60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

HusCompagniet AS (HUSCO) reported its H1 2025 financial results on August 22, 2025, showcasing strong revenue growth despite challenging market conditions. The Danish homebuilder achieved significant sales momentum in a market characterized by relatively stable conditions, despite ongoing geopolitical uncertainties and persistently low consumer confidence.

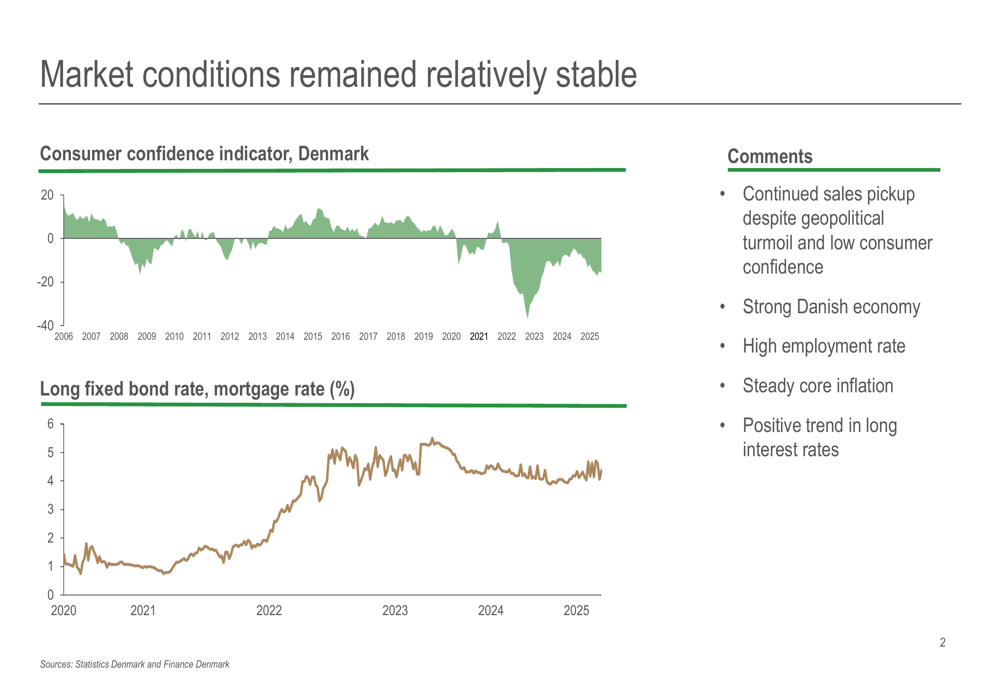

The company highlighted that Denmark's strong economy, high employment rate, and steady core inflation have helped sustain demand for housing, even as mortgage rates have climbed substantially over the past five years.

As shown in the following chart of Denmark's consumer confidence and mortgage rate trends:

Quarterly Performance Highlights

HusCompagniet reported Q2 2025 revenue of DKK 740 million, a substantial 27.8% increase from DKK 579 million in Q2 2024. For the first half of 2025, revenue reached DKK 1,375 million, up 29.5% from DKK 1,062 million in H1 2024. This growth was primarily driven by higher sales in the Detached and B2B segments.

However, profitability metrics showed pressure across the board. Gross profit for Q2 2025 was DKK 136 million with a margin of 18.4%, down from 20.7% in Q2 2024. EBITDA declined to DKK 23 million with a 3.1% margin, compared to DKK 27 million and 4.7% margin in the same period last year. The company cited unsatisfactory margins on certain HC Elements projects, lower Semi-detached contribution, and higher SG&A expenses as factors impacting profitability.

