German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Honeywell International Inc. (NYSE:NASDAQ:HON) presented its second-quarter 2025 earnings results on July 24, showing stronger-than-expected performance that prompted management to raise its full-year guidance. The industrial conglomerate reported solid organic growth across three of its four segments while continuing to advance its strategic transformation into three independent public companies.

In pre-market trading following the presentation, Honeywell shares rose 2.04% to $244.16, building on the previous day’s close of $239.27. The stock has been performing well in 2025, trading near its 52-week high of $242.77, reflecting investor confidence in the company’s transformation strategy and operational execution.

Quarterly Performance Highlights

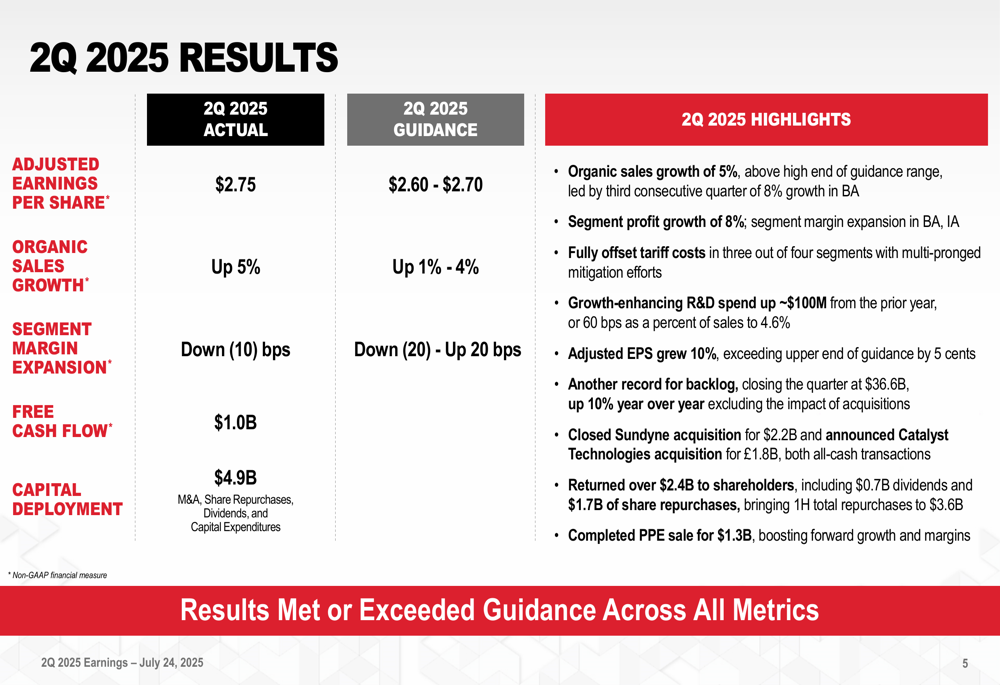

Honeywell delivered impressive second-quarter results with sales up 5% organically and adjusted earnings per share increasing by 10% compared to the same period last year. The company reported that both sales and adjusted EPS exceeded the high end of its previous guidance.

As shown in the following financial summary:

Free cash flow declined by 9% in the quarter, though management attributed this to timing factors rather than operational issues. The company highlighted "operational excellence in challenging environment" as a key achievement for the quarter.

A detailed breakdown of the EPS performance shows that segment profit growth and a lower tax rate were the primary drivers behind the 10% increase in adjusted EPS:

