S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Hannon Armstrong Sustainable Infrastructure Capital Inc (NYSE:HASI) released its first quarter 2025 earnings presentation on May 7, highlighting 12% year-over-year growth in managed assets while maintaining strong asset yields despite market fluctuations. The sustainable infrastructure investor reaffirmed its long-term growth guidance while emphasizing its resilience to potential policy and economic headwinds.

Quarterly Performance Highlights

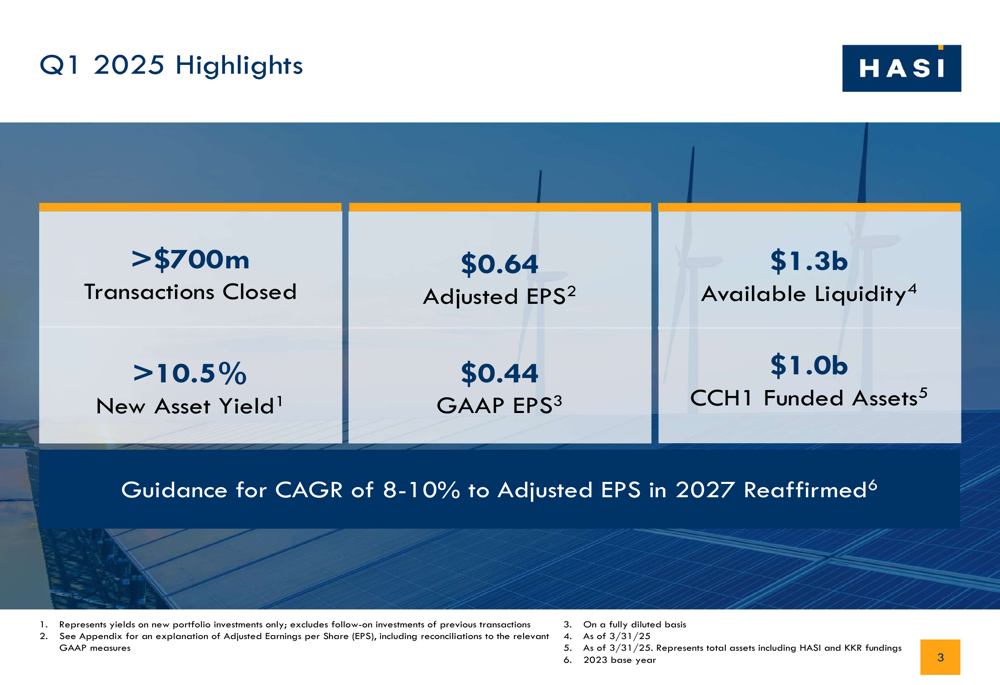

HASI reported Q1 2025 adjusted earnings per share of $0.64, compared to $0.68 in the same period last year. GAAP EPS came in at $0.44, down from $0.98 in Q1 2024. The company attributed the year-over-year decrease primarily to elevated gains on sale in Q1 2024 driven by its targeted asset rotation strategy.

The company closed more than $700 million in transactions during the quarter while maintaining new asset yields above 10.5%, consistent with its performance throughout 2024. Recurring income from adjusted net investment income and securitization asset income grew by a combined 14% year-over-year to $79 million.

As shown in the following quarterly highlights slide, HASI maintained strong liquidity of $1.3 billion while funding $1.0 billion in CCH1 assets:

The company’s managed assets reached $14.5 billion, representing 12% growth year-over-year. The portfolio composition remains diversified across multiple sustainable infrastructure segments, with residential solar, grid-connected solar, and onshore wind representing the largest portions of the portfolio.

