How are energy investors positioned?

Introduction & Market Context

Hormel Foods Corporation (NYSE:HRL) presented its second quarter fiscal 2025 results on May 29, 2025, highlighting solid top-line growth while narrowing its full-year guidance. The company’s stock was trading down 0.57% in premarket at $29.87, reflecting investor caution following the presentation.

The food manufacturer, known for brands including Planters, Jennie-O, and SPAM, emphasized its portfolio of "consumer-focused, protein-centric products" as it navigates a challenging market environment. This follows a disappointing first quarter where Hormel missed EPS expectations, reporting $0.35 against forecasts of $0.39.

Quarterly Performance Highlights

Hormel reported mixed performance across its three business segments in Q2. The Retail segment maintained flat net sales compared to the prior year while improving segment profit by 4%, despite a 7% volume decline. Management attributed two-thirds of this volume decline to lower commodity shipments and contract manufacturing rather than core brand performance.

The Foodservice segment delivered 4% organic net sales growth but experienced a 6% decrease in segment profit, as higher sales were offset by margin pressures in non-core businesses. Meanwhile, the International segment showed strong volume and sales growth of 9% and 7% respectively, but segment profit declined significantly by 21%.

As shown in the following chart, Hormel’s Applegate brand has demonstrated consistent growth over the past five quarters, maintaining positive momentum with 6% growth in Q2 FY25:

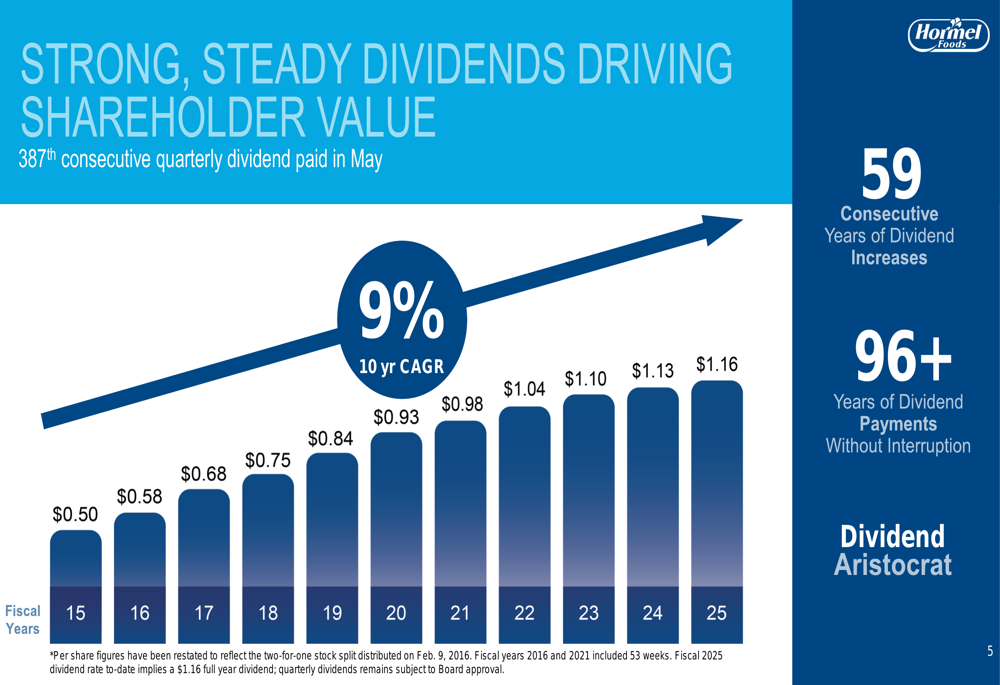

The company continues to emphasize its impressive dividend history as a key strength for investors. Hormel paid its 387th consecutive quarterly dividend in May and has increased dividends for 59 consecutive years, earning its status as a "Dividend Aristocrat."

As illustrated in this dividend growth chart, Hormel has increased its dividend from $0.50 per share in FY2015 to $1.16 in FY2025, representing a 10-year CAGR of 9%:

Detailed Financial Analysis

The Retail segment’s performance was supported by growth in the Mexican portfolio and value-added turkey products, which offset promotional timing impacts. Management highlighted that Planters exceeded expectations while Jennie-O lean ground turkey saw strong demand. Operational efficiencies from the company’s Transform and Modernize (T&M) initiative contributed to the segment’s profit improvement.

In the Foodservice segment, organic net sales growth was broad-based with contributions from the customized solutions business and turkey portfolio. Branded products including Jennie-O, Hormel Fire Braised, and Café H delivered strong results, though volume growth in several categories was offset by reduced commodity shipments.