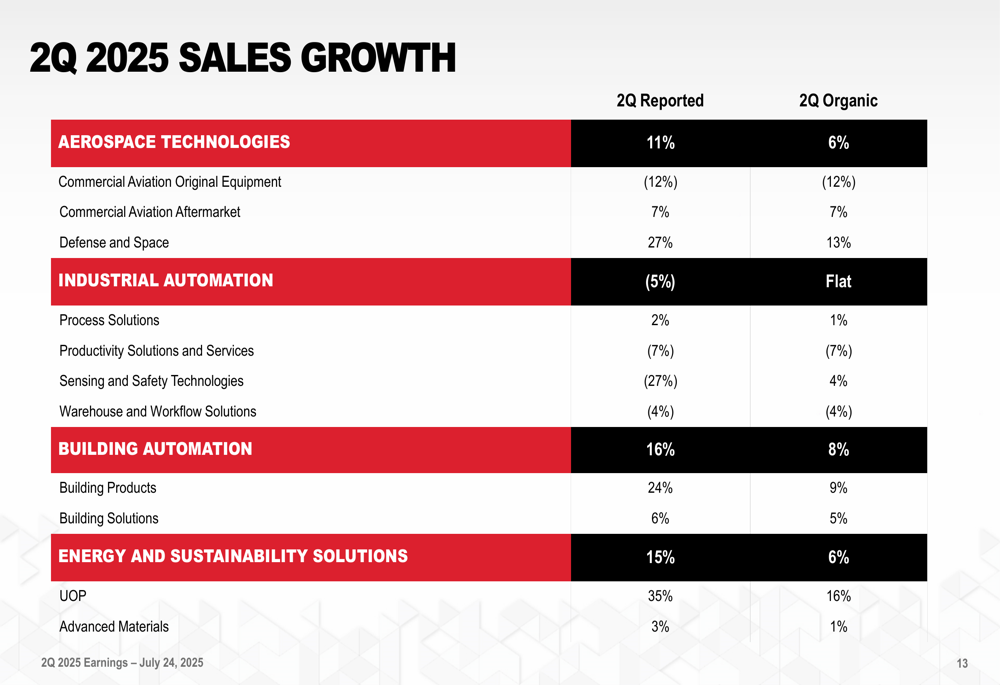

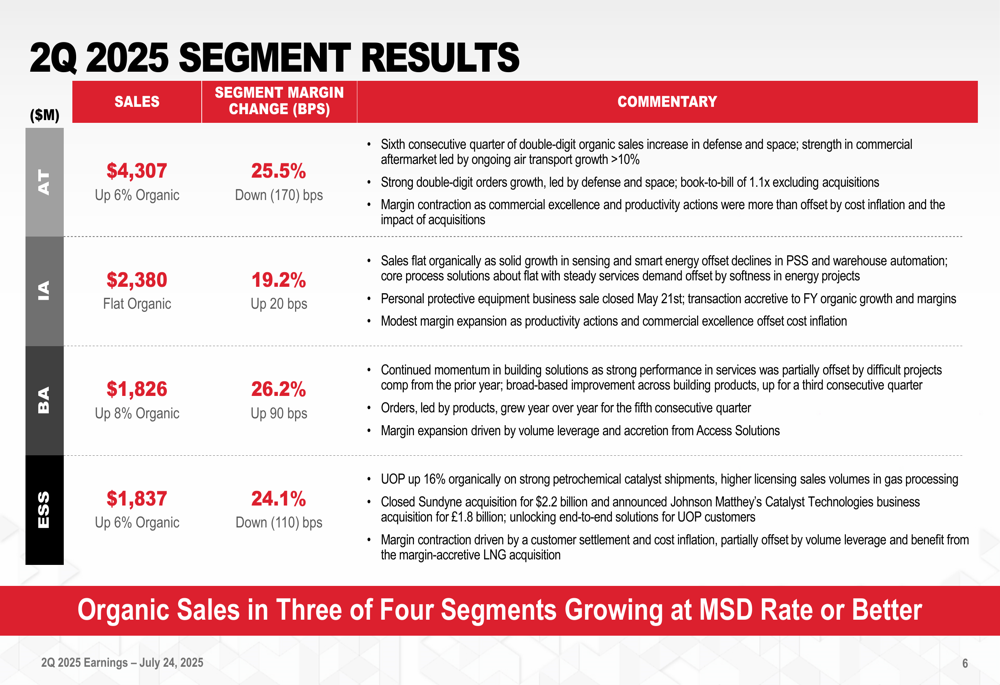

Segment Analysis

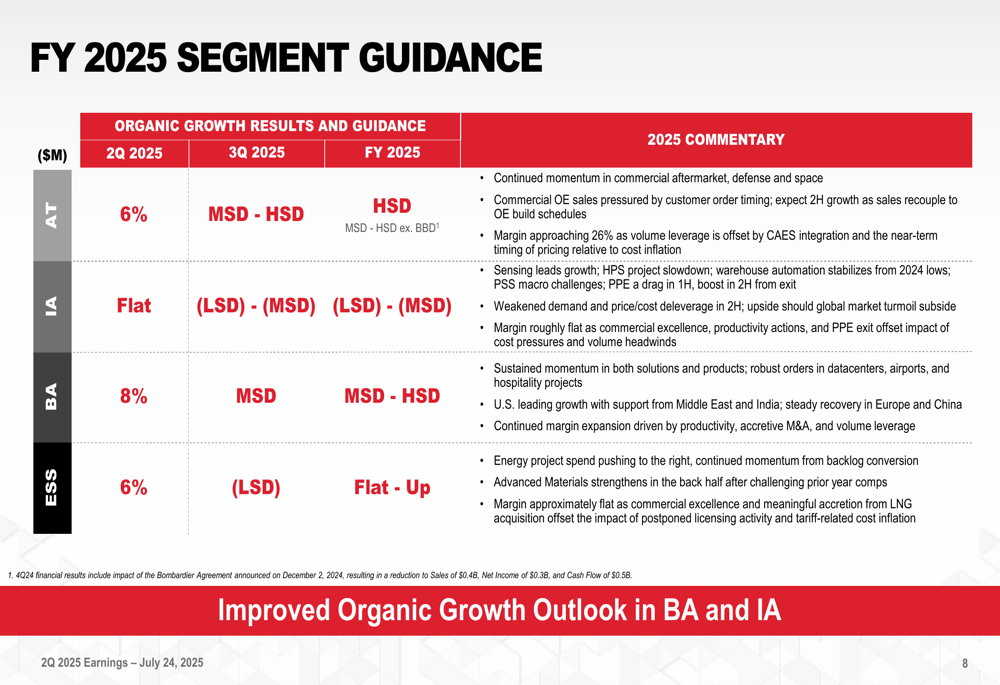

Honeywell’s performance varied across its four business segments, with three of them achieving mid-single-digit organic growth or better. The segment results reveal the company’s strengths in aerospace and building technologies, while industrial automation faced more challenging conditions.

The detailed segment breakdown shows:

Aerospace Technologies continued its strong trajectory with 6% organic growth, marking the sixth consecutive quarter of double-digit organic sales increase in defense and space. However, segment margin contracted by 170 basis points to 25.5%.

Building Automation emerged as the strongest performer with 8% organic sales growth and a 90 basis point improvement in segment margin to 26.2%. Energy and Sustainability Solutions also showed solid growth at 6% organically, though margins declined by 110 basis points to 24.1%.

Industrial Automation was the laggard with flat organic sales growth, though it managed a slight margin improvement of 20 basis points to 19.2%. The company noted that the personal protective equipment business sale closed on May 21st, affecting this segment’s results.

