JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

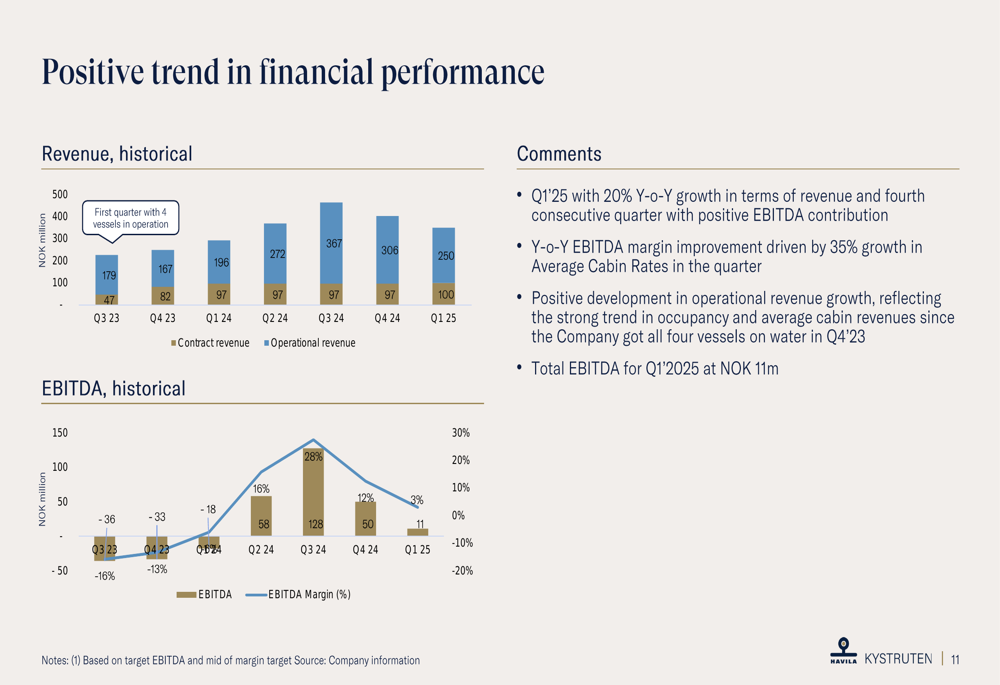

Havila Kystruten AS (EURONEXT:HKY) reported a 20% year-over-year revenue increase in its Q1 2025 results presentation delivered on May 27, 2025. The Norwegian coastal cruise operator achieved its fourth consecutive quarter of positive EBITDA, continuing its financial turnaround despite seasonal challenges in the winter quarter.

