S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

IDT Corporation (NYSE:IDT) released its third quarter fiscal 2025 investor presentation, highlighting continued momentum across its high-growth business segments. The company, which has transformed from a traditional telecommunications provider into a diversified SaaS and fintech enterprise, reported significant margin expansion and profitability improvements. With a current stock price of $67.78, down slightly by 0.31% in the most recent trading session, IDT continues to trade near its 52-week high of $69.67, reflecting strong investor confidence in its strategic direction.

Executive Summary

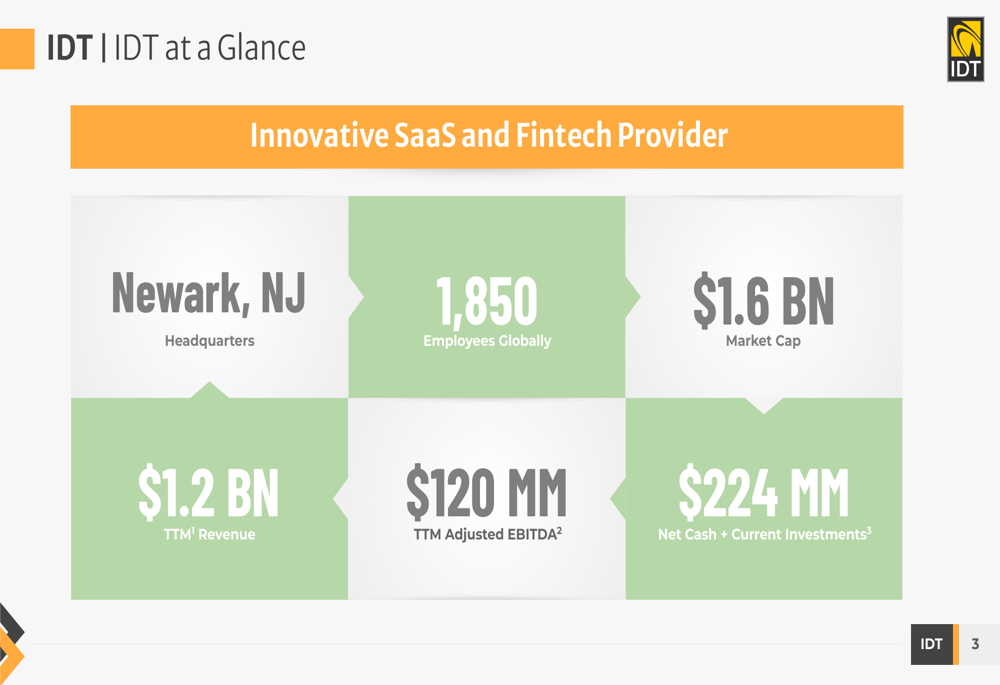

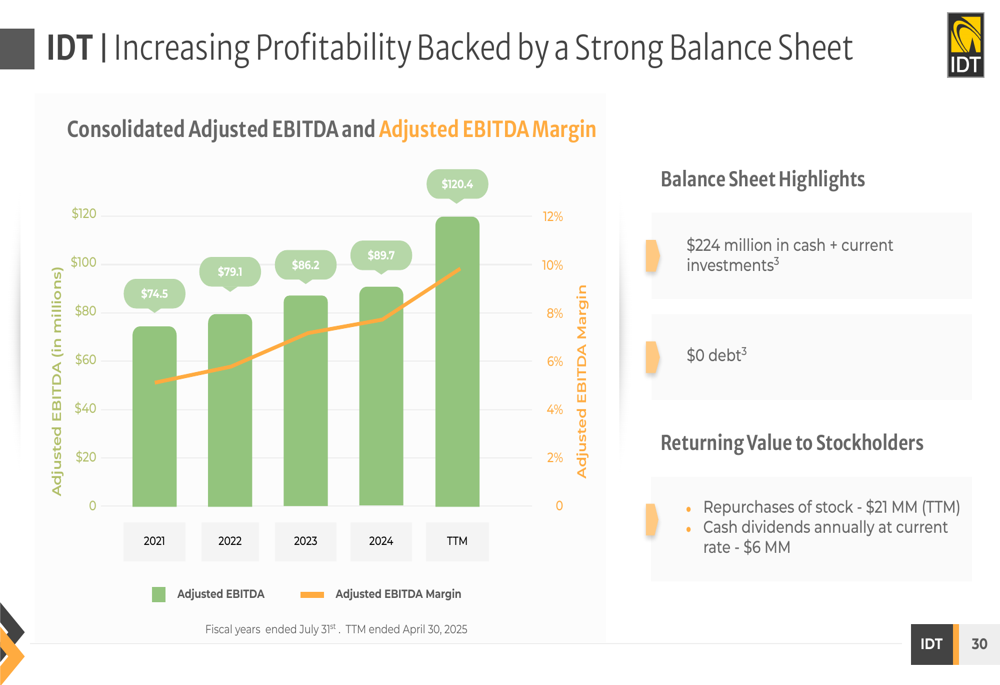

IDT’s Q3 2025 presentation emphasized the company’s successful pivot toward high-margin, high-growth business segments while maintaining its traditional communications operations as a stable cash generator. With a market capitalization of $1.6 billion, trailing twelve-month (TTM) revenue of $1.2 billion, and TTM adjusted EBITDA of $120 million, IDT has established itself as a significant player in multiple technology sectors. The company maintains a strong balance sheet with $224 million in cash and current investments with zero debt, enabling continued investment in growth initiatives and shareholder returns.

As shown in the following overview of IDT’s business profile:

Quarterly Performance Highlights

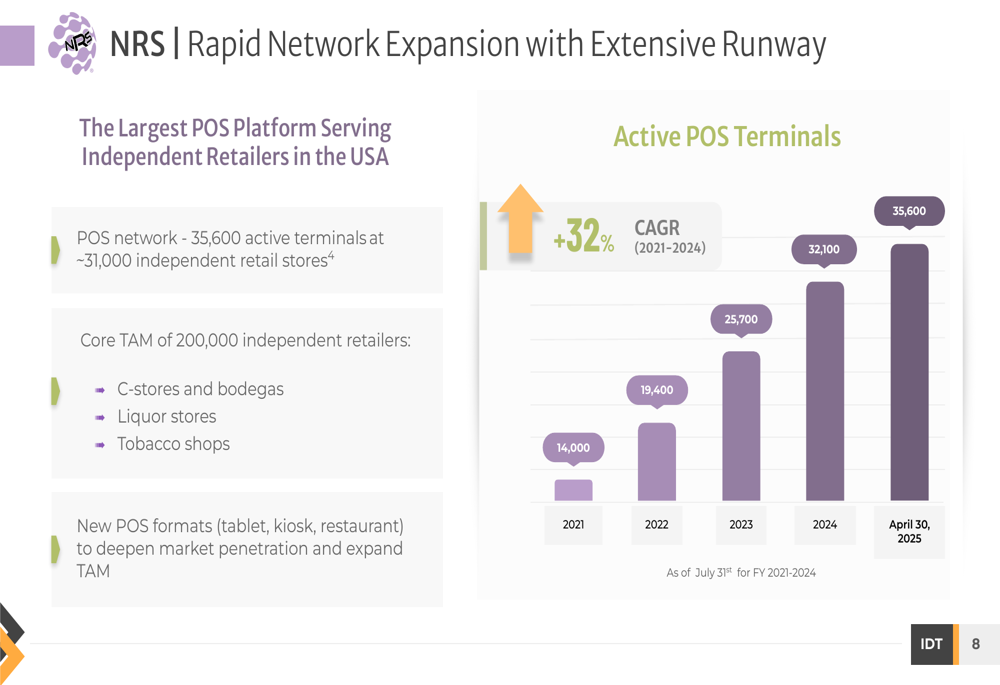

IDT’s National Retail (NYSE:NNN) Solutions (NRS) segment continued its impressive growth trajectory, expanding its network to 35,600 active terminals at approximately 31,000 independent retail stores as of April 30, 2025. This represents significant progress toward the company’s estimated total addressable market of 200,000 independent retailers in the United States. NRS generated $118 million in annual recurring revenue (ARR), with an adjusted EBITDA margin of 23.1% in Q3 2025, up from 21.8% in the same period last year.

