How are energy investors positioned?

Introduction & Market Context

Illinois Tool Works Inc. (NYSE:ITW) presented its second quarter 2025 earnings results on July 30, 2025, highlighting sequential improvement in key financial metrics despite varied performance across its business segments. The industrial manufacturer reported modest year-over-year growth while emphasizing its ability to outperform underlying end markets.

In pre-market trading, ITW shares remained steady at $259.50, following a previous close of $259.50. The stock has traded in a 52-week range of $214.66 to $279.13, currently sitting near the upper end of that range.

Quarterly Performance Highlights

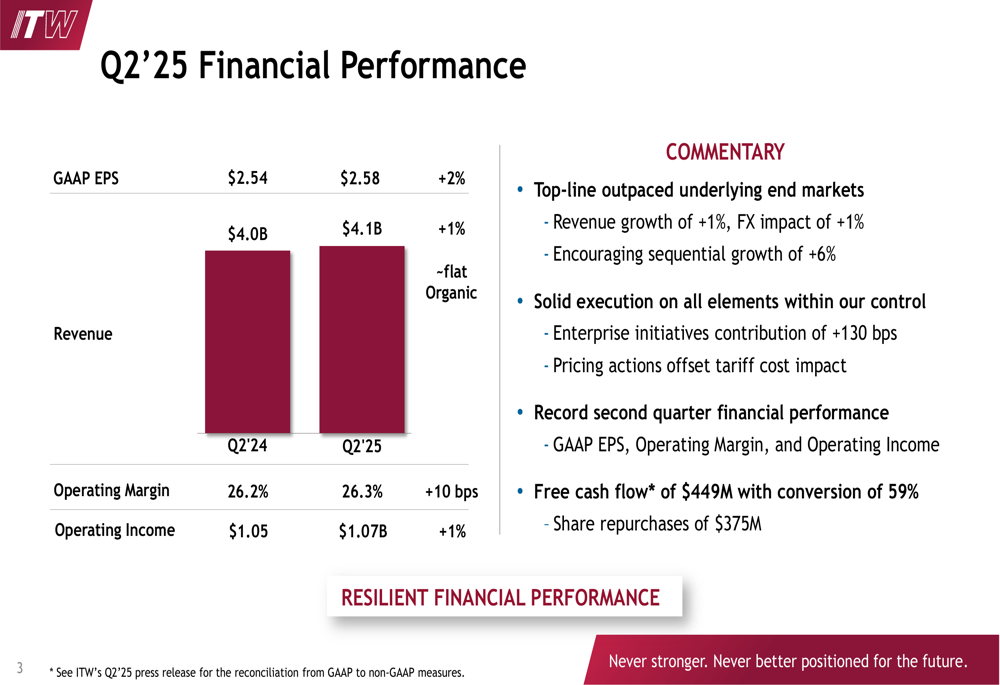

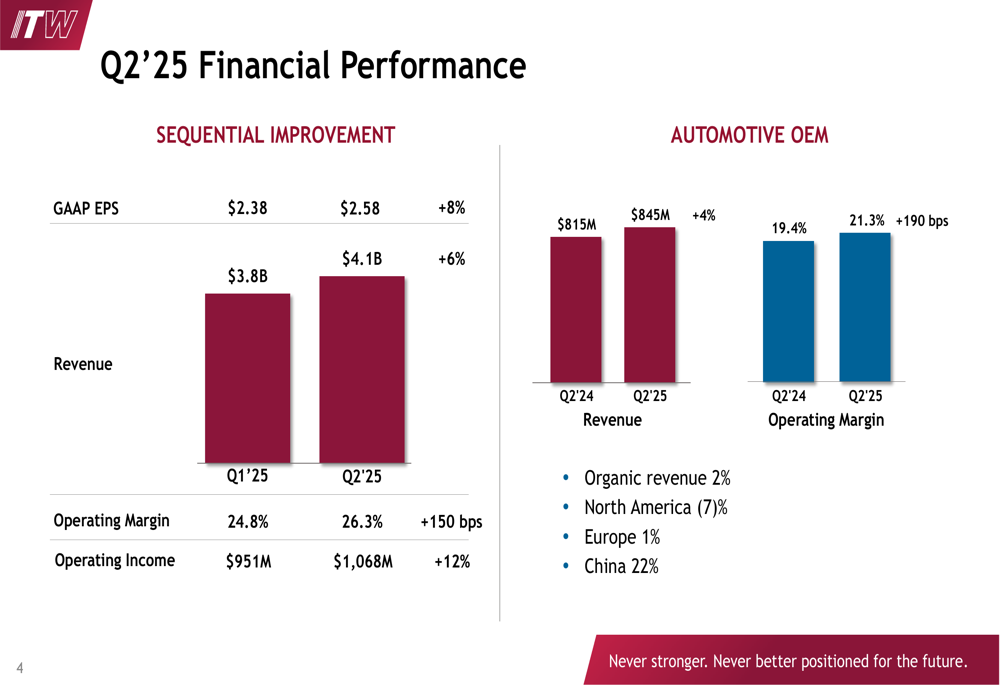