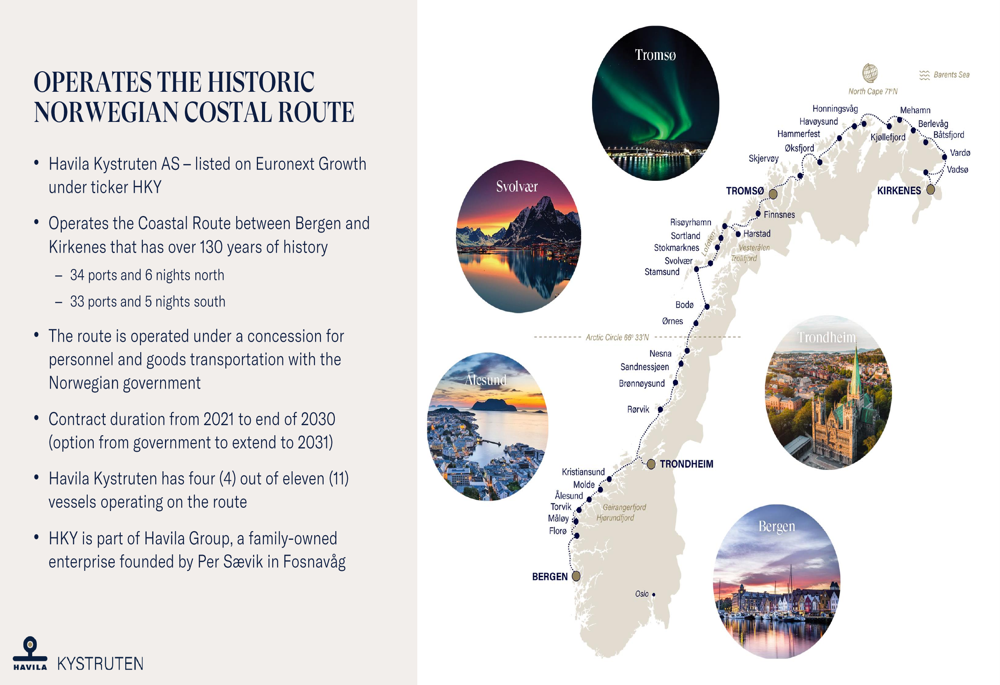

The company’s stock closed at 1.10 on the presentation day, up 0.91% from the previous close, reflecting investor confidence in the company’s improving financial trajectory. Havila operates four vessels along the historic Norwegian coastal route under a government concession running through 2030.

