Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Harvard Bioscience (NASDAQ:HBIO) presented its second quarter 2025 earnings results on August 11, 2025, highlighting improved profitability metrics despite ongoing revenue challenges. The company’s stock closed at $0.528 on August 8, significantly below its 52-week high of $3.27, but showing some recovery from its low of $0.281. In premarket trading on the day of the earnings presentation, the stock was down 5.3% to $0.5.

The life sciences tools provider continues to navigate a challenging macroeconomic environment characterized by funding uncertainties in the Americas, instability in European markets, and tariff impacts in China. Despite these headwinds, the company has maintained its focus on cost discipline and new product adoption.

Quarterly Performance Highlights

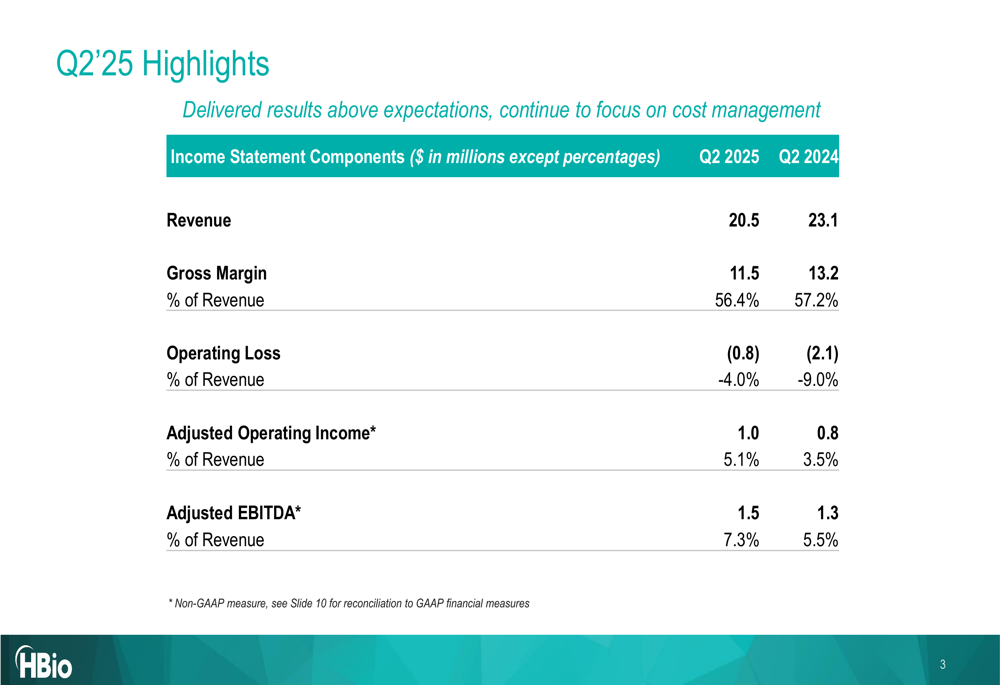

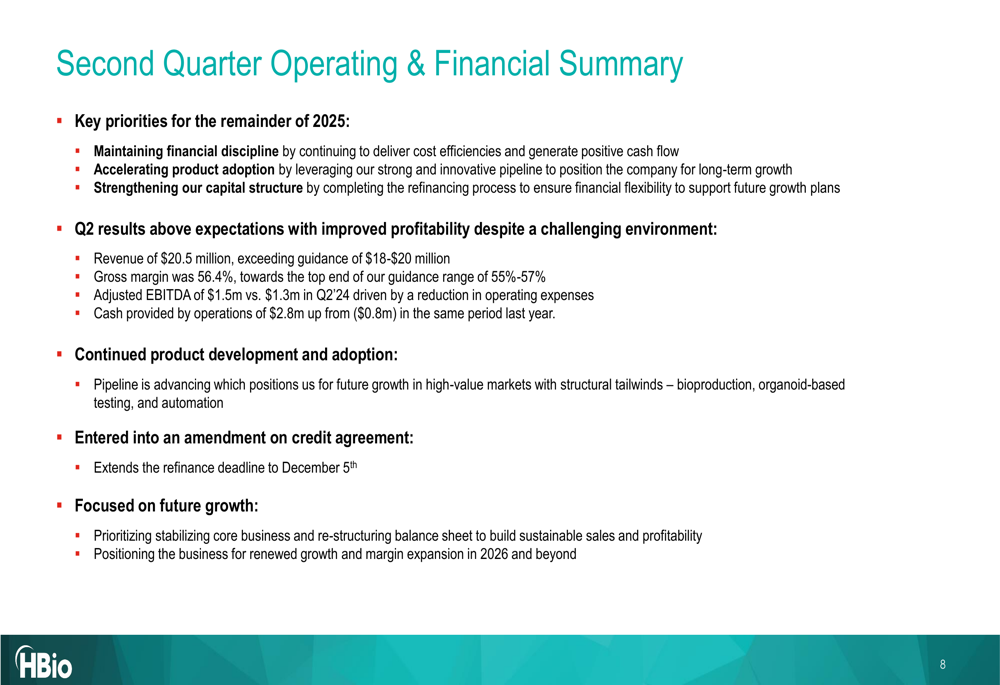

Harvard Bioscience reported Q2 2025 revenue of $20.5 million, down from $23.1 million in the same period last year but demonstrating sequential stability compared to recent quarters. Despite the revenue decline, the company improved its operating loss to $(0.8) million or -4.0% of revenue, compared to $(2.1) million or -9.0% in Q2 2024.

