Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

ING Group (NYSE:ING) ( AMS (VIE:AMS2):INGA) released its second quarter 2025 results on July 31, showcasing continued commercial growth across key metrics while improving its full-year outlook. The banking group reported a net profit of €1,675 million for the quarter, supported by strong fee income growth and stable commercial net interest income (NII). The presentation highlighted ING’s progress toward its strategic goals, particularly in growing its mobile primary customer base and diversifying revenue streams.

The bank’s performance comes amid a challenging but stabilizing European banking environment, with ING maintaining a robust capital position well above regulatory requirements. The company’s share price has shown strong appreciation, rising from €13.9 in Q2 2024 to €18.6 by the end of Q2 2025, reflecting positive market sentiment toward the bank’s strategic execution.

Quarterly Performance Highlights

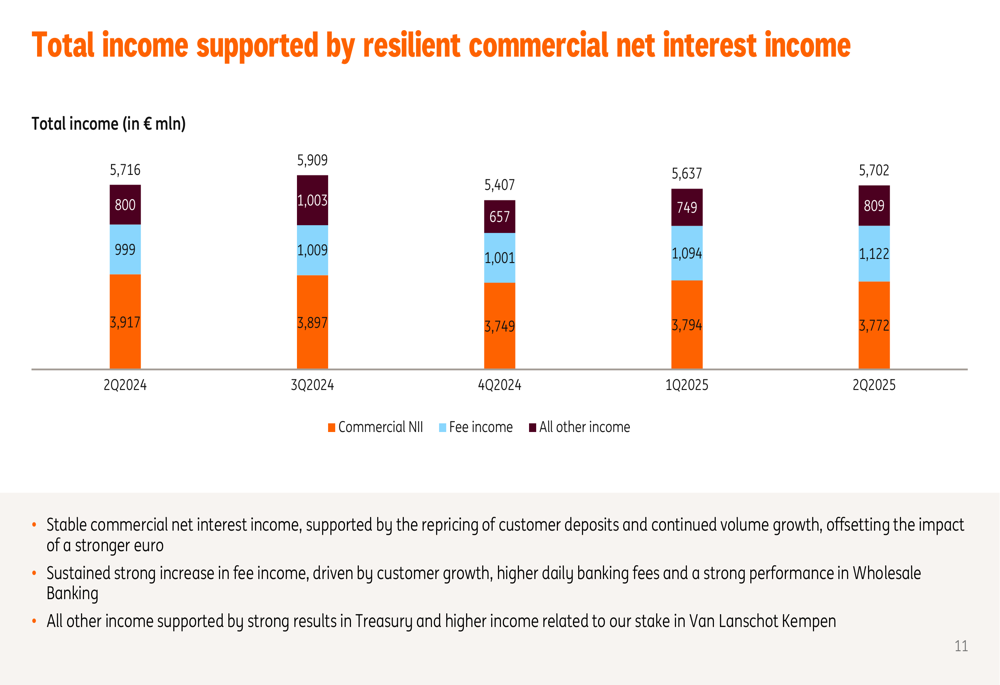

ING delivered solid financial results in Q2 2025, with total income reaching €5,702 million. The bank’s commercial net interest income remained resilient at €3,772 million, while fee income showed impressive growth, reaching €1,122 million – an 11% increase compared to the first half of 2024.

