BETA Technologies launches IPO of 25 million shares priced $27-$33

Introduction & Market Context

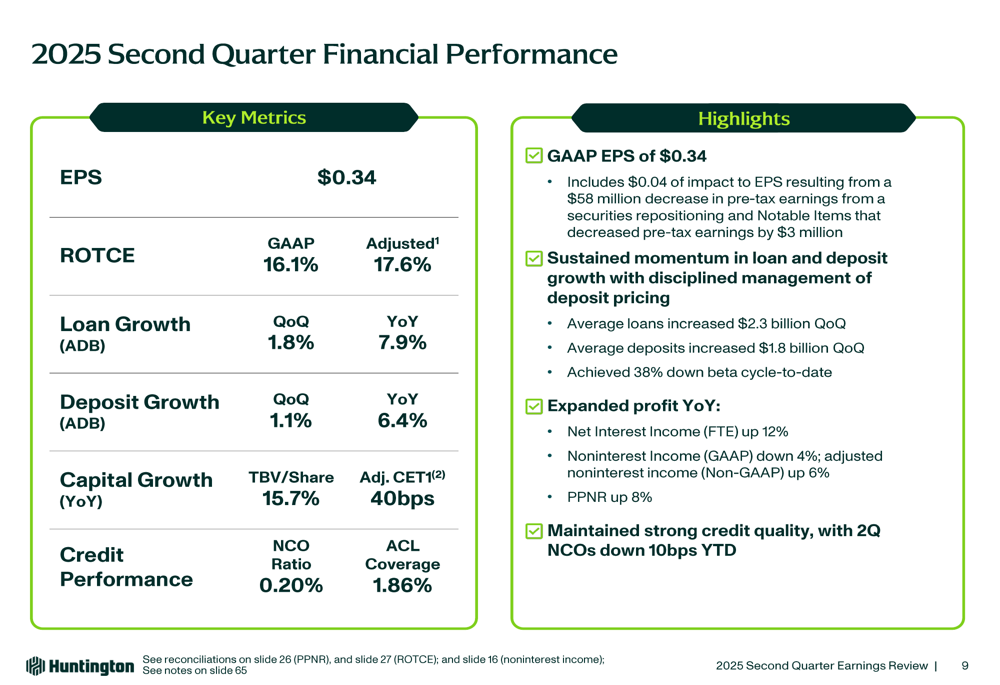

Huntington Bancshares Incorporated (NASDAQ:HBAN) released its second quarter 2025 earnings presentation on July 18, 2025, revealing continued strong performance across key metrics. The bank reported earnings per share of $0.34, which included a $0.04 impact from securities repositioning. Following the release, Huntington’s stock was trading at $17.03 in premarket, up 0.29% from the previous close of $16.98.

The Q2 results build on Huntington’s strong first quarter, when the bank also reported EPS of $0.34, exceeding analyst expectations. The presentation highlights Huntington’s vision to be the leading "People-First, Customer-Centered Bank in the Country" while delivering value through top-quartile performance.