As shown in the following financial highlights table, adjusted profitability metrics showed improvement year-over-year:

The company’s adjusted operating income increased to $1.0 million (5.1% of revenue) from $0.8 million (3.5%) in the prior year, while adjusted EBITDA rose to $1.5 million (7.3%) from $1.3 million (5.5%). These improvements reflect the company’s ongoing cost management initiatives despite top-line pressure.

Detailed Financial Analysis

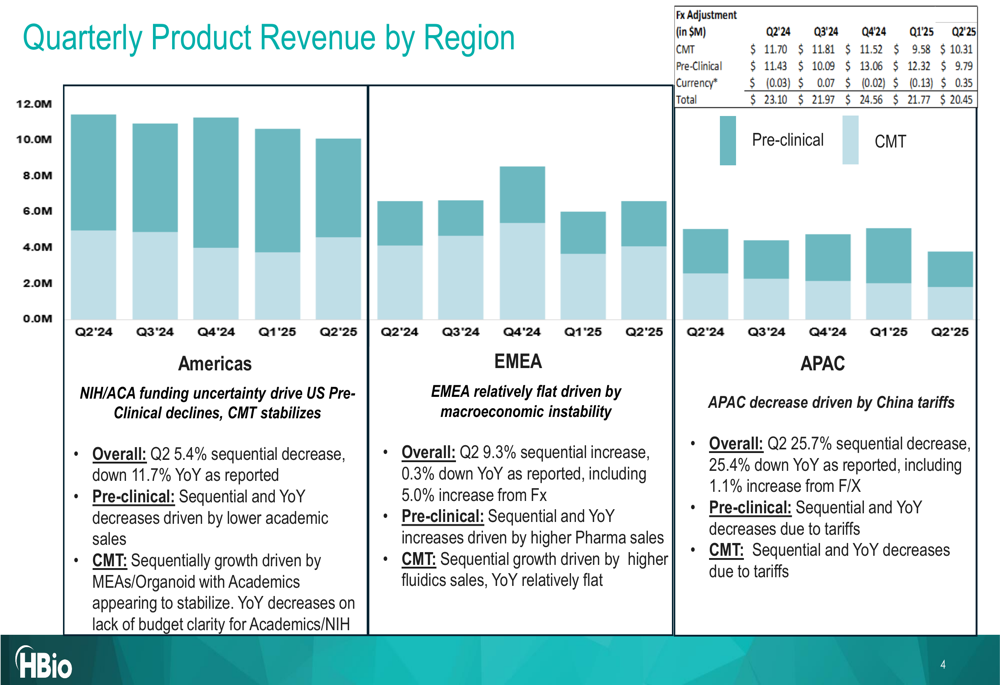

Harvard Bioscience’s regional performance revealed varying challenges across markets. The Americas region experienced an 11.7% year-over-year decline, driven by NIH/ACA funding uncertainties affecting pre-clinical sales. EMEA remained relatively flat with a 0.3% year-over-year decline as reported (including a 5.0% positive impact from foreign exchange), while APAC saw a significant 25.4% decline primarily due to China tariffs.

