Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

Icelandic Salmon AS (OB:ISLAX) presented its first quarter 2025 results on May 20, revealing a challenging period marked by biological issues and reduced harvest volumes. The company, which operates through its subsidiary Arnarlax ehf in Iceland’s Westfjords region, faced headwinds from both operational challenges and difficult market conditions characterized by increased global supply.

As shown in the company’s overview, Icelandic Salmon is listed on both the Euronext (EPA:ENX) Growth market in Oslo and NASDAQ First North in Reykjavik, with all operational activities performed under the Arnarlax brand. The company maintains four smolt facilities with capacity for 25-30 thousand tonnes of harvested volume, with farming operations across eight sites in three fjords.

Quarterly Performance Highlights

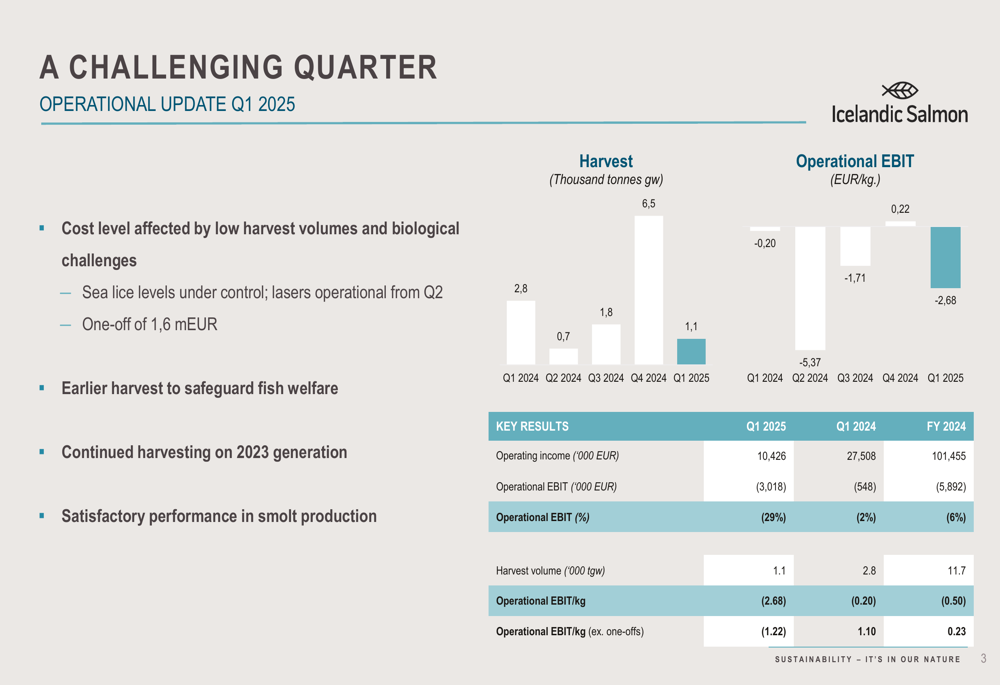

The first quarter of 2025 proved particularly challenging for Icelandic Salmon, with harvest volumes dropping significantly to 1.1 thousand tonnes gutted weight, down from 2.8 thousand tonnes in Q1 2024. This 61% decline in volume contributed to a substantial deterioration in financial performance.

Operating income fell to €10.4 million, compared to €27.5 million in the same period last year. Operational EBIT declined to negative €3.0 million (negative 29% margin), a significant worsening from the negative €548,000 (negative 2% margin) reported in Q1 2024. On a per-kilogram basis, operational EBIT reached negative €2.68, or negative €1.22 excluding one-off costs of €1.6 million.

The company cited several factors affecting performance, including biological challenges related to sea lice (though now reported to be under control), earlier harvesting to safeguard fish welfare, and continued harvesting of the 2023 generation. The presentation highlighted that laser technology to address sea lice issues would be operational from Q2 onward.