The company’s presentation highlighted how NRS has built the largest point-of-sale platform serving independent retailers in the United States, with substantial runway for continued expansion:

NRS’s revenue model has diversified across multiple recurring streams, creating a resilient business with high margins. The platform generates revenue through merchant services (67% of recurring revenue), advertising and data (20%), and SaaS fees (13%). Average monthly recurring revenue per terminal increased to $279 in Q3 2025 from $271 in Q3 2024.

The following chart illustrates how NRS has built multiple revenue streams from a single platform:

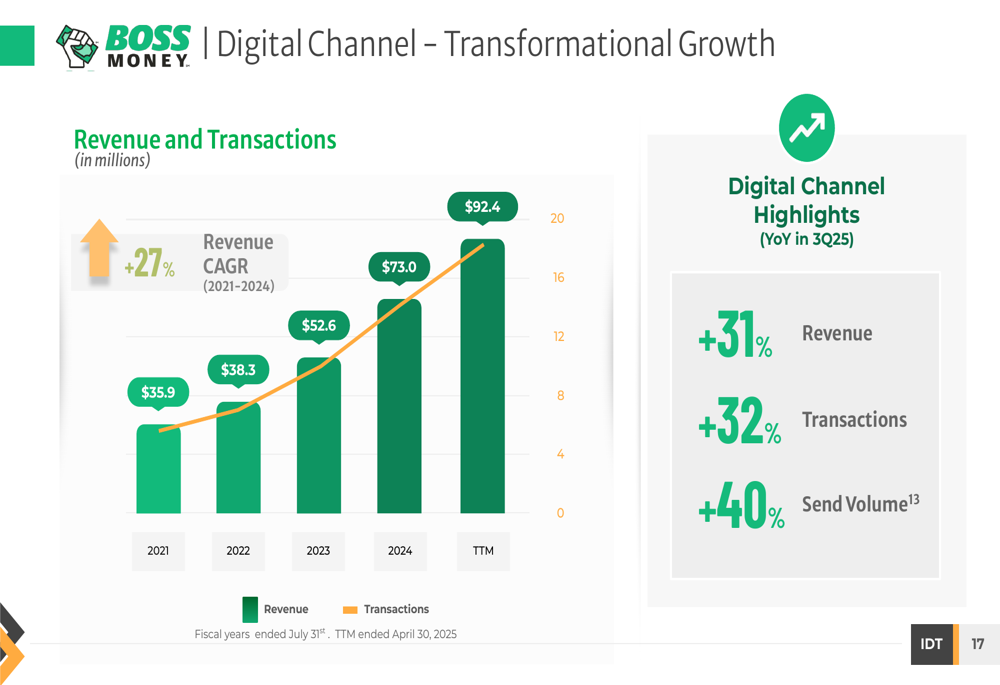

In the Fintech segment, BOSS Money’s digital channel demonstrated exceptional growth with a 31% year-over-year revenue increase in Q3 2025, accompanied by a 32% increase in transactions and a 40% increase in send volume. The digital-first strategy has transformed this business, with the segment’s adjusted EBITDA margin expanding dramatically to 13.0% in Q3 2025 from just 1.0% in Q3 2024.

The following graph demonstrates the transformational growth in BOSS Money’s digital channel:

The net2phone segment, which provides cloud communications solutions, reported 415,000 seats served as of April 30, 2025, and achieved an 11% annual subscription revenue increase on a constant currency basis. The segment’s adjusted EBITDA margin improved to 15% in Q3 2025 from 10% in Q3 2024, reflecting improved operational efficiency and scale benefits.