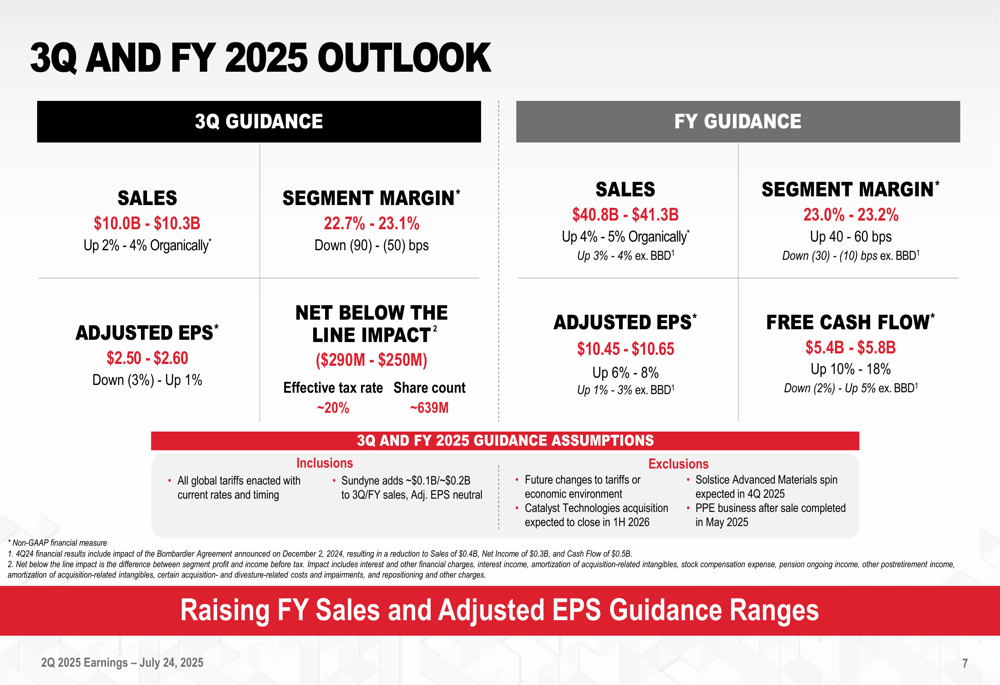

Updated 2025 Guidance

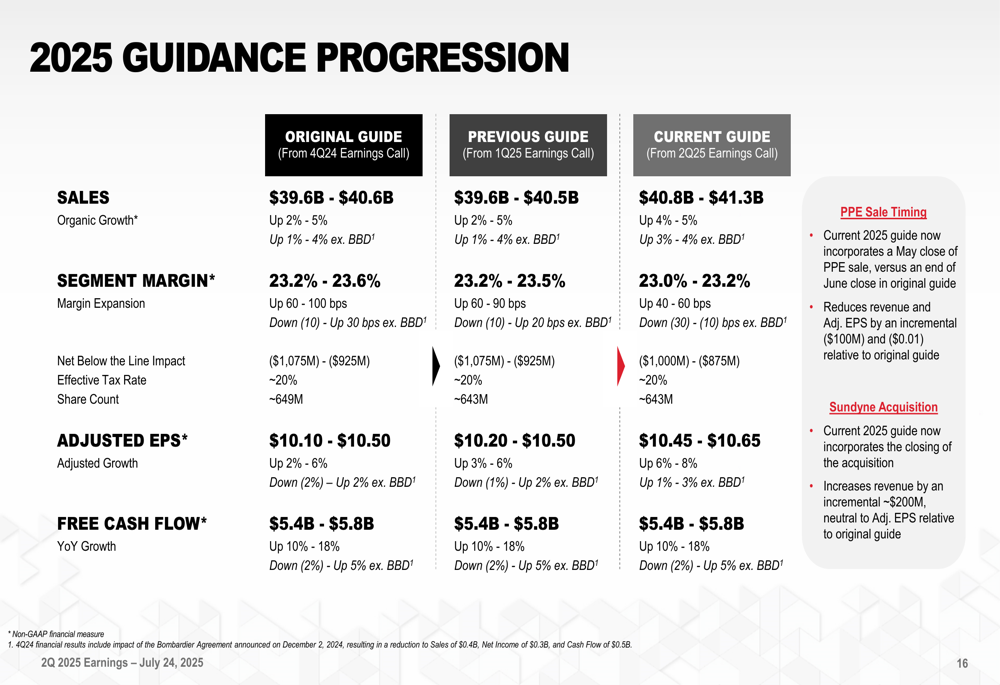

Based on the strong first-half performance, Honeywell raised its full-year 2025 guidance for both sales and earnings. The company now expects:

For the third quarter of 2025, Honeywell projects sales of $10.0-10.3 billion (up 2-4% organically) and adjusted EPS of $2.50-2.60. The company expects segment margin to contract by 50-90 basis points in Q3.

