Street Calls of the Week

Introduction & Market Context

Icelandic Salmon AS (OB:ISLAX) reported its second quarter 2025 results on August 21, revealing significant operational challenges despite substantially higher harvest volumes. The company’s presentation highlighted how accelerated harvesting due to biological issues, combined with soft market prices, resulted in widening losses for the quarter.

The salmon producer, which operates through its Arnarlax brand in Iceland’s Westfjords region, saw its stock rise 3.06% to 97.00 on the day of the presentation, though shares remain well below their 52-week high of 129.00.

Quarterly Performance Highlights

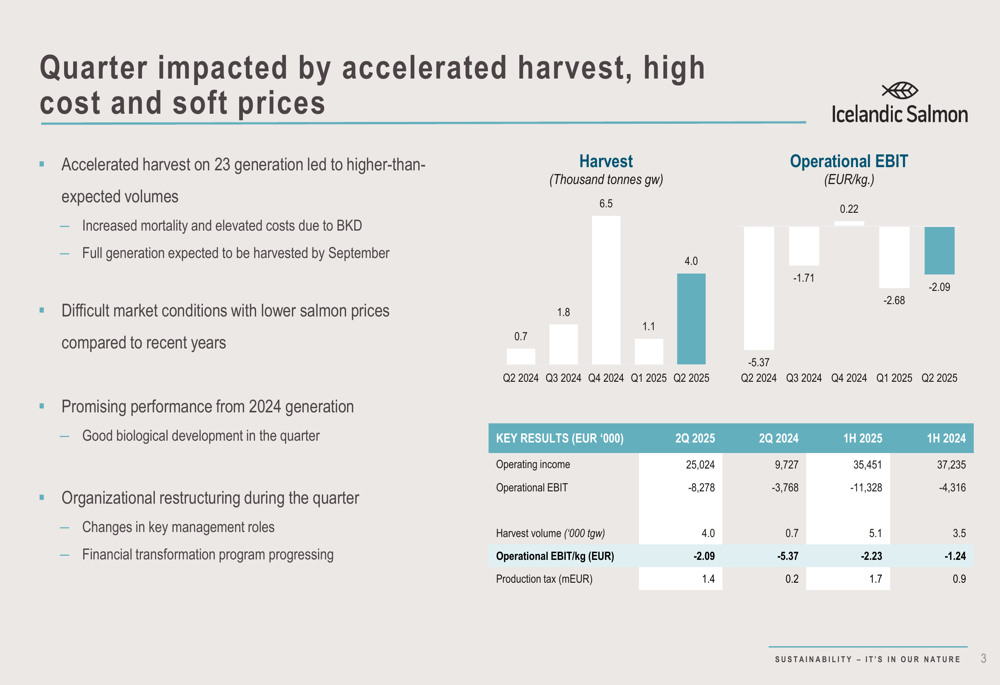

Icelandic Salmon reported operating income of €25.02 million for Q2 2025, a substantial increase from €9.73 million in the same quarter last year. However, this revenue growth was overshadowed by a deteriorating operational EBIT, which fell to -€8.28 million compared to -€3.77 million in Q2 2024.

The company’s harvest volume increased dramatically to 4,000 tonnes in Q2 2025, up from just 700 tonnes in Q2 2024. Despite this volume increase, operational EBIT per kilogram remained negative at -€2.09, though this represented an improvement from -€5.37 in the same period last year.

As shown in the following quarterly performance chart:

Operational Challenges

The accelerated harvest schedule was primarily driven by biological challenges, specifically Bacterial Kidney Disease (BKD) in the 2023 generation salmon. This resulted in increased mortality and elevated costs during the quarter. Management indicated that the full 2023 generation is expected to be harvested by September.

The company’s production facilities include four smolt facilities with capacity for 25-30 thousand tonnes of harvested volume, farming operations across eight sites in three fjords, and a harvesting plant in Bíldudalur with 30,000 tonnes annual capacity. All production is ASC (Aquaculture Stewardship Council) certified.