Quarterly Performance Highlights

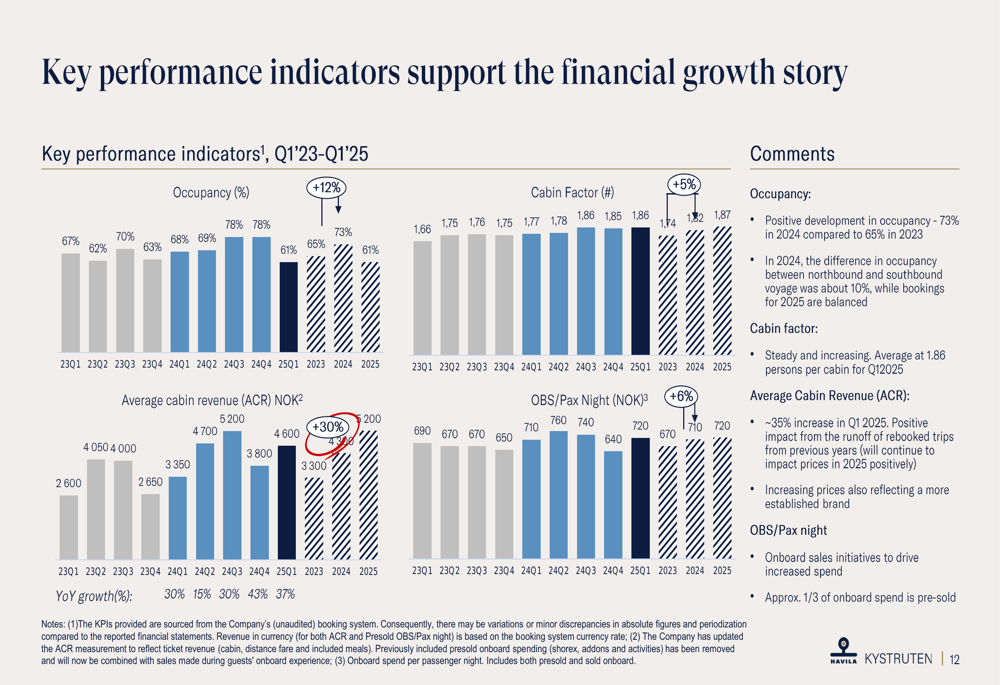

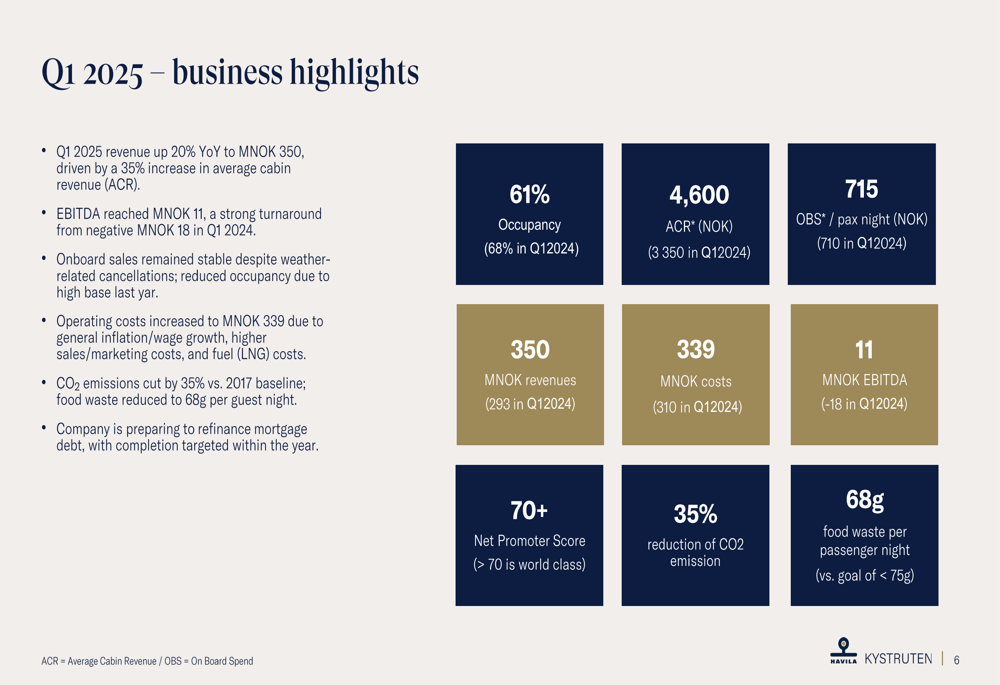

Havila Kystruten reported Q1 2025 revenue of 350 million NOK, up 20% from 293 million NOK in Q1 2024. This growth was primarily driven by a 35% increase in Average Cabin Revenue (ACR), which reached 4,600 NOK compared to 3,350 NOK in the same period last year.

The company achieved an EBITDA of 11 million NOK, a significant improvement from the negative 18 million NOK reported in Q1 2024. This marks the fourth consecutive quarter of positive EBITDA, demonstrating the company’s continued financial recovery.

As shown in the following revenue and EBITDA performance chart:

Operating costs increased to 339 million NOK due to general inflation, wage growth, higher sales and marketing expenses, and fuel costs. Occupancy decreased to 61% from 68% in Q1 2024, which the company attributed to a high base effect from last year.

The detailed breakdown of key performance indicators reveals the company’s operational trends:

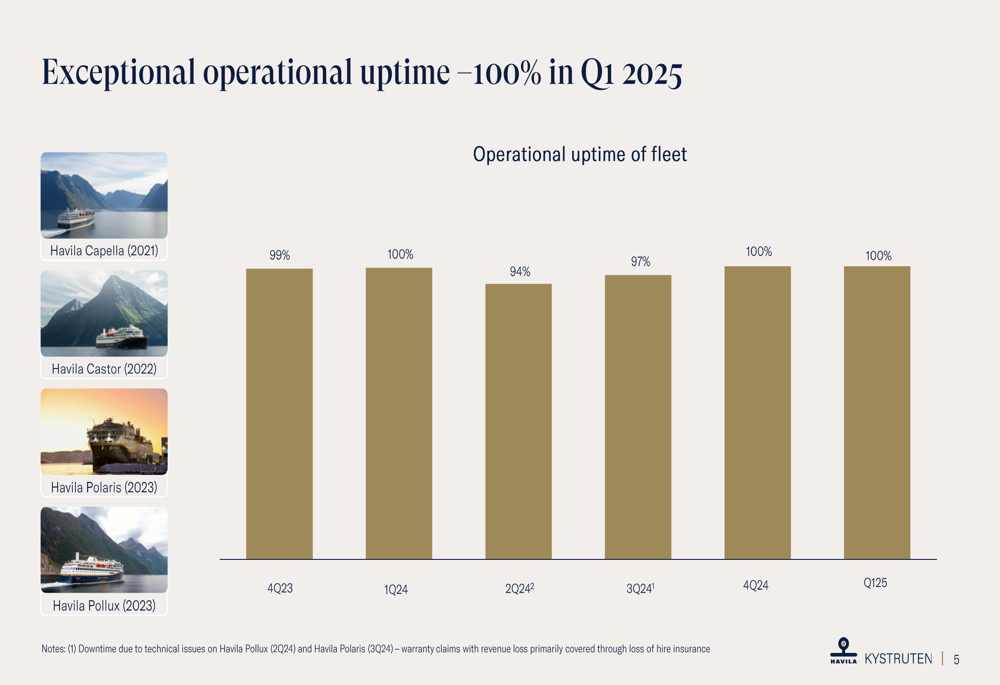

Havila maintained exceptional operational reliability with 100% uptime in Q1 2025, continuing the strong performance from the previous quarter:

Strategic Initiatives

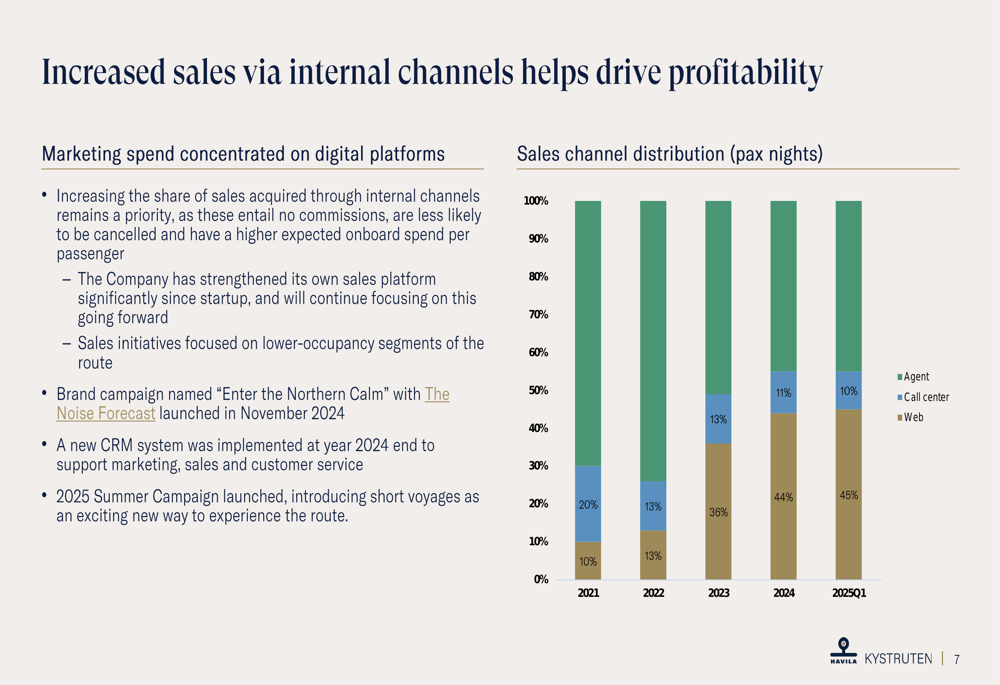

Havila Kystruten is implementing several strategic initiatives to improve profitability. A key focus has been increasing direct sales through internal channels, which reduces commission costs and typically leads to higher onboard spending per passenger.