As shown in the following chart detailing harvest volumes and operational EBIT performance:

Detailed Financial Analysis

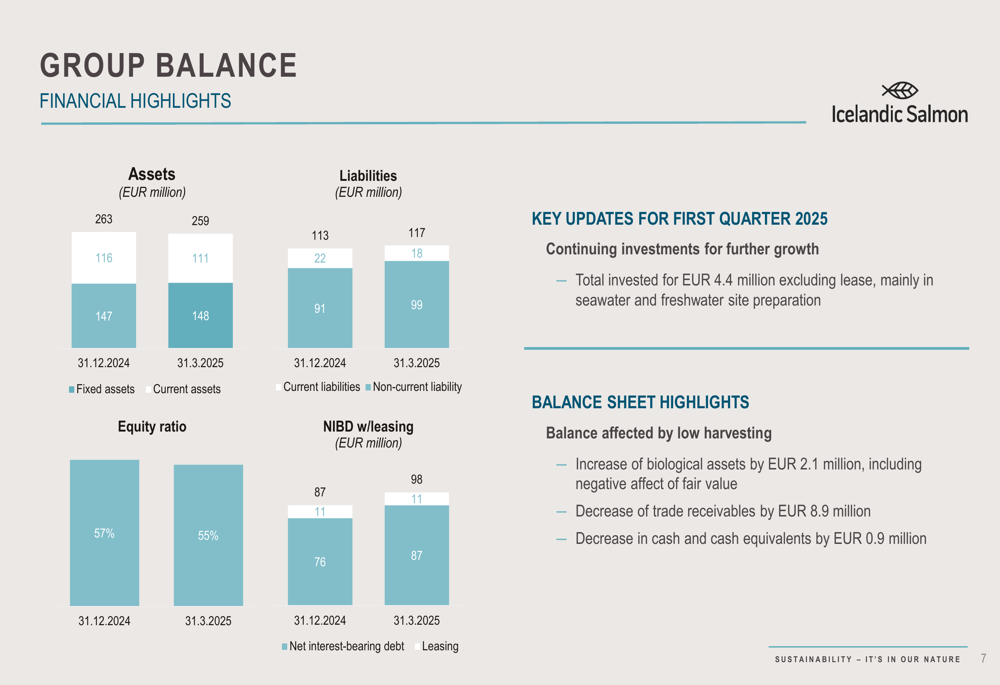

Icelandic Salmon’s balance sheet reflected the challenging quarter, with the equity ratio declining from 57% at year-end 2024 to 55% by March 31, 2025. Total (EPA:TTEF) assets decreased slightly from €263 million to €259 million during the quarter.