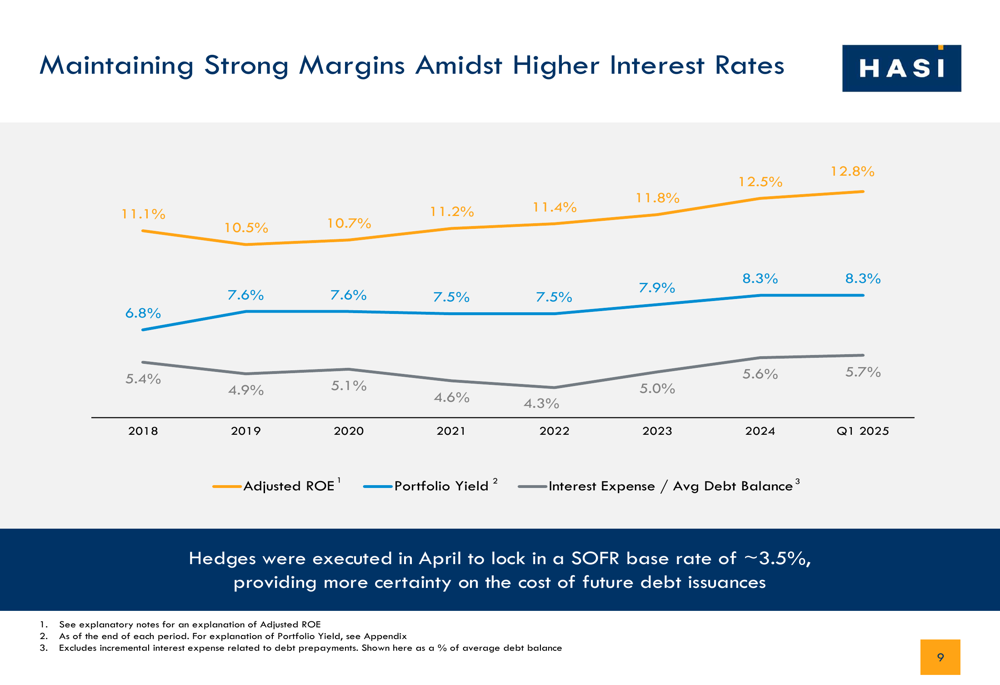

HASI’s portfolio yield continued its upward trajectory, reaching 8.3% in Q1 2025 compared to 6.8% in 2018, demonstrating the company’s ability to adapt to the higher interest rate environment while maintaining strong margins.

As illustrated in the following chart, HASI has successfully maintained strong margins despite the rising interest rate environment:

Strategic Positioning and Pipeline

HASI emphasized its minimal exposure to potential tariff dislocations, noting that its existing portfolio has "de minimis impact" as projects are already in operation or have parts procured. For its pipeline, the company indicated it is "largely protected" with most projects completed or under construction and secured component supply for near-term projects.

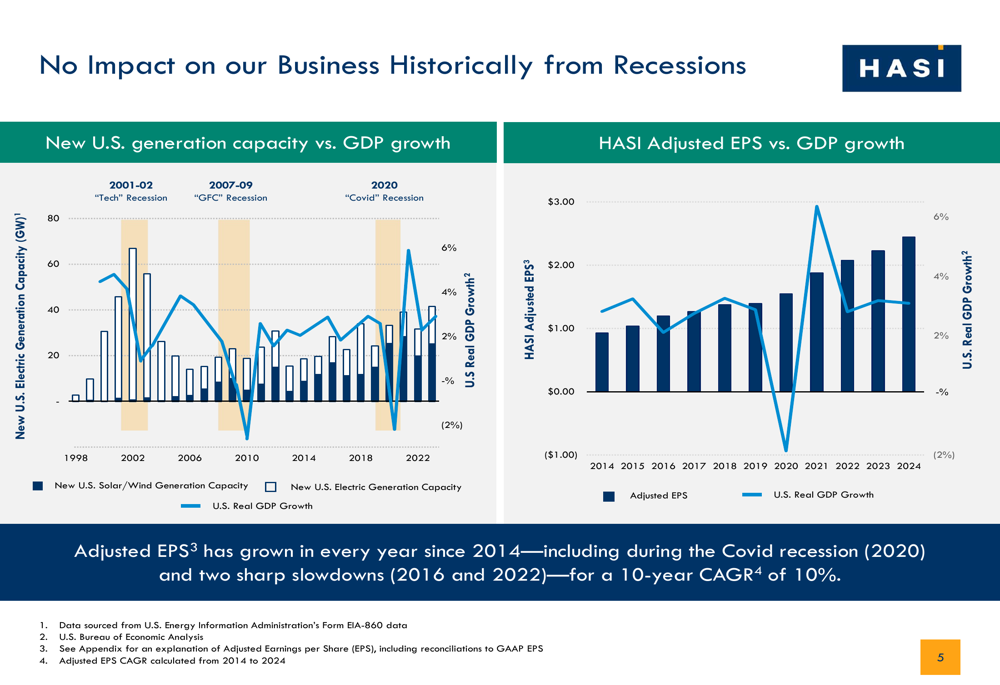

The company highlighted its historical resilience during economic downturns, showing that its adjusted EPS has grown consistently every year since 2014, including through the COVID-19 recession in 2020 and economic slowdowns in 2016 and 2022.