The full-year organic sales growth outlook improved particularly in the Building Automation and Industrial Automation segments:

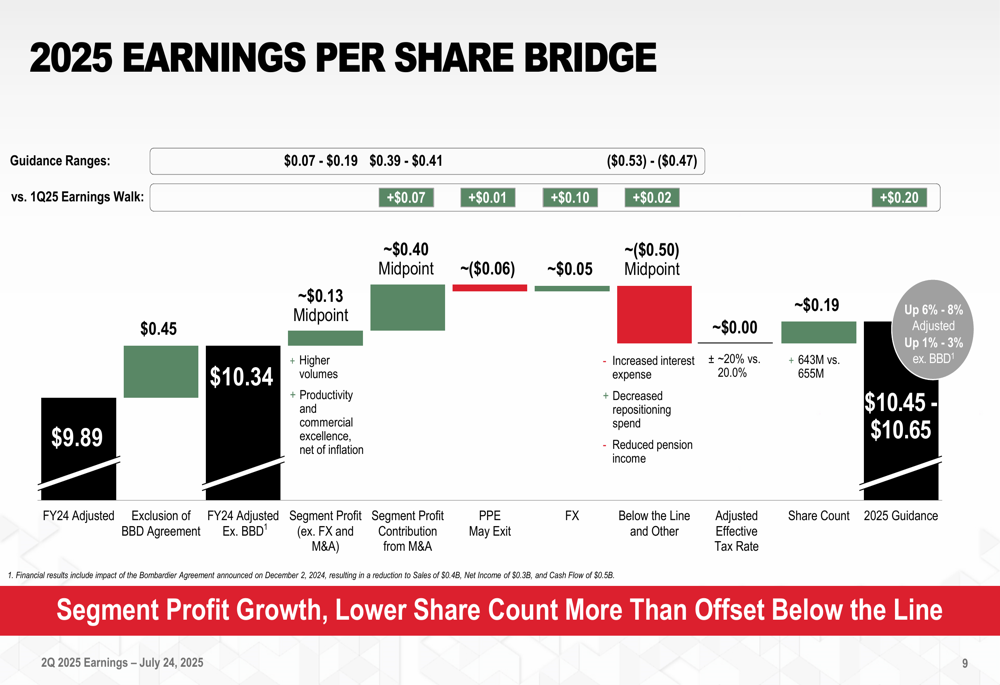

Management provided a detailed bridge analysis showing how various factors contribute to the expected EPS growth for 2025:

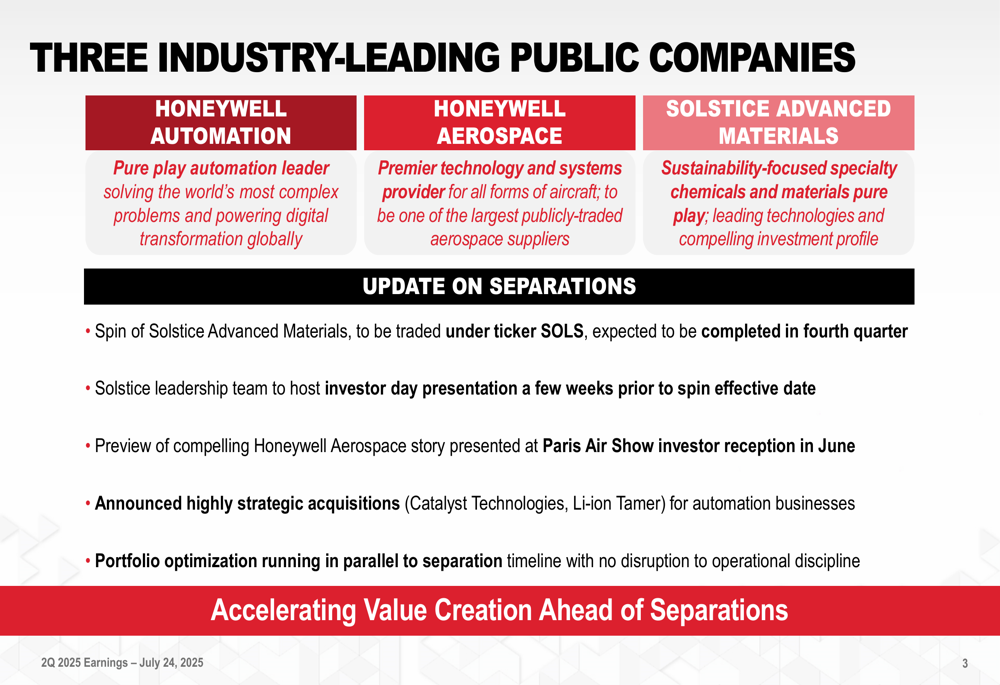

Portfolio Transformation Progress

A central theme of Honeywell’s presentation was the ongoing transformation of its portfolio into three independent public companies. This strategic initiative, first announced earlier in 2025, continues to progress according to plan.

The company outlined the three future entities and provided updates on the separation process:

The spin-off of Solstice Advanced Materials under the ticker SOLS is expected to be completed in the fourth quarter of 2025, with an investor day planned a few weeks prior to the effective date. The company also highlighted recent strategic acquisitions, including Catalyst Technologies and Li-ion Tamer for its automation businesses.

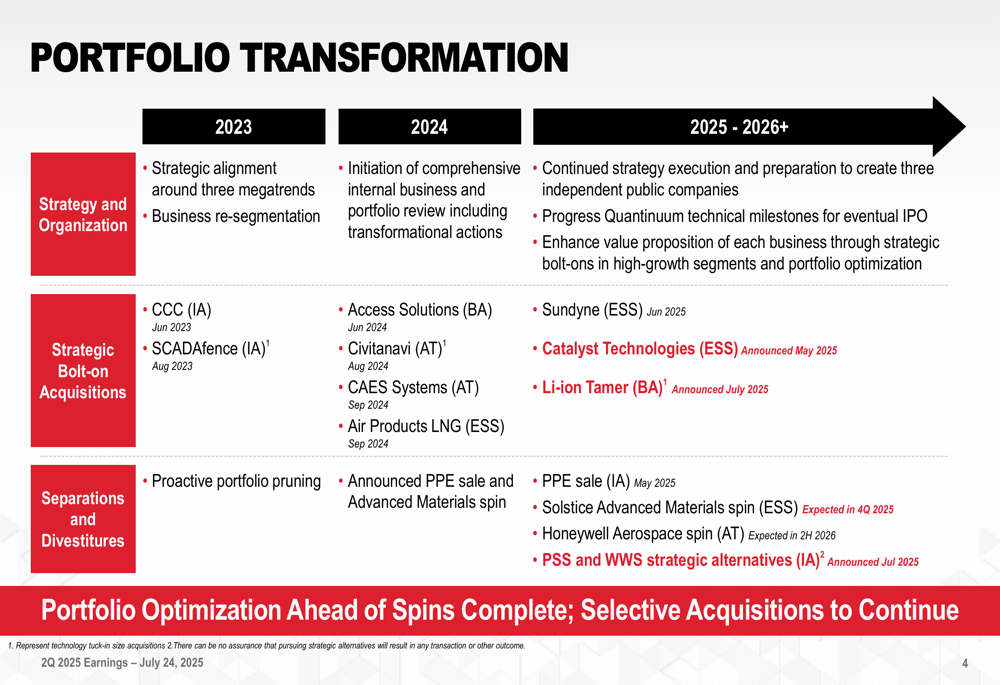

Honeywell’s transformation timeline shows a methodical approach to creating these three independent entities:

Strategic Outlook & Challenges

While Honeywell’s overall performance was strong, management acknowledged several challenges in the current business environment. The company noted that tariff impacts have been "well contained so far," but described the situation as "fluid" with potential demand impacts.

