These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Hensoldt AG (ETR:HAG) presented its Q1 2025 results on May 7, highlighting strong order intake growth despite temporary margin pressure from logistics infrastructure investments. The defense electronics specialist is benefiting from a fundamental shift in European defense policy, with Germany moving from "procure-to-budget" to "procure-to-capability" approaches amid heightened geopolitical tensions.

The company’s presentation emphasized how recent geopolitical developments, including statements at the Munich Security Conference and the EU’s ReArm initiative mobilizing up to €800 billion for defense and security, are creating substantial growth opportunities. Notably, Germany’s constitutional change now exempts defense spending above 1% of GDP from debt brake restrictions.

As shown in the following slide detailing the shift in German defense procurement policy:

Quarterly Performance Highlights

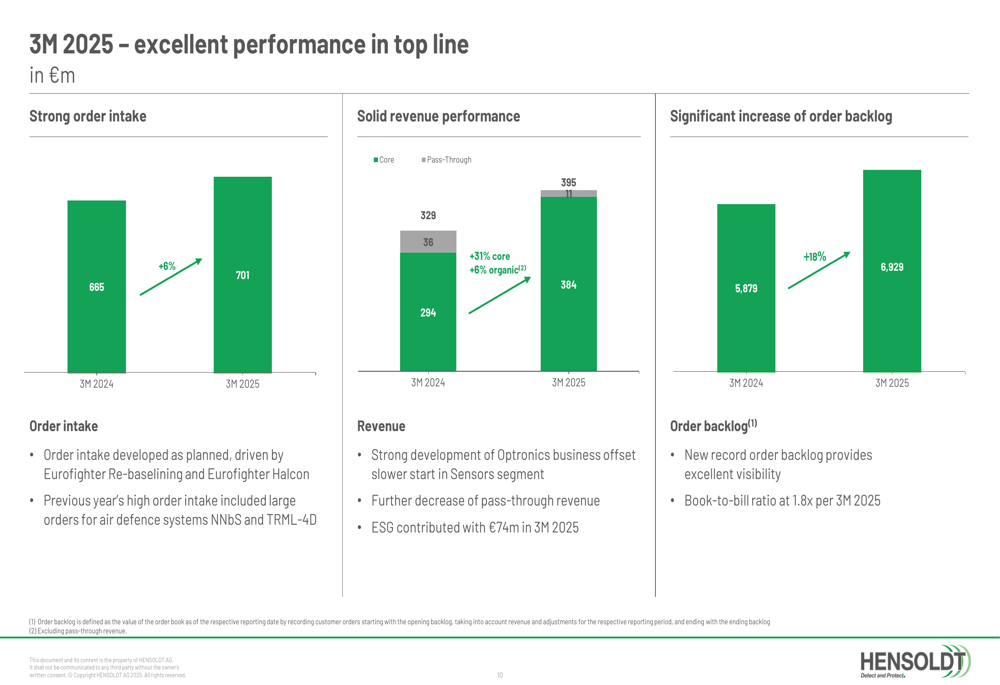

Hensoldt reported robust top-line performance for Q1 2025, with order intake increasing by 6% year-over-year to €701 million from €665 million in Q1 2024. The company’s order backlog grew significantly by 18% to €6.9 billion, providing strong visibility for future revenue. Core revenue increased by 31%, with organic growth of 6% and ESG (Environmental, Social, and Governance) contributing €74 million. The book-to-bill ratio stood at a healthy 1.8x, indicating continued strong demand.

The following chart illustrates these key performance metrics:

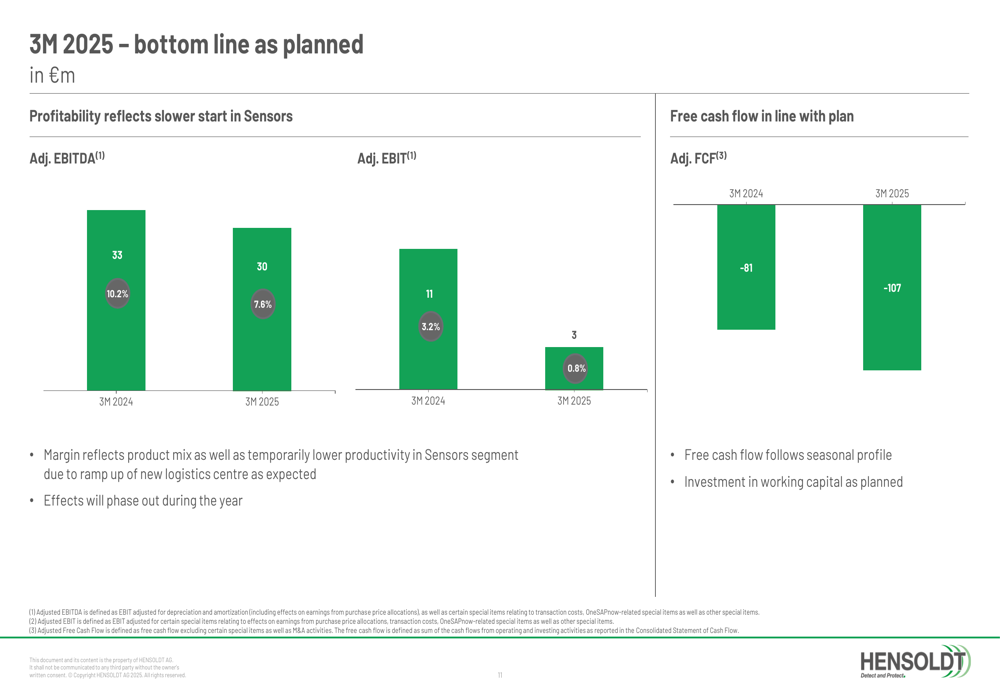

However, profitability metrics showed some pressure, with adjusted EBITDA declining to €30 million (7.6% margin) from €33 million (10.2% margin) in Q1 2024. Adjusted EBIT decreased to €3 million (0.8%) from €11 million (3.2%), while adjusted free cash flow was negative at -€107 million compared to -€81 million in the prior year period. Management attributed these temporary declines to product mix effects and lower productivity in the Sensors segment due to the ramp-up of a new logistics center.

The following slide details the company’s profitability and cash flow performance:

Segment Performance

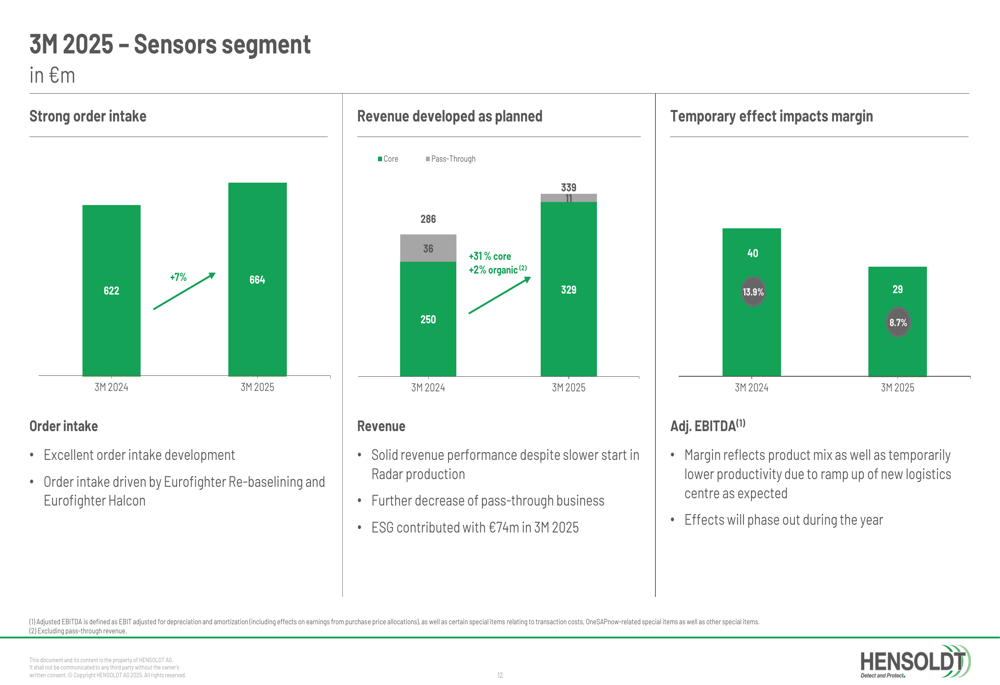

The Sensors segment, Hensoldt’s largest business unit, saw order intake increase by 7% to €664 million, while revenue grew by 31% on a core basis and 2% organically. However, adjusted EBITDA for the segment declined to €29 million (8.7% margin) from €40 million (13.9% margin) in Q1 2024, reflecting the temporary impact of the logistics center transition.

