AirNet Technology raises $180 million in digital assets offering

Introduction & Market Context

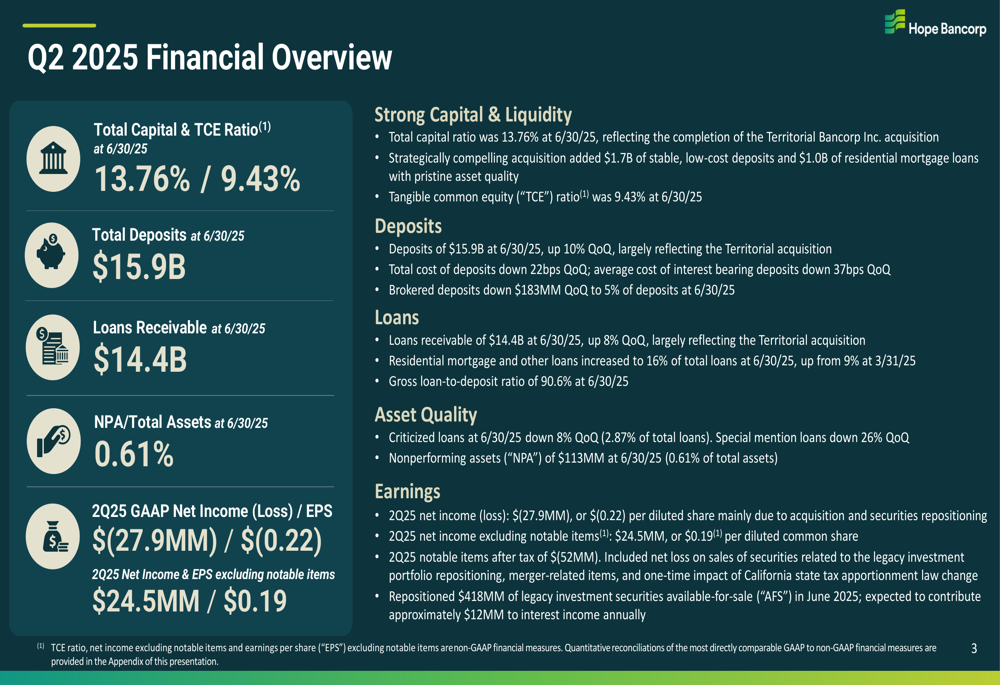

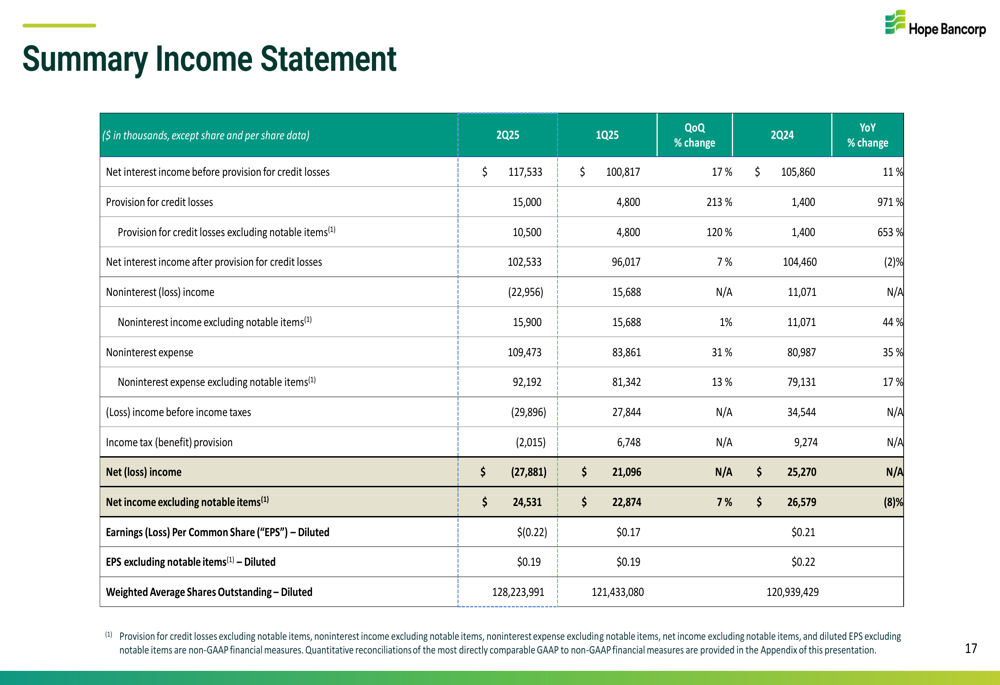

Hope Bancorp (NASDAQ:HOPE) reported a GAAP net loss of $27.9 million or $(0.22) per share for the second quarter of 2025, as revealed in its earnings presentation on July 22, 2025. However, excluding notable items related to its Territorial Bancorp (NASDAQ:TBNK) acquisition and securities repositioning, the bank posted net income of $24.5 million or $0.19 per share.

The bank’s stock closed at $11.36 on July 21, 2025, down 0.26% ahead of the earnings release, and remains closer to its 52-week low of $8.82 than its high of $14.54. This follows a first quarter where Hope Bancorp had exceeded analyst expectations with EPS of $0.17 versus forecasts of $0.13.

Quarterly Performance Highlights

Hope Bancorp’s second quarter results were significantly impacted by one-time items, creating a stark contrast between GAAP and adjusted figures. The company’s core operations showed improvement, with net interest margin expanding to 2.69% from 2.54% in the previous quarter.