The following regional breakdown illustrates these trends:

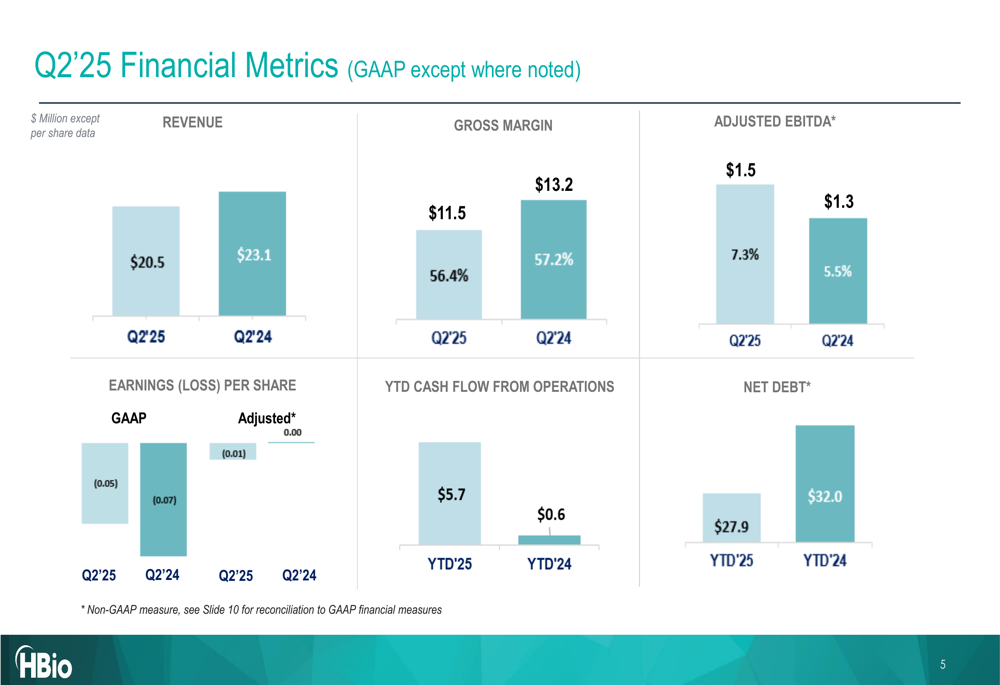

On a positive note, the company reported strong cash flow generation, with year-to-date cash flow from operations reaching $5.7 million, a substantial improvement from $0.6 million in the same period last year. This cash flow strength has enabled Harvard Bioscience to reduce its net debt to $27.9 million, down from $32.0 million in the prior year.

The company’s key financial metrics are summarized in the following chart:

While GAAP earnings per share remained negative at -0.05 for Q2 2025, this represented an improvement from -0.07 in Q2 2024. Adjusted EPS was -0.01, down slightly from 0.00 in the prior year period.

