How are energy investors positioned?

America’s largest audio company, iHeartMedia Inc. (NASDAQ:IHRT), released its second quarter 2025 results on August 11, showing continued strength in its digital audio business while traditional radio segments faced headwinds. The company reported modest overall revenue growth and improved profitability despite mixed segment performance.

Executive Summary

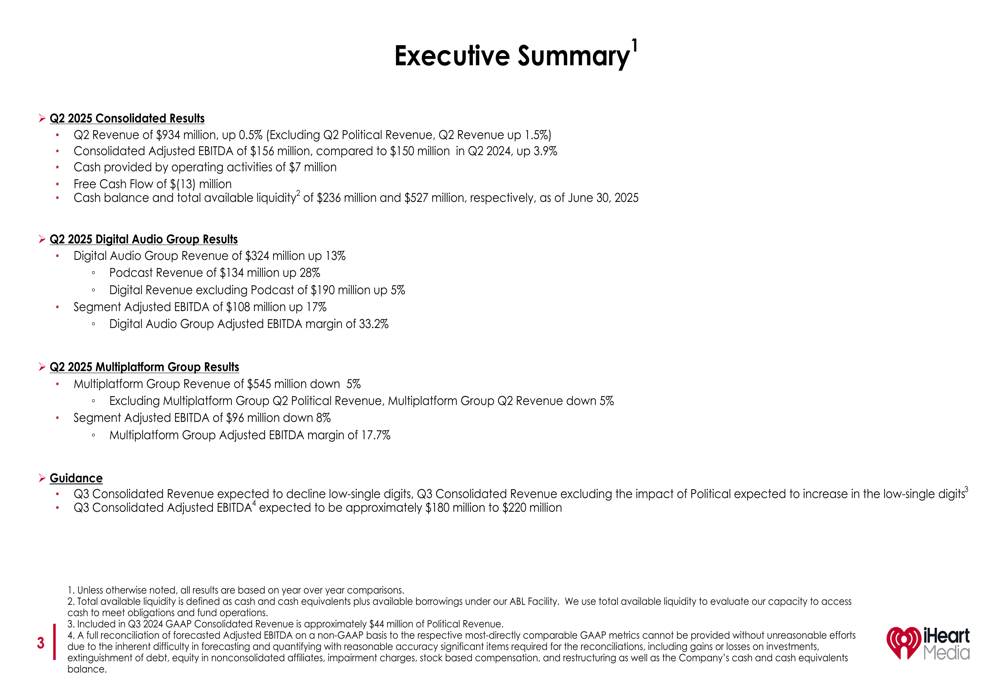

iHeartMedia posted Q2 2025 revenue of $934 million, up 0.5% year-over-year, or 1.5% when excluding political revenue. Consolidated adjusted EBITDA reached $156 million, representing a 3.9% increase compared to the $150 million reported in Q2 2024. The company’s cash balance stood at $236 million with total available liquidity of $527 million as of June 30, 2025.

As shown in the following summary of quarterly results:

The company’s performance was characterized by a stark contrast between its digital and traditional segments. The Digital Audio Group saw revenue increase by 13% to $324 million, driven by a remarkable 28% growth in podcast revenue, which reached $134 million. Meanwhile, the Multiplatform Group, which includes traditional radio operations, experienced a 5% revenue decline to $545 million.

Digital Audio & Podcast Growth

iHeartMedia’s digital transformation continues to gain momentum, with the Digital Audio Group now representing approximately 35% of total revenue. Podcast revenue growth was particularly impressive at 28% year-over-year, reaching $134 million for the quarter. The segment’s adjusted EBITDA grew 17% with margins expanding to 33.2%.

