BofA warns Fed risks policy mistake with early rate cuts

Introduction & Market Context

Hensoldt AG (ETR:HAG) reported solid revenue growth and a record order backlog in its H1 2025 results presentation on July 31, despite facing margin pressure and cash flow challenges. The German defense electronics specialist has positioned itself to capitalize on increasing European defense spending, particularly in Germany, where defense budgets are projected to more than double by 2029.

The company’s stock has shown remarkable momentum over the past year, with a 101.53% year-to-date gain according to recent market data, though it experienced a slight decline of 0.97% following the results announcement.

Financial Performance Highlights

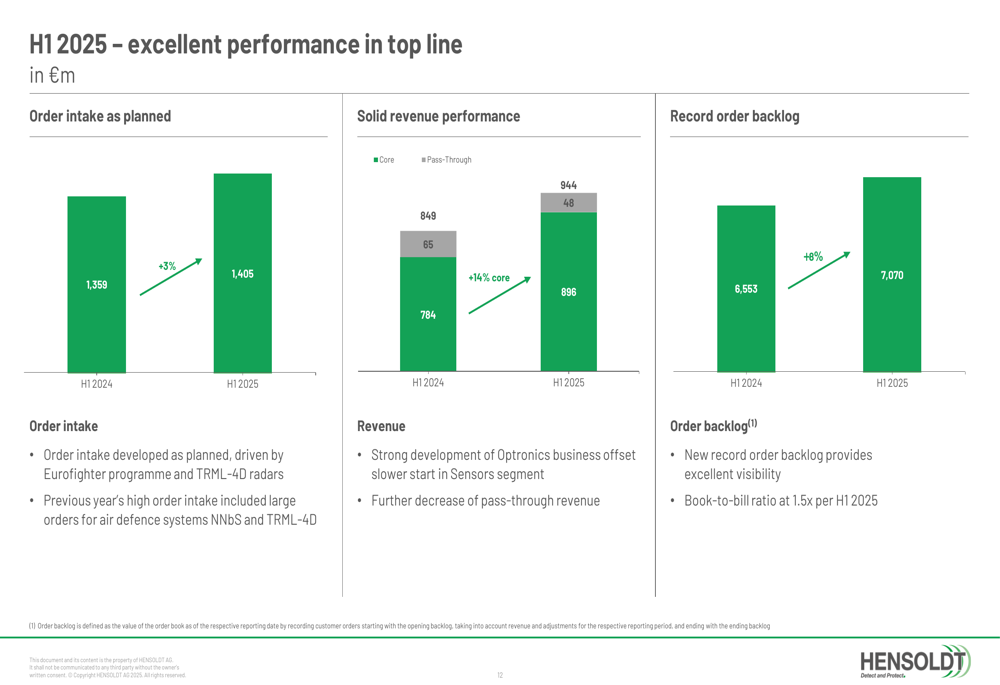

Hensoldt reported strong top-line performance in the first half of 2025, with revenue increasing by 14% core to €944 million, compared to €849 million in H1 2024. Order intake rose by 3% to €1,405 million, resulting in a book-to-bill ratio of 1.5x. The company achieved a record order backlog of €7,070 million, up 8% from the previous year, providing excellent visibility for future revenue.

As shown in the following chart of H1 2025 top-line performance:

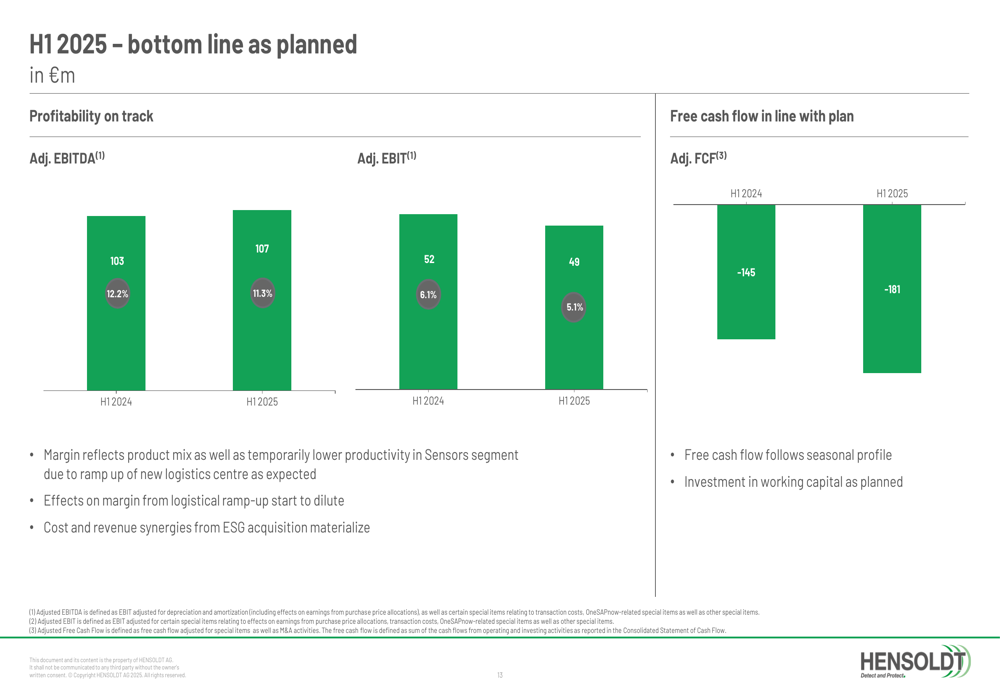

However, profitability metrics showed some pressure. Adjusted EBITDA increased slightly to €107 million from €103 million in H1 2024, but the margin decreased from 12.2% to 11.3%. Adjusted EBIT declined to €49 million (5.1% margin) from €52 million (6.1% margin) in the prior year. Free cash flow worsened to -€181 million compared to -€145 million in H1 2024.

The following chart illustrates the bottom-line performance:

The company reported a net loss of €44 million for H1 2025, compared to a loss of €26 million in H1 2024, primarily due to higher interest expenses and special items related to site relocation and system implementation costs.

Segment Analysis

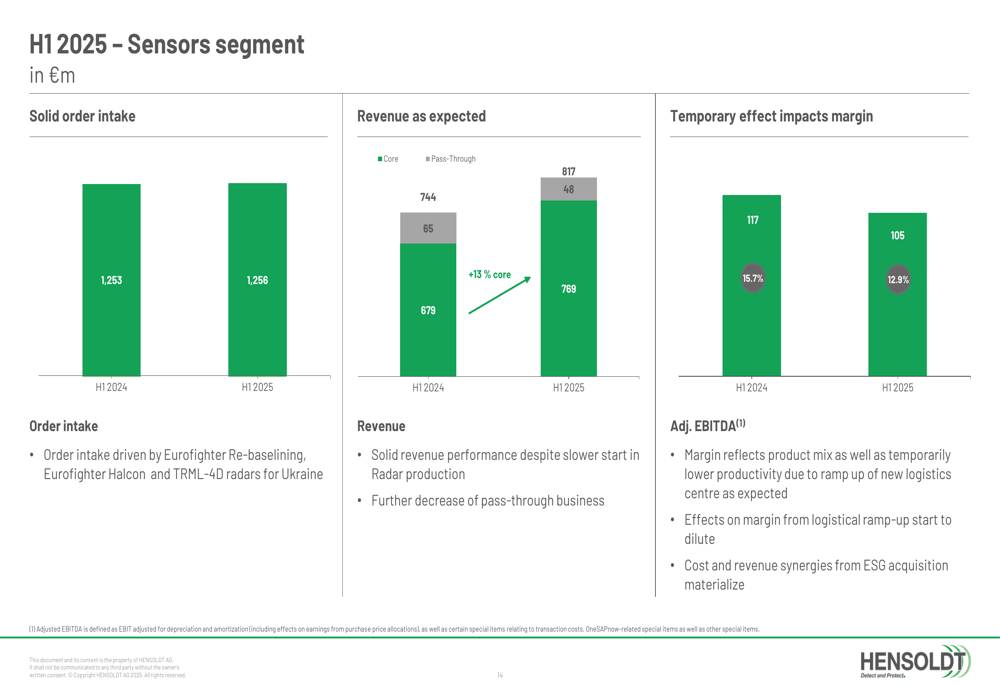

Hensoldt’s Sensors segment, which accounts for the majority of the company’s business, delivered solid performance with revenue increasing by 13% core to €817 million. However, adjusted EBITDA margin decreased to 12.9% from 15.7% in the prior year period, which the company attributed to temporary effects.

