Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Helmerich & Payne , Inc. (NYSE:HP) presented its third-quarter fiscal 2025 results on August 7, highlighting strong operational performance while pursuing aggressive debt reduction targets. The global drilling solutions provider reported consolidated adjusted EBITDA of $268 million for the quarter ended June 30, 2025, as it continues to maintain leading market positions in key regions despite a challenging industry environment.

Q3 Performance Highlights

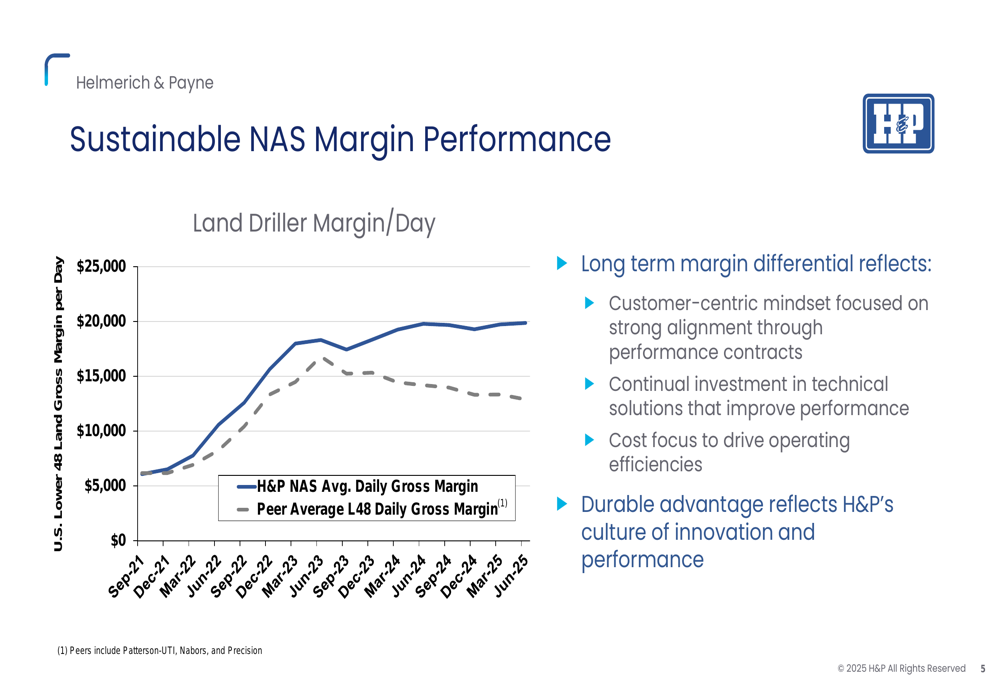

Helmerich & Payne delivered robust financial results in its third fiscal quarter, with its North America Solutions (NAS) segment generating a direct margin of $266 million. The company maintained approximately 50% of its active rigs on performance-based contracts, achieving a daily direct margin of $19,860 with 147 average rigs in operation during the quarter.

"Our North America Solutions segment continues to deliver industry-leading margins, consistently achieving our 50% gross margin target," the company stated in its presentation. This performance comes as H&P pursues significant cost reduction initiatives, having identified over $50 million in savings against an upwardly revised target of $50-75 million.

As shown in the following chart comparing H&P’s margin performance to industry peers:

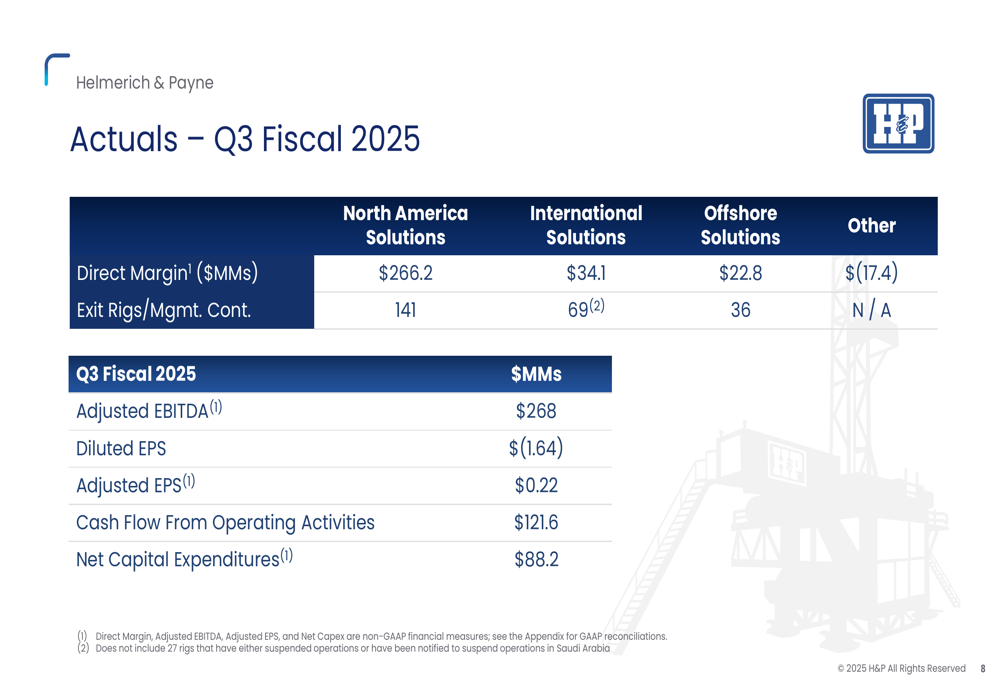

The company’s International and Offshore Solutions segments also performed well, generating a combined direct margin exceeding $55 million. H&P noted that eight FlexRigs are now working in Saudi Arabia, although the presentation mentioned that 27 rigs in Saudi Arabia were either suspended or notified to suspend operations.

The detailed breakdown of Q3 fiscal 2025 actual results shows strong performance across segments:

Competitive Industry Position

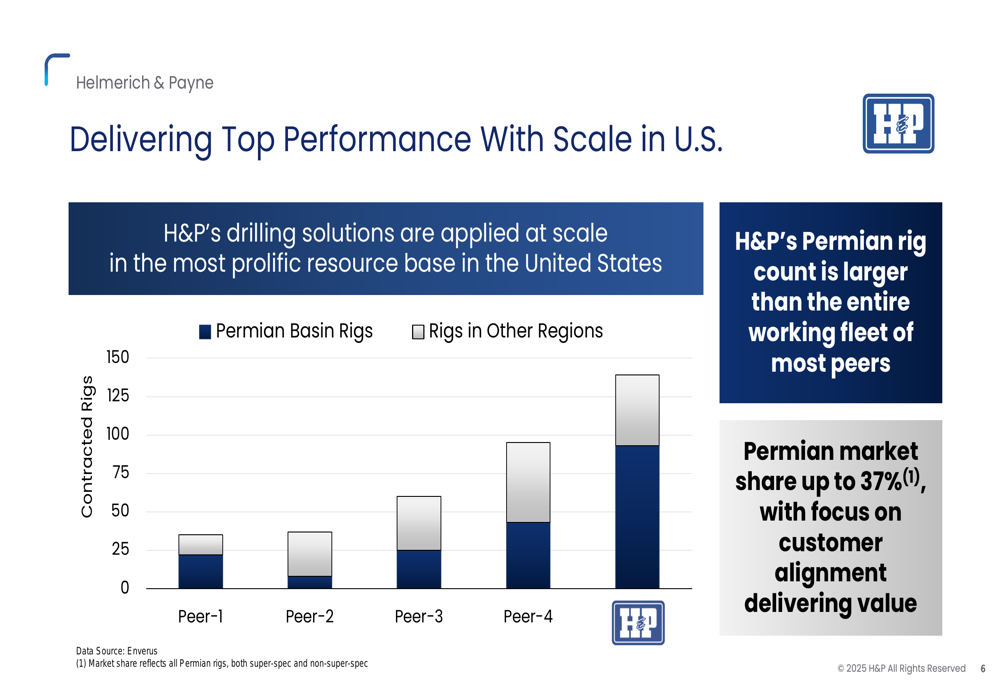

Helmerich & Payne emphasized its market leadership, particularly in the Permian Basin where it has increased its market share to 37%. The company’s Permian rig count exceeds the entire working fleet of most competitors, underscoring its dominant position in the most active U.S. oil and gas basin.