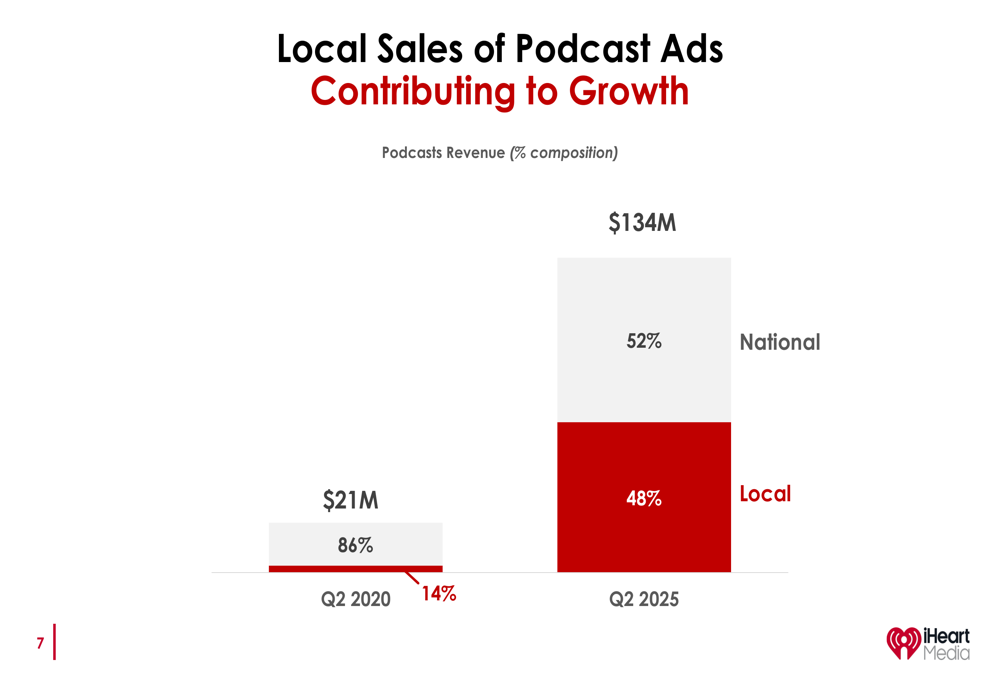

A notable shift in the podcast business has been the increasing contribution from local sales:

Local sales of podcast ads have grown from just 14% of total podcast revenue in Q2 2020 to 48% in Q2 2025, indicating successful penetration into local advertising markets that have traditionally been the stronghold of broadcast radio.

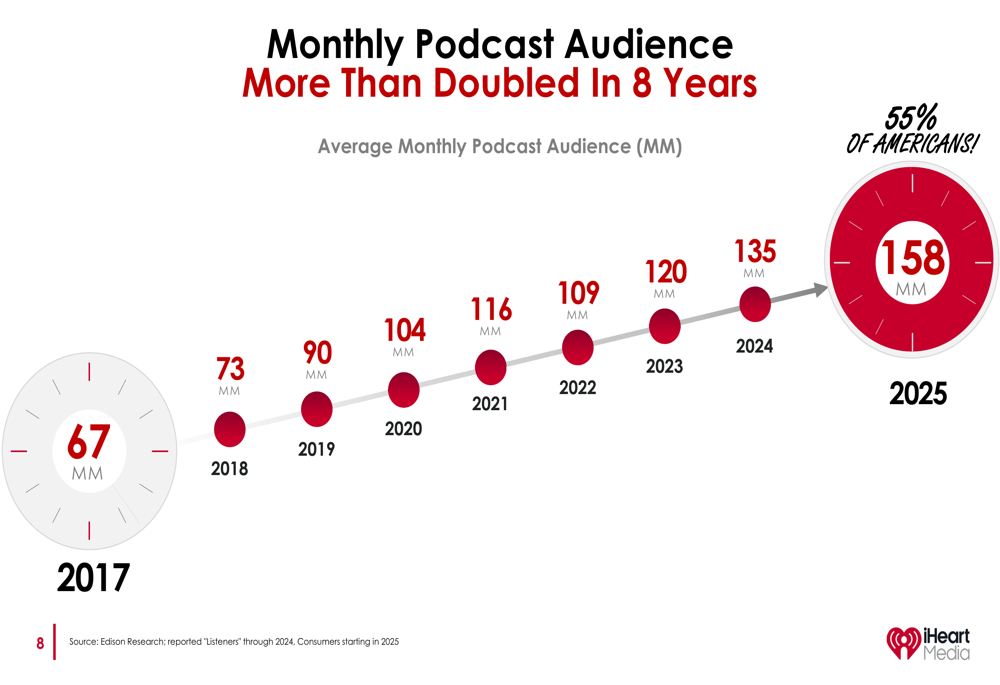

This growth is supported by the continued expansion of the podcast audience in the United States:

With 158 million monthly podcast listeners in 2025, representing 55% of Americans, the addressable market continues to expand, providing further growth opportunities for iHeartMedia’s podcast business.

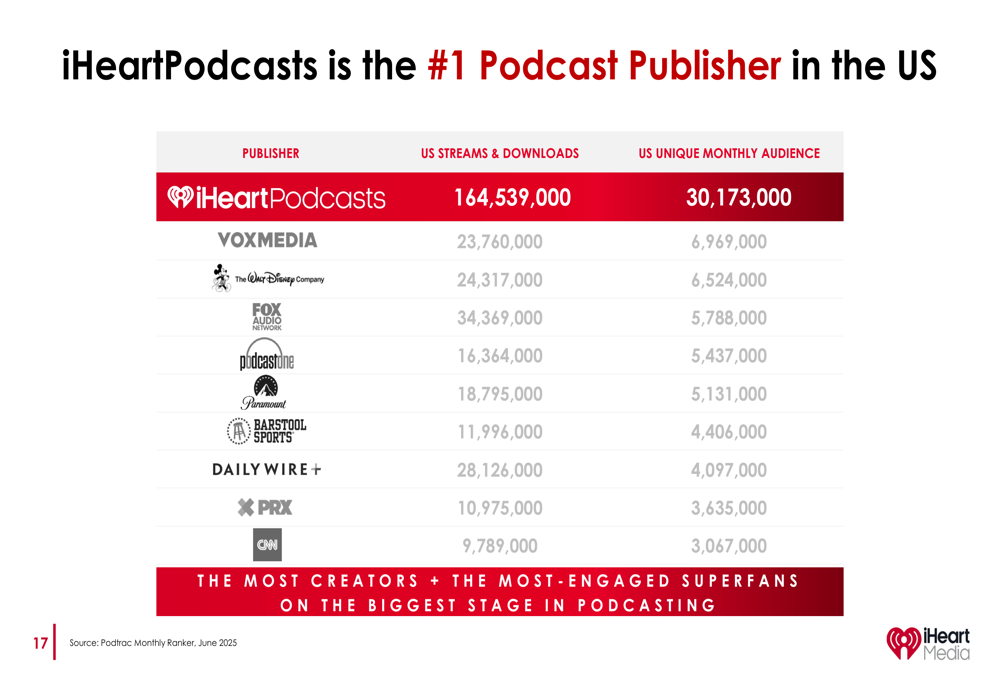

The company has maintained its dominant position in the podcast market:

As the #1 podcast publisher in the U.S., iHeartPodcasts generated 164.5 million U.S. streams and downloads in June 2025, reaching 30.2 million unique monthly listeners, significantly outpacing competitors like VOXMEDIA and The Walt Disney Company (NYSE:DIS).

The company’s leadership extends across all podcast categories:

Modernization Program Progress

iHeartMedia’s $200 million gross savings modernization program is on track, with expected net savings of $150 million in 2025. The program focuses on technology and AI-driven efficiencies across the organization.

The following chart breaks down the distribution of these savings:

The majority of savings (65%) are coming from the Multiplatform Group, with the remainder distributed across Corporate (15%), Audio & Media Services (10%), and Digital Audio Group (10%). By type, cost of sales represents the largest portion at 65%, followed by headcount reductions (20%), vendor reductions (10%), and occupancy costs (5%).

