Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

International Container Terminal Services Inc. (ICT) delivered a strong financial performance in the second quarter of 2025, as revealed in its investor presentation on August 5, 2025. The global port operator reported growth across all key metrics, with consolidated volume and revenues increasing in all regions. The company’s stock closed at 455 prior to the presentation, up 1.1% for the day, and has traded between 311 and 473.6 over the past 52 weeks.

Quarterly Performance Highlights

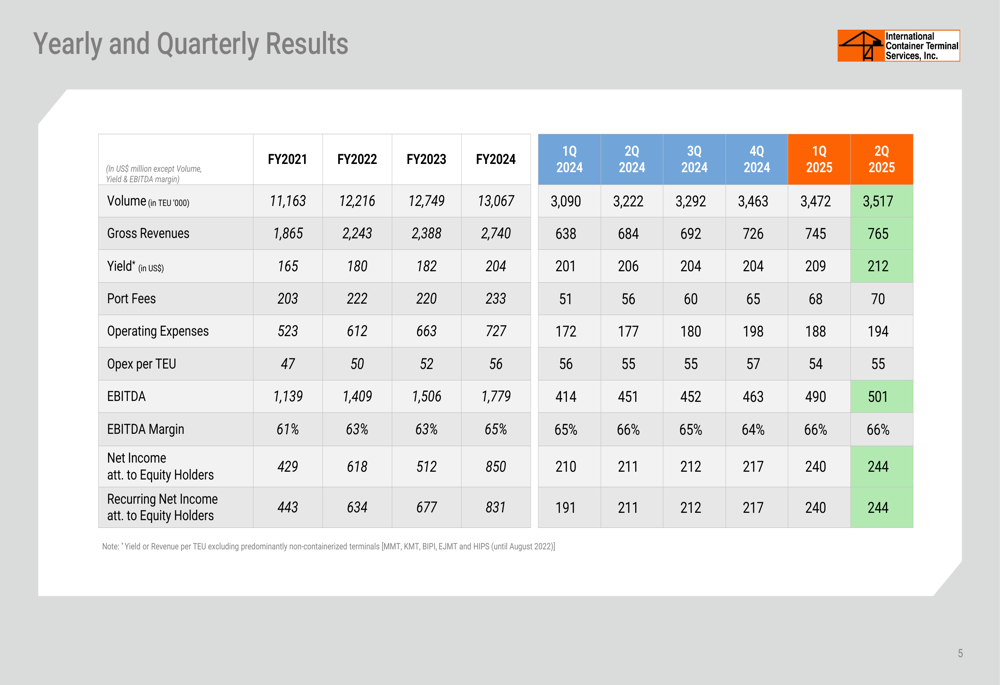

ICTSI reported impressive growth in Q2 2025, with volume increasing by 9%, yield by 3%, and revenue by 12% compared to the same period last year. EBITDA grew by 11% with a robust margin of 66%, while net income and diluted EPS both increased by 16%.

As shown in the following comprehensive financial results table:

For the first half of 2025, the company’s performance was even stronger, with volume up 11%, yield up 3%, and revenue increasing by 14% compared to 1H 2024. EBITDA grew by 15% with the same 66% margin, while net income and diluted EPS rose by 15%. Notably, recurring net income showed an impressive 20% growth.