ITW reported GAAP earnings per share of $2.58 for Q2 2025, representing a 2% increase year-over-year and an 8% sequential improvement from Q1’s $2.38. Revenue reached $4.1 billion, up 1% from the prior year and 6% sequentially from Q1’s $3.8 billion.

As shown in the following quarterly performance overview:

The company maintained strong profitability with an operating margin of 26.3%, a 10 basis point improvement year-over-year, resulting in operating income of $1.07 billion. Free cash flow reached $449 million with a conversion rate of 59%, while the company continued its capital return program with $375 million in share repurchases during the quarter.

The sequential improvement from Q1 to Q2 demonstrates the company’s resilience and execution capabilities, as illustrated in this comparison:

Segment Analysis

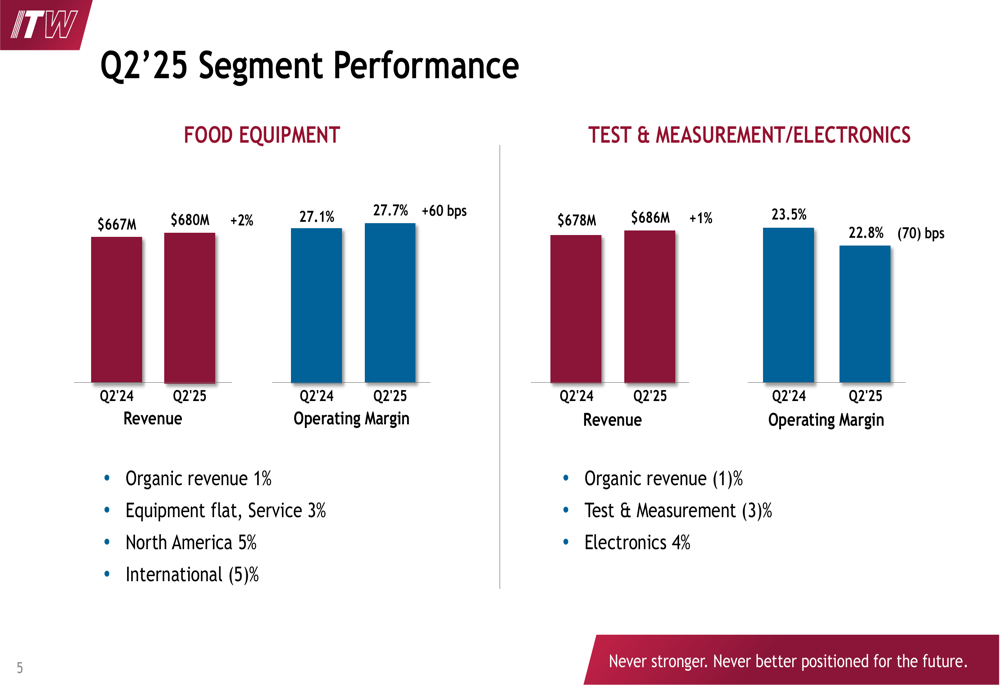

ITW’s performance varied significantly across its seven business segments, with five reporting revenue growth and margin improvement.