The International segment’s double-digit volume and net sales growth in exports, along with robust growth in the China market, drove top-line performance. However, segment profit decreased due to what management described as a temporary shift in export customer mix and softness in Brazil.

Strategic Initiatives

Hormel outlined several strategic priorities that guided its Q2 performance, including retail business growth, foodservice leadership expansion, global presence development, and snacking vision execution.

Key brand highlights included:

- Applegate brand outpacing total edible category consumption

- Jennie-O ground turkey experiencing notable sales growth

- Wholly and Herdez (BMV:HERDEZ) refrigerated guacamole portfolio seeing double-digit consumption growth

- Planters brand showing sequential improvement in distribution and retail sales

- Introduction of new products including Corn Nuts partially popped corn kernels and Hormel Gatherings bold and spicy tray

The company also reported progress on its Transform and Modernize initiative, including the beginning of operations at a new distribution center and network optimization that led to the announced closure of one dry sausage facility. The T&M initiative is expected to deliver incremental benefits in the range of $100-150 million.

Forward-Looking Statements

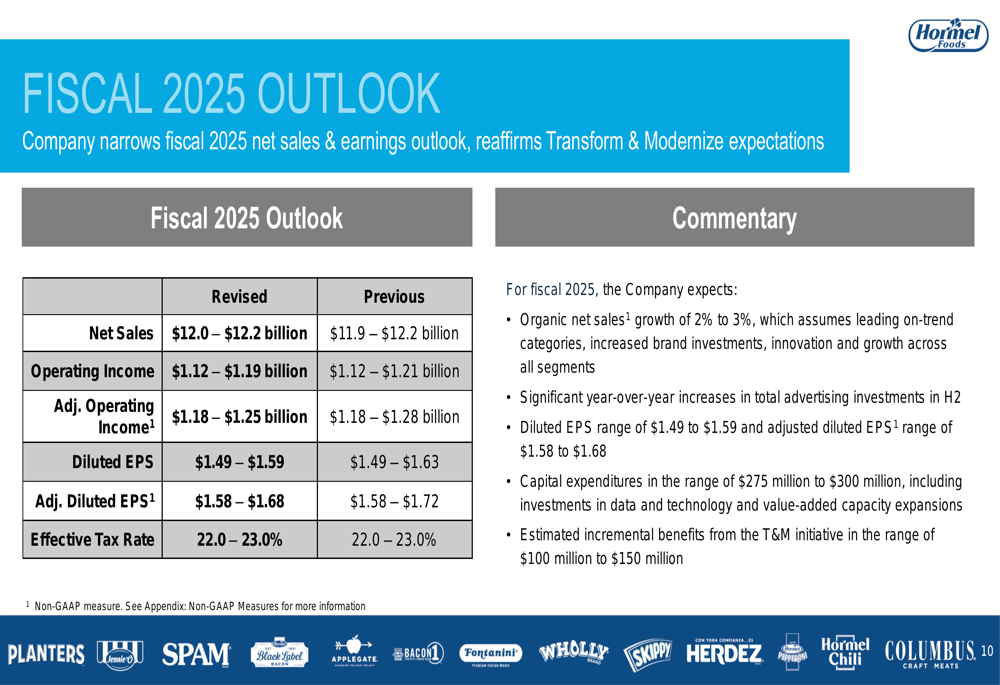

Hormel narrowed its fiscal 2025 guidance ranges, suggesting more clarity but slightly reduced expectations for the upper end of its projections:

The revised outlook includes:

- Net Sales: $12.0-$12.2 billion (narrowed from $11.9-$12.2 billion)

- Operating Income: $1.12-$1.19 billion (narrowed from $1.12-$1.21 billion)

- Adjusted Operating Income: $1.18-$1.25 billion (narrowed from $1.18-$1.28 billion)

- Diluted EPS: $1.49-$1.59 (narrowed from $1.49-$1.63)

- Adjusted Diluted EPS: $1.58-$1.68 (narrowed from $1.58-$1.72)

The company expects organic net sales growth of 2-3% for the full year and plans to increase brand investments, innovation, and growth across all segments. Significant year-over-year increases in total advertising investments are planned for the second half of fiscal 2025.

Hormel’s long-term strategy aims to deliver 2-3% organic net sales growth and 5-7% operating income growth, as outlined in its strategic framework:

Capital expenditures are planned in the range of $275-300 million, including investments in data and technology and value-added capacity expansions, as the company continues to position itself for long-term growth in the competitive food manufacturing landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.