The following chart illustrates H&P’s scale advantage in the Permian Basin compared to peers:

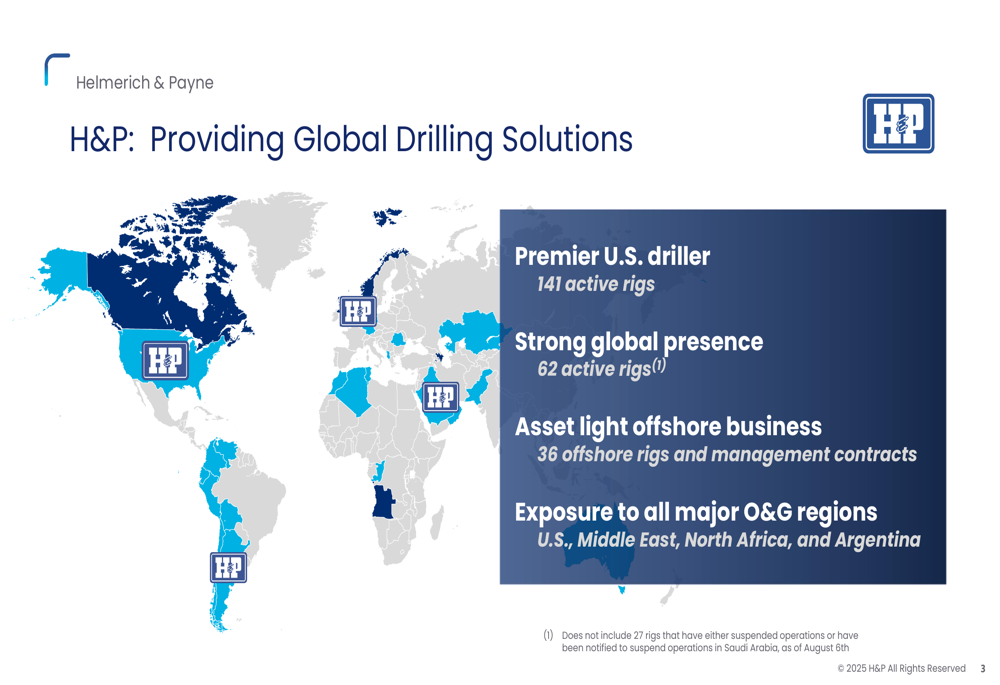

Globally, H&P highlighted its expanding international footprint with operations in major hydrocarbon basins including the Middle East, South America, and the North Sea. The company’s international presence includes operations in Kuwait (2 active rigs), Bahrain (3 active rigs), Saudi Arabia (17 active rigs), Oman (16 active rigs), and Argentina (9 active rigs), along with 30 management contracts in the North Sea.

The company’s global operations are visualized in this map showing its international presence:

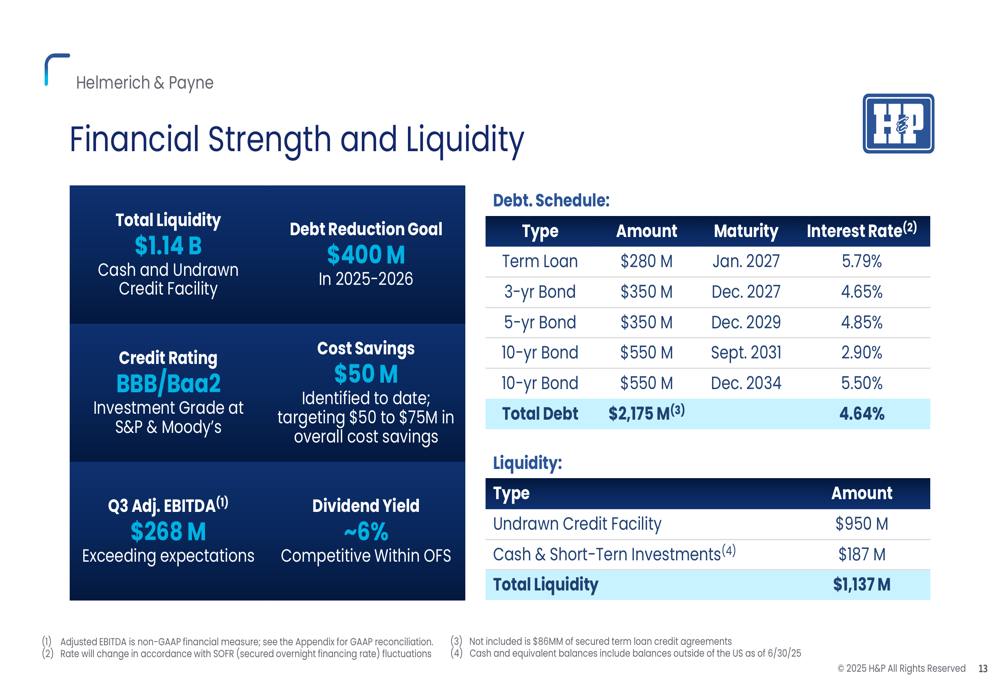

Financial Strength and Outlook

Helmerich & Payne emphasized its strong financial position, highlighting total liquidity of $1.14 billion and an investment grade credit rating (BBB/Baa2). The company is focusing on debt reduction, having repaid $120 million through July with plans to reach $200 million by the end of fiscal 2025.

The company’s financial strength and debt structure are detailed in the following slide:

Despite these positive developments, it’s worth noting that H&P’s stock has faced significant pressure in recent months. According to market data, shares closed at $15.49 on August 6, 2025, down 0.77% for the day and significantly below the 52-week high of $37.46, though still above the 52-week low of $14.65.