The Automotive OEM segment showed notable strength with revenue of $845 million, up 4% year-over-year, and an operating margin of 21.3%, representing a substantial 190 basis point improvement. Regional performance within this segment was particularly varied, with North America declining 7%, Europe growing 1%, and China delivering exceptional 22% growth.

Food Equipment continued its positive trajectory with revenue of $680 million, up 2%, and an operating margin of 27.7%, a 60 basis point improvement. North American food equipment sales grew 5%, while international markets declined 5%.

As shown in the following segment breakdown:

Test & Measurement/Electronics reported mixed results with revenue increasing 1% to $686 million, but operating margin declining 70 basis points to 22.8%. Within this segment, Test & Measurement declined 3% organically, while Electronics grew 4%.

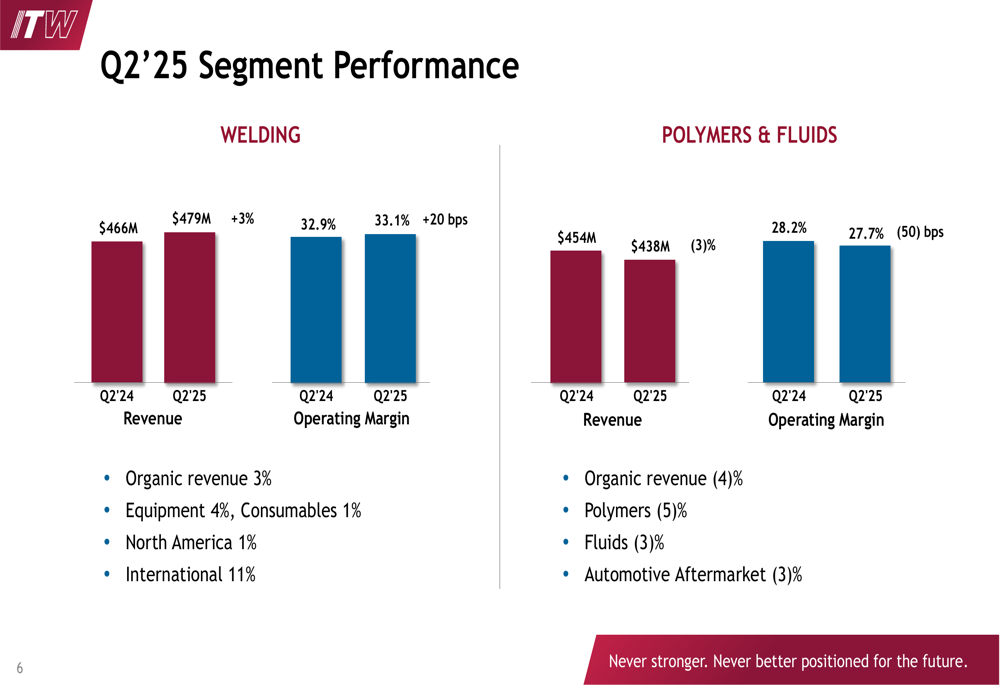

The Welding segment demonstrated solid performance with 3% revenue growth to $479 million and a 20 basis point margin improvement to 33.1%, maintaining its position as the company’s highest-margin business.