The following chart illustrates the company’s progress in shifting sales from agents to direct channels:

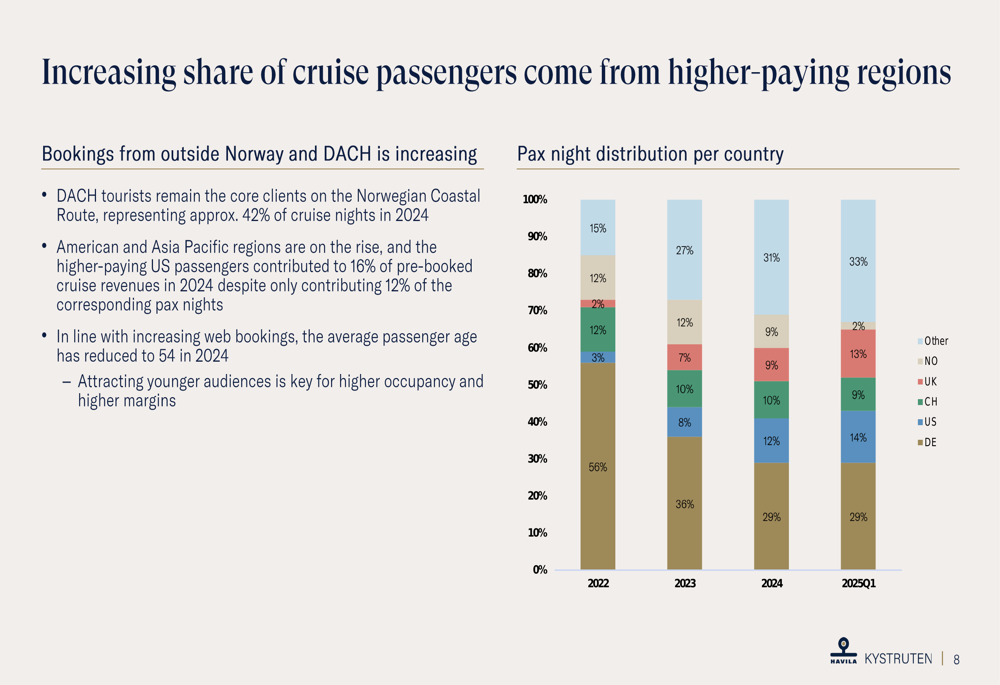

The company is also benefiting from a changing passenger mix, with an increasing proportion of travelers coming from higher-paying regions such as the United States and Asia Pacific. The U.S. market share has grown from 4% in 2022 to 14% in Q1 2025, while the traditionally dominant German market has decreased from 56% to 28% during the same period.

Sustainability remains a core focus, with CO2 emissions reduced by 35% compared to the 2017 baseline. Food waste has been reduced to 68 grams per guest night, below the company’s target of 75 grams. These achievements have contributed to several industry recognitions, including first place in the Sustainability category at the Kreuzfahrtguide Awards.