The following slide illustrates the key Q2 2025 financial metrics:

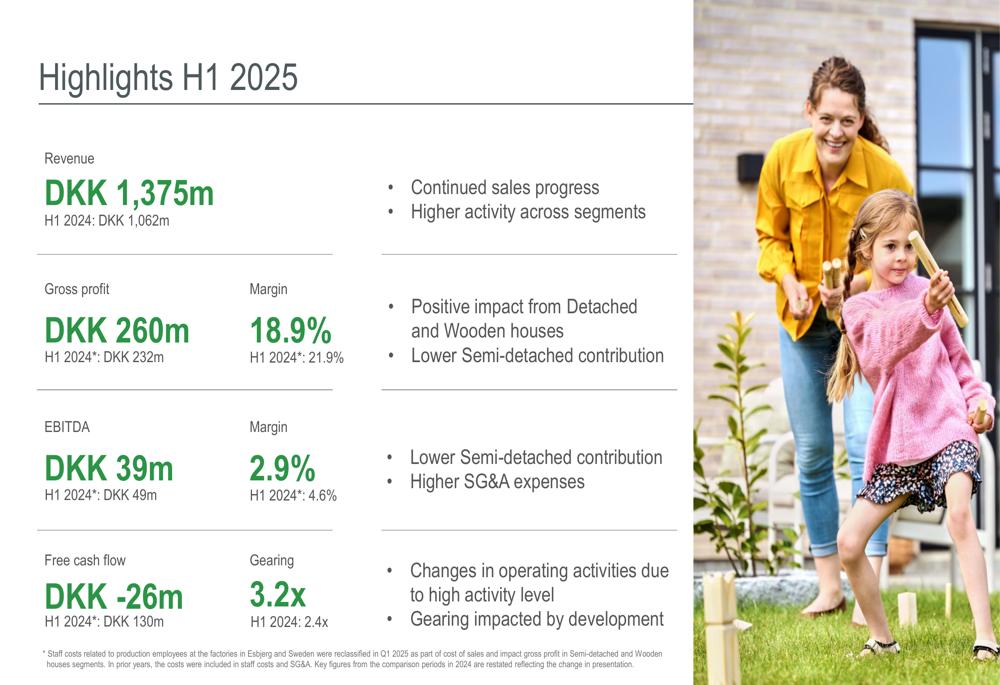

For the first half of 2025, the company reported similar trends with gross profit of DKK 260 million (18.9% margin) and EBITDA of DKK 39 million (2.9% margin), both showing margin compression compared to H1 2024:

Detailed Financial Analysis

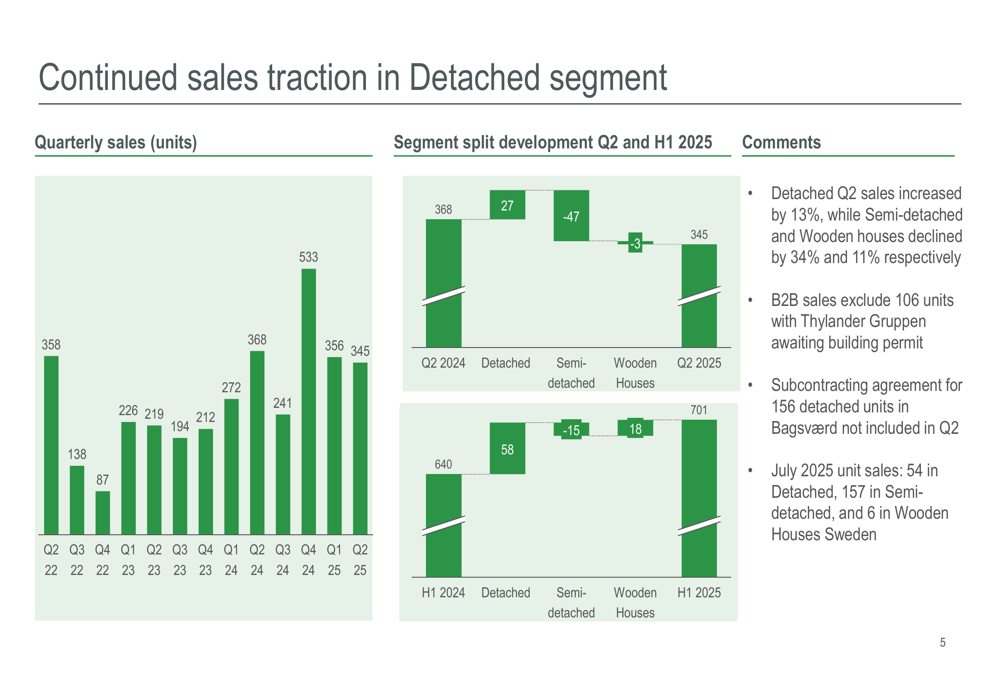

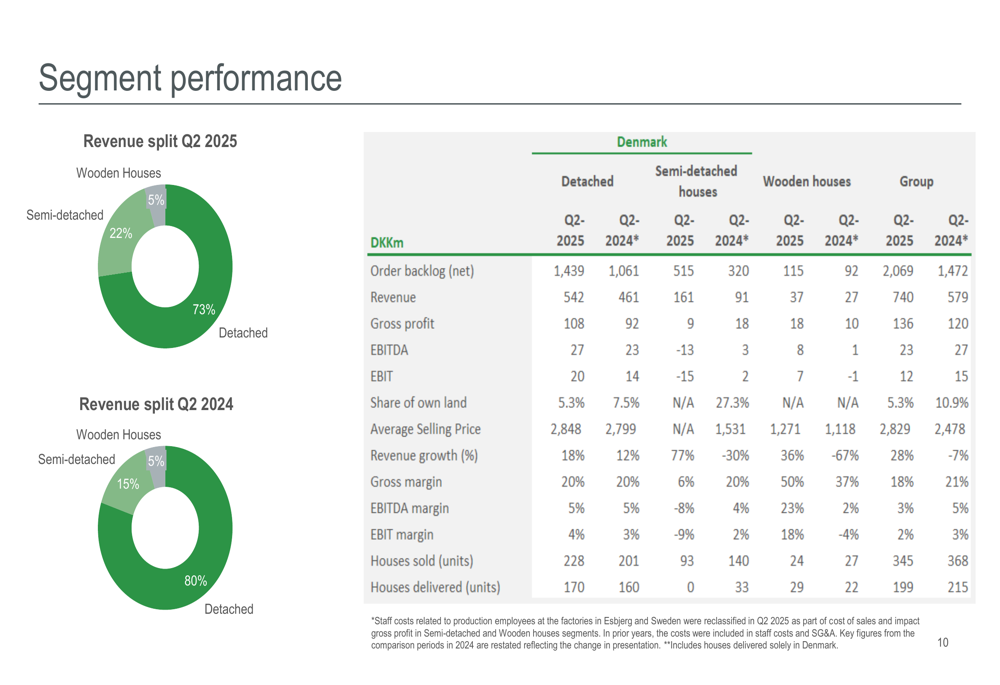

HusCompagniet's segment performance revealed divergent trends. The Detached segment, which now represents 73% of total revenue (up from 80% in Q2 2024), saw sales increase by 13% in Q2 2025. However, Semi-detached and Wooden houses segments experienced sales declines of 34% and 11% respectively.

The company's sales momentum in the Detached segment has been particularly strong, as illustrated in the following chart:

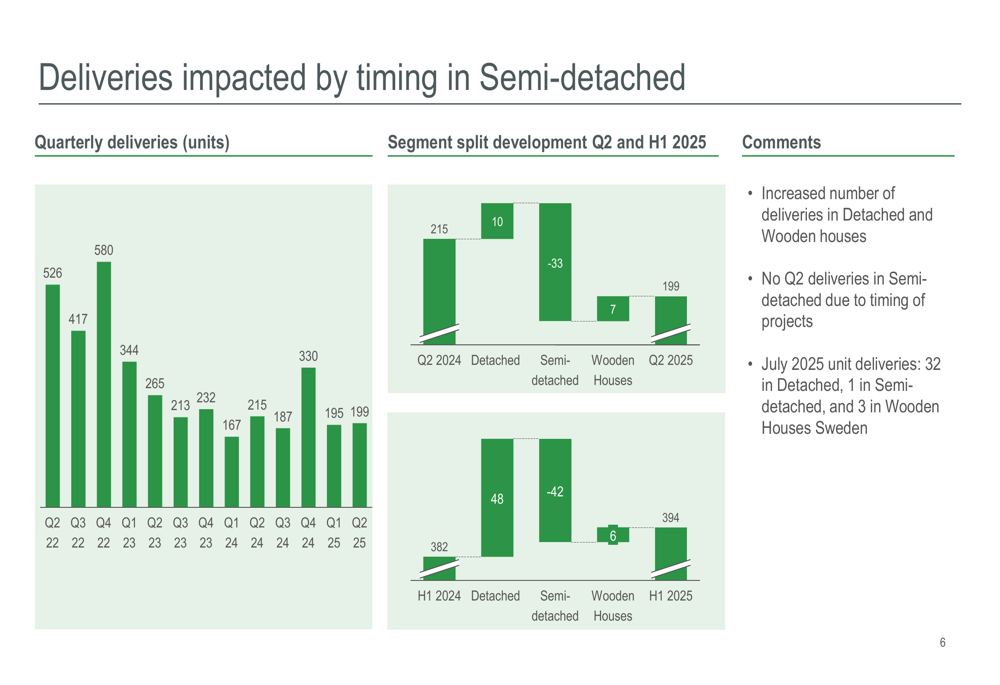

Deliveries were significantly impacted by timing issues in the Semi-detached segment, with no Q2 deliveries reported due to project timing. Overall deliveries fell to 199 units in Q2 2025 from 215 units in Q2 2024, though the Detached segment saw a modest increase:

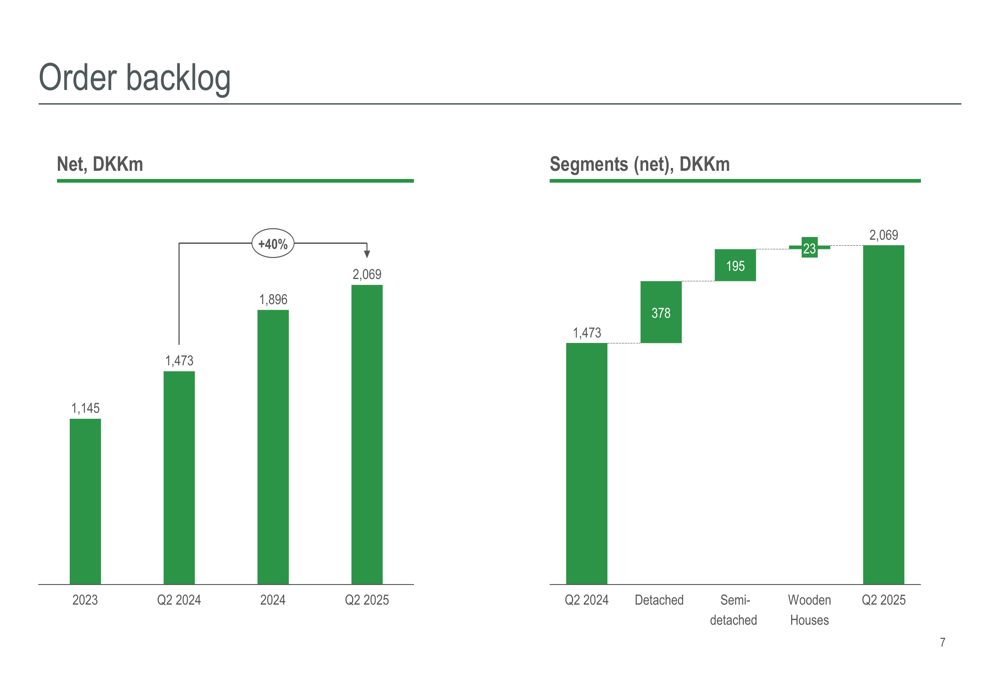

Despite these challenges, HusCompagniet's order backlog grew impressively to DKK 2,069 million in Q2 2025, representing a 40% increase from DKK 1,473 million in Q2 2024. This strong backlog provides visibility for future revenue and suggests continued growth potential:

Free cash flow remained negative at DKK -12 million for Q2 2025 and DKK -26 million for H1 2025, a significant deterioration from the positive DKK 133 million and DKK 130 million reported in the respective periods of 2024. The company attributed this to changes in working capital due to higher activity levels. The gearing ratio increased to 3.2x in H1 2025 from 2.4x in H1 2024, reflecting increased leverage.