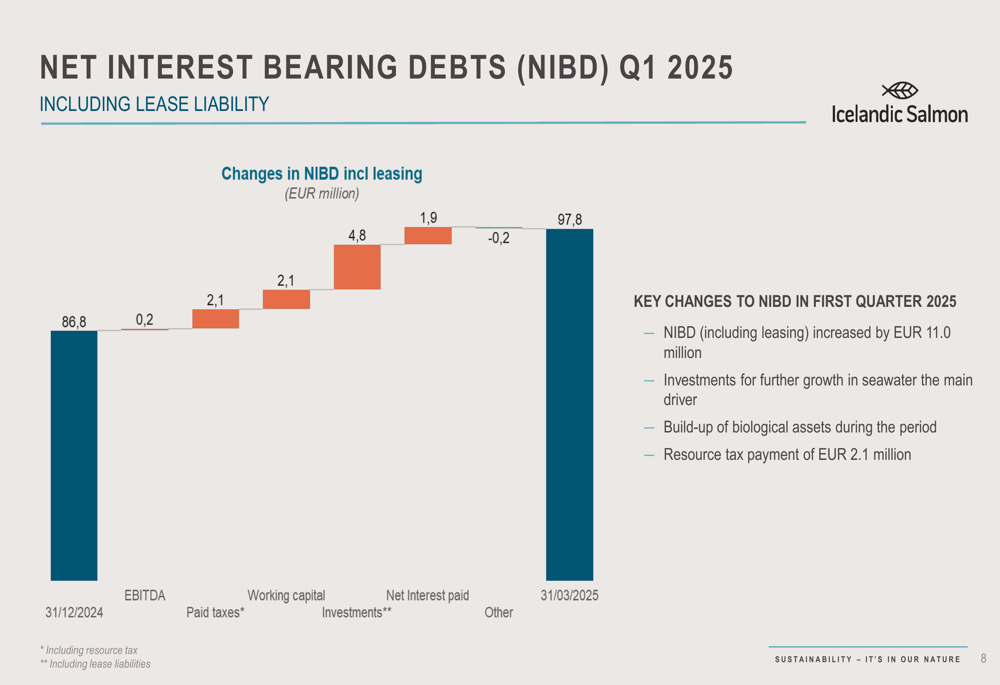

The company’s net interest-bearing debt (NIBD) including leasing increased by €11.0 million during the quarter, reaching €97.8 million by the end of March 2025. This increase was primarily driven by continued investments for growth, particularly in seawater and freshwater site preparation, totaling €4.4 million excluding lease arrangements. Additional factors contributing to the higher debt level included biological asset build-up and a resource tax payment of €2.1 million.

The following financial highlights illustrate the company’s balance sheet position:

The changes in net interest-bearing debt during the quarter are detailed in this chart:

Working capital changes and investments were the primary drivers of increased debt, while the company’s EBITDA contribution was minimal at just €0.2 million for the quarter.

Strategic Initiatives & Outlook

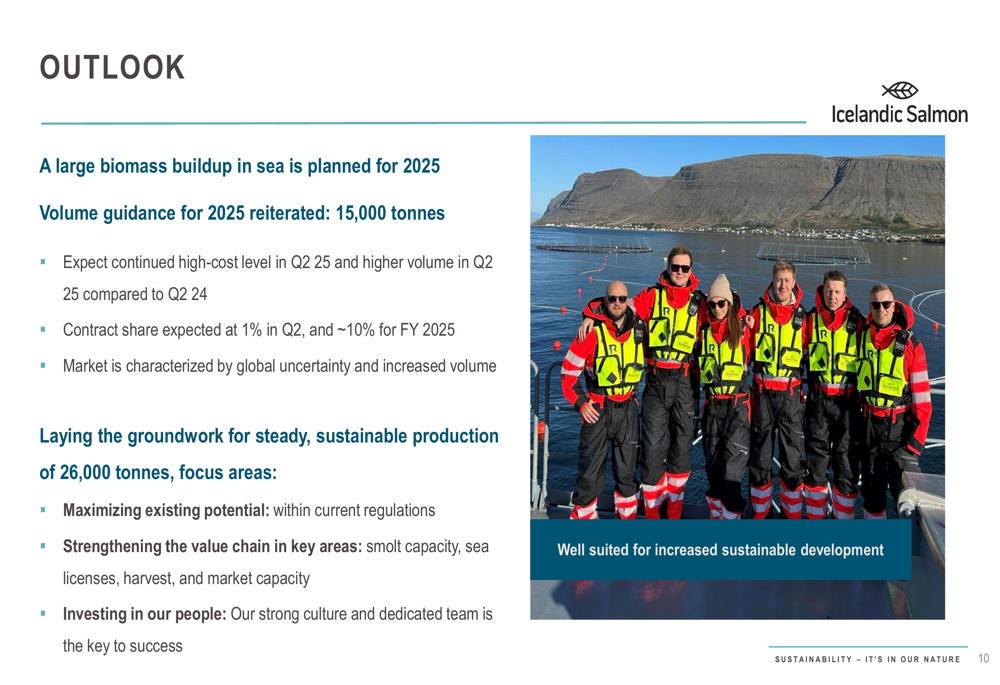

Despite current challenges, Icelandic Salmon maintains its volume guidance of 15,000 tonnes for 2025, representing a significant increase from the 11,700 tonnes harvested in 2024. The company expects continued high cost levels in Q2 2025 but anticipates higher volumes compared to Q2 2024.