Quarterly Performance Highlights

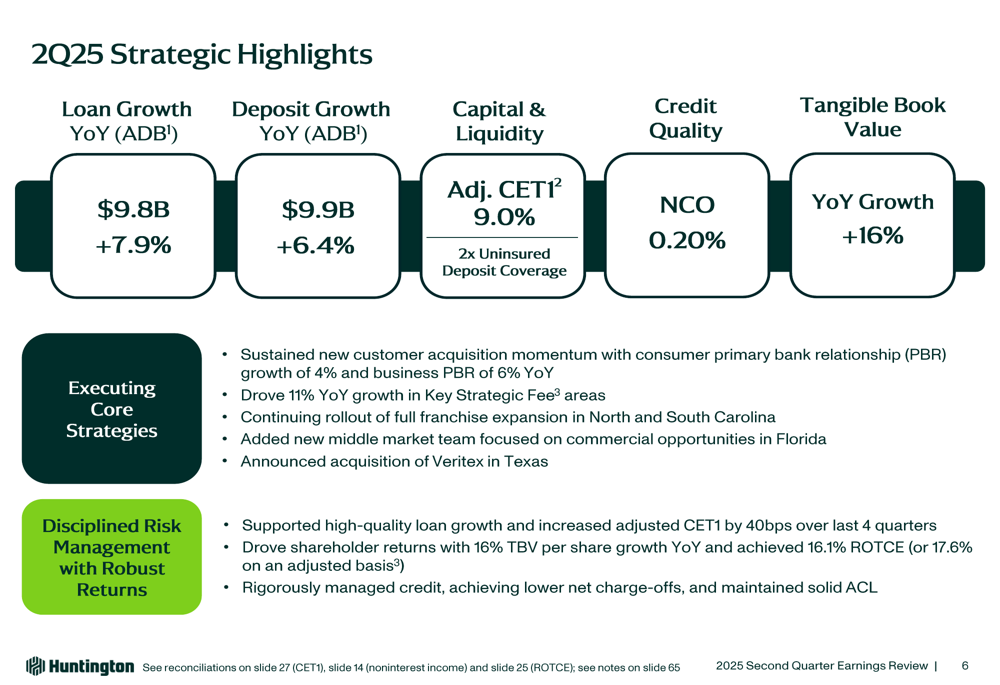

Huntington delivered robust financial results in Q2 2025, with loan growth of 7.9% year-over-year and 1.8% quarter-over-quarter, while deposits grew 6.4% year-over-year and 1.1% quarter-over-quarter. The bank achieved a return on tangible common equity (ROTCE) of 16.1% on a GAAP basis and 17.6% on an adjusted basis.

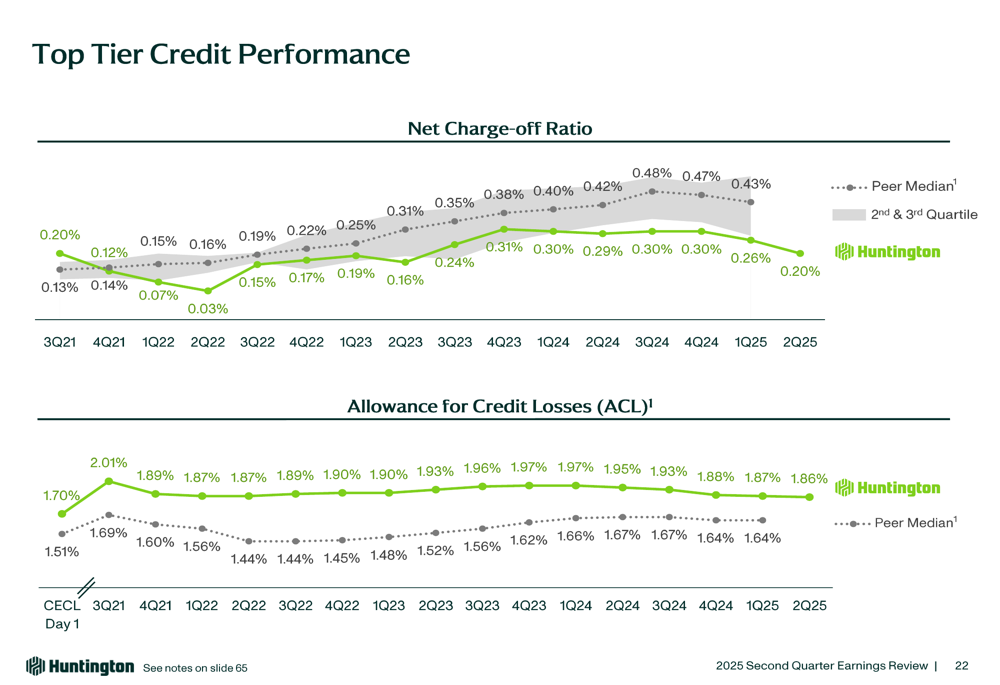

As shown in the following chart of Q2 2025 financial performance, Huntington maintained strong credit quality with a net charge-off ratio of 0.20% and allowance for credit losses coverage of 1.86%:

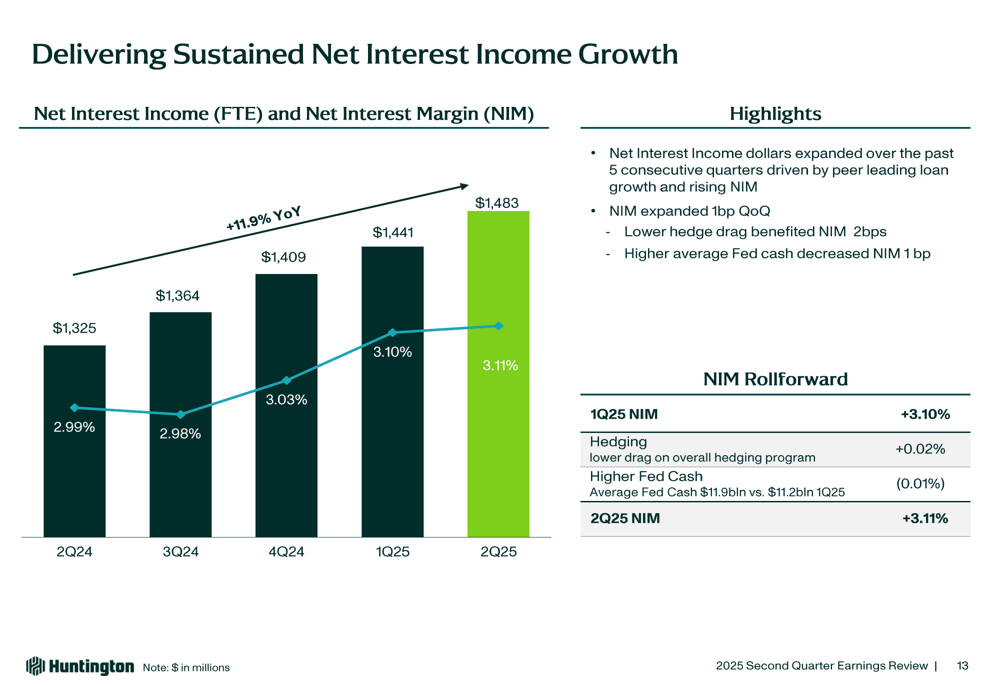

Net interest income increased by 11.9% year-over-year to $1,483 million, while the net interest margin expanded to 3.11%, up from 2.99% in Q2 2024. This improvement came despite the challenging interest rate environment, reflecting the bank’s effective balance sheet management.

The following chart illustrates Huntington’s sustained net interest income growth and margin expansion:

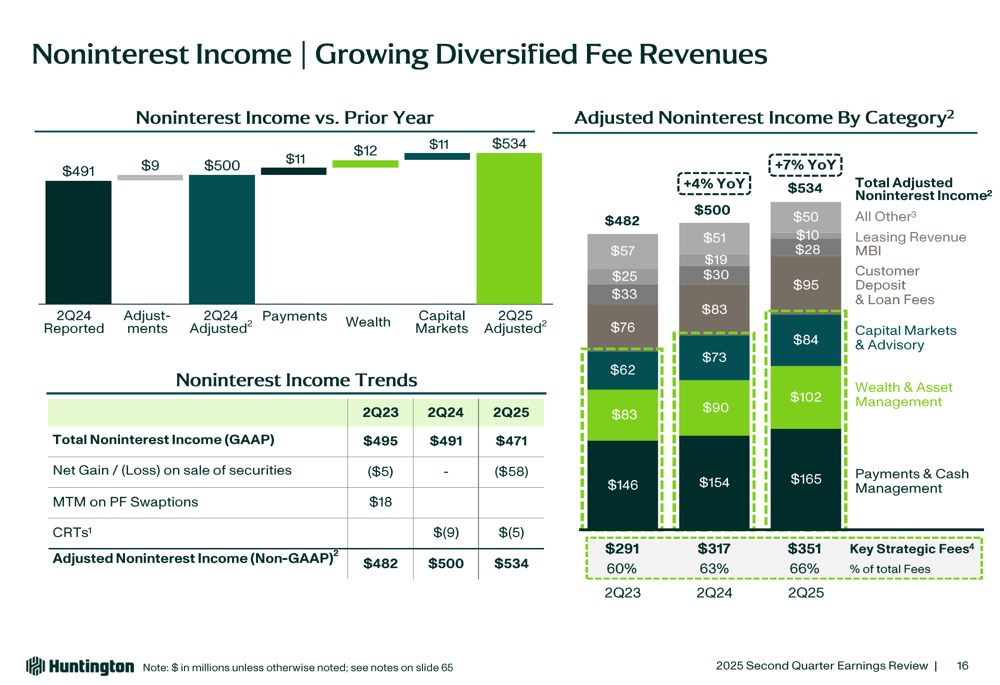

Noninterest income grew to $534 million, up from $491 million in Q2 2024, driven by strong performance in key strategic fee areas including payments, wealth management, and capital markets. The bank’s focus on diversifying revenue streams is evident in the breakdown of fee income sources:

Strategic Initiatives

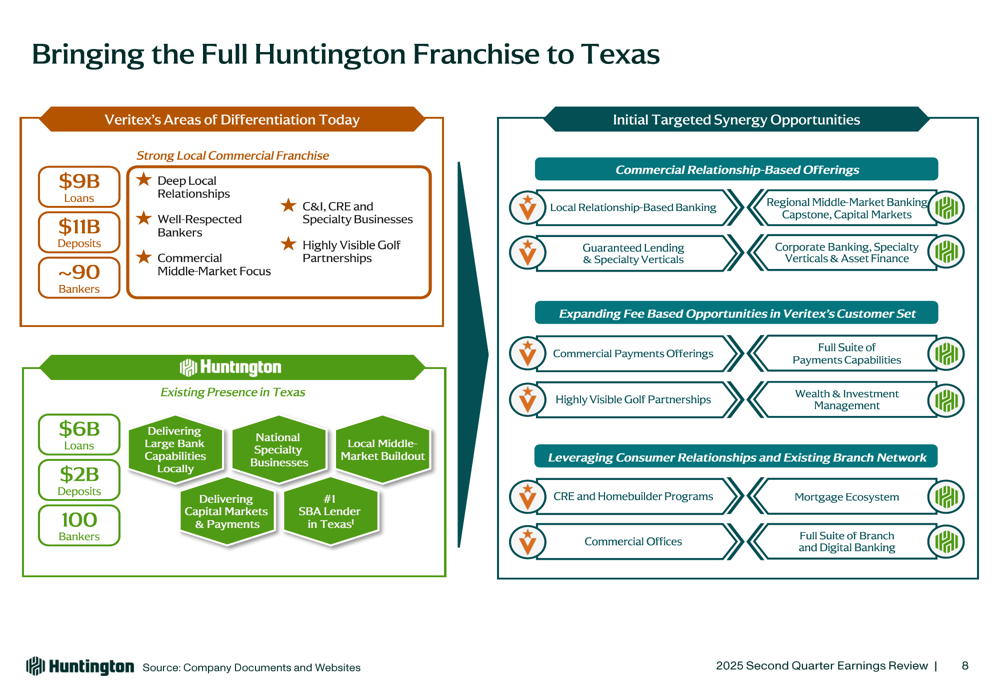

A central element of Huntington’s growth strategy is its expansion in Texas through the acquisition of Veritex (NASDAQ:VBTX). This partnership accelerates Huntington’s organic growth in the Texas market, leveraging Veritex’s strong local presence and Huntington’s broader capabilities.

The following slide details how Huntington plans to bring its full franchise capabilities to Texas:

Huntington has also been optimizing its balance sheet through strategic initiatives, including a $0.9 billion corporate bond repositioning and reinvestment of $2.0 billion of securities at a 4.75% yield. The bank has classified 35% of its securities portfolio as held-to-maturity to protect capital.