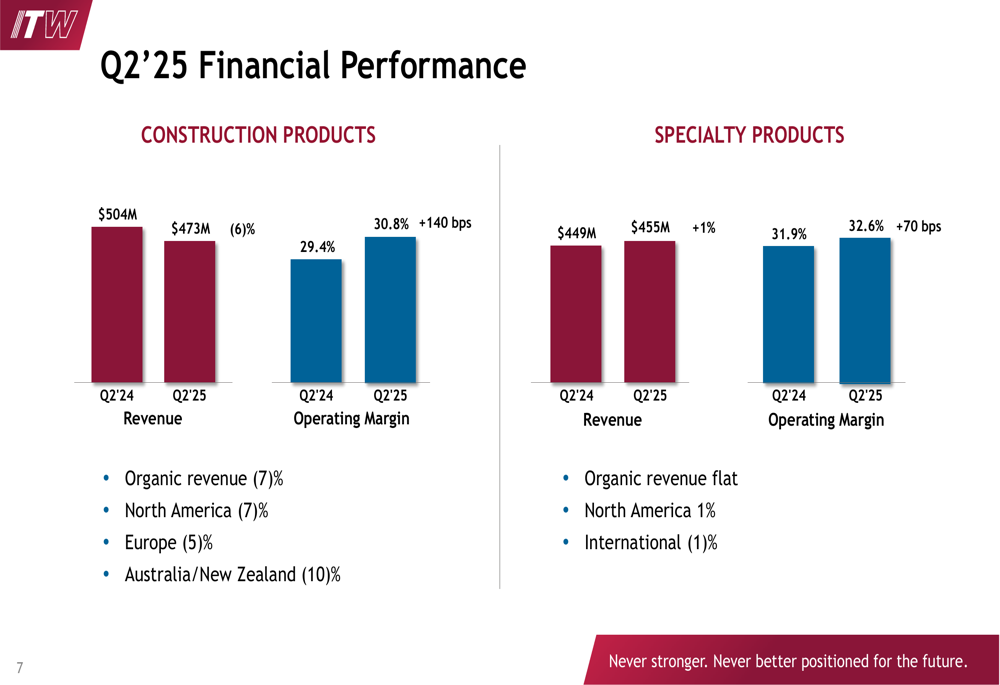

Construction Products faced the most significant challenges among all segments, with revenue declining 6% to $473 million. However, the segment managed to improve operating margin by 140 basis points to 30.8%, showcasing ITW’s ability to maintain profitability despite revenue pressure. The construction slowdown was widespread, with North America down 7%, Europe down 5%, and Australia/New Zealand down 10%.

