Functional Brands closes $8 million private placement and completes Nasdaq listing

Introduction & Market Context

Inderes Oyj (HEL:INDERES) shared its Q3 2025 business review on October 22, 2025, revealing mixed results as the company navigates challenging market conditions. Despite reporting a 7% decline in quarterly revenue, Inderes saw its stock price rise by 1.89% to €15.9 following the presentation, suggesting investor confidence in the company’s strategic direction.

The Finnish financial services firm continues to face headwinds from increased delistings in Nordic markets and customer cost-saving pressures, particularly affecting its events business. However, the company’s focus on recurring revenue streams and software development appears to be resonating with investors as it transitions into its internationalization phase.

Quarterly Performance Highlights

For Q3 2025, Inderes reported a revenue decline of 7% compared to the same period last year, with project revenue dropping significantly by 28%. However, this was partially offset by a 3% growth in recurring revenue, which now accounts for 75% of total revenue, up from 67% in Q3 2024.

The company’s EBITA for the quarter totaled €0.7 million, representing an 18.4% margin, down from €1.0 million (23.6% margin) in the previous year. International operations contributed 25% of total revenue, slightly up from 23% in Q3 2024.

As shown in the quarterly income statement below:

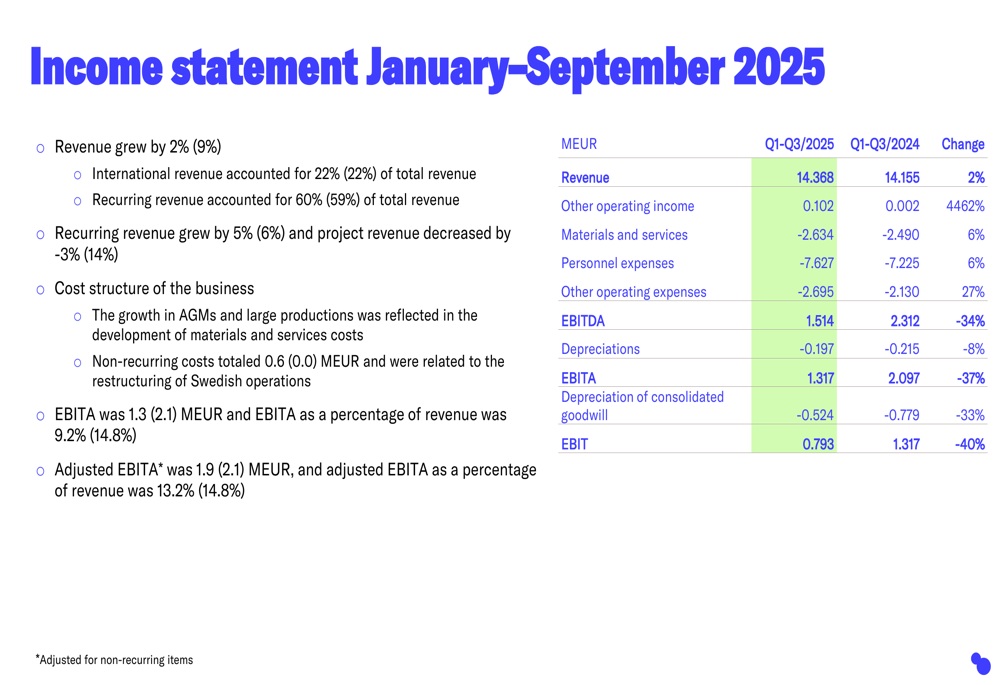

For the first nine months of 2025, Inderes achieved modest revenue growth of 1.5%, compared to 9.2% in the same period last year. The January-September adjusted EBITA margin stood at 13.2%, down from 14.8% in the previous year, reflecting ongoing investments in growth initiatives.

The company’s key financial metrics for the nine-month period are illustrated here:

Inderes has maintained a strong focus on recurring revenue, which reached 60.4% of total revenue for the January-September period, up from 58.5% last year. This strategic emphasis on stable revenue streams has helped buffer against volatility in project-based income.

Strategic Initiatives

Inderes is implementing several strategic initiatives across its three business segments: Research, Events, and Software. In its research business, the company has maintained strong customer retention despite market delistings, with its contract portfolio decreasing slightly to 143 from 149. The Inderes platform reached 20.0 million site visits in the past 12 months, though active membership decreased to 66,000 from 72,000.