The company’s operational structure and facilities are illustrated here:

Balance Sheet and Debt Position

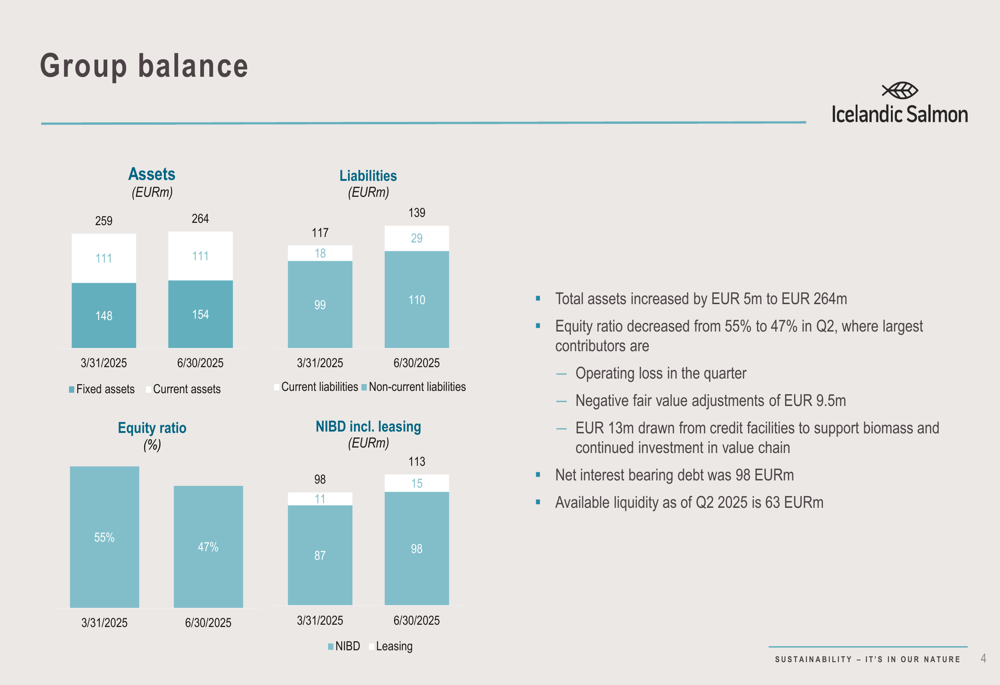

Icelandic Salmon’s financial position showed signs of strain during Q2 2025. Total (EPA:TTEF) assets increased by €5 million to €264 million, while the equity ratio declined from 55% to 47%. This deterioration was primarily attributed to operating losses and negative fair value adjustments of €9.5 million.

The company drew €13 million from credit facilities during the quarter to support biomass growth and continued investment in its value chain. Net interest-bearing debt increased to €98 million, up from €87 million at the end of Q1 2025. Available liquidity stood at €63 million as of June 30, 2025.

The balance sheet comparison is illustrated in the following chart:

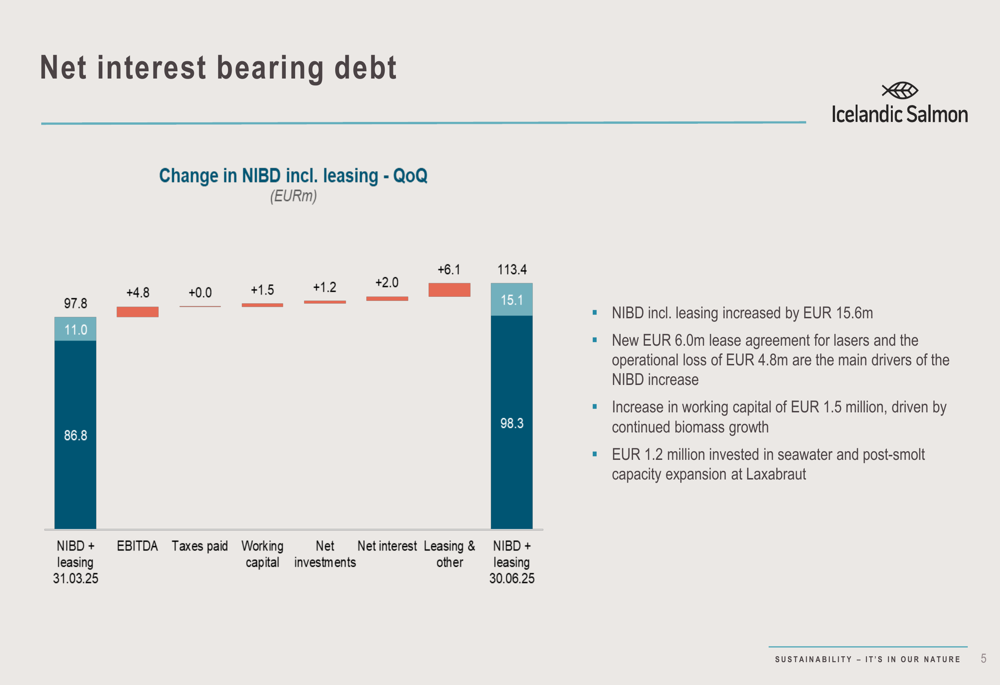

The increase in net interest-bearing debt was further detailed in a waterfall chart showing the main contributors to the €15.6 million increase:

Market Conditions

Icelandic Salmon reported challenging market conditions characterized by higher global supply putting downward pressure on salmon prices. The first-half price for SISALMON 3-6kg was €2.55/kg lower than the same period last year, significantly impacting profitability.