As shown in the following financial overview:

Net interest income increased to $118 million in Q2 2025, up from $101 million in Q1 2025, representing a 17% quarter-over-quarter improvement. This growth was driven by the Territorial acquisition and the repositioning of $418 million in legacy investment securities, which is expected to contribute approximately $12 million to interest income annually.

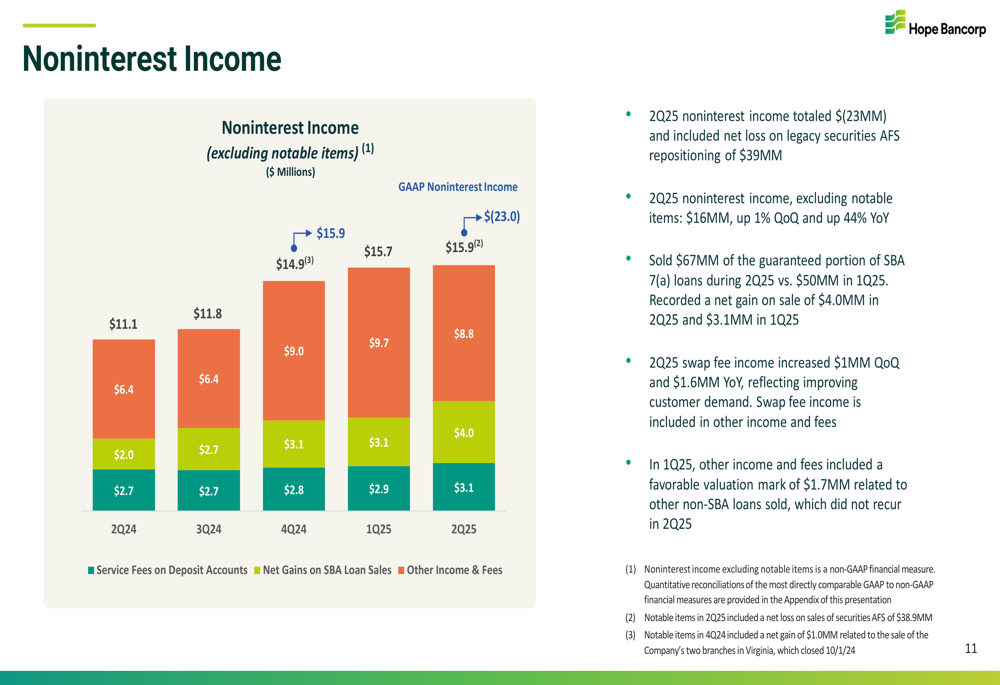

The bank’s noninterest income, excluding notable items, reached $15.9 million, a slight 1% increase from the previous quarter but a substantial 44% improvement year-over-year. However, GAAP noninterest income was negative at $(23.0) million due to one-time charges.

The following chart illustrates the noninterest income trend:

Noninterest expenses increased to $92.2 million (excluding notable items), up 13% quarter-over-quarter, primarily due to the integration of Territorial Bancorp. This contributed to an efficiency ratio of 115.8% on a GAAP basis, though the adjusted efficiency ratio was 69.1%.