The segment performance is illustrated in the following chart:

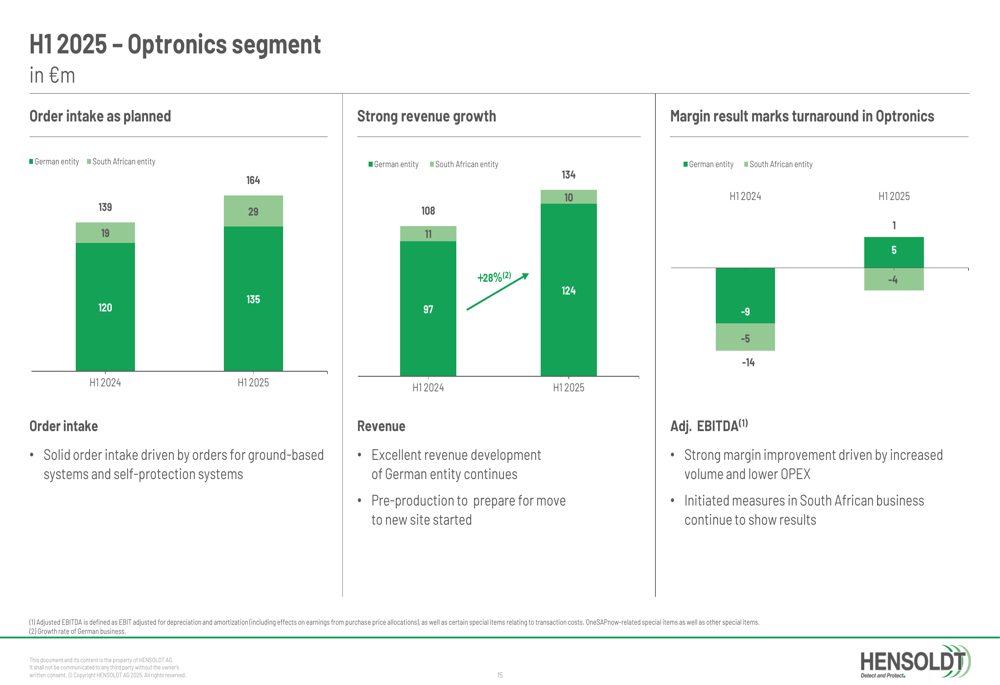

The Optronics segment showed strong revenue growth of 28% in the German entity, increasing from €108 million to €134 million. The segment also showed signs of a turnaround in profitability, with the German entity improving from -€9 million to €1 million in adjusted EBITDA, though the South African entity continued to face challenges with a slight decline from -€5 million to -€6 million.

Order Intake and Future Pipeline

Hensoldt secured several significant orders in H1 2025, including a €350 million Eurofighter re-baselining contract, €300 million for TRML-4D radars for Ukraine, €35 million for self-protection systems for the Spanish Halcon program, and €50 million for sights for ground-based systems.

The key orders received in H1 2025 are shown below:

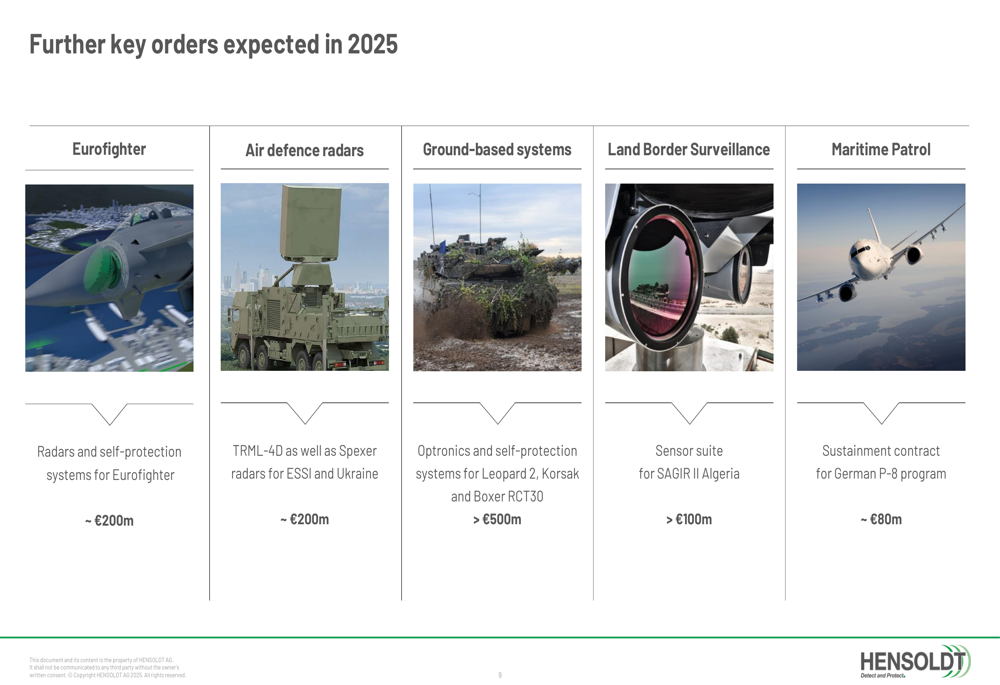

The company also highlighted a strong pipeline of expected orders for the remainder of 2025, totaling over €1 billion. These include additional Eurofighter contracts, more radar systems for Ukraine, optronics and self-protection systems for various platforms, and a sustainment contract for the German P-8 program.

The expected orders for the remainder of 2025 are illustrated here:

Market Context and Growth Drivers

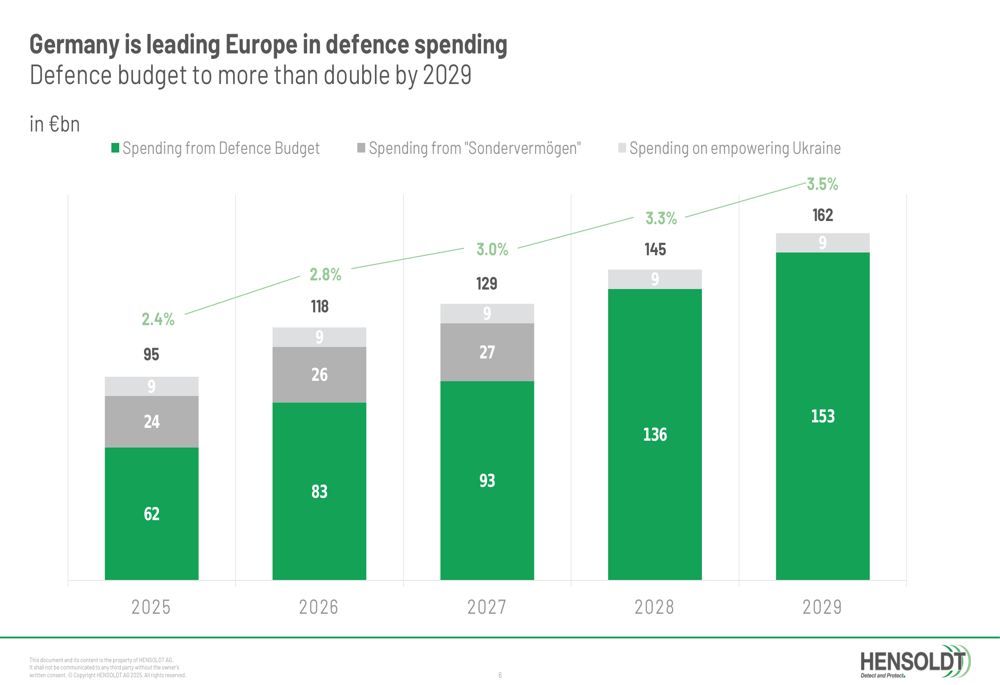

A key growth driver for Hensoldt is the projected increase in German defense spending, which is expected to more than double from €62 billion in 2025 to €153 billion by 2029. This aligns with NATO force goals and German procurement priorities in areas such as air defense, electromagnetic warfare, AI, uncrewed systems, and space-based reconnaissance.