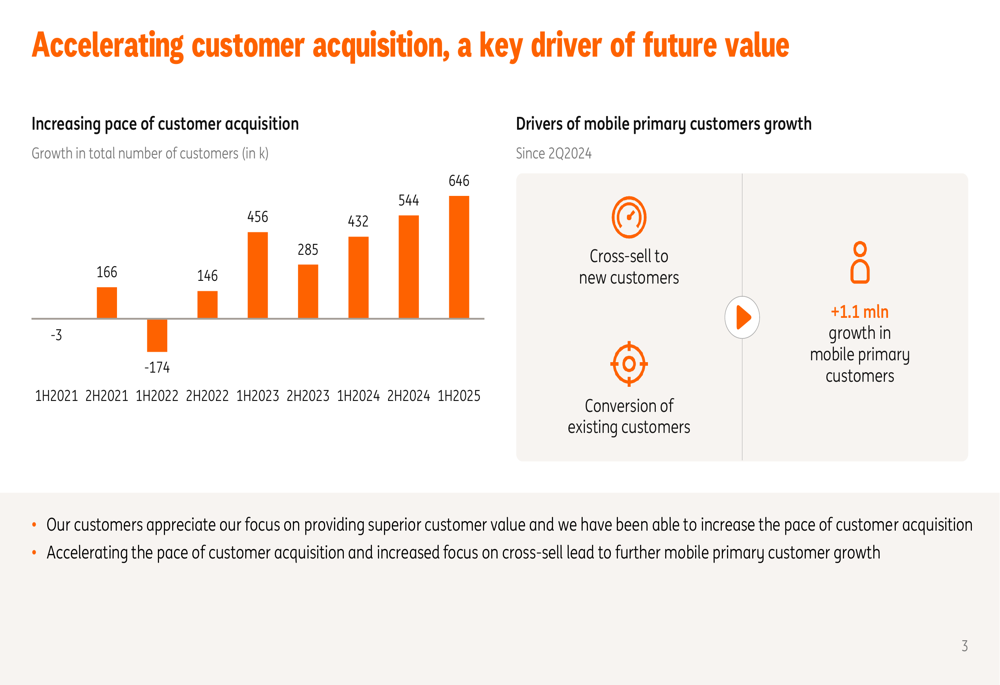

As shown in the following chart of key performance indicators, ING added 309,000 mobile primary customers during the quarter, with 37% of its over 40 million customers now classified as mobile primary:

Return on equity stood at 12.7%, keeping the bank on track to meet its revised 2025 target of approximately 12.5%, with a further increase to 14% targeted by 2027. The bank also reported significant progress in sustainable finance, with €68 billion mobilized, representing a 19% increase in sustainable finance activities.

Customer Growth and Strategy

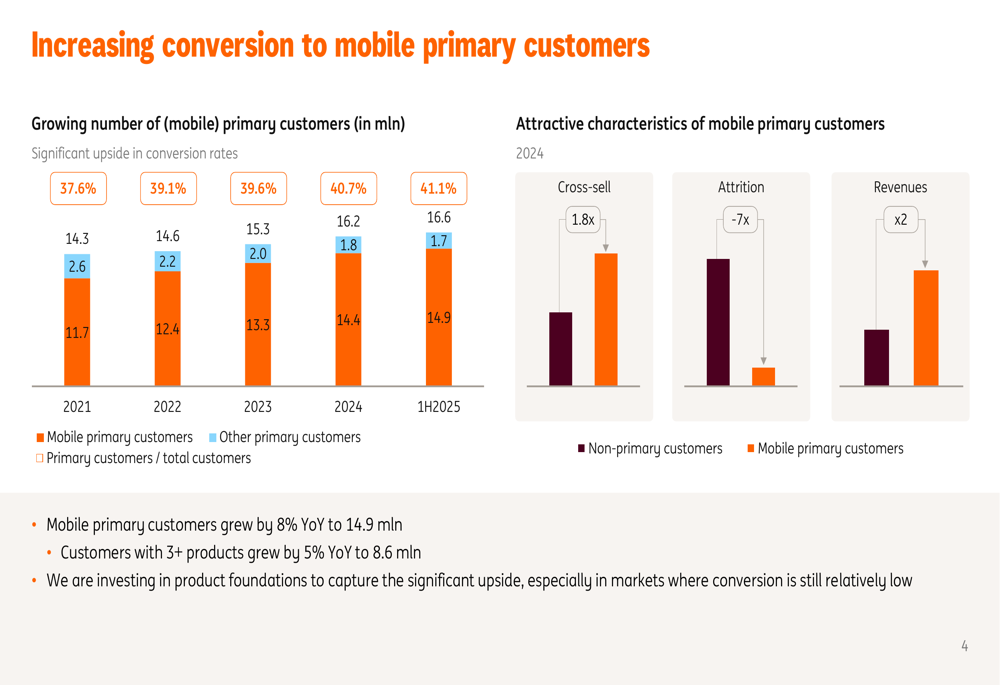

ING’s strategy continues to focus on growing its mobile primary customer base, which expanded by 8% year-over-year to 14.9 million. The bank is successfully converting existing customers to mobile primary status while also cross-selling additional products, with customers holding three or more products increasing by 5% year-over-year to 8.6 million.

The following chart illustrates ING’s accelerating customer acquisition trend, showing a consistent upward trajectory in new customer additions over recent periods:

This growth in the customer base is translating into increased business volumes. The bank reported lending growth of €15.4 billion and deposit growth of €6.2 billion in the first half of 2025, representing annualized growth rates of 6% and 8% respectively – both exceeding the bank’s annual target of approximately 4% growth.

The conversion to mobile primary customers is particularly important for ING’s business model, as these customers demonstrate significantly higher engagement and profitability:

Income and Balance Sheet Analysis

ING’s total income for Q2 2025 was supported by three main components: commercial NII at €3,772 million, fee income at €1,122 million, and other income at €809 million. While commercial NII remained stable compared to previous quarters, the bank expects it to increase in the second half of 2025.

