Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Hudson (NYSE:HUD) Global Inc (NASDAQ:HSON) released its second-quarter 2025 earnings presentation on August 8, 2025, revealing improved profitability metrics despite essentially flat revenue. The company’s stock, which closed at $9.12 on August 7, showed signs of positive reception with a 1.32% increase to $9.24 in pre-market trading following the release.

The recruitment and contracting services provider continues to trade near the lower end of its 52-week range of $8.26-$18.44, suggesting investors remain cautious despite the improved profitability metrics. This follows a similar pattern from Q1 2025, when the company beat EPS expectations but missed revenue forecasts.

Quarterly Performance Highlights

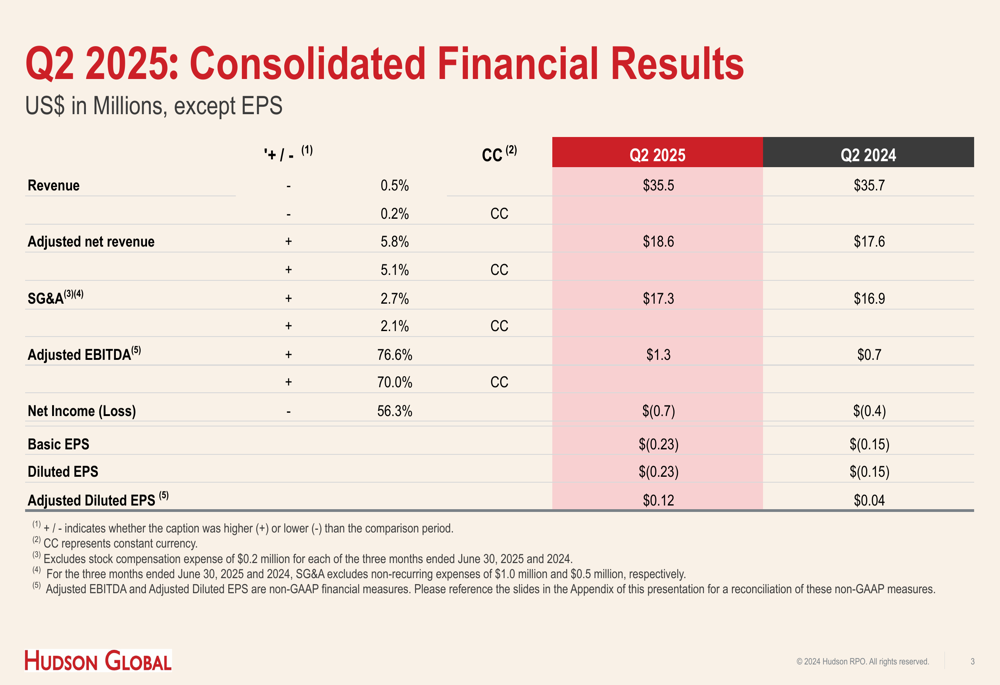

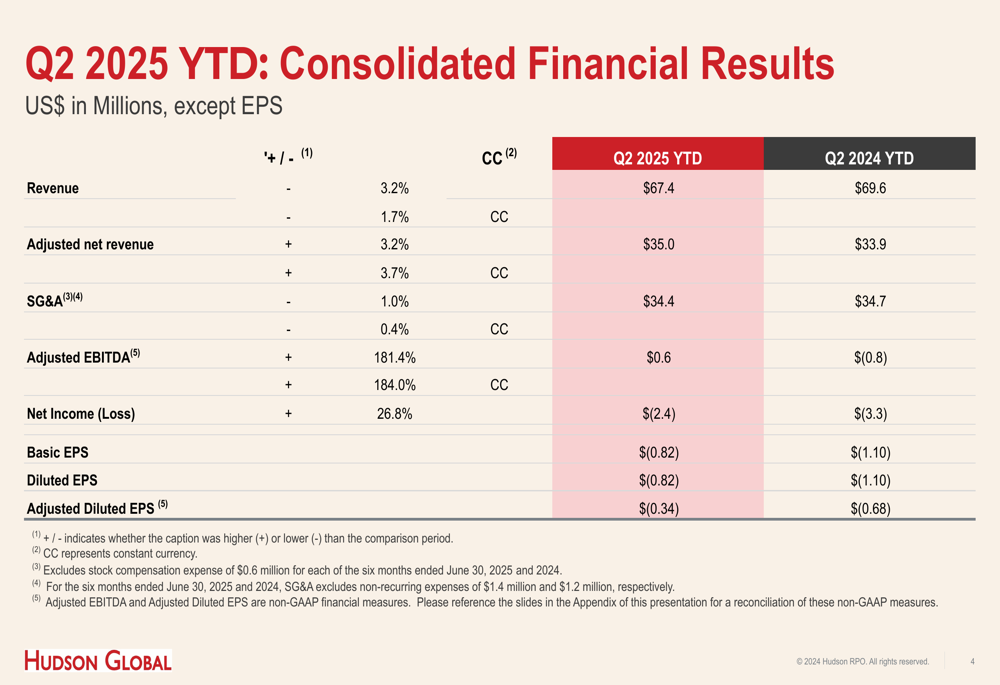

Hudson Global reported Q2 2025 revenue of $35.5 million, a slight decrease of 0.5% compared to $35.7 million in Q2 2024. However, adjusted net revenue increased by 5.8% to $18.6 million, indicating a shift toward higher-margin business.

The company’s profitability metrics showed significant improvement, with adjusted EBITDA jumping 76.6% to $1.3 million compared to $0.7 million in the same period last year. Adjusted diluted EPS tripled to $0.12 from $0.04 in Q2 2024, despite reporting a net loss of $0.7 million for the quarter.

As shown in the following consolidated financial results:

Year-to-date results also reflected improvement, with adjusted EBITDA turning positive at $0.6 million compared to a loss of $0.8 million in the first half of 2024. The company’s net loss for the first six months narrowed to $2.4 million from $3.3 million in the prior year period.