Forward-Looking Statements

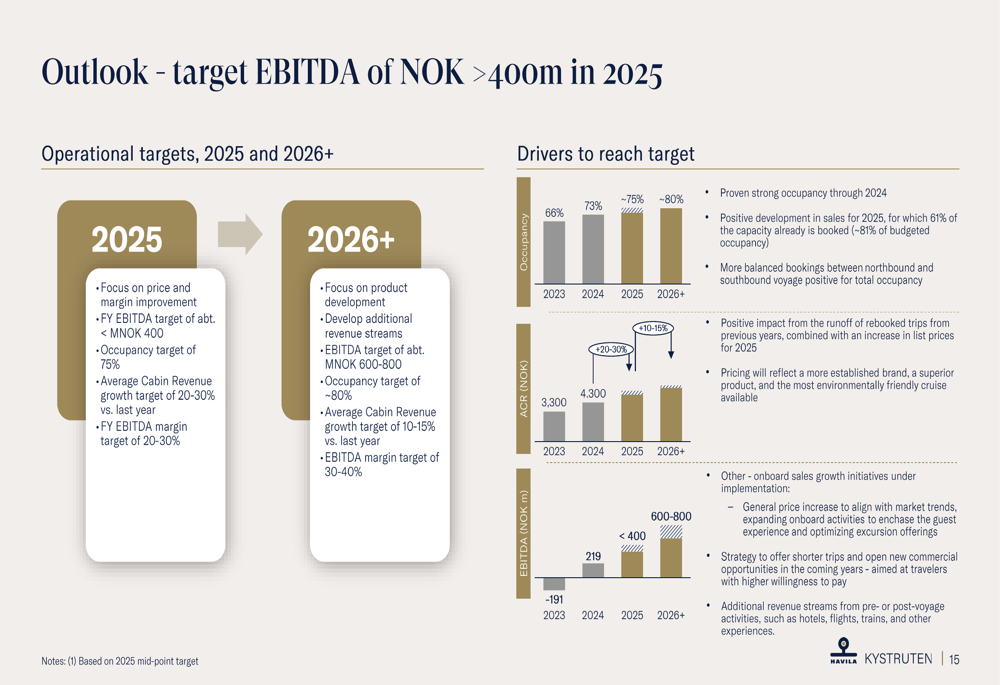

Havila Kystruten presented an optimistic outlook for 2025 and beyond. The company has already secured 81% of its target capacity for 2025, with current bookings at 61% of total capacity. Occupancy for Q2 2025 is tracking at 73%, compared to 69% for the same period last year.

For full-year 2025, Havila targets an EBITDA exceeding 400 million NOK, with an occupancy rate of approximately 75% and continued ACR growth of 20-30%. Looking further ahead to 2026 and beyond, the company aims to achieve an EBITDA of 600-800 million NOK with 80% occupancy and 10-15% ACR growth.

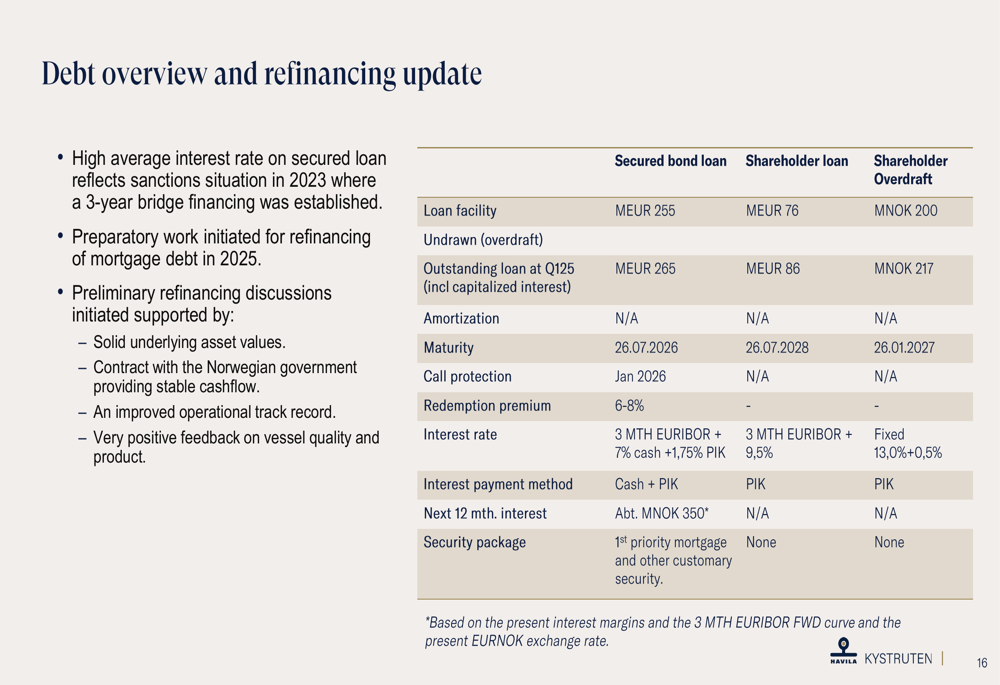

The company is also preparing to refinance its mortgage debt, with completion targeted within the year. Current debt includes a secured bond loan of 265 million EUR with maturity in July 2026 and an interest rate of 3-month EURIBOR plus 7% cash and 1.75% PIK.