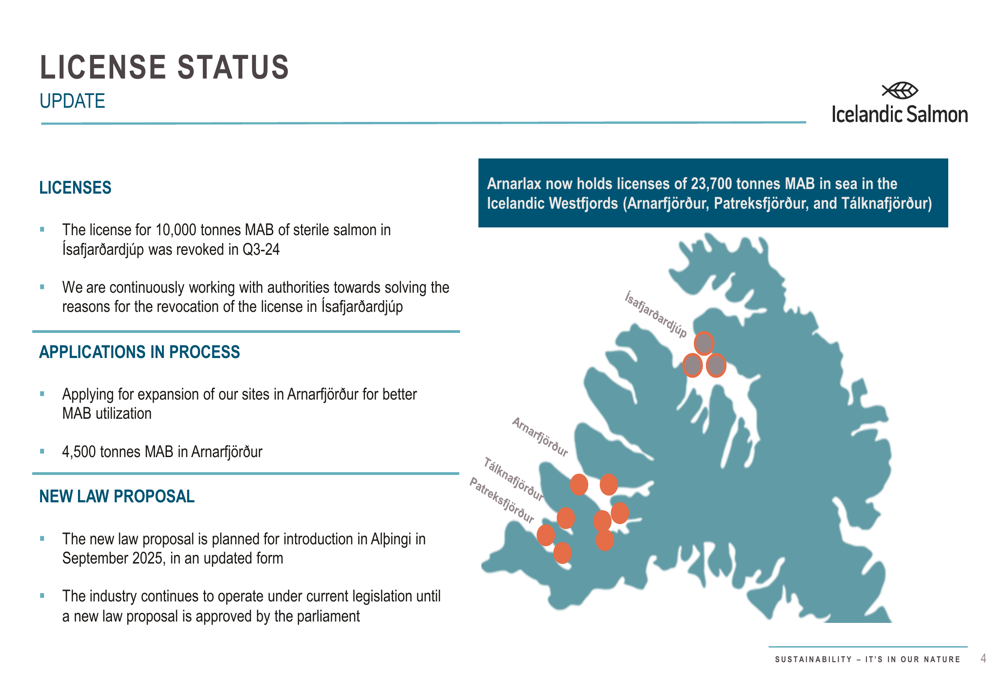

On the regulatory front, Icelandic Salmon currently holds licenses for 23,700 tonnes maximum allowed biomass (MAB) in the Westfjords. However, a license for 10,000 tonnes MAB of sterile salmon in Ísafjarðardjúp was revoked in Q3 2024, and the company is working with authorities to resolve this issue. Additionally, applications are in process for expansion in Arnarfjörður and for 4,500 tonnes MAB in Arnarfjörður.

Looking ahead, Icelandic Salmon is focused on laying the groundwork for steady, sustainable production of 26,000 tonnes. Key strategic priorities include maximizing existing potential within current regulations, strengthening the value chain in areas such as smolt capacity, sea licenses, harvest, and market capacity, and investing in its workforce.

The market outlook remains challenging, with global uncertainty and increased volume characterizing the salmon industry. The company expects a contract share of approximately 1% in Q2 and around 10% for the full year 2025. Regarding specific markets, Icelandic Salmon reports no significant effects from US tariffs thus far, though uncertainties persist. North America represents 9% of the company’s total volume, with 91% transported by boat, while Asia accounts for just 2% of total volume.

The company’s focus on long-term sustainable growth, despite current operational and market challenges, underscores management’s commitment to establishing Icelandic Salmon as a significant player in the premium salmon market. However, investors should note the significant headwinds facing the company in the near term, including biological challenges, regulatory uncertainties, and competitive market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.