As shown in the following segment performance chart:

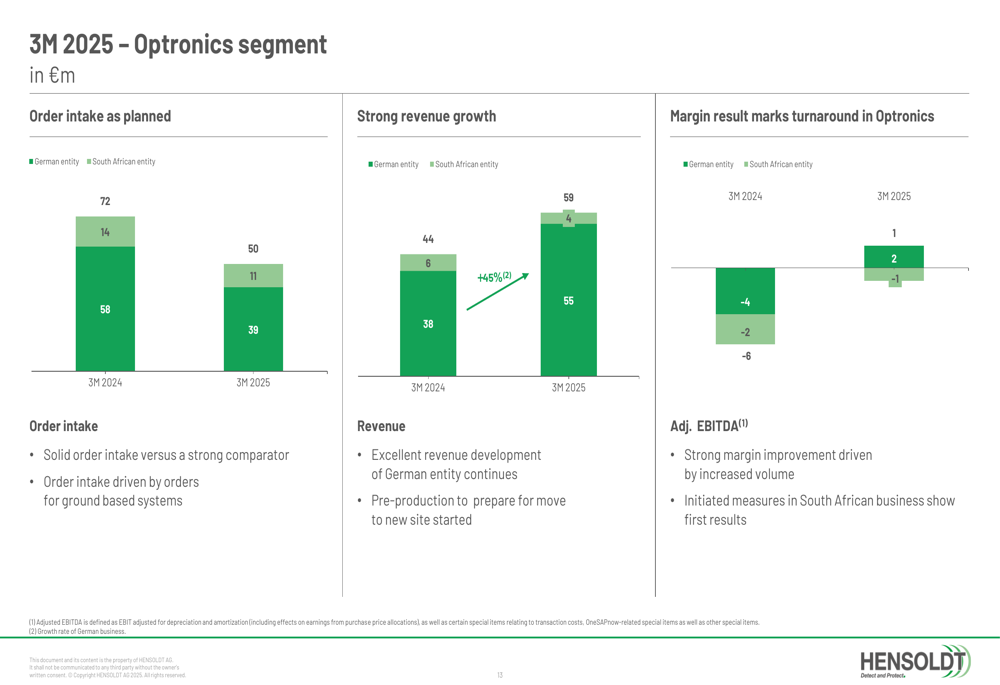

Meanwhile, the Optronics segment showed signs of a turnaround, with strong revenue growth of 34% to €59 million and a return to positive adjusted EBITDA of €1 million, compared to -€4 million in Q1 2024. This improvement reflects the success of restructuring efforts in this business unit.

The following chart details the Optronics segment’s performance:

Strategic Initiatives

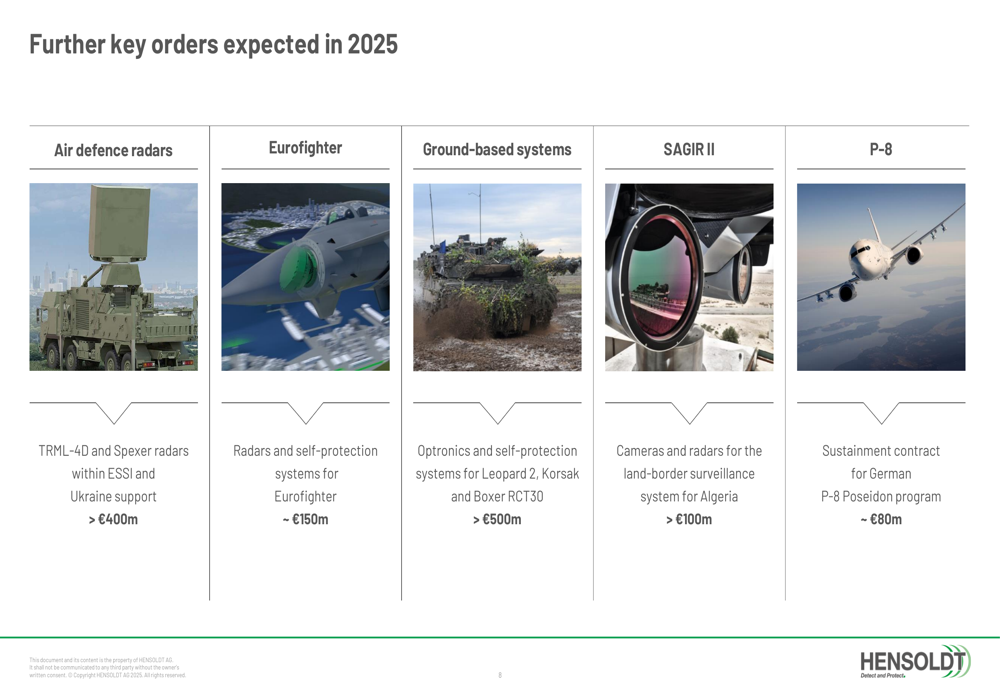

Hensoldt is positioning itself to capitalize on changing defense priorities through several strategic initiatives. The company has identified key expected orders for 2025 totaling over €1.2 billion, including air defense radars (>€400 million), Eurofighter systems (~€150 million), ground-based systems (>€500 million), the SAGIR II border surveillance system (>€100 million), and P-8 sustainment contracts (~€80 million).

The following slide outlines these key expected orders:

The company is also pioneering "Software-Defined Defence" (SDD), leveraging its existing software-defined products while developing new capabilities. As part of this strategy, Hensoldt announced a strategic partnership with drone manufacturer Quantum Systems, combining Hensoldt’s sensor expertise with Quantum’s unmanned aerial systems and software stack.

Additionally, Hensoldt successfully completed a €1.8 billion refinancing, replacing its Leveraged-Buyout (LBO) financing with more favorable terms, securing funding until 2032 and releasing fundamental securities from the LBO structure.

To support production scaling, the company has invested in a new logistics center that is transitioning from handling 250 materials per day during the relocation phase to over 1,300 materials per day in the system ramp-up phase starting February 2025.

Forward-Looking Statements

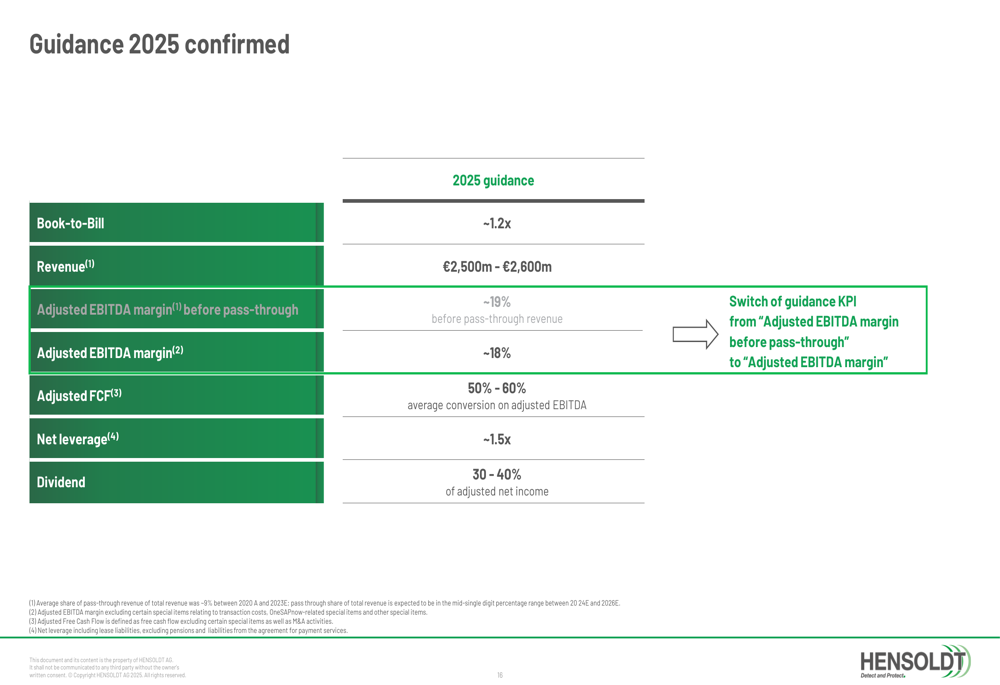

Despite the temporary margin pressure in Q1, Hensoldt confirmed its 2025 guidance, projecting a book-to-bill ratio of approximately 1.2x, revenue between €2,500-2,600 million, an adjusted EBITDA margin of around 18%, and adjusted free cash flow conversion of 50-60% of adjusted EBITDA. The company also targets a net leverage ratio of approximately 1.5x and a dividend payout of 30-40% of adjusted net income.

