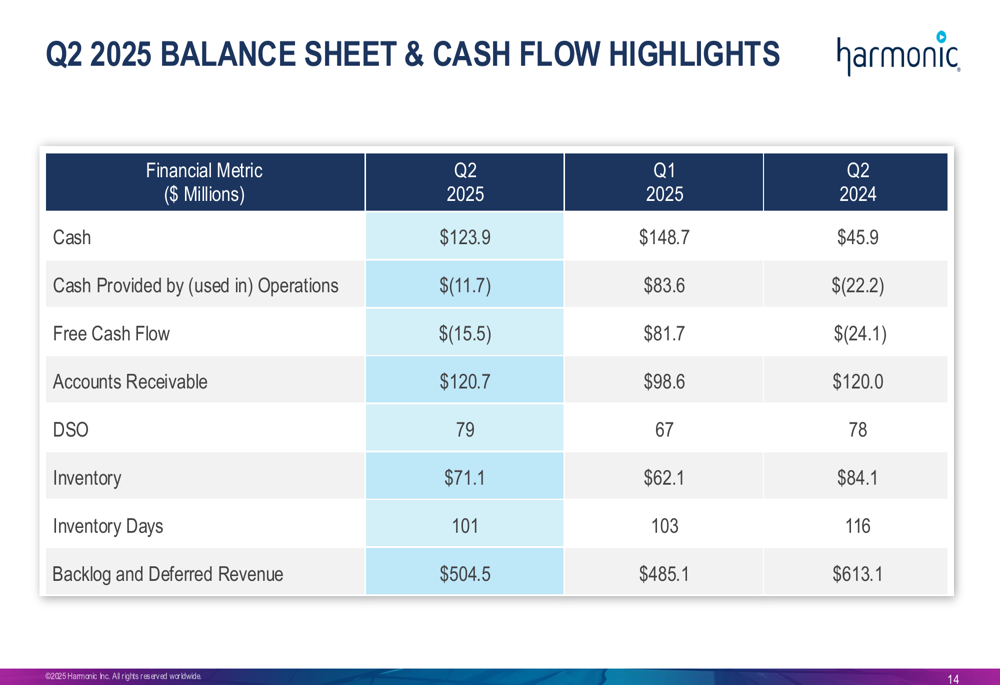

Harmonic’s balance sheet showed considerable strength, with cash increasing to $123.9 million from $45.9 million in Q2 2024. This improvement comes despite negative free cash flow of $15.5 million in the quarter, suggesting strong cash generation in previous periods.

Segment Analysis: Broadband vs. Video

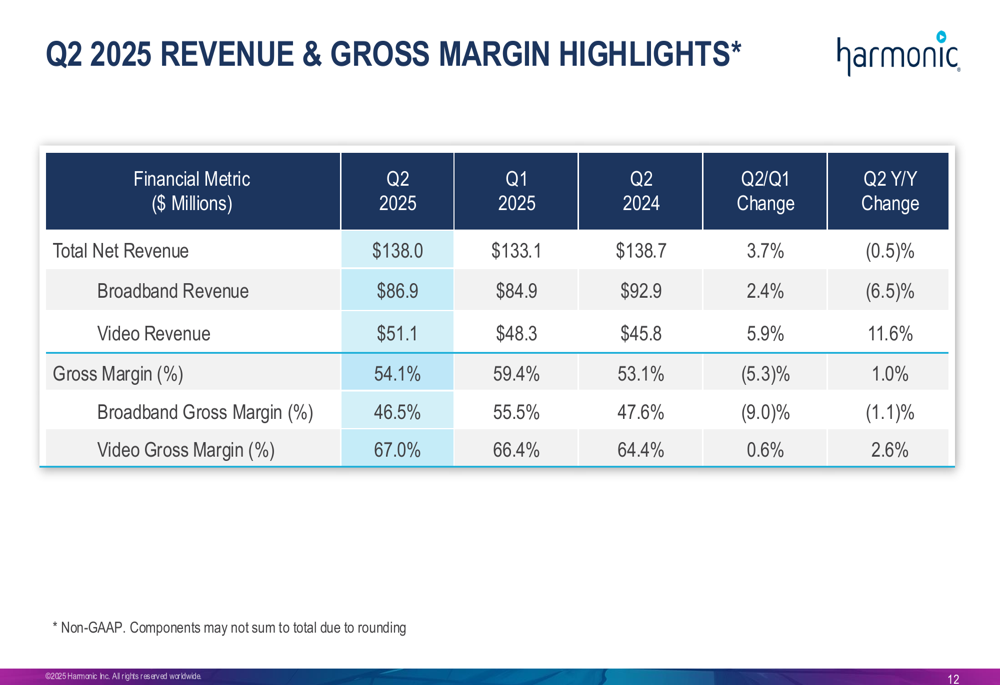

The company’s two main business segments showed divergent performance in Q2 2025. Broadband revenue declined 6.5% year-over-year to $86.9 million, while Video revenue grew 11.6% to $51.1 million. This pattern is clearly illustrated in the revenue and margin breakdown:

Broadband segment challenges were attributed to the industry’s transition to Unified DOCSIS 4.0 technology and tariff impacts. Despite these headwinds, Harmonic reported four new customer wins and strong Rest of World (ROW) bookings, suggesting the foundation for future growth remains solid.