This historical performance during economic challenges is illustrated in the following chart:

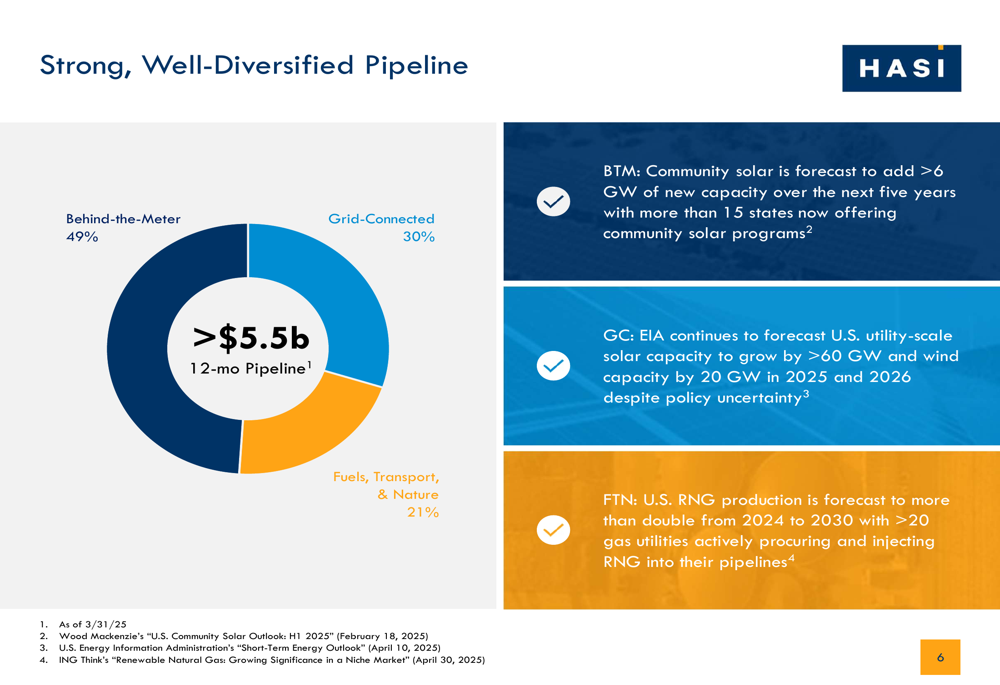

HASI reported a strong and diversified pipeline exceeding $5.5 billion over the next 12 months, broken down into three segments: Behind-the-Meter (49%), Grid-Connected (30%), and Fuels, Transport, & Nature (21%). The company highlighted significant growth opportunities across these segments, including community solar expected to add more than 6 GW of new capacity, utility-scale solar forecast to grow by more than 60 GW, and U.S. renewable natural gas production projected to more than double from 2024 to 2030.

The composition of HASI’s pipeline is visualized in the following chart:

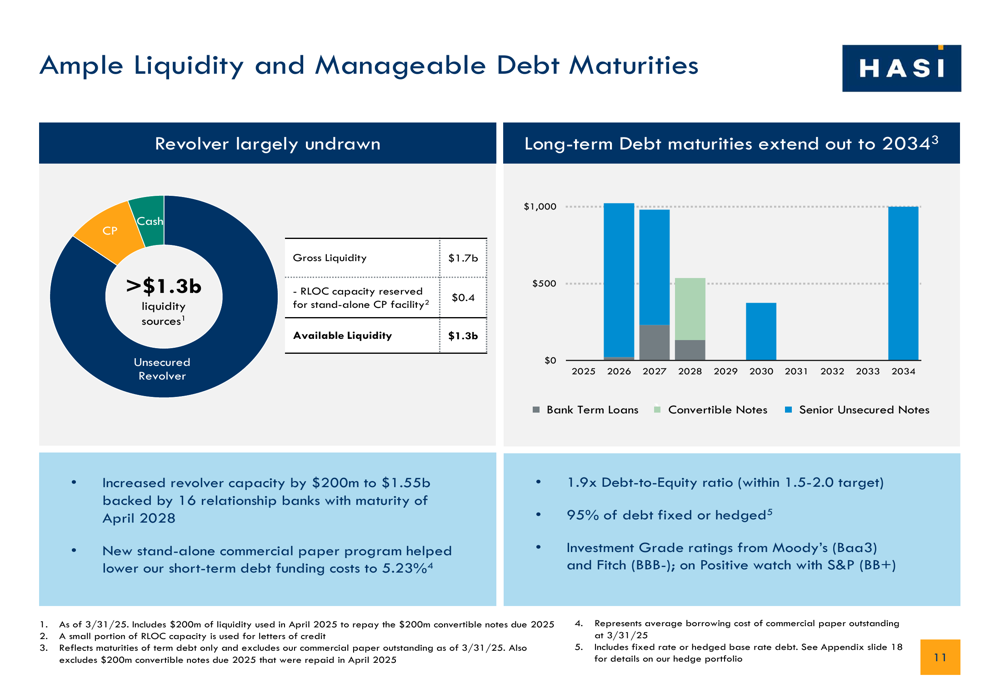

Financial Resilience and Liquidity

HASI maintained a strong financial position with $1.3 billion in available liquidity as of March 31, 2025. The company increased its revolver capacity by $200 million to $1.55 billion, backed by 16 relationship banks with maturity in April 2028. It also implemented a new stand-alone commercial paper program that helped lower short-term debt funding costs to 5.23%.