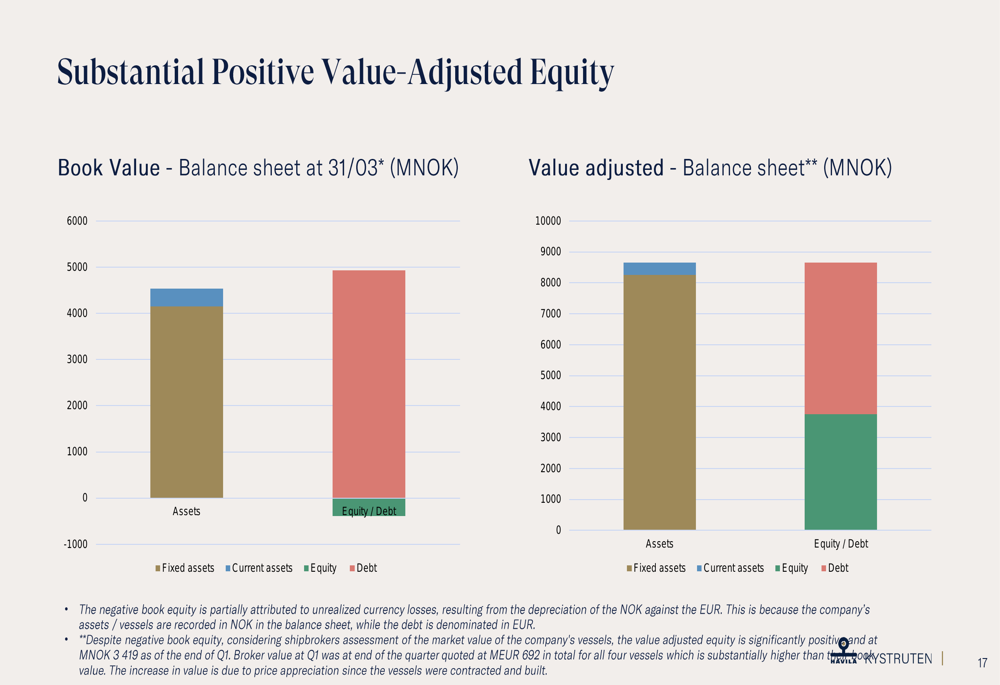

Despite negative book equity, Havila emphasized its substantial positive value-adjusted equity of 3,419 million NOK, based on shipbrokers’ assessment of vessel market values totaling 692 million EUR.