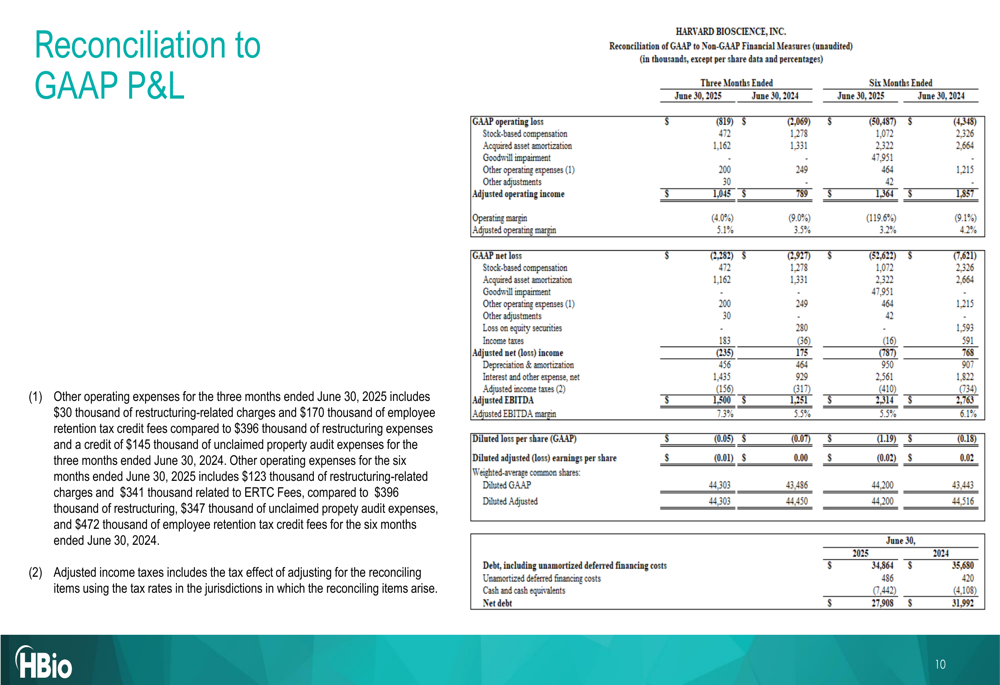

For a complete reconciliation of GAAP to non-GAAP measures, the company provided the following detailed breakdown:

Strategic Initiatives

Harvard Bioscience emphasized three key priorities for the remainder of 2025: maintaining financial discipline, accelerating product adoption, and strengthening its capital structure. The company recently entered into an amendment on its credit agreement, extending the refinance deadline to December 5th.

The following summary highlights the company’s strategic focus areas:

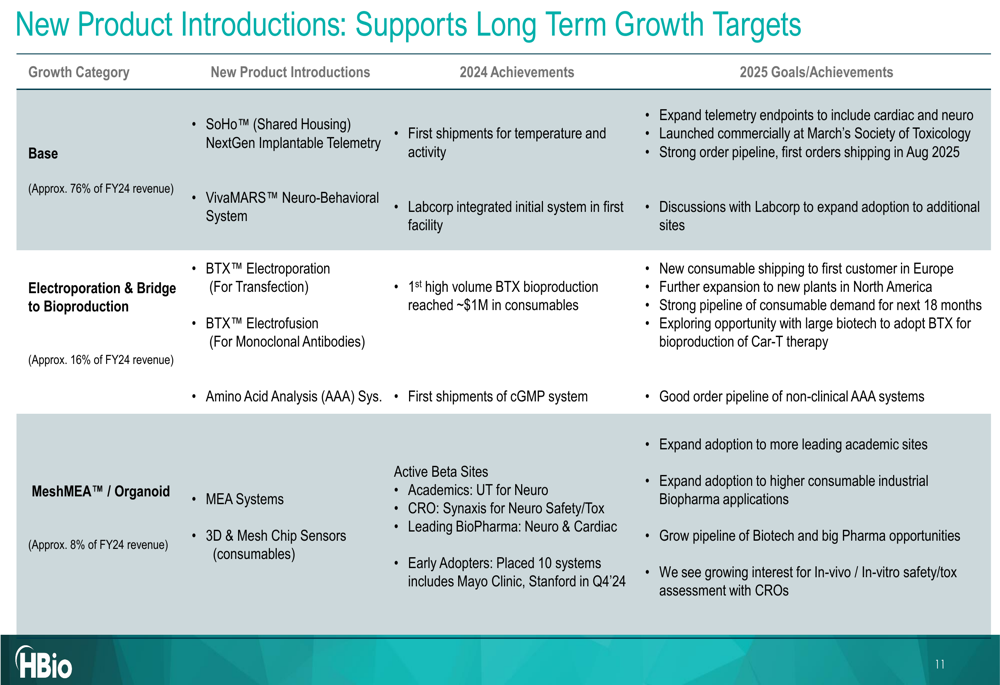

Product development remains a cornerstone of Harvard Bioscience’s long-term growth strategy. The company is advancing its product pipeline in three key categories: Base products, Electroporation & Bridge to Bioproduction, and MeshMEAT™/Organoid technologies. These innovations position the company for future growth in high-value markets with structural tailwinds.