The summary slide highlighted both achievements and ongoing focus areas:

Management emphasized that the company has achieved a record backlog while prudently increasing its full-year adjusted EPS and organic sales growth guidance. The company continues to balance capital deployment between accelerated share repurchases and strategic bolt-on acquisitions.

The presentation revealed that Honeywell is maintaining its disciplined approach to portfolio optimization ahead of the planned separations, with selective acquisitions expected to continue. The company expressed confidence in creating positive momentum through both fundamental execution and transformational initiatives.

Forward-Looking Statements

Looking ahead, Honeywell’s guidance reflects cautious optimism about its ability to navigate economic uncertainties while executing its transformation strategy. The company’s sales bridge for 2025 illustrates how organic growth and acquisitions are expected to offset the impact of divestitures:

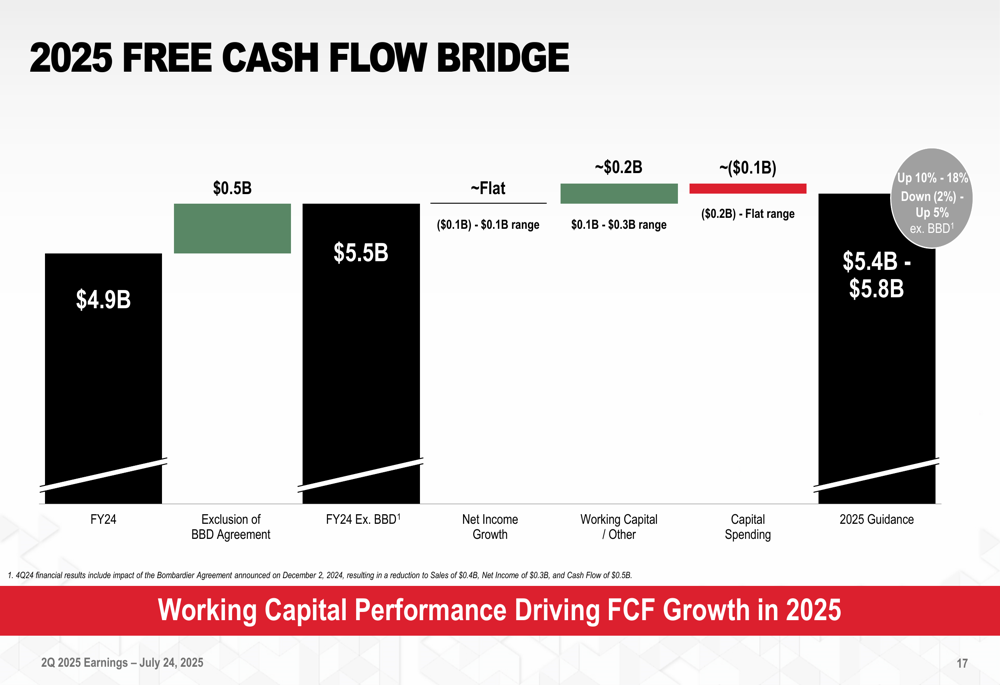

Similarly, the free cash flow bridge shows that working capital performance is expected to be the primary driver of cash flow growth in 2025:

With the separation of Solstice Advanced Materials scheduled for Q4 2025 and continued progress on creating Honeywell Automation and Honeywell Aerospace as standalone entities, the company appears well-positioned to complete its strategic transformation while delivering on its operational commitments for the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.