Regional Performance Analysis

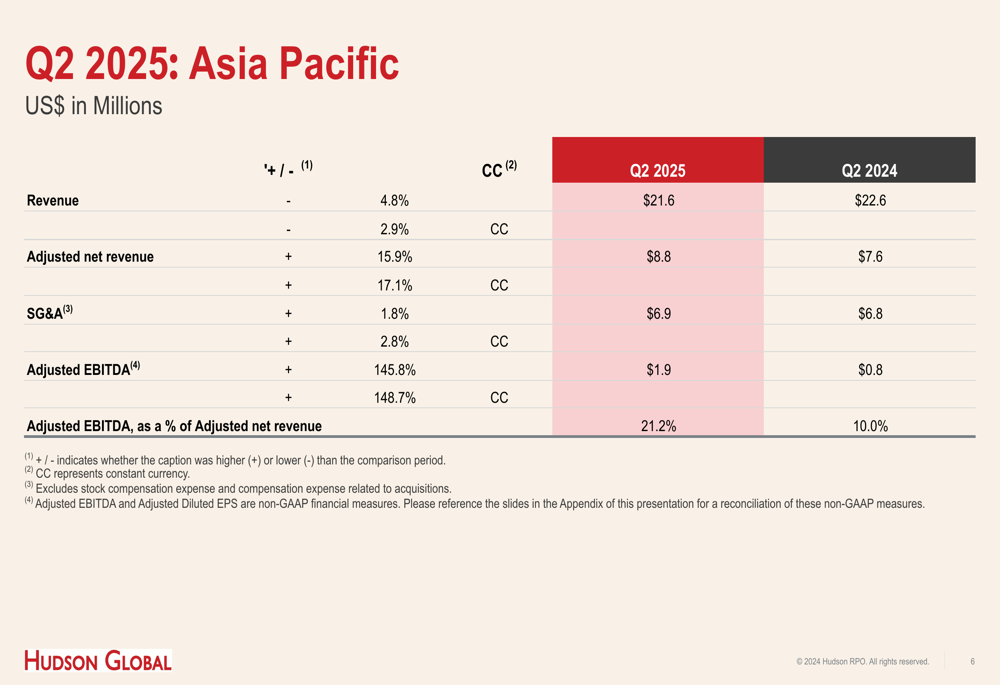

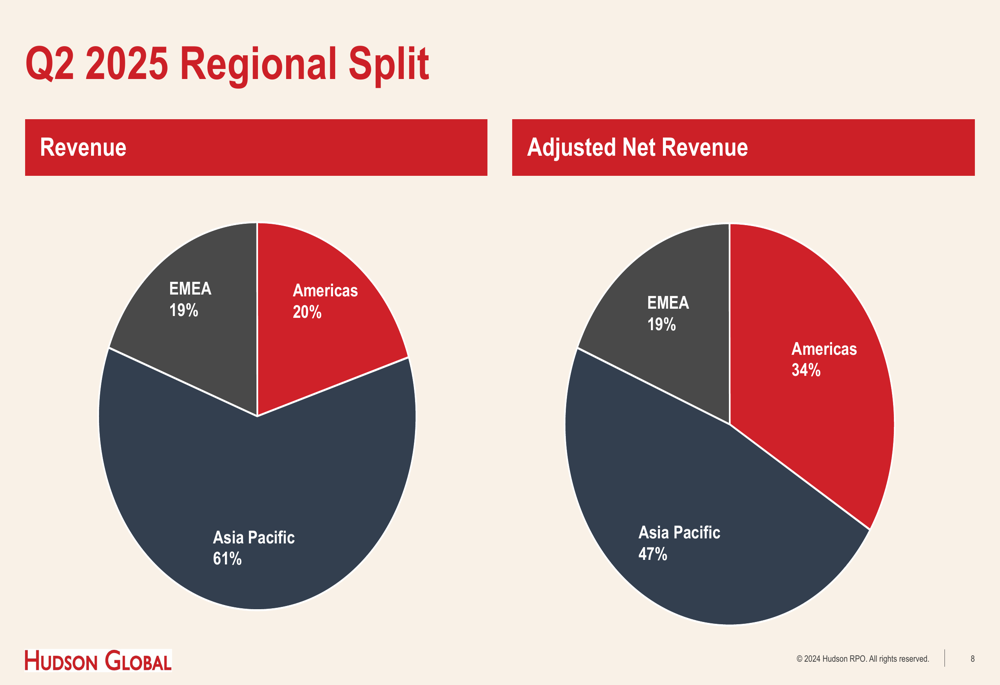

Hudson Global’s performance varied significantly across regions, with Asia Pacific emerging as the clear growth driver while EMEA faced challenges.

The Asia Pacific region, which accounts for 61% of total revenue and 47% of adjusted net revenue, delivered exceptional results with a 145.8% increase in adjusted EBITDA to $1.9 million. This performance came despite a 4.8% decrease in revenue, as adjusted net revenue grew by 15.9%, demonstrating improved margins in the region.

The Americas region, representing 20% of total revenue and 34% of adjusted net revenue, showed modest improvement with an 8.8% increase in adjusted EBITDA to $0.7 million on relatively flat revenue.

In contrast, the EMEA region struggled significantly, swinging from a positive adjusted EBITDA of $0.3 million in Q2 2024 to a loss of $0.4 million in Q2 2025, despite a 12.2% increase in revenue. This concerning performance in Europe, Middle East, and Africa suggests operational challenges that may require management attention.

The regional distribution of Hudson Global’s business is illustrated in the following charts:

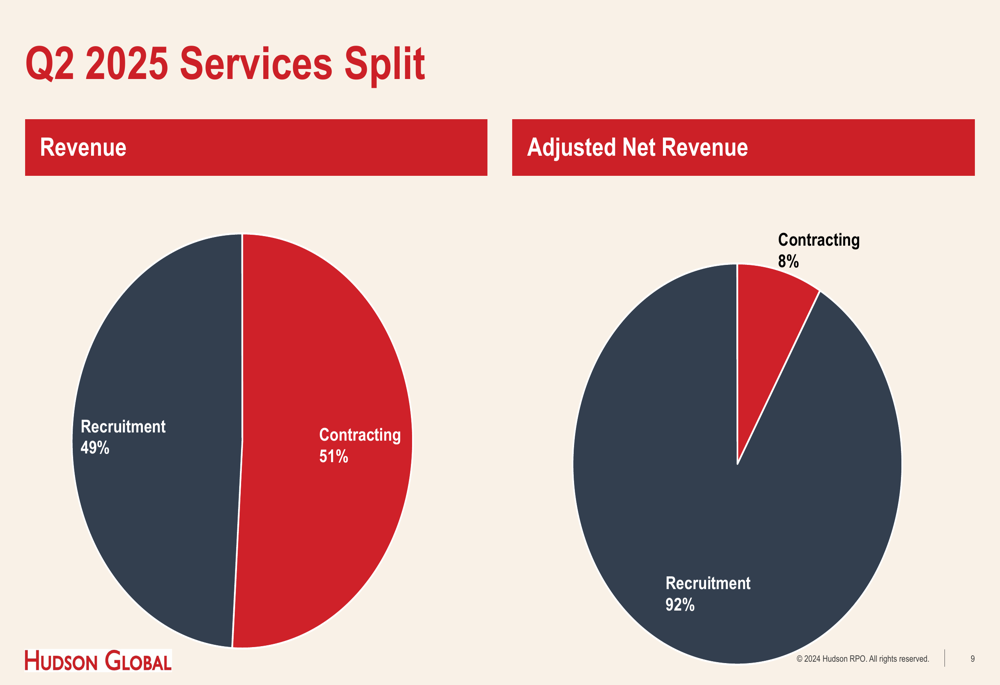

Service Mix Analysis

Hudson Global’s presentation revealed an important insight into its business model through the breakdown of services between contracting and recruitment. While contracting accounts for 51% of total revenue, it generates only 8% of adjusted net revenue. Conversely, recruitment services represent 49% of revenue but deliver a substantial 92% of adjusted net revenue.

This stark contrast highlights the significantly higher margins in recruitment services and explains the company’s ability to improve profitability metrics despite flat overall revenue.

The service split is clearly illustrated in the following charts:

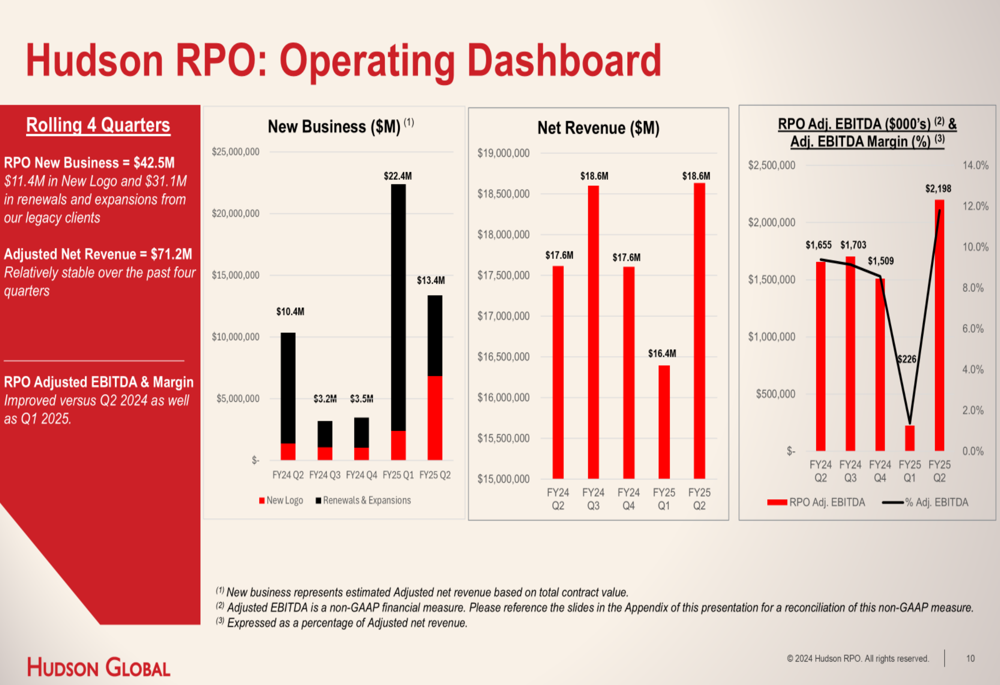

Business Performance Trends

The company’s RPO (Recruitment Process Outsourcing) operating dashboard showed positive momentum in new business acquisition, with $42.5 million in new business over the rolling four quarters, including $11.4 million from new logos and $31.1 million from renewals and expansions.