Acquisition Impact

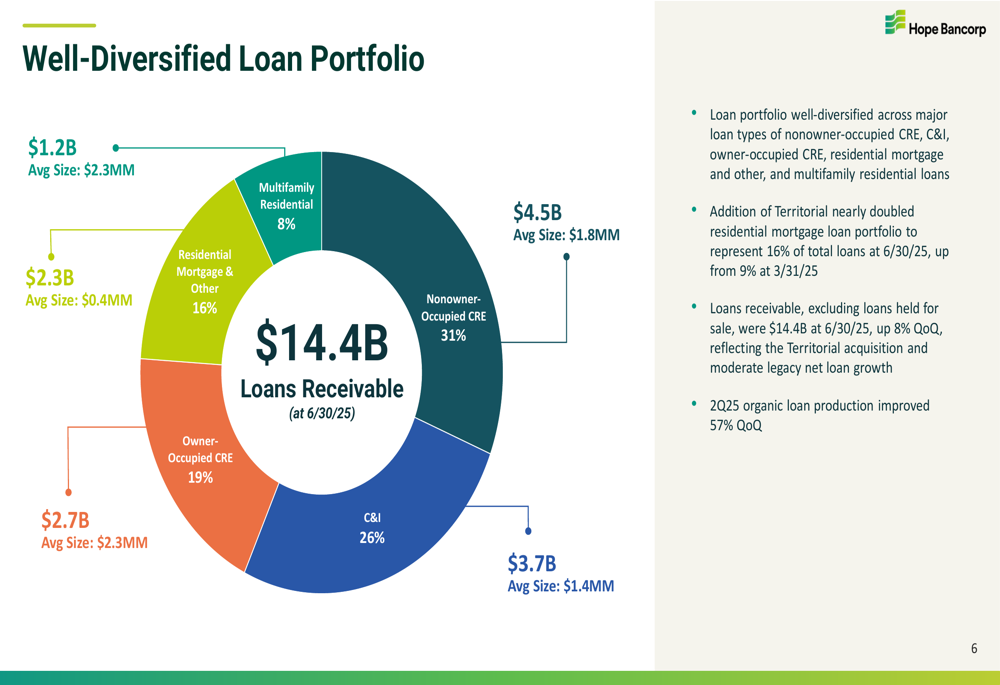

The completion of the Territorial Bancorp acquisition has significantly transformed Hope Bancorp’s balance sheet and market presence. Total (EPA:TTEF) deposits grew to $15.9 billion, a 10% increase quarter-over-quarter, while loans receivable expanded to $14.4 billion, up 8% from the previous quarter.

The acquisition has particularly strengthened Hope’s residential mortgage portfolio, which nearly doubled, enhancing the bank’s loan diversification as shown in this breakdown:

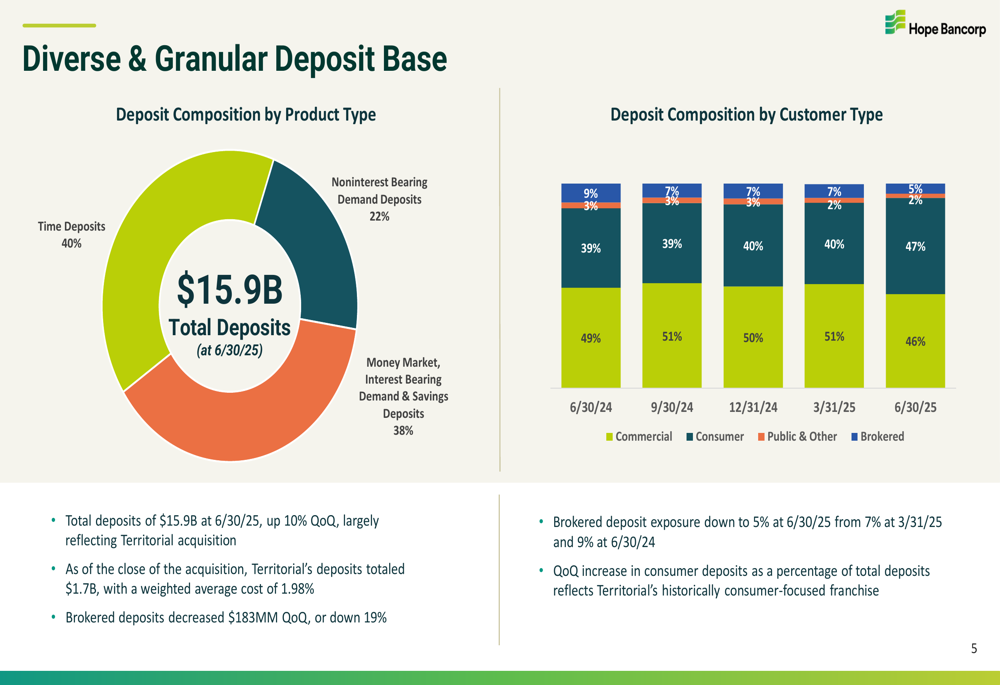

The deposit base remains well-diversified across product types and customer segments, with a healthy balance between commercial (46%) and consumer (47%) deposits:

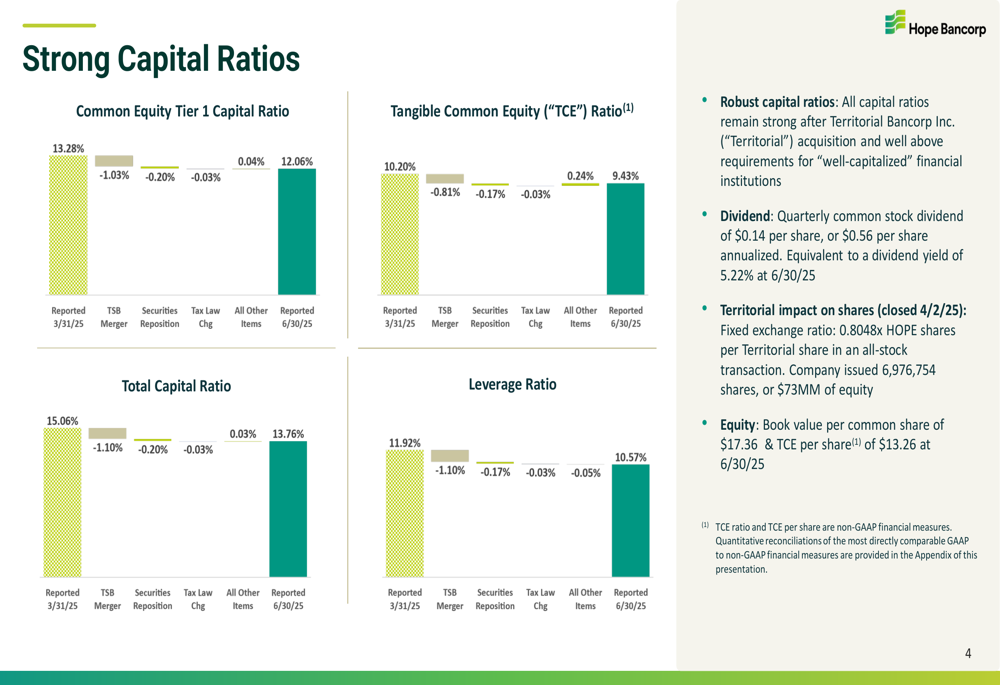

The Territorial acquisition had a measurable impact on capital ratios, though they remain strong. The Common Equity Tier 1 Capital Ratio decreased from 13.28% to 12.06%, while the Tangible Common Equity Ratio declined from 10.20% to 9.43%, as illustrated in this capital analysis:

Balance Sheet Strength

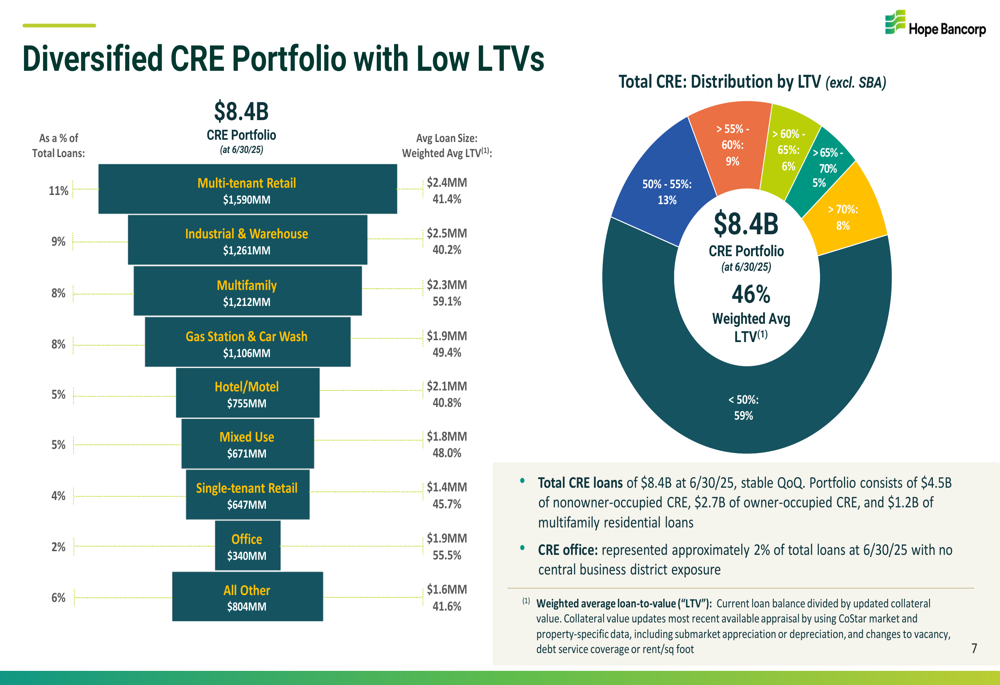

Hope Bancorp’s commercial real estate (CRE) portfolio, which represents a significant portion of its loan book at $8.4 billion, maintains low loan-to-value ratios with a weighted average of 46%. This conservative approach provides substantial cushion against potential market downturns.

The following chart details the CRE portfolio composition and LTV metrics:

Notably, office exposure is limited to approximately 2% of total loans with no central business district exposure, reducing vulnerability to ongoing challenges in the commercial office sector.

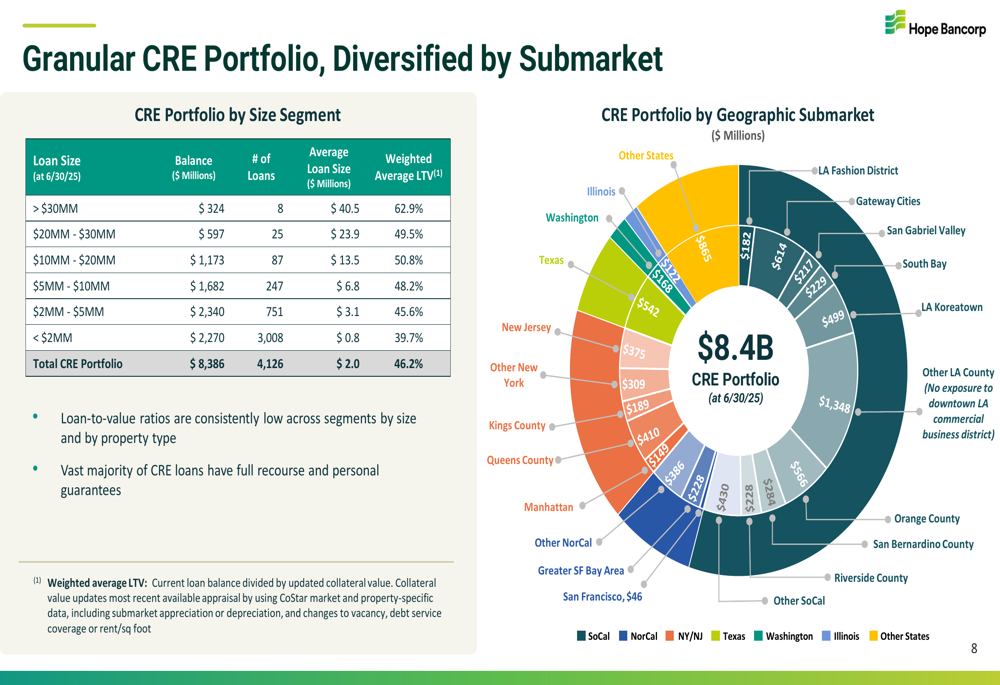

The bank’s CRE portfolio is also well-diversified geographically, with no excessive concentration in any single submarket:

Asset quality remained stable with nonperforming assets to total assets at 0.61%. The allowance for credit losses coverage ratio declined slightly to 1.04% from 1.15% in the previous quarter, partly reflecting the addition of Territorial’s residential mortgage loans, which have historically demonstrated excellent credit quality.