The company’s product roadmap is outlined below:

Notable product introductions include the SohoTM Shared Housing system, VivaMARS™ Neuro-Behavioral System, BTX™ Electroporation and Electrofusion technologies, and advanced MEA Systems with 3D & Mesh Chip Sensors. These innovations align with the company’s strategy to capitalize on emerging trends in bioproduction and alternative testing methods.

Forward-Looking Statements

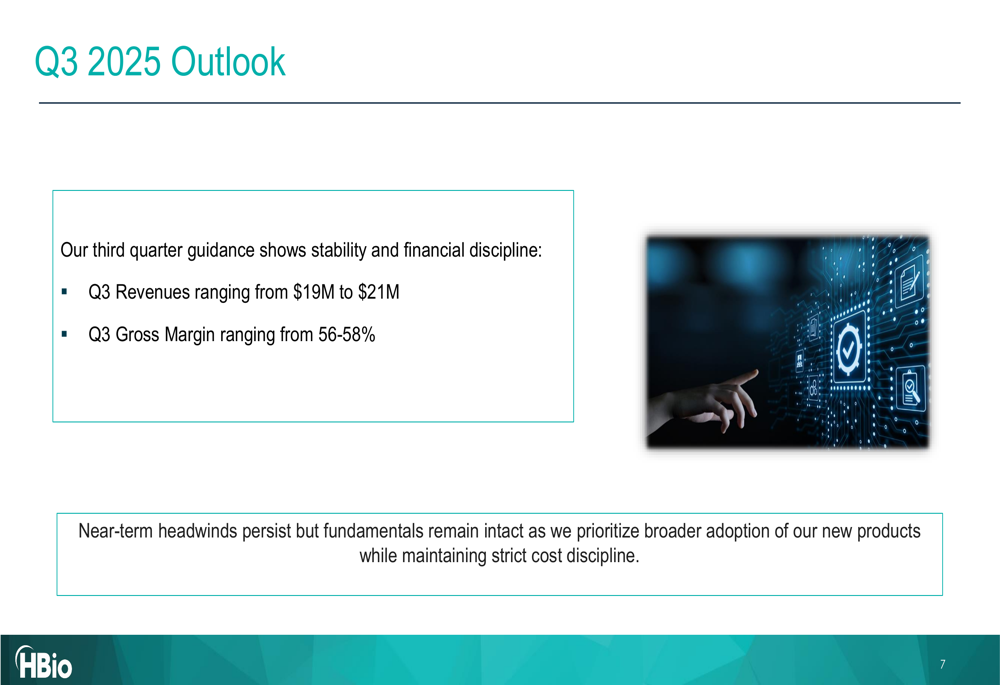

Looking ahead to Q3 2025, Harvard Bioscience provided revenue guidance of $19 million to $21 million with projected gross margins of 56-58%. This outlook reflects the company’s expectation that near-term headwinds will persist while it prioritizes broader adoption of new products and maintains strict cost discipline.

The company’s Q3 outlook is summarized as follows:

Management emphasized that while challenges remain, the fundamentals of the business remain intact. The focus on financial discipline has yielded improved profitability metrics despite revenue pressures, and the company continues to advance its product pipeline to position itself for future growth.

Harvard Bioscience’s approach reflects a balanced strategy of navigating current market challenges while investing in innovation and strengthening its financial position for long-term success. Investors will be watching closely to see if the company’s cost discipline and product strategy can drive sustainable improvement in both top-line performance and profitability in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.