The quarterly trend data indicates improving adjusted EBITDA margins, suggesting operational efficiencies are taking hold despite market challenges.

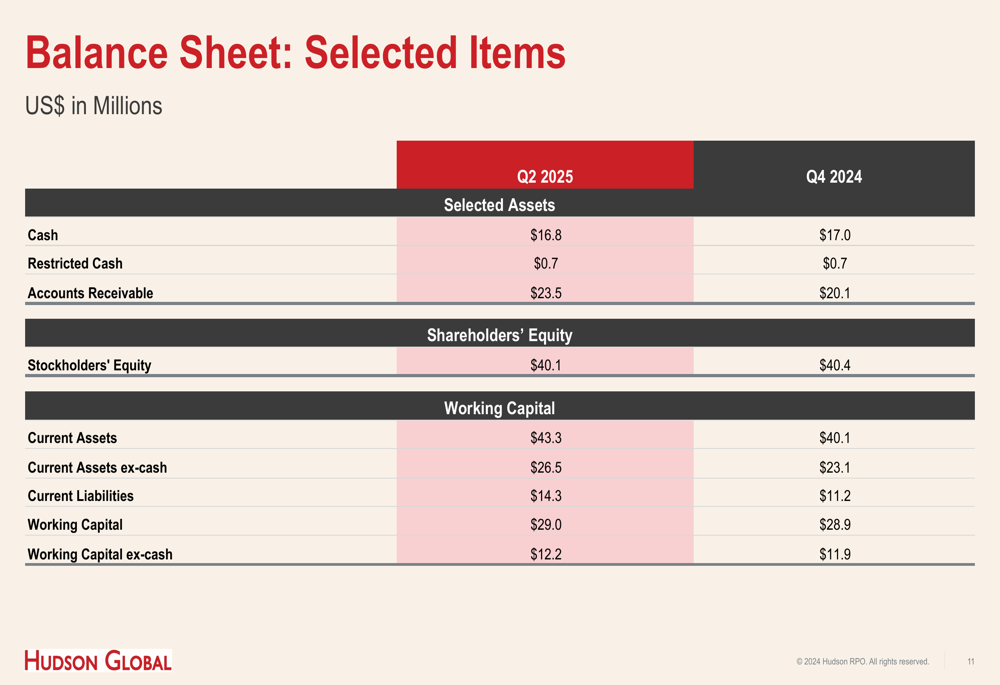

Balance Sheet and Cash Flow

Hudson Global maintained a solid financial position with $16.8 million in cash as of Q2 2025, slightly down from $17.0 million at the end of 2024. The company’s working capital remained stable at $29.0 million, providing adequate liquidity for operations.

Cash flow from operations showed significant improvement, turning positive at $0.1 million for the quarter compared to a negative $4.3 million in Q2 2024. Year-to-date cash flow from operations also improved substantially to negative $0.7 million from negative $6.1 million in the prior year period.

Strategic Initiatives and Outlook

Based on the Q1 2025 earnings call information, Hudson Global is pursuing several strategic initiatives that likely continued into Q2, including the launch of "Hudson Fusion," a new digital division focused on AI technology expected by the end of Q3 or beginning of Q4 2025.

The company also appears to be focusing on geographic expansion in high-growth markets, particularly in the Middle East, Latin America, and India, while managing through challenges in more established markets.

The significant improvement in Asia Pacific performance suggests that the company’s strategic focus on this region is yielding positive results, potentially offsetting weaknesses in the EMEA region.

Conclusion

Hudson Global’s Q2 2025 presentation reveals a company in transition, successfully improving profitability metrics and cash flow despite flat revenue. The stark regional performance differences highlight both opportunities and challenges, with Asia Pacific emerging as the clear growth engine while EMEA requires attention.

The company’s focus on high-margin recruitment services appears to be paying dividends, though investors may remain cautious until revenue growth resumes. With the stock trading near the lower end of its 52-week range, market sentiment suggests a wait-and-see approach despite the improved profitability metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.