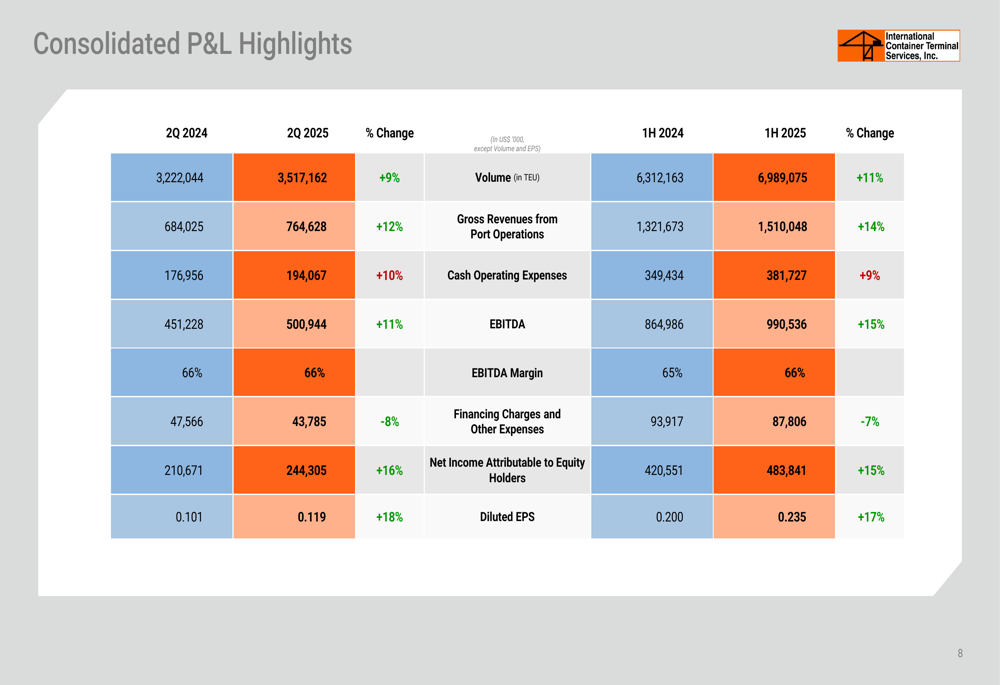

The detailed profit and loss statement highlights the consistent growth across key metrics:

The company’s recurring net income, which excludes one-time events, reached $483.8 million for the first half of 2025, representing a 20% increase from the $401.7 million reported in the same period of 2024. This figure excludes non-recurring items such as income from legal settlements that affected the previous year’s results.

Regional Performance Analysis

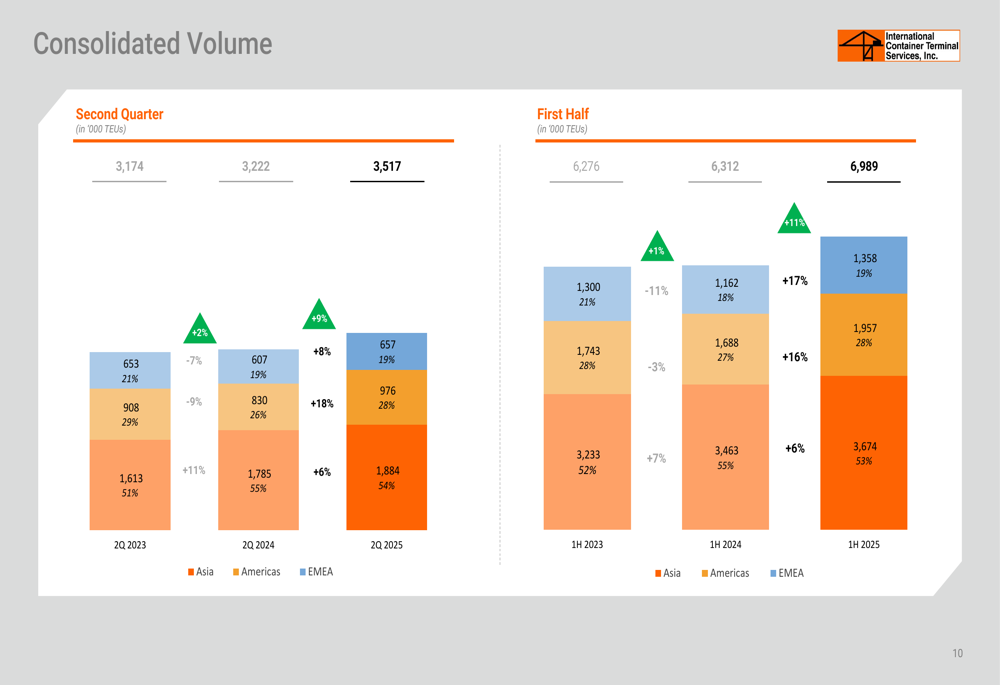

ICTSI’s global diversification strategy continues to pay dividends, with volume growth across all regions. The company’s operations are divided into three geographic segments: Asia, Americas, and EMEA (Europe, Middle East, and Africa).