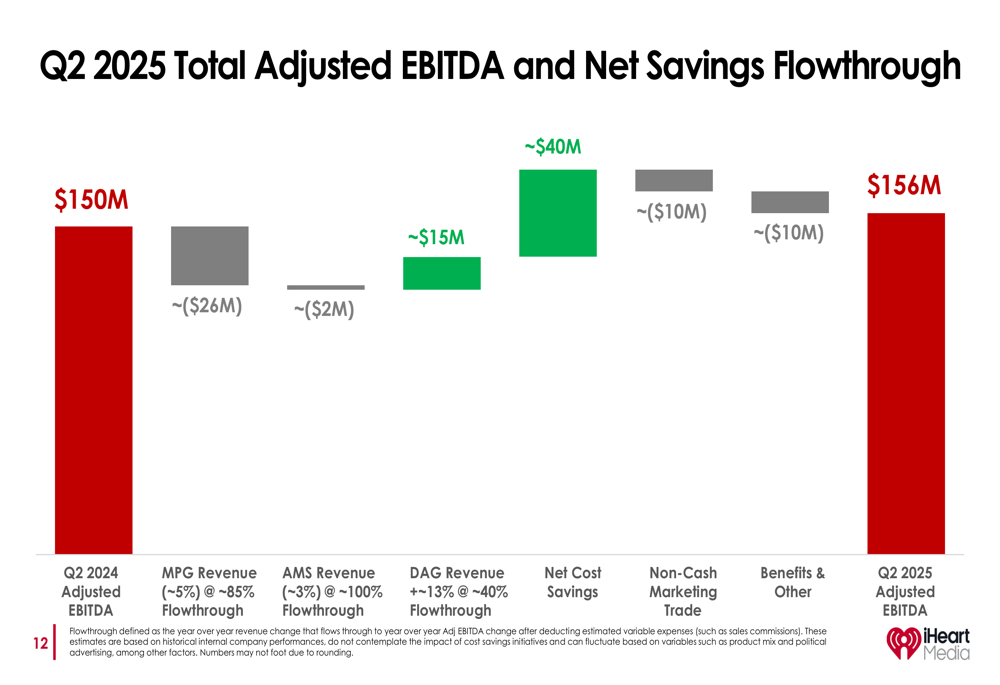

These cost-saving measures have contributed significantly to the improved EBITDA performance despite revenue challenges in the traditional radio business:

The waterfall chart illustrates how the $40 million in net cost savings helped offset the negative impact from Multiplatform Group revenue decline (-$26 million) and other factors, resulting in the overall EBITDA growth from $150 million in Q2 2024 to $156 million in Q2 2025.