Detailed Financial Analysis

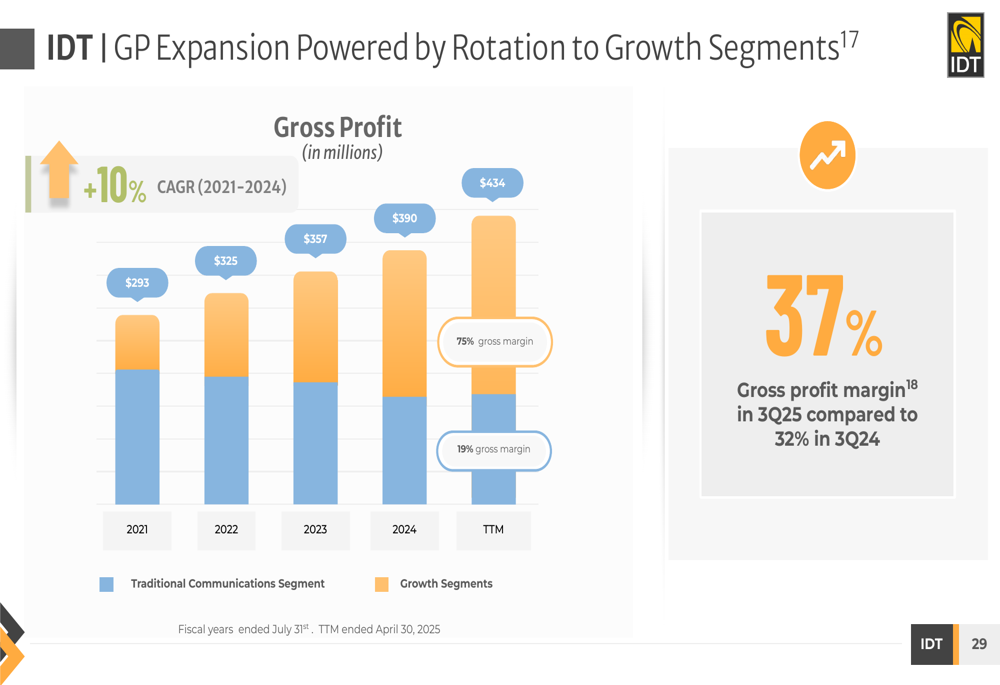

IDT’s consolidated gross profit has shown consistent growth with a 10% CAGR from 2021 to 2024, reaching $434 million TTM. This expansion has been driven by the company’s strategic shift toward higher-margin growth segments, which now contribute a significantly larger portion of the overall gross profit despite generating lower revenue than the traditional communications segment.

The presentation highlighted how this rotation toward growth segments has powered gross profit expansion:

Consolidated adjusted EBITDA reached $120.4 million TTM, reflecting the company’s improved operational efficiency and focus on high-margin businesses. The traditional communications segment, while experiencing gradual revenue decline, continues to generate substantial cash flow with $73.7 million in TTM adjusted EBITDA and an improved margin of 9.2% in Q3 2025 compared to 6.7% in Q3 2024.

The following chart illustrates IDT’s increasing profitability and strong balance sheet position:

These financial results align with the trajectory reported in IDT’s Q2 2025 earnings, which showed a 133% year-over-year increase in income from operations and a 290% surge in EPS. The company’s gross profit margin reached a record high of 37.1% in that quarter, consistent with the margin expansion trend highlighted in the Q3 presentation.

Strategic Initiatives

IDT’s presentation emphasized its focus on underserved markets across all business segments. The company has structured its operations into synergistic businesses that target specific market opportunities:

For NRS, the strategic focus remains on expanding its POS network while increasing revenue per terminal through additional services. The business has achieved a "Rule of 40" metric of 49%, indicating a healthy balance between growth and profitability.

BOSS Money continues to leverage its digital-first platform strategy, which has resulted in superior user experience with a 4.8/5 star rating and over 90% repeat customers. The digital channel now represents a significant and growing portion of the overall remittance business.

net2phone has differentiated itself through a focus on mid-market businesses, channel partner relationships, and a distinctive geographic strategy with deeply localized offerings primarily in the Americas. This approach has enabled steady growth in subscription revenue with a 26% CAGR from 2021 to 2024.

Forward-Looking Statements

IDT’s presentation suggests continued momentum across its growth segments, with particular emphasis on scaling the NRS network, expanding BOSS Money’s digital channel, and growing net2phone’s subscription base. The company’s strong balance sheet position with $224 million in cash and investments provides flexibility for both organic growth initiatives and potential acquisitions.

Based on the Q2 2025 earnings call, IDT appears to be on track to meet its full-year adjusted EBITDA target of $126 million. Management has indicated interest in exploring M&A opportunities while maintaining financial discipline, noting they "will not take on debt like some other companies do to buy back shares."

The company continues to return value to shareholders through stock repurchases ($21 million TTM) and cash dividends (current annual rate of $6 million). With all business segments showing margin expansion and the high-growth portions of the business gaining increasing prominence, IDT appears well-positioned to continue its successful transformation from a traditional telecom provider to a diversified technology company with multiple growth vectors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.