The following chart shows the projected increase in German defense spending:

Hensoldt’s CEO Oliver Dörre emphasized that the company is well-positioned to benefit from this spending increase, stating that Hensoldt has "strategy, products, technologies and operational capacities to play a major role in upcoming German and EU procurement programmes."

Outlook and Guidance

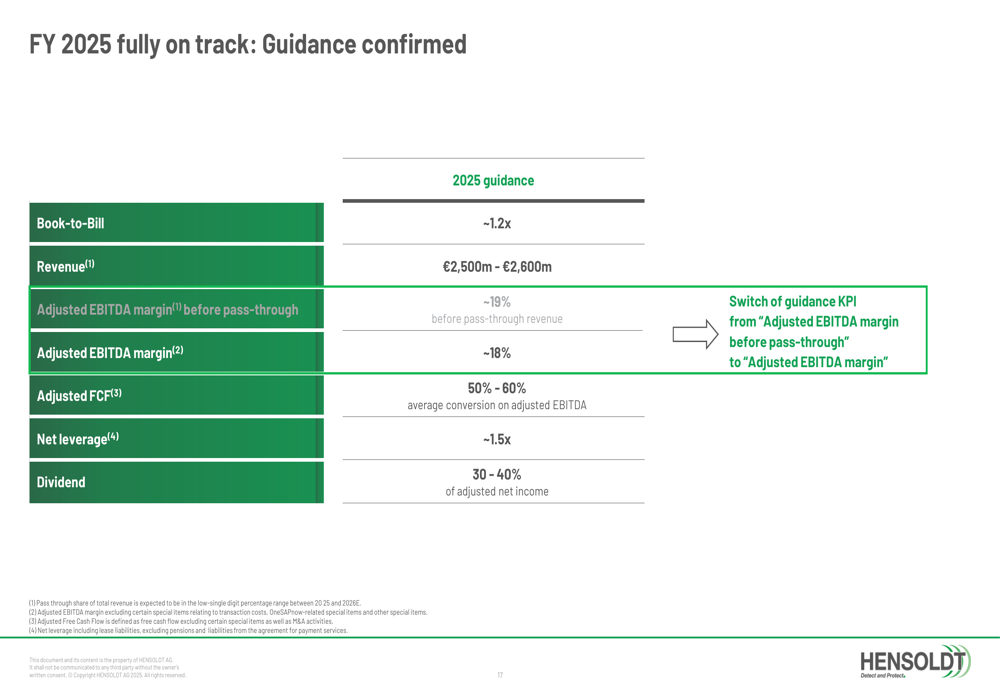

Despite the margin pressure in H1, Hensoldt confirmed its full-year 2025 guidance, targeting:

- Book-to-Bill ratio of approximately 1.2x

- Revenue of €2,500-2,600 million

- Adjusted EBITDA margin of approximately 18%

- Adjusted FCF conversion rate between 50-60%

- Net leverage of approximately 1.5x

- Dividend payout ratio between 30-40% of adjusted net income

The company’s full-year guidance is shown in the following chart:

To achieve the 18% EBITDA margin target for the full year, Hensoldt will need to significantly improve its profitability in the second half of 2025 from the current 11.3% level in H1.

Strategic Initiatives and Challenges

To support future growth, Hensoldt is implementing several strategic initiatives, including a capacity ramping plan called "Operations 2.0" to build scalable industrial systems and create resilience. The company has established a new logistics center and is relocating to a new site in Oberkochen to enable more efficient operations.

The company also successfully completed refinancing, which it says will provide more flexible financing instruments, strengthen its long-term capital structure, improve cost structure, release fundamental securities, and diversify its funding structure.

However, challenges remain, including margin pressure, worsening free cash flow, and the need to scale operations to meet increasing demand. The company will need to execute effectively on its operational improvements to achieve its ambitious full-year margin targets and position itself for sustainable long-term growth in the expanding defense market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.