The bank’s credit quality remains strong, with performance metrics outpacing industry peers:

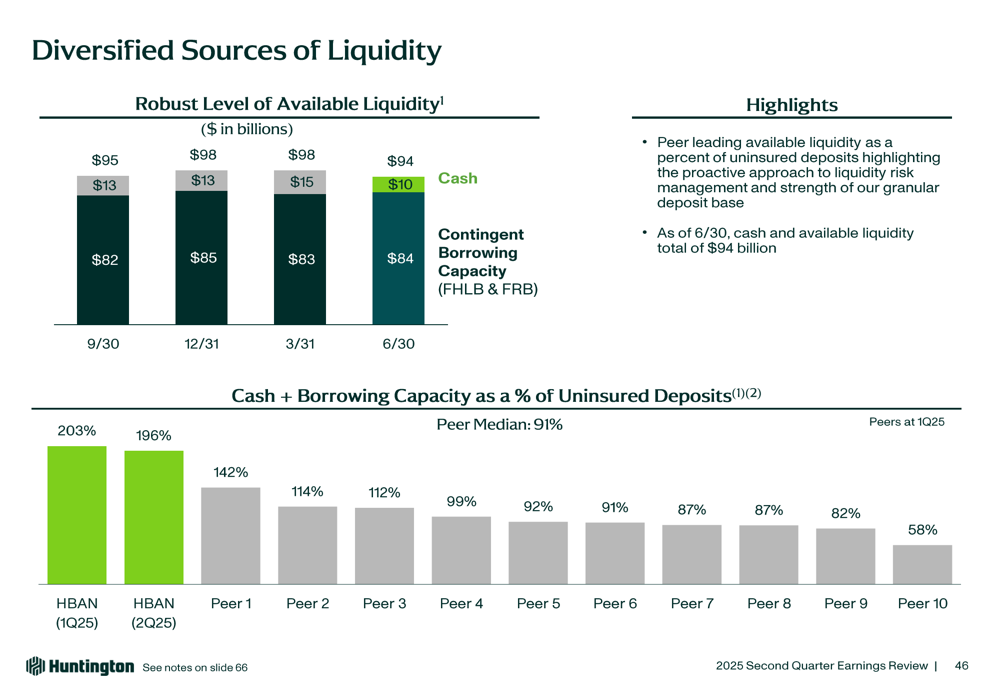

Huntington maintains a solid liquidity position with diversified funding sources, providing robust coverage for uninsured deposits:

Fee Income Growth Strategies

Huntington is focusing on three key areas for fee income growth: payments, wealth management, and capital markets. Payments revenue grew 7% year-over-year, led by commercial payments increasing from $57 million to $67 million. Wealth management fee revenue increased from $90 million to $102 million, supported by growth in assets under management from $31.4 billion to $35.3 billion.

In capital markets, Huntington reported building momentum in its advisory deal backlog and highlighted its recognition as Middle Market M&A Advisor of the Year. These fee-based businesses provide important diversification to the bank’s interest income.

Forward-Looking Statements

Huntington updated its 2025 standalone outlook, raising guidance for both loan and deposit growth. The bank now expects average loan growth of 6-8% (up from 5-7% in April) and average deposit growth of 4-6% (up from 3-5%).

The following slide summarizes the bank’s key strategic highlights for Q2 2025, including growth metrics and strategic initiatives:

For the medium term, Huntington has set ambitious targets including 6-9% pre-provision net revenue compound annual growth rate and a return on tangible common equity goal of 16-17%+ by 2027, while maintaining positive operating leverage.

Conclusion

Huntington’s Q2 2025 presentation demonstrates the bank’s continued strong performance across multiple metrics, with expanding margins, growing fee income, and solid credit quality. The strategic acquisition of Veritex positions Huntington to accelerate its growth in the dynamic Texas market, while the bank’s balance sheet optimization and risk management strategies prepare it for various economic scenarios.

With a CET1 ratio of 9.0% (adjusted) and tangible book value per share growth of 16% year-over-year, Huntington appears well-positioned to continue delivering on its strategic objectives while navigating the evolving economic landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.