LIVE UPDATES: Fed Chair Jerome Powell to deliver major speech at Jackson Hole

Introduction & Market Context

HomeStreet Inc (NASDAQ:HMST) presented its second quarter 2025 financial results on July 28, 2025, revealing continued challenges as the Seattle-based bank works toward a return to profitability. The presentation comes as the company’s stock trades at $13.18, down 0.53% from its previous close, but significantly above its 52-week low of $8.41, suggesting some investor optimism despite ongoing financial struggles.

Founded in 1921, HomeStreet operates as a diversified commercial and consumer bank serving customers throughout the western United States with total assets of $7.6 billion. The company maintains a presence across key western markets including Seattle/Puget Sound, Southern California, Portland, Oregon, the Hawaiian Islands, and specialized lending in Idaho/Utah.

Quarterly Performance Highlights

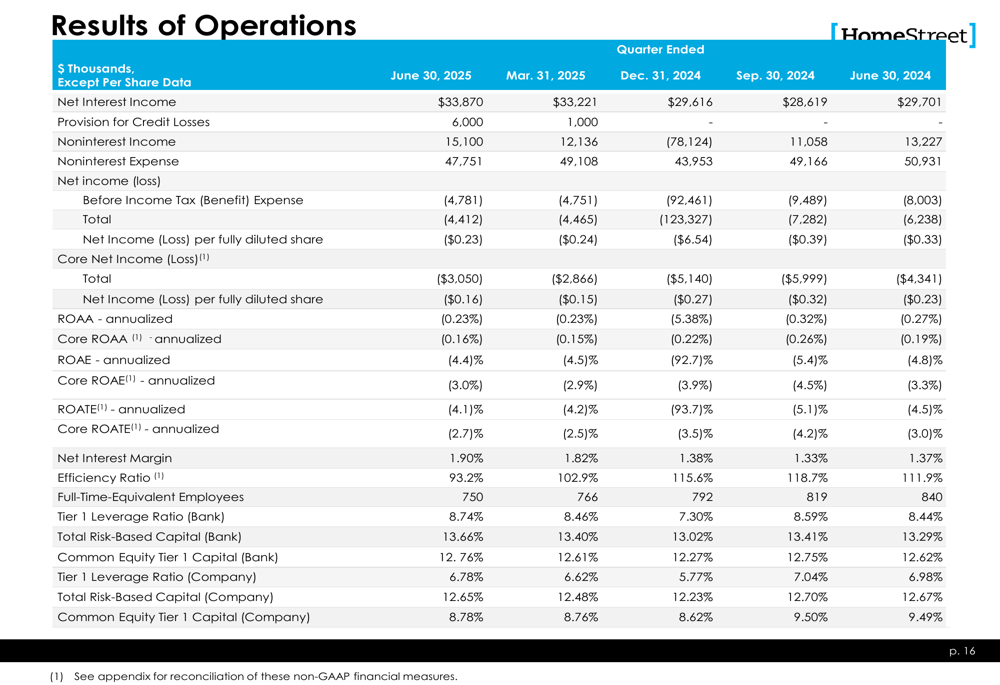

HomeStreet reported a net loss of $4.4 million, or $0.23 per share, for the second quarter of 2025. On a core basis, which excludes certain non-recurring items, the net loss was $3.1 million, or $0.16 per share. Notably, while the parent company reported losses, HomeStreet Bank, the subsidiary, achieved a modest profit of $0.7 million for the quarter.

The company’s net interest margin stood at 1.90%, showing improvement from previous quarters. Deposit balances remained stable with a slight increase in noninterest-bearing deposits, while uninsured deposits totaled $604 million, representing just 10% of total deposits – a relatively low level that management highlighted as a strength.

As shown in the following comprehensive financial results table:

Asset quality metrics showed some pressure with nonperforming assets to total assets at 0.76%. The company maintained a book value per share of $21.30 and tangible book value per share of $20.97, providing a significant premium to the current trading price.