A significant focus for the company is its AI implementation, which aims to improve operational efficiency and international scalability. Additionally, Inderes has successfully migrated most customers to its new IR Suite platform and finalized the localization of its release distribution system in Sweden.

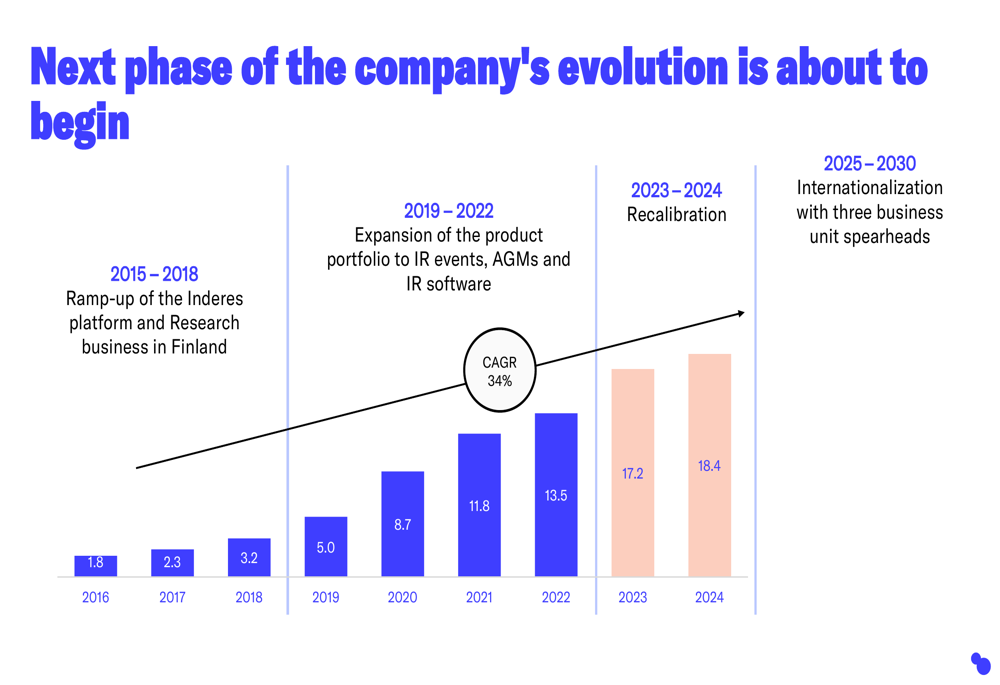

The company’s strategic evolution is clearly illustrated in this timeline, showing its transition from a Finnish research platform to an international financial services provider:

In the events business, Inderes faced challenges from an exceptionally strong comparison period and customer cost-saving pressures, which led to some productions being scaled down or postponed. However, the company is implementing a new strategy to transition to a unified operating model that will better serve large clients across the Nordic region.

The software business shows promising growth, with determined progress toward market leadership in Finland. Inderes has signed new international channel partners for both its IR software and Videosync platform, with significant investments being made in product development and sales.