The following slide details the company’s 2025 guidance:

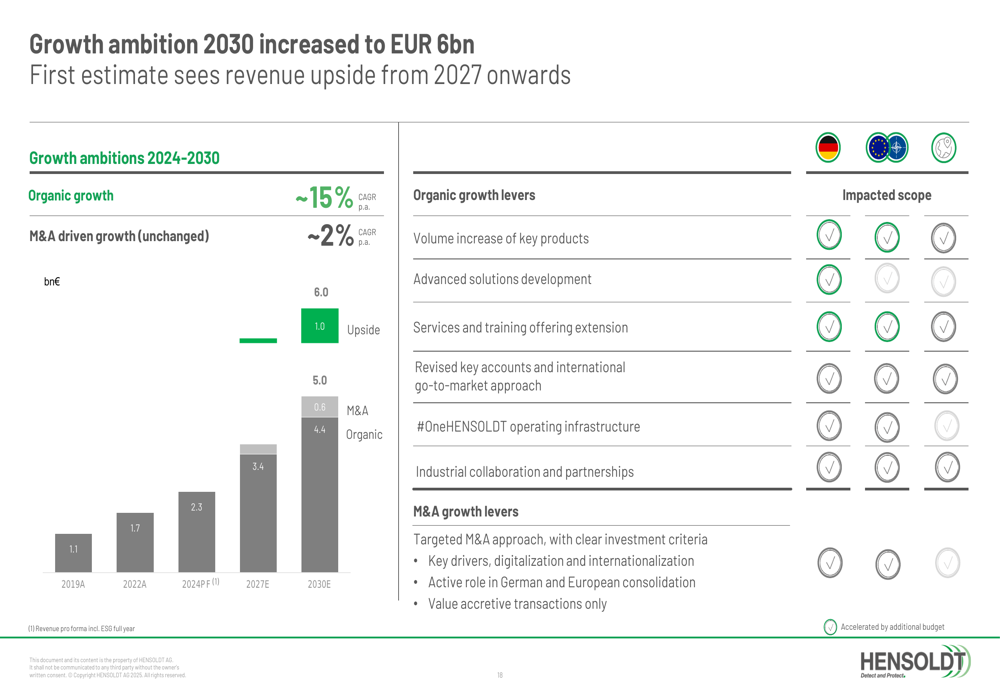

More significantly, Hensoldt has increased its long-term growth ambition to €6 billion in revenue by 2030, representing approximately 15% organic CAGR plus 2% from M&A activities. This growth projection is supported by an identified pipeline of €55 billion for 2025-2030, a substantial increase from the €10 billion pipeline identified at the company’s IPO.

The following chart illustrates this ambitious growth target:

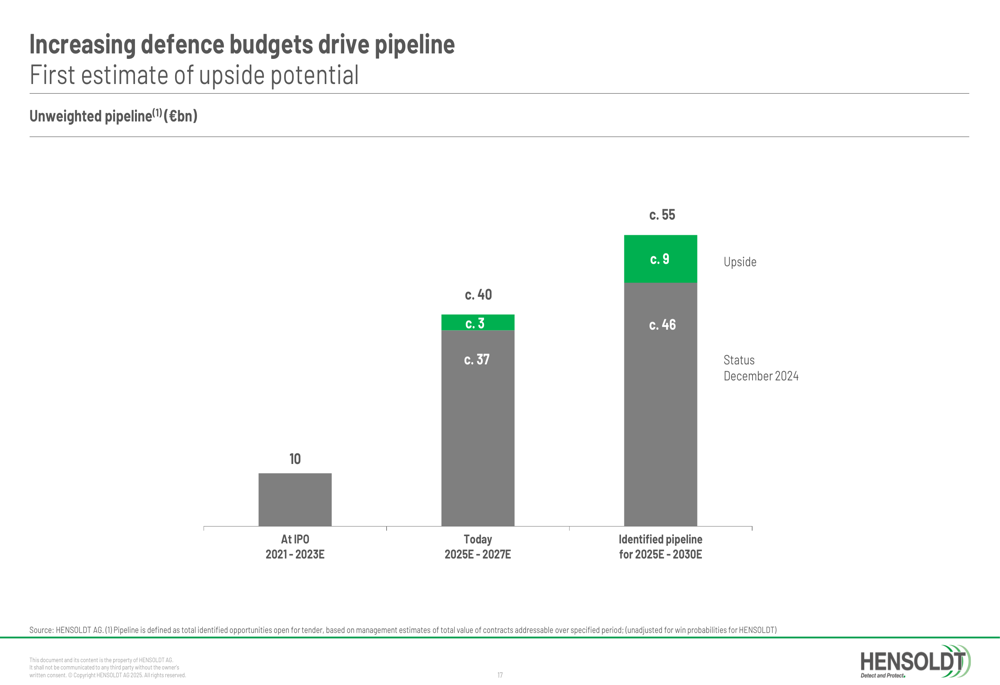

The growth in defense budgets underpins these projections, with the company’s unweighted pipeline growing from €10 billion at IPO to €40 billion today, with an additional €9 billion in potential upside.

As shown in the following chart of increasing defense budgets:

Competitive Industry Position

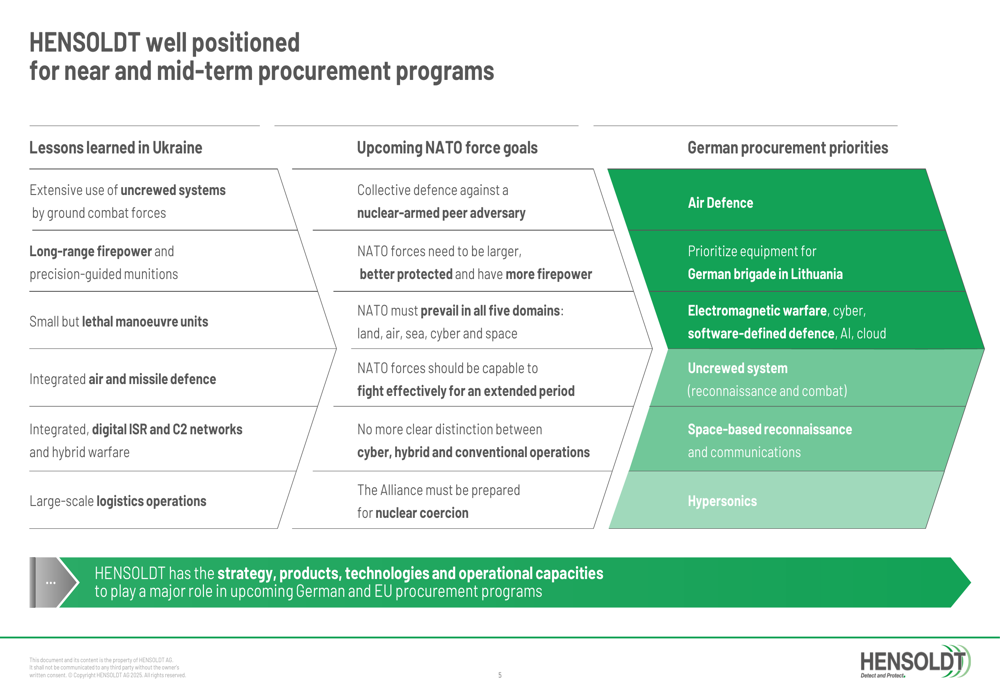

Hensoldt has strategically aligned its capabilities with lessons learned from the Ukraine conflict, upcoming NATO force goals, and German procurement priorities. The company highlighted how its technologies address key military requirements including uncrewed systems, long-range firepower, and integrated intelligence, surveillance, and reconnaissance networks.

The following slide illustrates how Hensoldt is positioning itself within these defense priorities:

Conclusion

Hensoldt’s Q1 2025 results demonstrate strong order intake and revenue growth, albeit with temporary margin pressure from strategic investments in logistics infrastructure. The company’s confirmation of 2025 guidance suggests confidence that profitability will recover throughout the year as the logistics center ramp-up is completed.

The increased long-term growth ambition to €6 billion by 2030 reflects management’s confidence in the structural growth of European defense spending and Hensoldt’s competitive positioning within this expanding market. Strategic initiatives in software-defined defense, partnerships, and production scaling further support this ambitious growth trajectory.

Investors will likely focus on the company’s ability to recover margins in the coming quarters while maintaining its strong order momentum in an increasingly favorable defense spending environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.