Detailed Financial Analysis

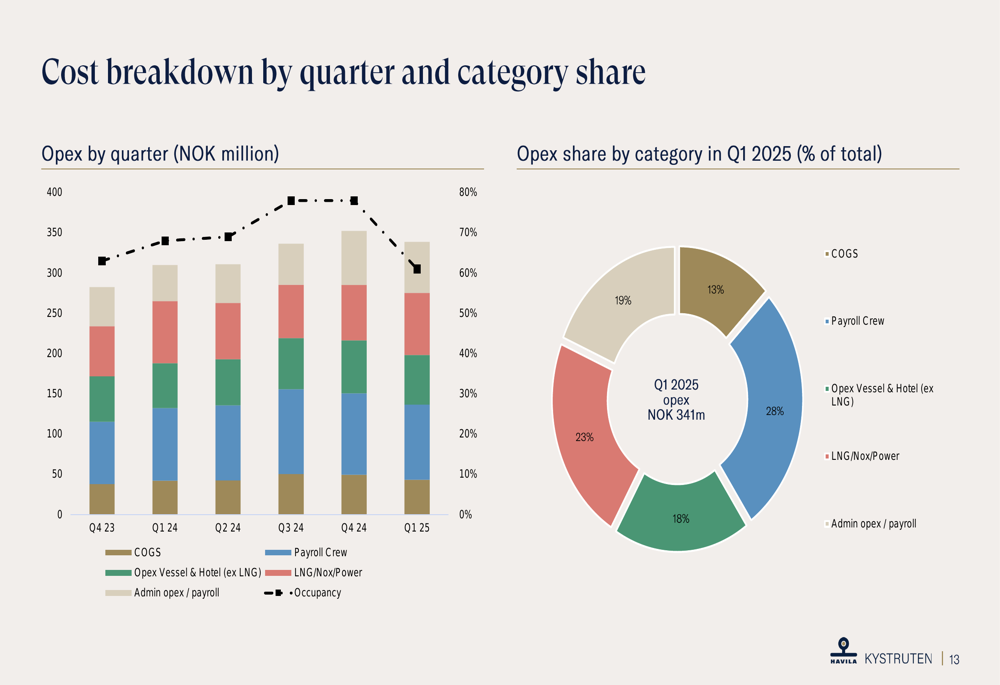

A closer examination of Havila’s cost structure reveals that vessel and hotel operations (excluding LNG) represent the largest expense category at 28% of total operating expenses in Q1 2025, followed by crew payroll at 23% and cost of goods sold at 19%.

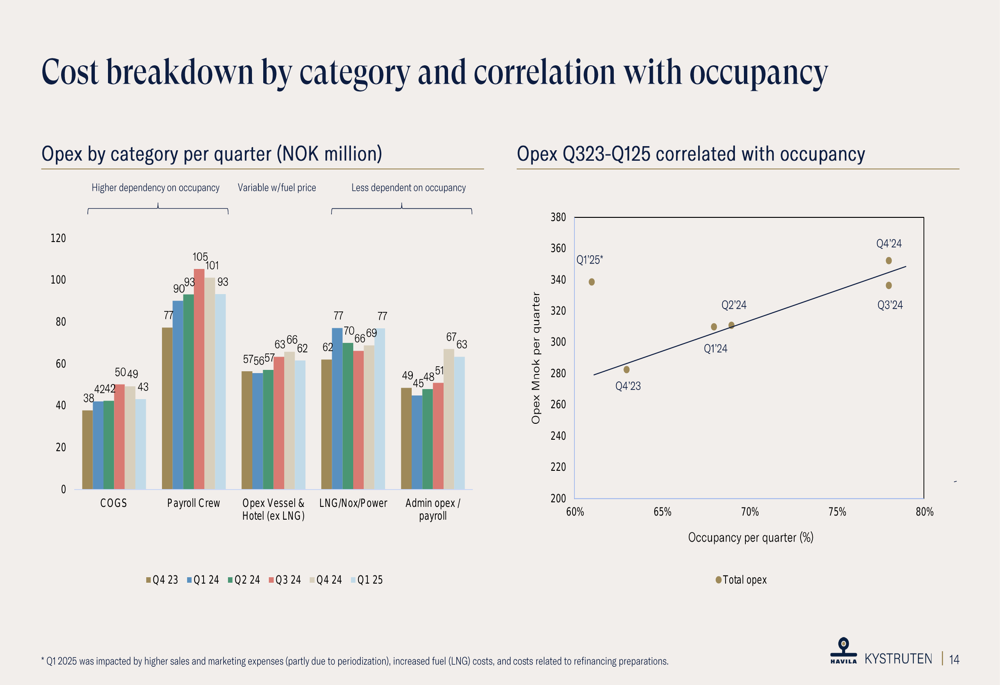

The company has identified a correlation between occupancy rates and operating expenses, providing a path to improved margins as occupancy increases:

Havila’s business highlights for Q1 2025 demonstrate the company’s balanced approach to growth and cost management:

The Norwegian coastal route operated by Havila represents a unique market position, with the company’s four vessels serving 34 ports northbound and 33 ports southbound along Norway’s scenic coastline:

As Havila Kystruten continues its financial recovery and implements its strategic initiatives, the company appears well-positioned to capitalize on growing demand for sustainable cruise experiences in the Norwegian coastal market. With strong forward bookings and a clear focus on higher-yielding passenger segments, the outlook for 2025 and beyond suggests continued improvement in financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.