Forward-Looking Statements

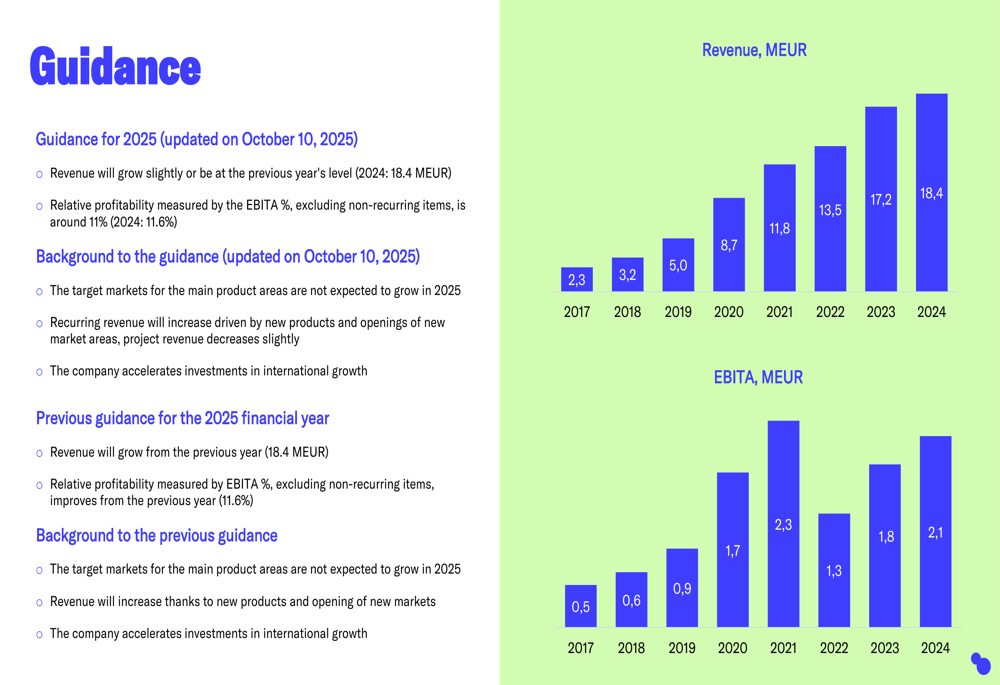

Inderes has updated its full-year 2025 guidance, expecting revenue to grow slightly or remain at the previous year’s level of €18.4 million. The company projects relative profitability measured by adjusted EBITA percentage to be around 11%, compared to 11.6% in 2024.

The guidance and historical performance trends are shown in the following chart:

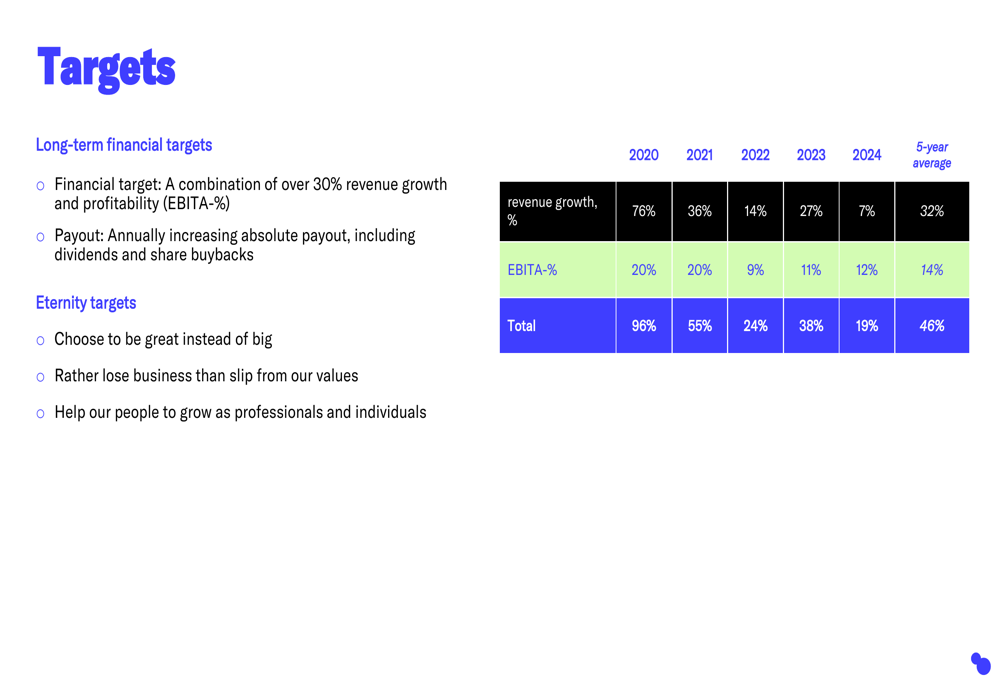

Long-term, Inderes maintains ambitious targets, aiming for a combined revenue growth and profitability (EBITA-%) of over 30%. The company has historically exceeded this target with a five-year average of 46%, though recent performance has been more modest.

The company’s strategic focus for 2025-2030 centers on internationalization with three business unit spearheads. This comes after a recalibration period in 2023-2024 following rapid expansion between 2019-2022.

Market indicators suggest potential tailwinds, with IPO activity showing signs of recovery after several years of increased delistings in both Finland and Sweden. This could create new opportunities for Inderes’ research and IR services as new companies enter public markets.

Despite current challenges, Inderes’ shift toward recurring revenue streams, software development, and international expansion positions the company to capitalize on market recovery while maintaining its commitment to shareholder returns, as evidenced by its 5.49% dividend yield and four consecutive years of dividend increases.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.