The company’s contract share for Q2 was minimal at less than 1%. Regarding geographic distribution, 12% of Q2 volume was sold to North America and 9% to Asia. The company noted uncertainty regarding the impact of the 15% tariff rate on the US market, though no obvious effects have been observed so far.

License Status and Regulatory Environment

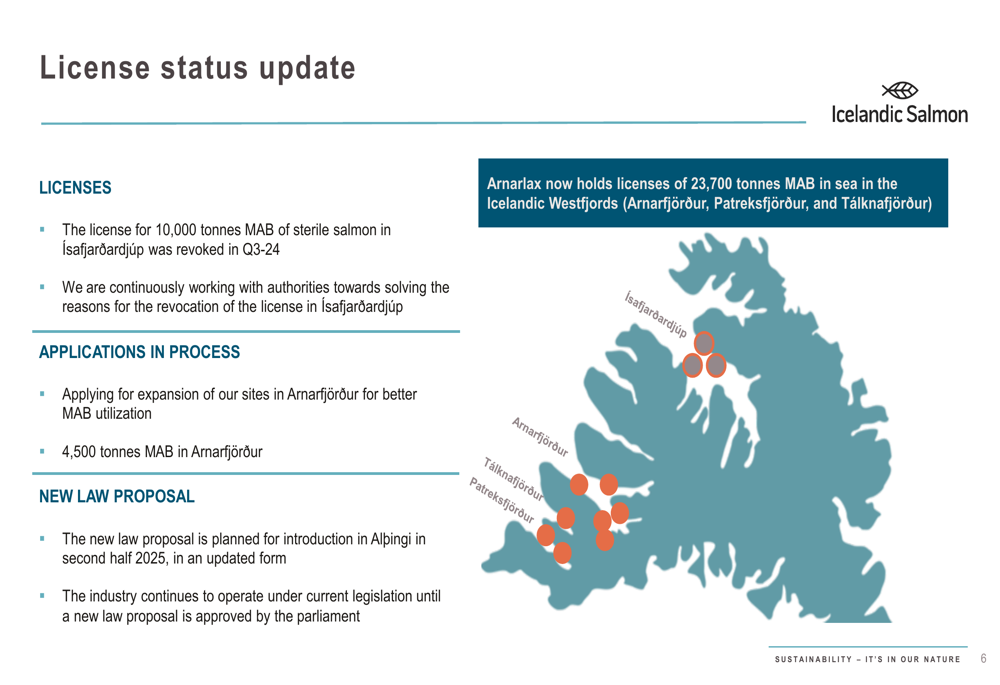

Icelandic Salmon currently holds licenses for 23,700 tonnes Maximum Allowable Biomass (MAB) across three fjords in the Icelandic Westfjords. The company noted that a license for 10,000 tonnes MAB of sterile salmon in Ísafjarðardjúp was revoked in Q3 2024, and they are working with authorities to resolve these issues.

The company is applying for expansion of sites in Arnarfjörður for better MAB utilization and an additional 4,500 tonnes MAB. A new law proposal is planned for introduction in the Icelandic parliament (Alþingi) in the second half of 2025.

The license status is illustrated in this map:

Forward-Looking Statements

In a significant revision to previous guidance, Icelandic Salmon lowered its 2025 volume forecast from 15,000 tonnes to 13,000 tonnes, citing higher mortality and the accelerated harvesting of the 2023 generation. This represents a change from the Q1 2025 earnings call, when the company had maintained its 15,000 tonnes guidance.

The outlook for Q3 2025 indicates continued high cost levels due to remaining harvest from the 2023 generation, with the first harvest of the 2024 generation expected in October. The company anticipates biomass building to continue, with year-end levels expected to be considerably higher than last year.

Contract share is projected to remain low at approximately 1% in Q3 and around 5% for the full year 2025. The company acknowledged ongoing uncertainty in the salmon market due to increased global supply pressure and potential implications of tariffs on US exports.

Conclusion

Icelandic Salmon’s Q2 2025 presentation revealed a company navigating significant operational and market challenges. While harvest volumes increased substantially year-over-year, biological issues, soft market prices, and rising costs combined to widen operational losses. The reduction in full-year volume guidance and deteriorating financial metrics suggest continued headwinds for the remainder of 2025.

Investors will be watching closely to see if the company’s organizational restructuring and financial transformation program, mentioned briefly in the presentation, can help address these challenges and return the operation to profitability in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.