The consolidated volume by region shows particularly strong growth in EMEA:

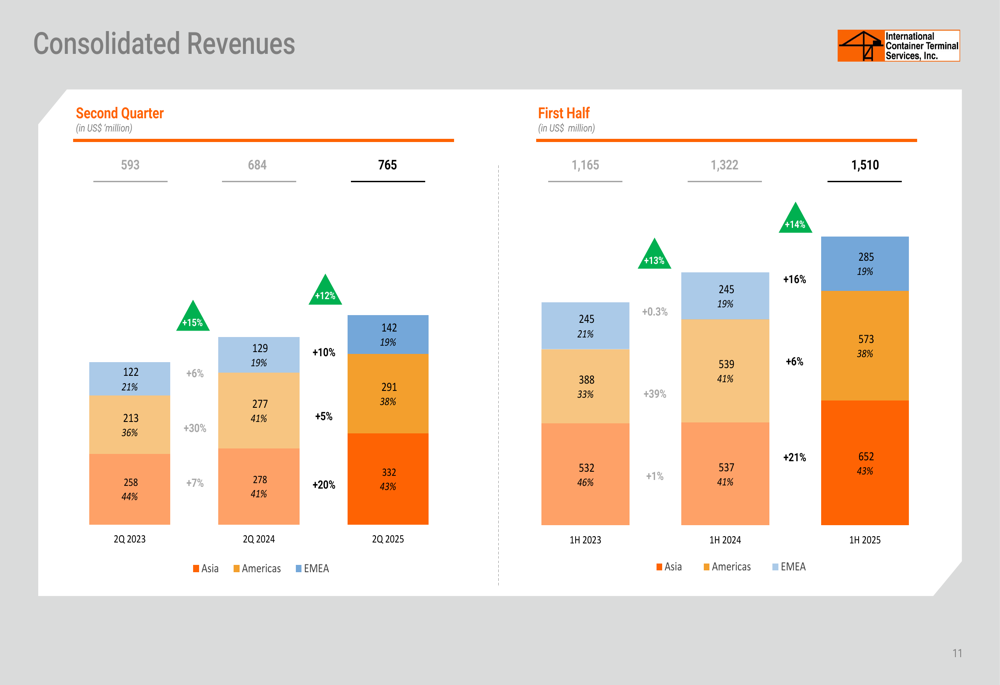

In terms of revenue, the Americas region led the way with a 20% increase in Q2 2025 compared to Q2 2024, generating $332 million. The EMEA region saw a 10% increase to $176 million, while Asia grew by 7% to $258 million. This regional diversification provides stability across various trade scenarios, as highlighted in the company’s presentation.

The revenue breakdown by region illustrates this balanced growth:

Strategic Expansion Initiatives

ICTSI continues to expand its global footprint with strategic acquisitions. The company has acquired a 73% interest in Inhaúma Fundo de Investimento Imobillario - FII in Rio de Janeiro, Brazil, which holds perpetual rights to a 32-hectare marine property adjacent to ICTSI’s Rio Brazil terminal. The company plans to develop a future Private Use Terminal (TUP) at this site.

In Indonesia, ICTSI has entered into a 75/25 joint venture with PT Interport Sarana Infrastruktur Indonesia for the operation and development of Batu Ampar Container Terminal (BACT) in Batam. This terminal is strategically located along the Malacca Strait and serves as the main container terminal for Batam Island, a special economic zone with significant investment potential and current volume estimated at over 600,000 TEUs.