The company’s debt-to-equity ratio stood at 1.9x, within its target range of 1.5-2.0x. Approximately 95% of HASI’s debt is fixed or hedged, providing stability in the face of interest rate fluctuations. The company maintains investment grade ratings from Moody’s (Baa3) and Fitch (BBB-), with a positive watch from S&P (BB+).

HASI’s liquidity position and debt maturity profile are detailed in the following slide:

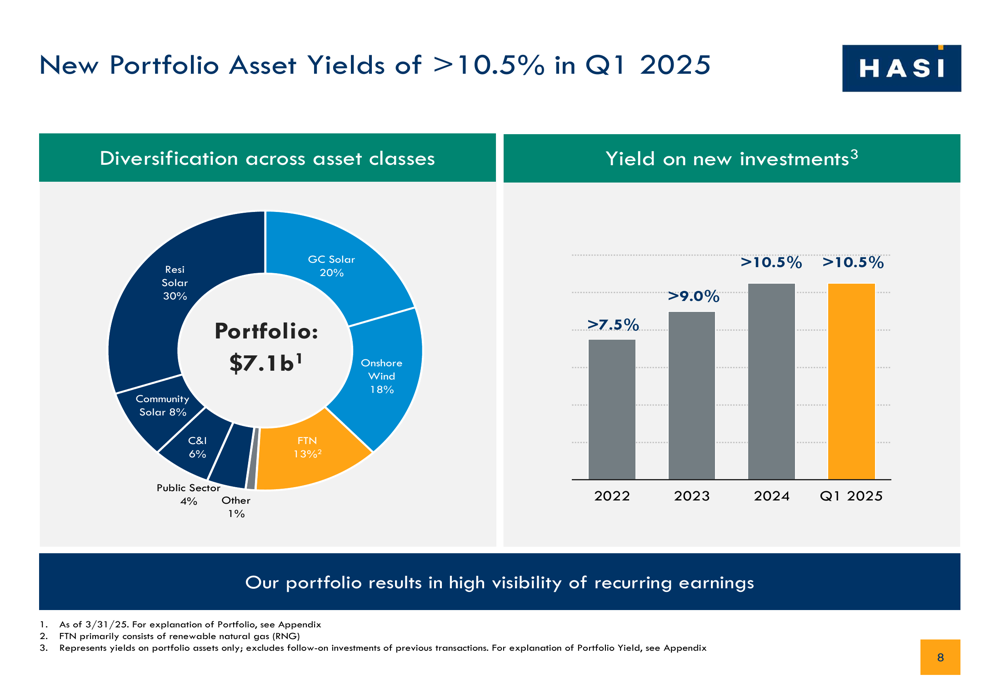

The company’s portfolio value reached $7.1 billion, with a diverse mix of asset classes including residential solar (30%), grid-connected solar (20%), onshore wind (18%), and fuels, transport & nature (13%). New portfolio asset yields remained strong at over 10.5% in Q1 2025, consistent with 2024 and significantly higher than the >7.5% yields in 2022.

The portfolio composition and yield trends are illustrated in this chart:

Forward-Looking Statements

HASI reaffirmed its guidance of 8-10% compound annual growth rate (CAGR) in adjusted EPS from 2024 to 2027. The company emphasized its resilient business model supported by a strong funding platform, manageable public policy impact, and interest rate adaptability.

In April 2025, HASI executed hedges to lock in a SOFR base rate of approximately 3.5%, providing more certainty on the cost of future debt issuances. This strategic move demonstrates the company’s proactive approach to managing interest rate risks.

The company also highlighted its sustainability impact, reporting that its investments have resulted in 8.4 million metric tons of CO2 avoided annually and 7.4 billion gallons of water saved annually as of Q1 2025. HASI published its seventh annual Sustainability & Impact Report during the quarter.

In the after-hours trading session following the earnings release, HASI stock was down 2.31% to $25.16, according to available market data. The stock has traded between $21.98 and $36.56 over the past 52 weeks.

With its diversified portfolio, strong pipeline, and maintained guidance, HASI appears well-positioned to navigate potential market uncertainties while continuing to capitalize on growth opportunities in sustainable infrastructure.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.