Quarterly Performance Highlights

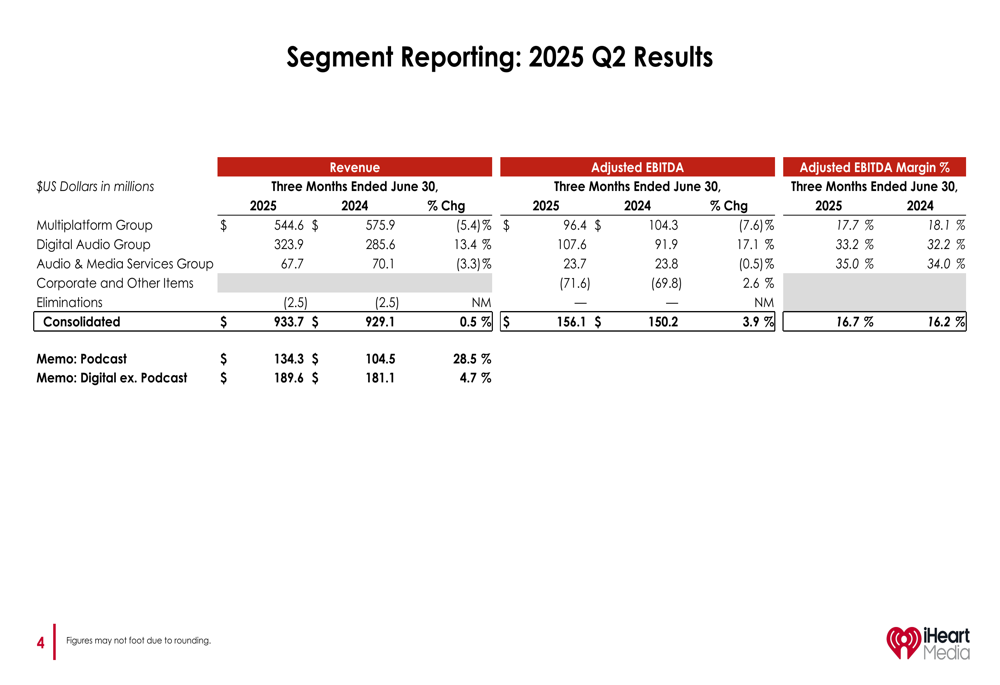

A more detailed breakdown of the Q2 2025 results by segment reveals the divergent performance across the company:

The Digital Audio Group’s 33.2% adjusted EBITDA margin significantly outperforms the Multiplatform Group’s 17.7% margin, highlighting the superior economics of the digital business. The Audio & Media Services Group maintained strong profitability with a 35.0% adjusted EBITDA margin on revenue of $67.7 million.

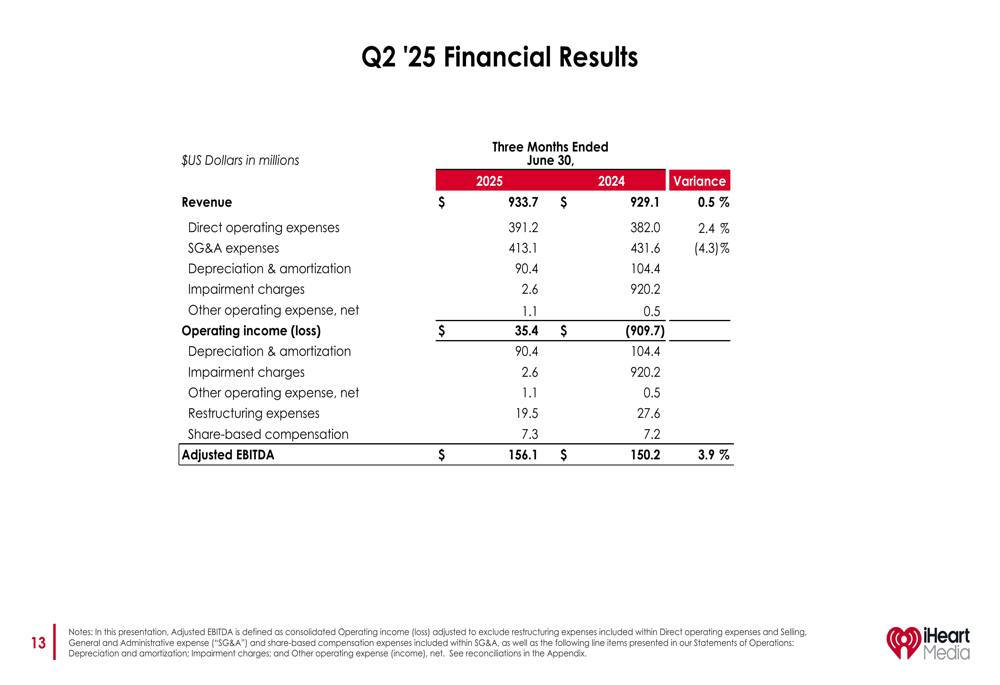

The company’s overall financial results for the quarter show improvement in profitability metrics despite increased direct operating expenses:

Direct operating expenses increased by 2.4% to $391.2 million, while SG&A expenses decreased by 4.3% to $413.1 million, reflecting the impact of the modernization program’s cost-saving initiatives.