The segment performance breakdown provides additional insight into the company's operations:

Forward-Looking Statements

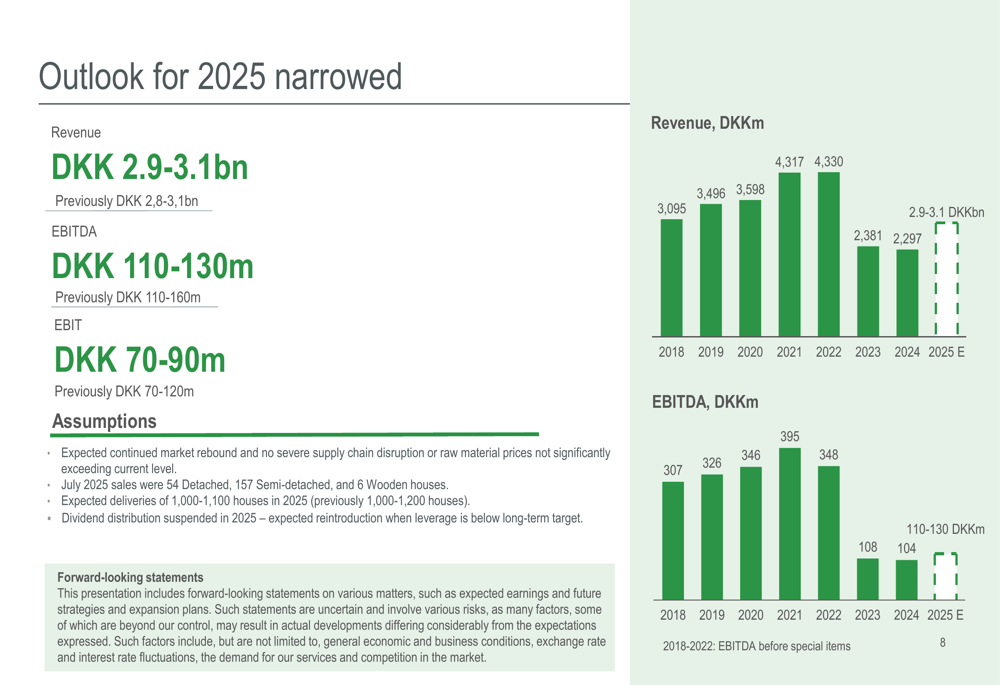

HusCompagniet narrowed its guidance for 2025, maintaining the upper end of its revenue forecast at DKK 3.1 billion while raising the lower end to DKK 2.9 billion (previously DKK 2.8-3.1 billion). However, the company reduced its profitability outlook, with EBITDA now expected to be DKK 110-130 million (previously DKK 110-160 million) and EBIT forecast at DKK 70-90 million (previously DKK 70-120 million).

The company expects to deliver 1,000-1,100 houses in 2025 and has suspended dividend distribution for the year. These projections assume continued market rebound and no severe supply chain disruptions or significant increases in raw material prices.

The following chart illustrates the company's historical performance and revised outlook:

Strategic Initiatives

HusCompagniet's strategic focus appears to be shifting toward the Detached segment and B2B sales, which have shown stronger performance. The company mentioned a subcontracting agreement for 156 detached units in Bagsværd not included in Q2 figures, as well as 106 units with Thylander Gruppen awaiting building permits.

The company's July 2025 sales data showed 54 units in the Detached segment, 157 in Semi-detached, and 6 in Wooden Houses Sweden, indicating potential recovery in the Semi-detached segment. However, deliveries remained concentrated in the Detached segment with 32 units in July 2025.

With HUSCO shares closing at DKK 46.8 on August 21, 2025 (down 0.85% for the day), investors appear cautious about the company's ability to translate its strong revenue growth into improved profitability. The stock is currently trading well below its 52-week high of DKK 68, reflecting concerns about margin pressure and increased leverage despite the impressive sales momentum.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.