Forward-Looking Statements

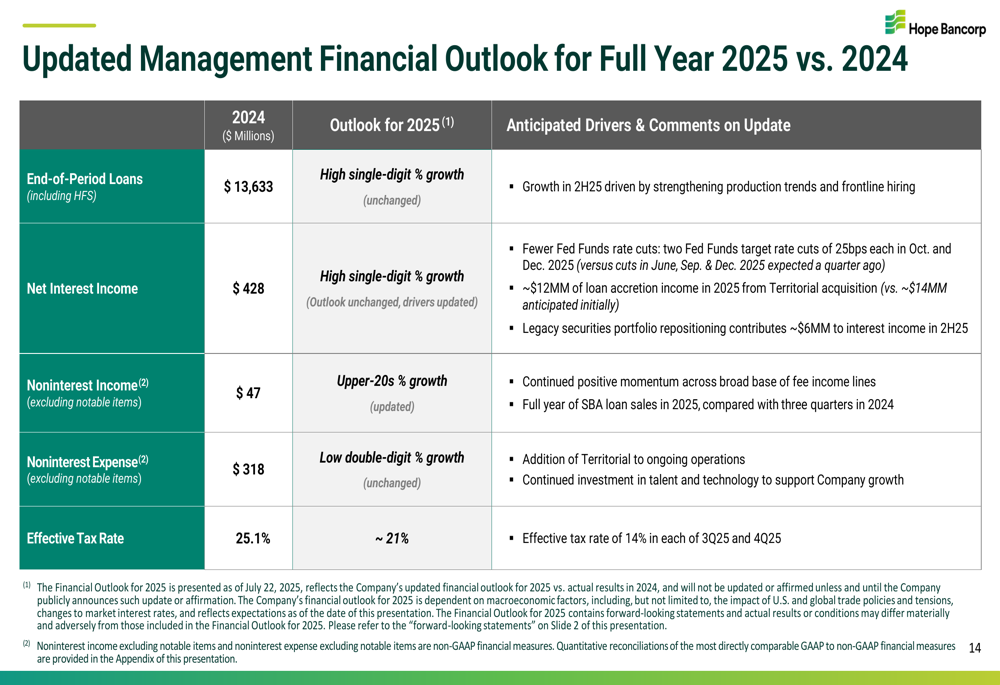

Management provided an updated financial outlook for the full year 2025, maintaining a positive growth trajectory across key metrics:

The bank expects high single-digit percentage growth in both end-of-period loans and net interest income compared to 2024. Noninterest income is projected to grow in the upper-20s percentage range, slightly higher than the mid-20s guidance provided in Q1.

Noninterest expenses are anticipated to increase at a low double-digit percentage rate, reflecting the full-year impact of the Territorial acquisition. The effective tax rate is expected to be approximately 21%, down from 25.1% in 2024.

