Gold prices near 3-week high; could reach $4,700/oz - UBS

Introduction & Market Context

Haypp Group AB (STO:HAYPP) presented its Q2 2025 earnings on August 7, 2025, revealing continued growth in its nicotine pouch segment despite market challenges. The company’s stock closed at SEK 139.40, down 5.17% from the previous close of SEK 147, suggesting investors may have concerns about the company’s increased investments impacting short-term profitability.

The presentation, delivered by CEO Gavin O’Dowd and CFO Peter Deli, highlighted the company’s strategic positioning in the growing nicotine pouch market, particularly in the US where regulatory conditions are described as stable and increasingly favorable for compliant online retailers.

Quarterly Performance Highlights

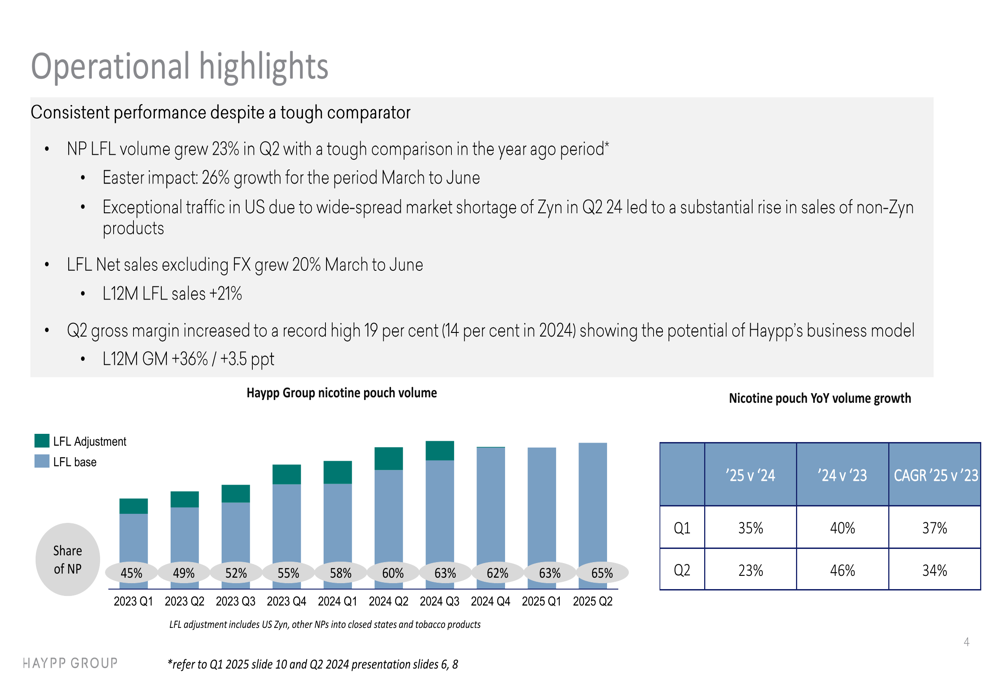

Haypp Group reported solid operational performance in Q2 2025, with nicotine pouch like-for-like (LFL) volume growth of 23% compared to the same period last year. The company noted that LFL net sales excluding foreign exchange effects grew by 20% from March to June, while the last twelve months (L12M) LFL sales increased by 21%.

As shown in the following chart of operational highlights, the company has maintained strong nicotine pouch volume growth:

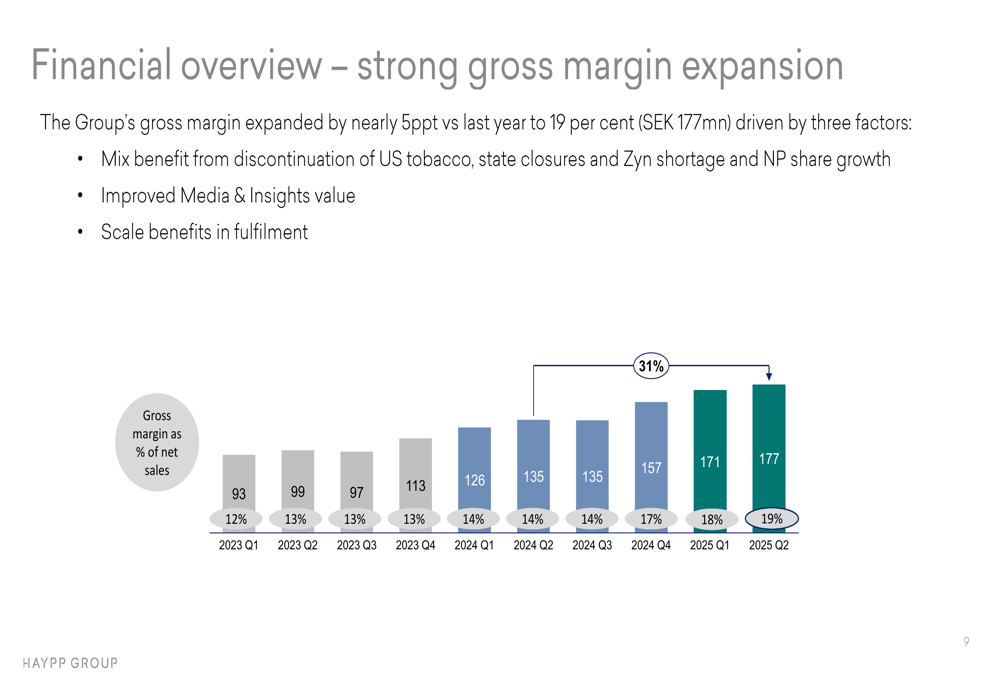

Gross margin showed significant improvement, increasing to 19% in Q2 2025, representing a nearly 5 percentage point expansion compared to the same period last year. This expansion was attributed to three main factors: mix benefits from discontinued US tobacco and state closures, improved media and insights value, and scale benefits in fulfillment operations.

The following chart illustrates the company’s gross margin expansion over time:

Detailed Financial Analysis

Haypp Group’s adjusted EBIT for the second quarter grew by 11% to SEK 38.3 million (34.5), with the adjusted EBIT margin increasing to 4.2% (3.7). However, the company’s overhead base increased to SEK 117 million, representing a 39% increase compared to Q2 2024, primarily driven by US and other growth market initiatives.

The company’s financial performance varied significantly across its market segments:

Core Markets: Net sales increased 4% to SEK 679.3 million, with nicotine pouch volume growing by 15%. EBITDA for this segment was SEK 69.3 million, with a margin of 10.2%.