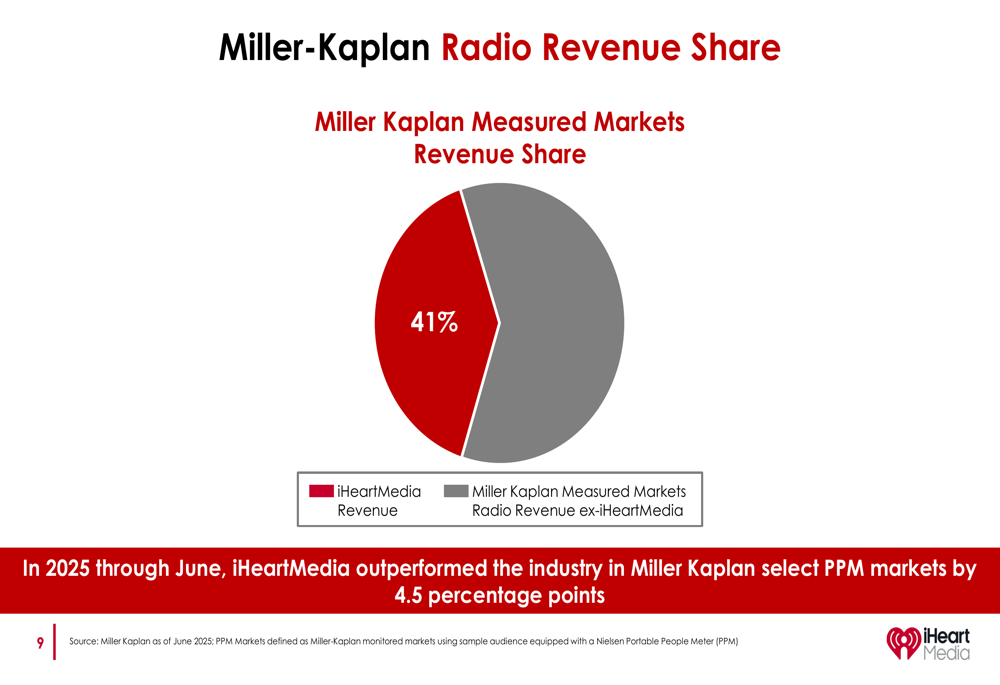

Competitive Industry Position

iHeartMedia continues to dominate the U.S. radio market, with a 41% share of revenue in Miller Kaplan measured markets:

The company outperformed the industry in these PPM markets by 4.5 percentage points through June 2025, demonstrating relative strength despite the overall challenges facing traditional radio.