Detailed Financial Analysis

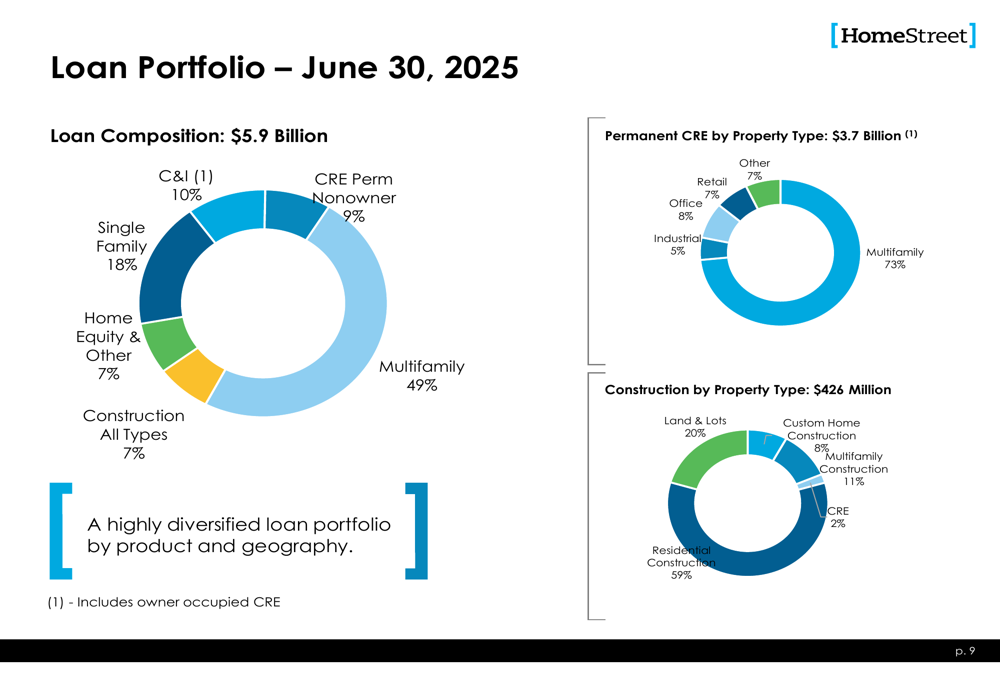

HomeStreet’s balance sheet reflects its focus on real estate lending, with a $5.9 billion loan portfolio heavily weighted toward multifamily properties. The loan composition breakdown reveals that multifamily loans represent 49% of the portfolio, followed by single-family loans at 18%, commercial and industrial loans at 10%, and commercial real estate at 9%.

The following chart illustrates the loan portfolio composition as of June 30, 2025:

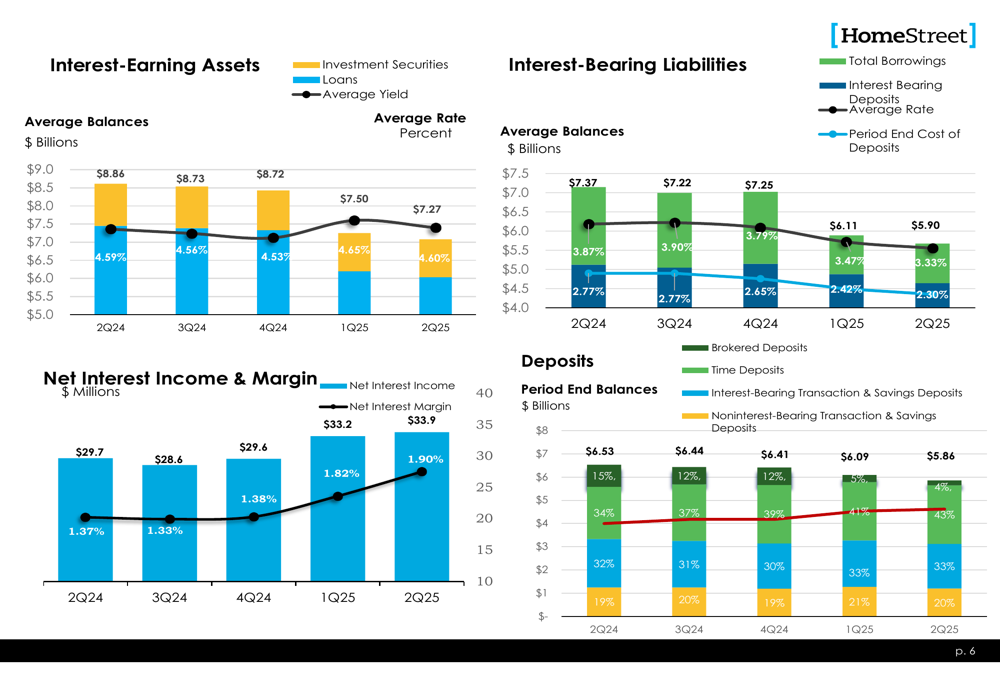

The company’s interest-earning assets yielded an average rate of 4.60% in Q2 2025, slightly down from 4.65% in the previous quarter. Meanwhile, the cost of interest-bearing liabilities decreased more significantly to 3.33% from 3.47% in Q1 2025, helping to improve the net interest margin.

This trend in interest rates for assets and liabilities is illustrated in the following chart:

Noninterest income totaled $15.1 million for the quarter, providing an important revenue stream to offset challenges in the interest income segment. The company’s efficiency metrics continue to be a focus area as management works to align expenses with revenue generation capabilities.

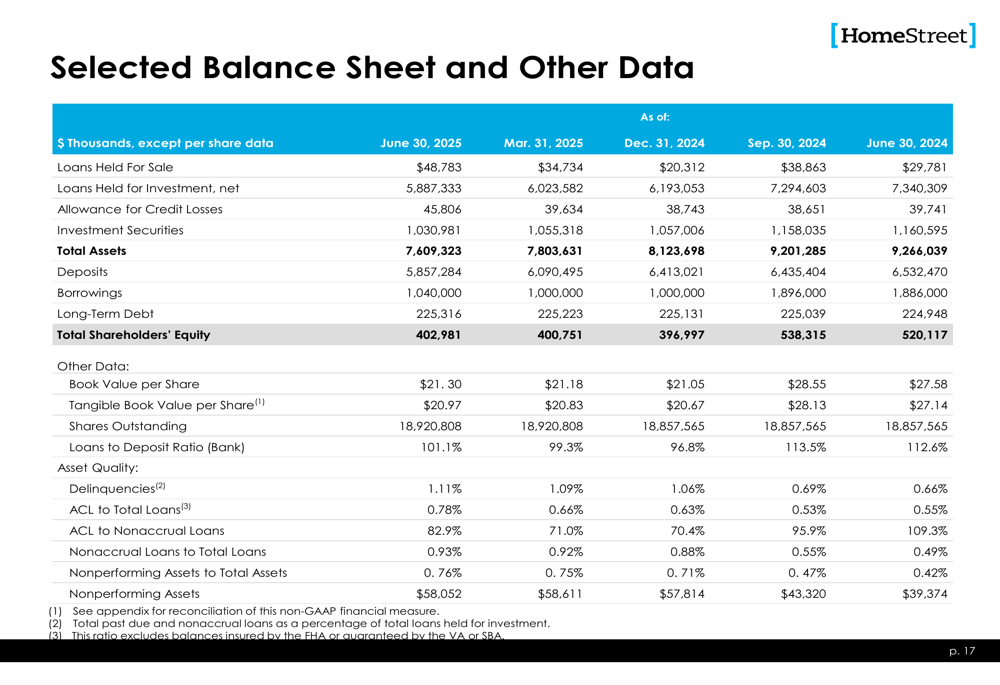

The bank’s balance sheet shows selected metrics across recent quarters:

Strategic Initiatives

A key strategic development highlighted in the presentation is the pending merger with Mechanics Bank, which is estimated to close in the third quarter of 2025. This transaction represents a significant potential turning point for HomeStreet, which has implemented a Profitability Plan aimed at returning to core profitability in 2025.