Forward Guidance

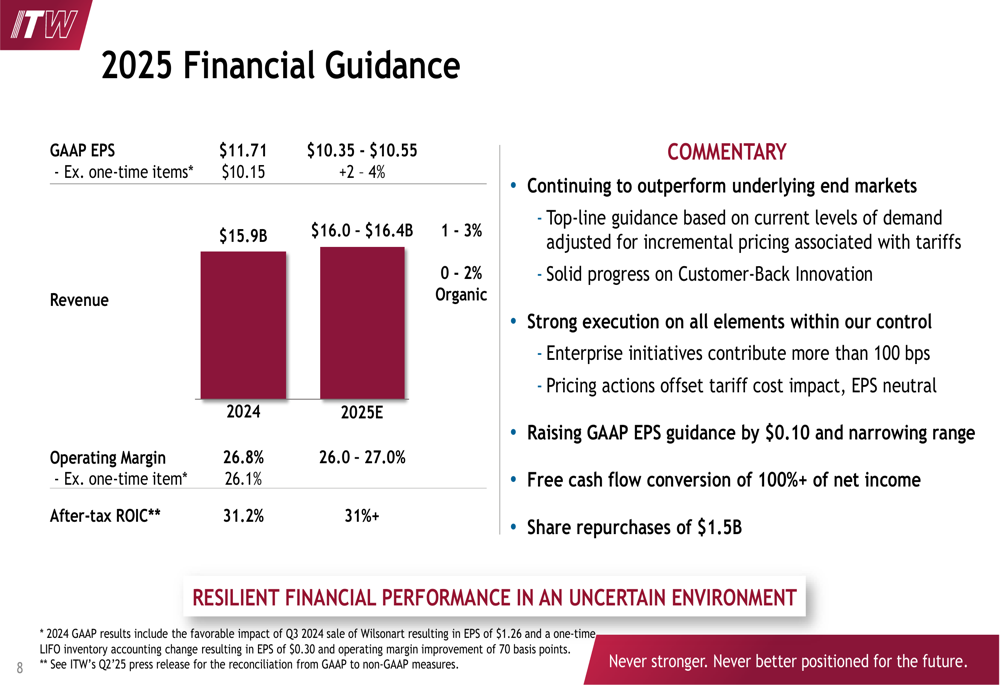

Illinois Tool Works raised the lower end of its full-year 2025 earnings guidance while maintaining the upper end. The company now expects GAAP EPS between $10.35 and $10.55, representing 2-4% growth. This is a $0.10 increase to the lower end compared to previous guidance.

Revenue is projected to reach between $16.0 billion and $16.4 billion, a 1-3% increase, with organic growth of 0-2%. Operating margin is expected to remain strong at 26.0-27.0%, with after-tax return on invested capital exceeding 31%.

The detailed guidance is presented in the following slide:

Management emphasized that enterprise initiatives are expected to contribute more than 100 basis points to margin expansion, while pricing actions will offset tariff cost impacts. The company projects free cash flow conversion exceeding 100% of net income and plans to execute $1.5 billion in share repurchases for the full year.

Strategic Initiatives

ITW continues to focus on its Customer-Back Innovation approach, which the company credits for helping it outperform underlying end markets. This strategy appears to be yielding results, particularly in segments like Food Equipment and Welding, where organic growth exceeded broader market performance.

The company’s ability to implement pricing actions to offset tariff impacts demonstrates its pricing power and strategic agility. Management indicated these actions would be EPS neutral, protecting margins without sacrificing competitiveness.

The presentation repeatedly emphasized ITW’s positioning statement: "Never stronger. Never better positioned for the future," reflecting management’s confidence despite mixed market conditions. This sentiment echoes CEO Chris O’Hareli’s statement from the Q1 earnings call that "ITW is built to outperform in uncertain and volatile environments."

Regional Trends

Geographic performance varied significantly across ITW’s portfolio, revealing important global economic trends. China stood out as a growth driver, particularly in the Automotive OEM segment where it posted 22% growth, contrasting sharply with North America’s 7% decline in the same segment.

Construction markets showed weakness globally, with North America, Europe, and Australia/New Zealand all reporting declines. This aligns with broader economic indicators suggesting a slowdown in construction activity across developed markets.

Food Equipment demonstrated strength in North America (+5%) but weakness internationally (-5%), potentially reflecting different stages of post-pandemic recovery and consumer spending patterns across regions.

The Welding segment’s international business grew 11%, significantly outpacing North America’s 1% growth, suggesting stronger industrial activity in overseas markets.

These regional variations highlight the value of ITW’s diversified global footprint, allowing the company to offset weakness in certain regions with strength in others while maintaining overall growth.

Market Perspective

ITW’s Q2 2025 results demonstrate sequential improvement from Q1, with the company successfully navigating a challenging environment characterized by tariff pressures and mixed end markets. The ability to maintain and even expand margins despite revenue challenges in some segments showcases the effectiveness of the company’s enterprise initiatives and pricing strategies.

The raised guidance suggests management’s growing confidence in the company’s outlook for the remainder of 2025, despite acknowledging ongoing market uncertainties. With a strong balance sheet and consistent share repurchase program, ITW continues to deliver shareholder value even in a complex operating environment.

As the company enters the second half of 2025, investors will likely focus on whether the sequential improvement trend continues and how effectively ITW can manage the divergent performance across its segments and regions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.