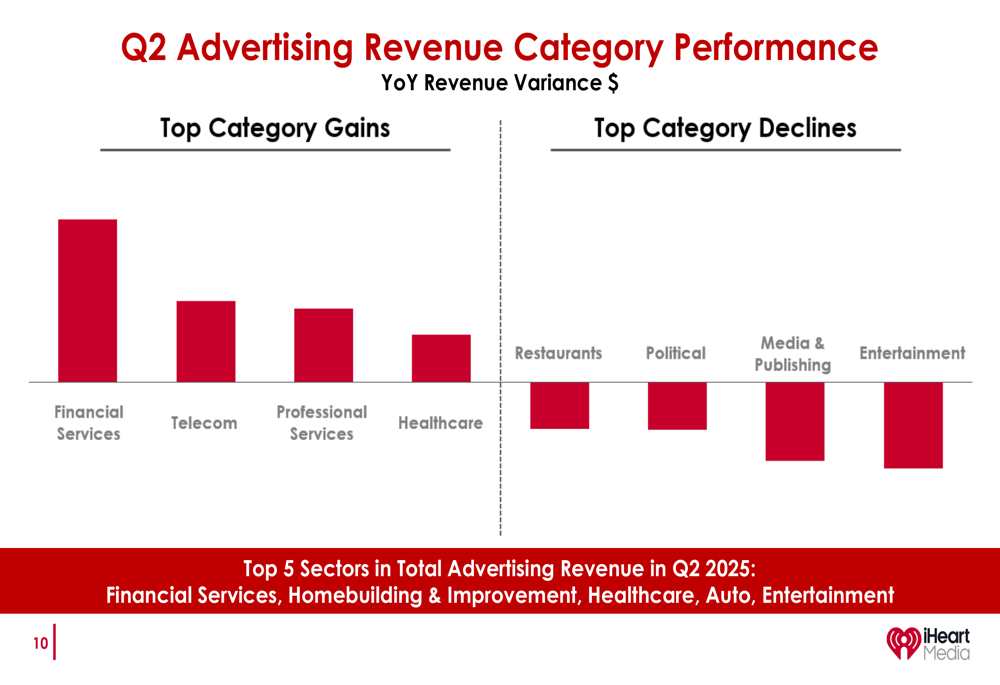

The top advertising categories for Q2 2025 included Financial Services, Homebuilding & Improvement, Healthcare, Auto, and Entertainment:

Forward-Looking Statements

Looking ahead to Q3 2025, iHeartMedia expects consolidated revenue to decline in the low-single digits, though revenue excluding political impact is projected to increase in the low-single digits. Consolidated adjusted EBITDA is expected to be approximately $180-220 million.

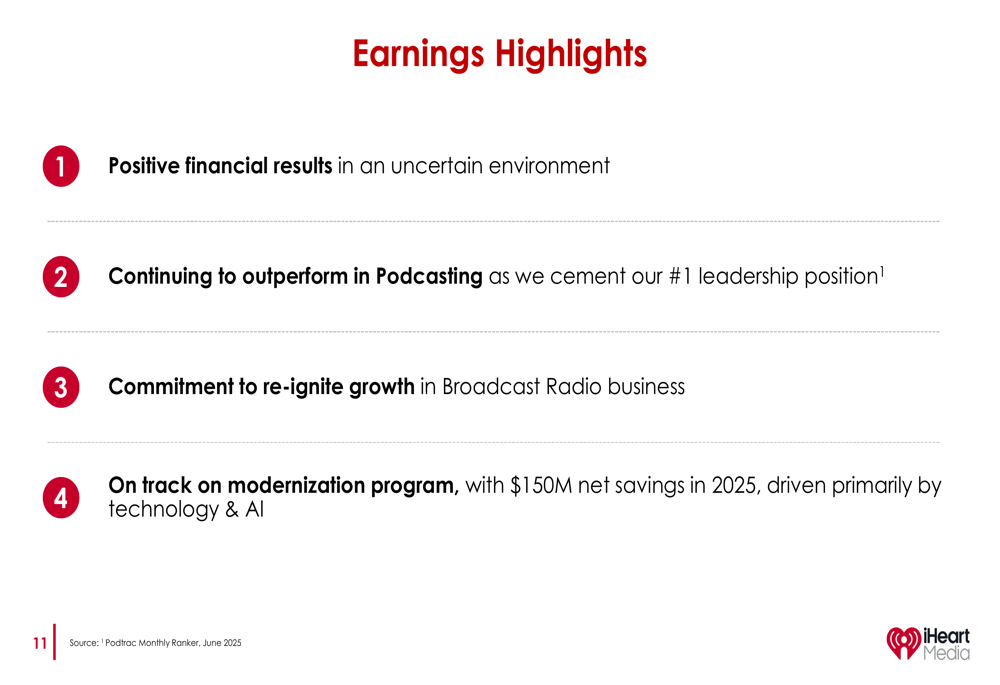

The company highlighted four key points in its earnings summary:

Management emphasized positive financial results despite an uncertain environment, continued leadership in podcasting, commitment to revitalizing the broadcast radio business, and progress on the modernization program.

Debt and Liquidity

Despite operational improvements, iHeartMedia continues to carry a substantial debt burden, with total debt of $5.14 billion and net debt of $4.64 billion as of June 30, 2025. The weighted average cost of debt stands at 9.2%, representing a significant financial expense for the company.

The stock closed at $1.60 on August 11, 2025, down 0.31% for the day, and remains well below its 52-week high of $2.84. The company’s market performance continues to be impacted by concerns over its high debt levels and the ongoing structural challenges in the traditional radio business, despite the impressive growth in its digital segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.