The company maintains strong liquidity with on-balance sheet liquidity at 21% as of June 30, 2025, and available contingent liquidity borrowing sources of $5.4 billion, equivalent to 92% of total deposits. This robust liquidity position provides flexibility as the bank navigates its current challenges.

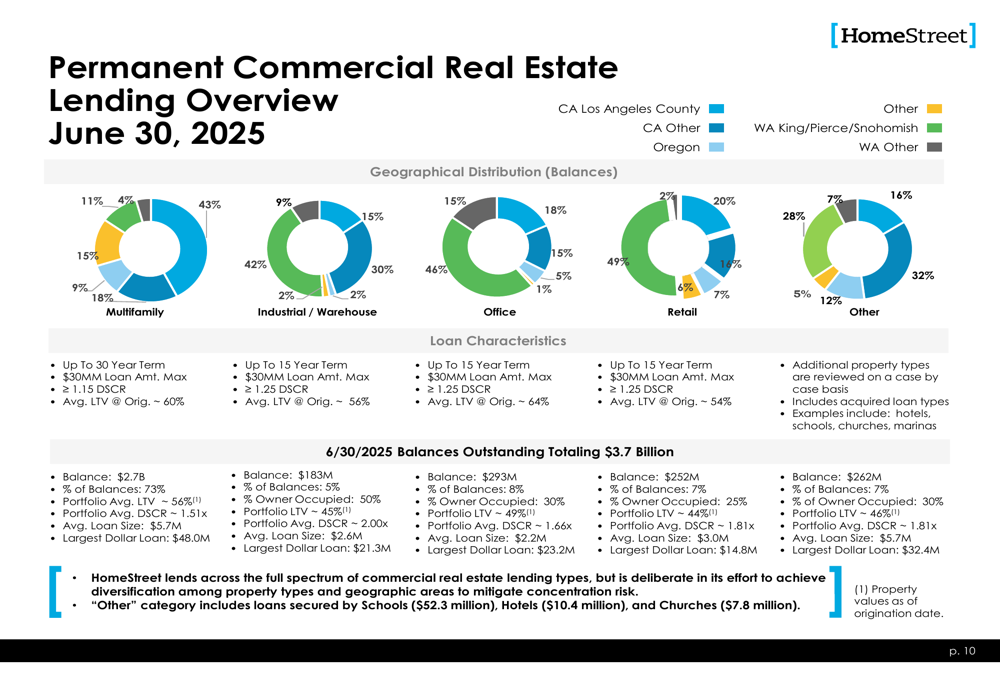

HomeStreet’s permanent commercial real estate lending portfolio, which represents a significant portion of its business, is detailed in the following overview:

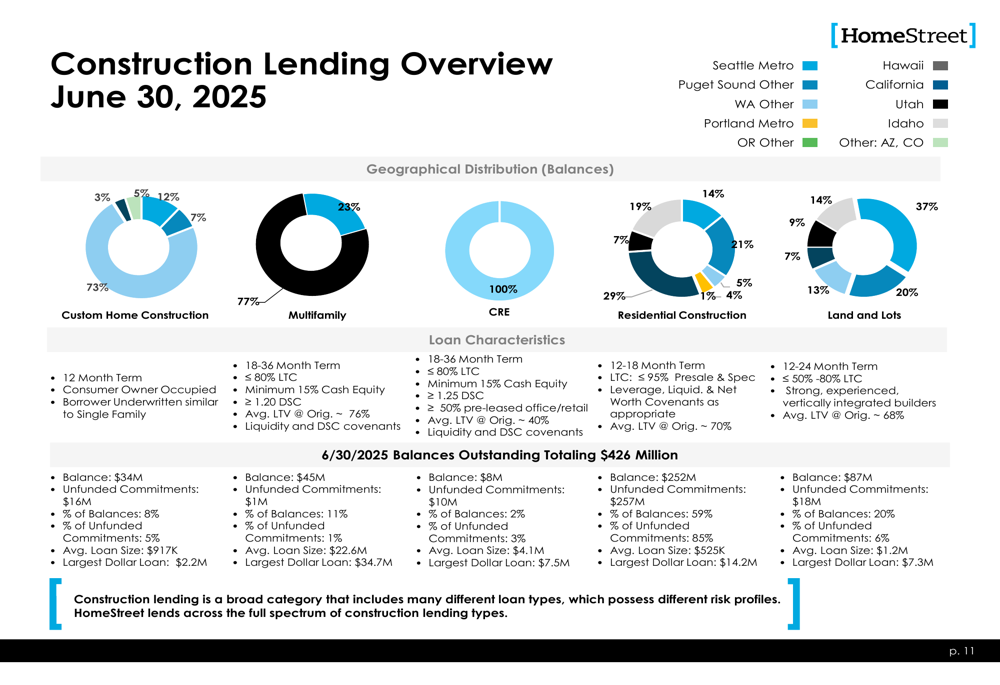

The construction lending portfolio, while smaller at $426 million, represents another important segment of the bank’s business:

Forward-Looking Statements

Despite the continued losses in Q2 2025, HomeStreet’s management remains focused on its path to profitability. The implementation of the Profitability Plan and the pending merger with Mechanics Bank are central to the company’s forward strategy.

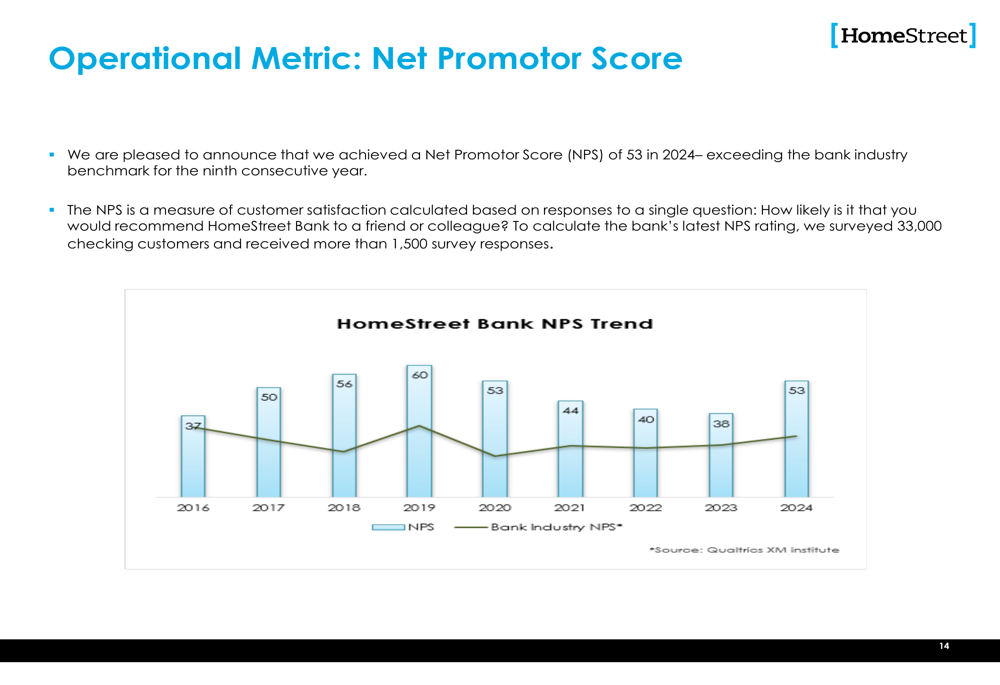

The bank continues to demonstrate strong customer satisfaction, with a Net Promoter Score (NPS) of 53 in 2024, exceeding the bank industry benchmark for the ninth consecutive year. This customer loyalty provides a foundation for potential recovery as the company works through its financial challenges.

As shown in the following chart, HomeStreet has consistently outperformed the banking industry in customer satisfaction:

The coming quarters will be critical for HomeStreet as it works to complete the Mechanics Bank merger and execute on its profitability initiatives. Investors will be watching closely to see if the company can reverse its loss trend and deliver on its stated goal of returning to profitability in 2025, a timeline that has already been extended from earlier projections that targeted profitability in the first half of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.