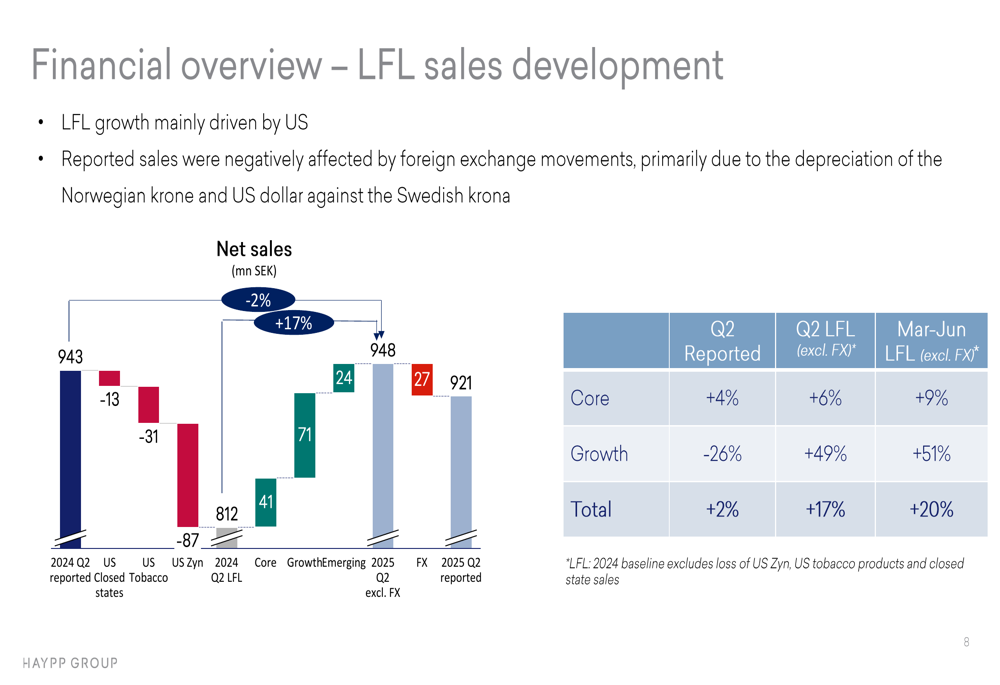

Growth Markets: Reported net sales decreased by 26% to SEK 205.7 million, primarily due to the loss of US Zyn, US tobacco products, and closed state sales. However, nicotine pouch volume grew by 40% on a LFL basis. EBITDA was SEK 3.1 million with a margin of 1.5%.

The following waterfall chart breaks down the components affecting net sales development:

Emerging Markets: Net sales amounted to SEK 36.4 million with growth across all markets (UK, SE, DE). EBITDA was negative at SEK -11.4 million, with a margin of -31.3%, reflecting commercial investments and a high share of fixed costs.

The company maintained a healthy balance sheet with a Net Debt to adjusted EBITDA ratio of 0.4x and inventory turnover at 12x on a last twelve months basis.

Strategic Initiatives

Haypp Group outlined several strategic initiatives, particularly focused on the US market. The company is building out its US team with key hires including a Chief Commercial Officer, Head of Legal, and VP of Regulatory Affairs. Programs are underway to improve consumer retention and loyalty through same-day delivery and revised loyalty programs.

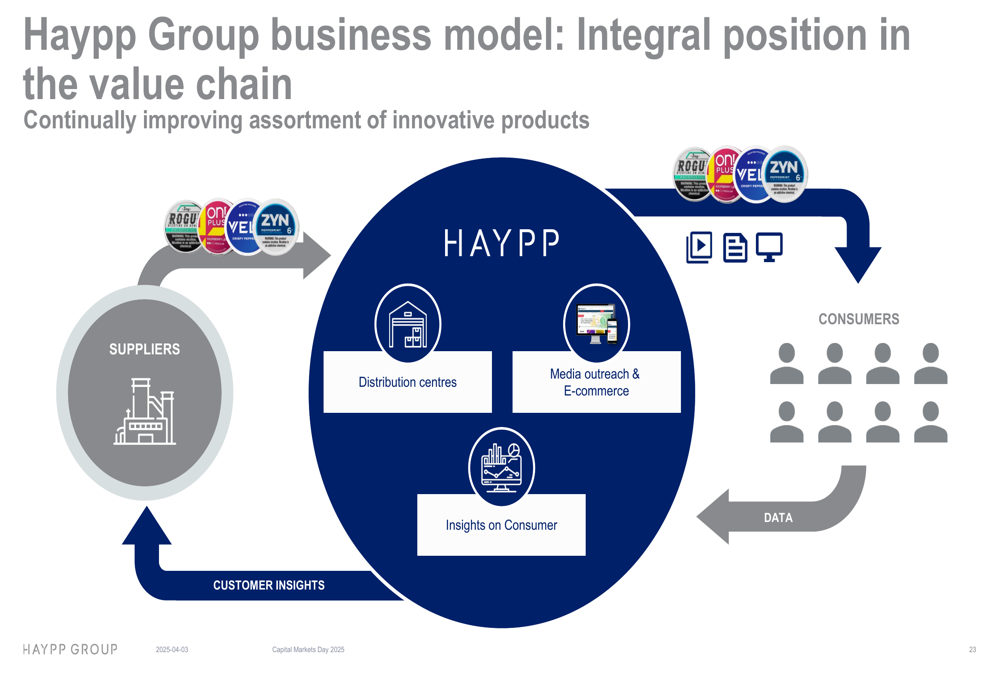

The company’s business model positions it as an integral part of the value chain, connecting suppliers and consumers while providing valuable insights:

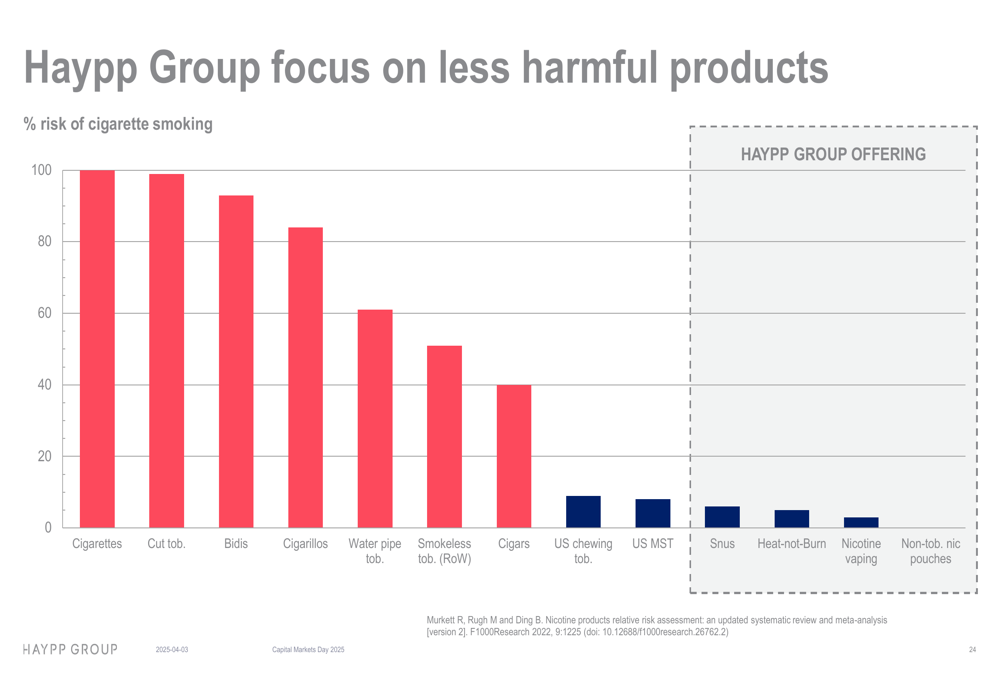

A key component of Haypp’s strategy is its focus on less harmful nicotine products compared to traditional cigarettes:

The company also highlighted its approach to regulatory compliance, noting full compliance with new regulations including the European Commission’s Tobacco Taxation Directive proposal and the UK’s nationwide ban on disposable nicotine vaping devices.

Forward-Looking Statements

Haypp Group maintained its long-term optimism while acknowledging near-term challenges. The company expects US investment to result in lower profit margins in the second half of 2025, which may have contributed to the negative market reaction following the earnings release.

For 2028, Haypp Group has set ambitious financial targets, including:

- Revenue growth of 18-25% CAGR annually (with 2025 growth expected to be below this range)

- Adjusted EBIT margin of 5.5% +/- 150 basis points

- A dividend policy focused on reinvesting cash flows into continued expansion

The company emphasized that long-term fundamentals remain robust for risk-reduced products, for the online channel, and for Haypp specifically. Management believes that tightening legislation will make the company’s commitment to compliance a significant competitive advantage.

This outlook builds on the momentum seen in Q1 2025, when the company reported a 22% increase in like-for-like sales and a 35% rise in nicotine pouch volumes. The Q2 results show continued strength in the nicotine pouch segment, though investors appear cautious about the increased investments and their impact on near-term profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.