The Video segment continued its positive trajectory, with SaaS revenue reaching a record $15.4 million, up 10.1% year-over-year. Video Adjusted EBITDA showed remarkable improvement, reaching $6.2 million compared to a $0.3 million loss in the same period last year.

Strategic Initiatives & Technology Leadership

Harmonic emphasized its strategic positioning for long-term growth despite near-term challenges. The company highlighted its technology leadership in Unified DOCSIS 4.0, with initial node shipments expected in late 2025, setting the stage for revenue growth in 2026.

The following overview illustrates Harmonic’s execution strategy and key initiatives:

In the Broadband segment, Harmonic is focusing on customer diversification, technology leadership, fiber growth, and cloud services expansion. The company reported record fiber revenue in Q2, including contributions from a recent Tier 1 customer win.

For the Video segment, Harmonic is pursuing a dual strategy of maintaining appliance profitability while accelerating SaaS transformation. The Akamai (NASDAQ:AKAM) partnership is expected to drive growth in the second half of 2025, and the company reported a strong Tier 1 pipeline.

Financial Outlook & Guidance

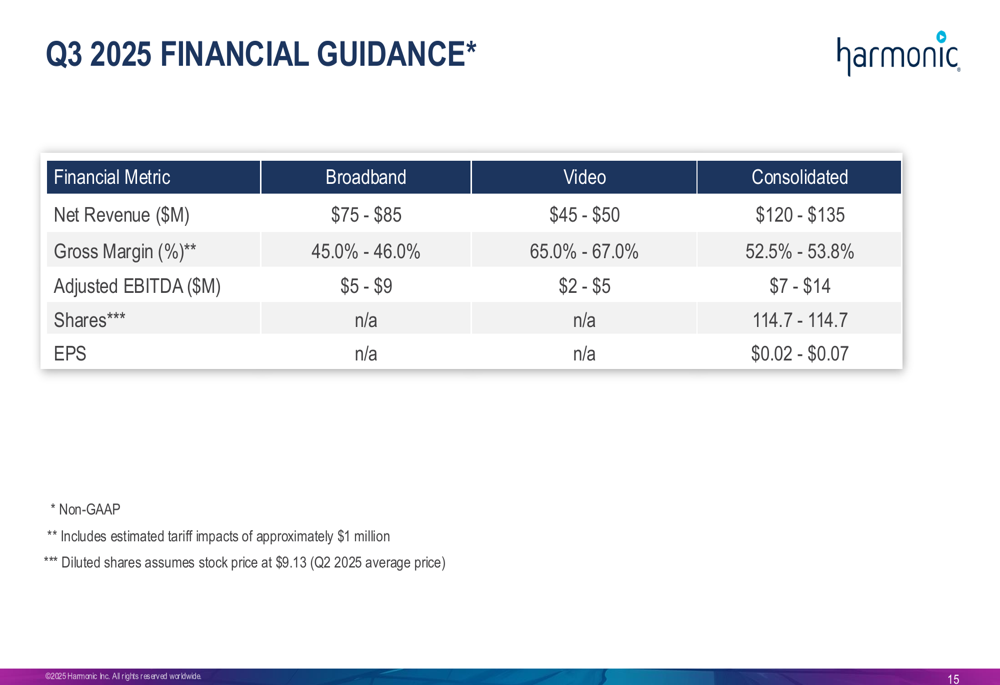

Looking ahead to Q3 2025, Harmonic provided the following guidance:

The company expects Q3 2025 consolidated revenue between $120-$135 million, with Broadband contributing $75-$85 million and Video adding $45-$50 million. Adjusted EBITDA is projected at $7-$14 million, with EPS ranging from $0.02 to $0.07.

Harmonic’s guidance includes estimated tariff impacts of approximately $1 million, reflecting ongoing challenges in this area. Despite these near-term headwinds, management expressed confidence in a growth rebound in 2026, driven by the Unified DOCSIS 4.0 rollout and customer ramps.

The company continues to prioritize shareholder returns, having repurchased $14 million in stock during Q2 2025, bringing year-to-date repurchases to $50 million. With $124 million in cash and an $82 million undrawn credit facility, Harmonic maintains significant financial flexibility to navigate current challenges while investing in future growth opportunities.

In conclusion, while Harmonic faces short-term revenue pressure in its Broadband segment, the company’s strong bookings, improving Video segment performance, and solid balance sheet position it well for the anticipated growth rebound in 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.