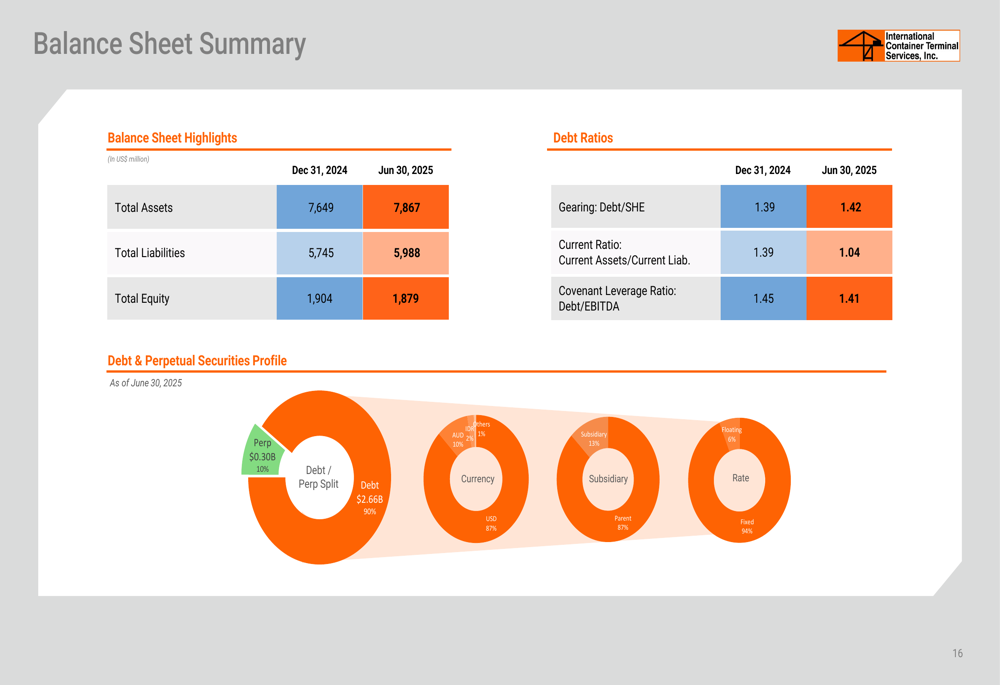

Balance Sheet and Capital Resources

ICTSI maintains a healthy balance sheet with total assets of $7.87 billion as of June 30, 2025, up from $7.65 billion at the end of 2024. The company’s debt profile has improved, with the covenant leverage ratio (Debt/EBITDA) decreasing from 1.45 to 1.41.

The balance sheet summary provides a clear picture of the company’s financial position:

Capital expenditure for the first half of 2025 totaled $393 million, with $232 million (59%) allocated to expansionary projects and $161 million (41%) to maintenance. The company’s 2025 CAPEX budget stands at $580 million, with major expansions planned at several terminals including MICT, CMSA, IDRC, AGCT, BCT, Batangas terminal, ICTSI Rio, MNHPI, VICT, and MICTSI.

Financing charges decreased by 9% in the first half of 2025 compared to the same period in 2024, reflecting improved debt management. The average cost of financing (post-CIT) decreased slightly from 4.7% in 1H 2024 to 4.6% in 1H 2025.

Forward-Looking Statements

ICTSI’s management highlighted several factors that will drive future growth. The company’s globally diversified portfolio of origin and destination ports provides stability across various trade scenarios. Yield improvement initiatives are expected to further enhance revenue growth, while the focus on operating leverage continues to boost earnings growth.

The company summarized its strategic positioning with these key points:

With a healthy balance sheet, superior cash generation, and tactical use of capital, ICTSI is well-positioned to unlock future growth opportunities in the global port operations sector. The company’s consistent performance across all regions demonstrates the effectiveness of its diversification strategy and operational excellence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.