Detailed Financial Analysis

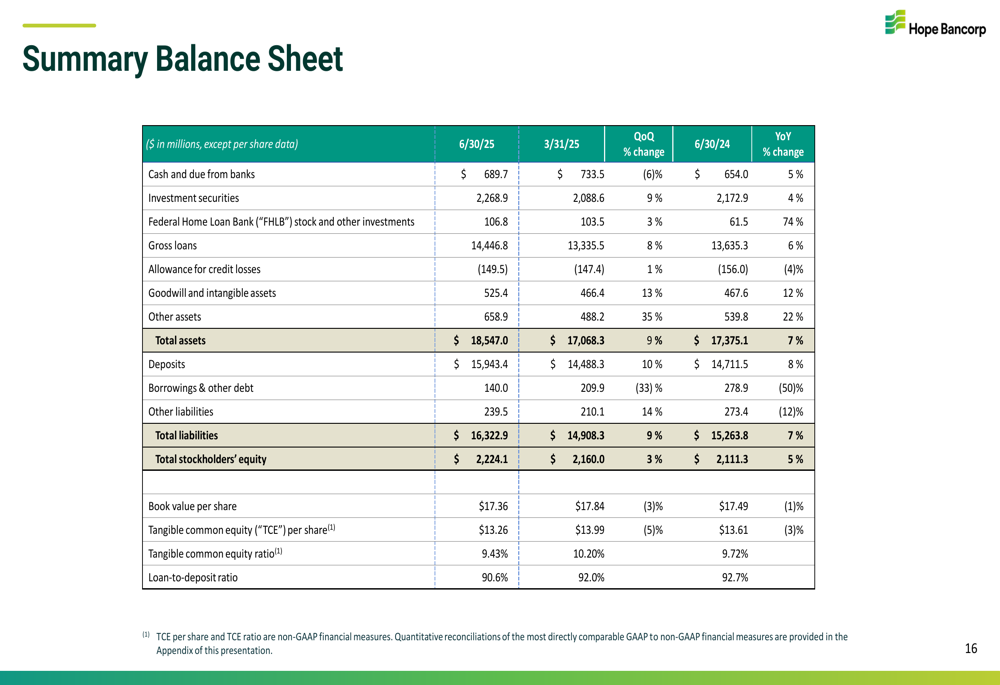

Hope Bancorp’s balance sheet as of June 30, 2025, showed total assets of $18.55 billion, up from $16.46 billion at the end of the first quarter. The loan-to-deposit ratio stood at 90.6%, indicating a balanced approach to lending relative to funding sources.

The summary balance sheet provides a comprehensive view of the bank’s financial position:

The income statement comparison reveals the significant impact of notable items on Q2 results:

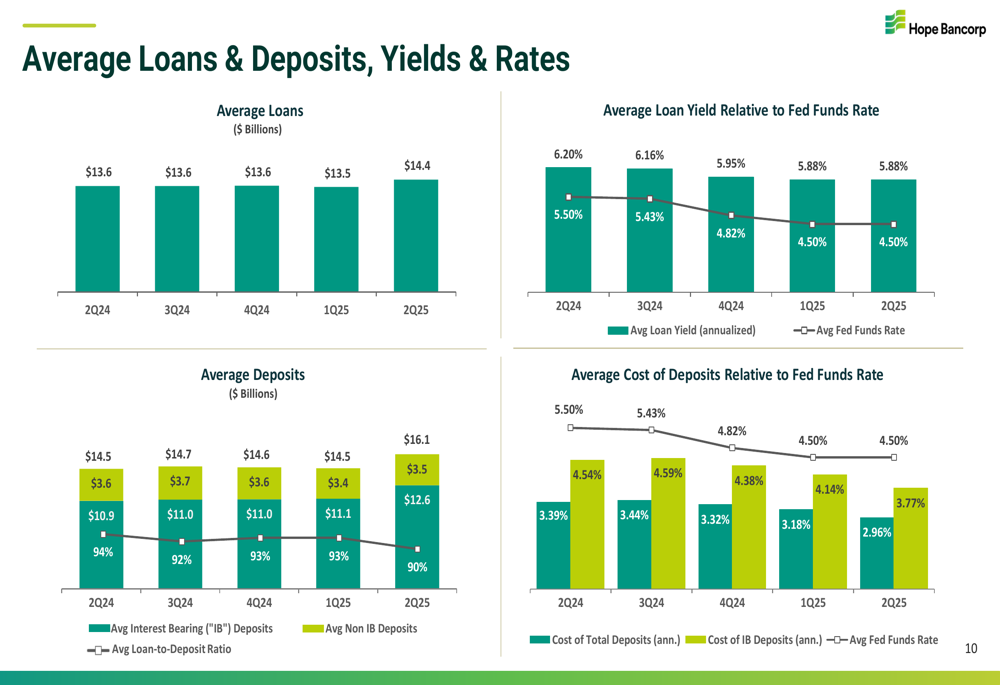

Net interest margin improvement was supported by rising loan yields relative to the Federal Funds Rate, as shown in the following chart tracking yields and rates:

With the integration of Territorial Bancorp progressing and the securities repositioning expected to enhance interest income, Hope Bancorp appears positioned for improved performance in the second half of 2025, provided it can successfully manage integration costs and capitalize on its expanded deposit and loan base.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.