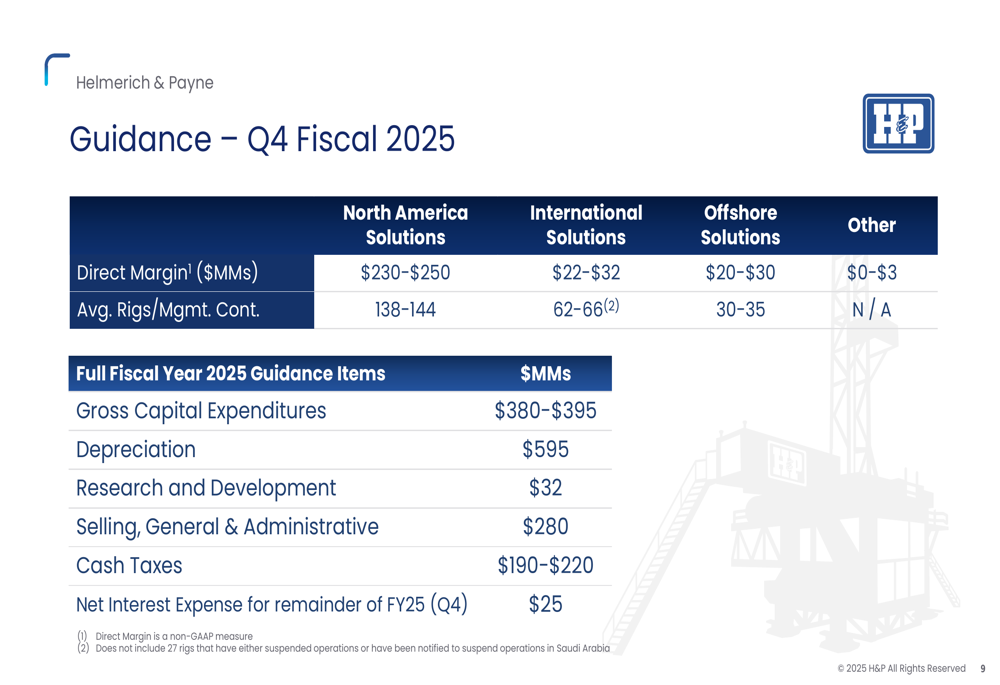

Q4 Guidance and Forward-Looking Statements

Looking ahead to the fourth quarter of fiscal 2025, Helmerich & Payne provided guidance that suggests a slight moderation in financial performance compared to Q3. The company projects direct margin for its North America Solutions segment to range between $230-250 million, down from the $266.2 million achieved in Q3.

Similarly, international direct margin is expected to decrease to $22-32 million in Q4, compared to $34.1 million in Q3, potentially reflecting the impact of suspended operations in Saudi Arabia. Average rig count is projected at 138-144 for North America and 62-66 for International operations.

The detailed Q4 guidance is presented in the following slide:

For the full fiscal year 2025, H&P expects gross capital expenditures of $380-395 million, depreciation of $595 million, and cash taxes of $190-220 million.

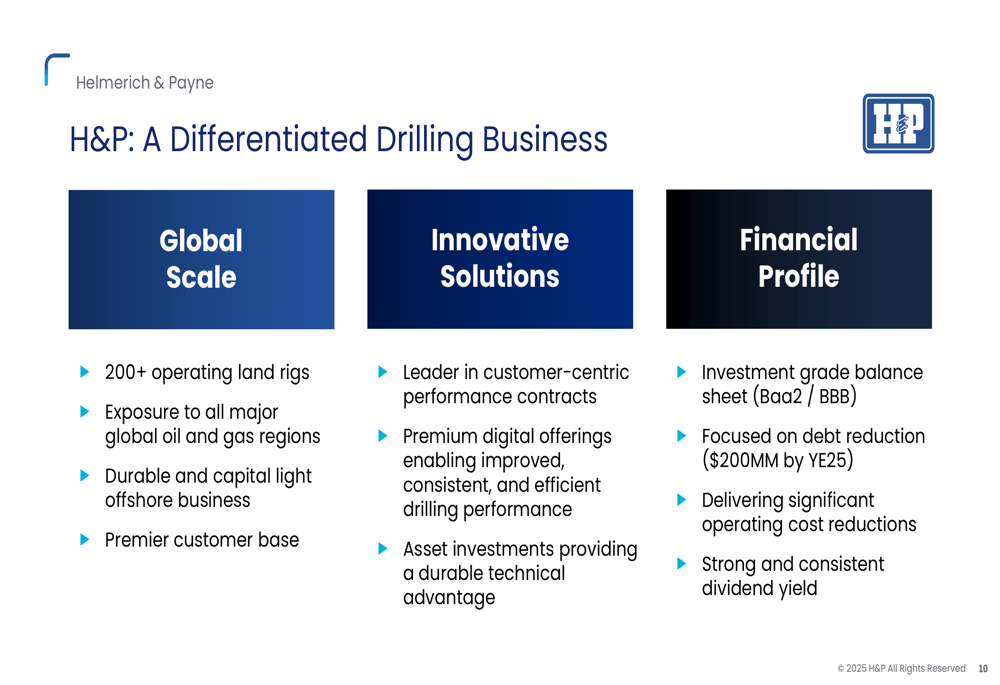

The company highlighted its differentiated position in the drilling industry, emphasizing three key advantages: global scale with over 200 operating land rigs, innovative solutions including performance-based contracts and digital offerings, and a strong financial profile anchored by an investment grade balance sheet.

Helmerich & Payne continues to position itself as a leader in the drilling industry, maintaining strong operational performance while navigating industry challenges. The company’s focus on debt reduction, cost-cutting initiatives, and international expansion provides a foundation for long-term stability, though near-term headwinds remain as reflected in both the stock performance and the slightly more conservative Q4 guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.