The following chart breaks down ING’s total income components over the past five quarters:

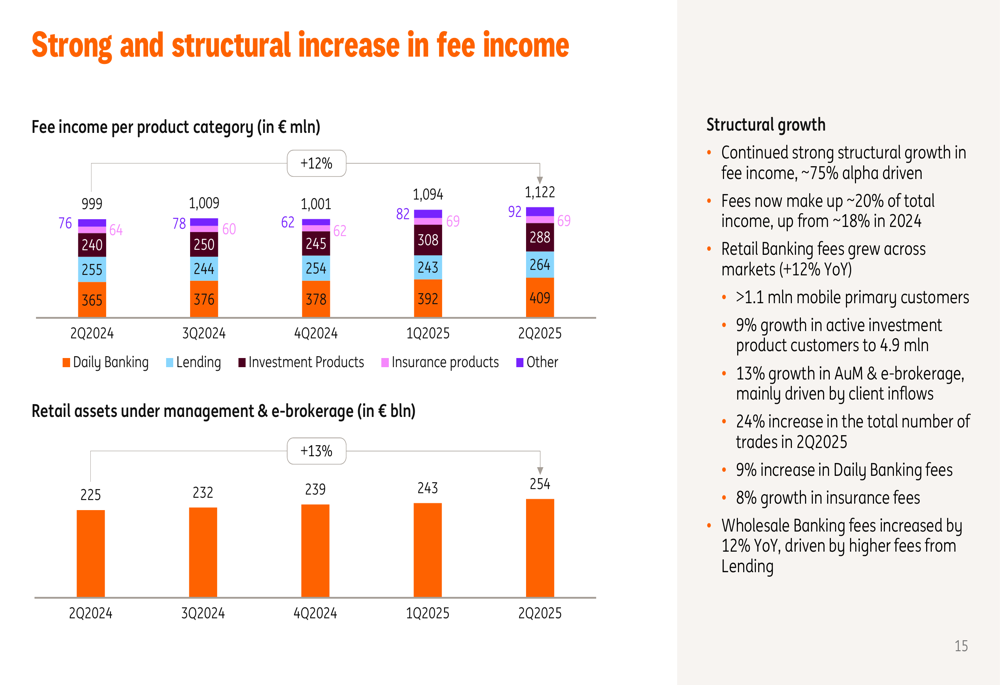

Fee income continues to be a bright spot, with double-digit growth driven by increases across most product categories. Investment products contributed €288 million, insurance products €264 million, and daily banking €92 million to the Q2 2025 fee income total. The bank’s assets under management and e-brokerage reached €254 billion, up from €225 billion in Q2 2024.

The detailed breakdown of fee income sources demonstrates the bank’s success in diversifying its revenue streams:

Capital Position and Shareholder Returns

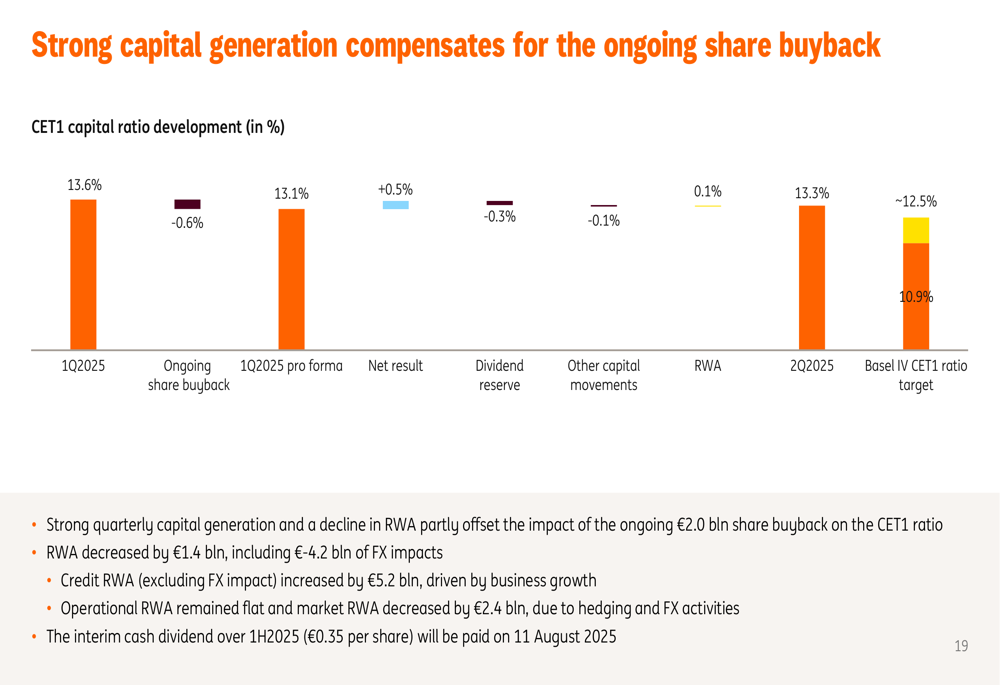

ING maintained a strong capital position, with a CET1 ratio of 13.3% at the end of Q2 2025, well above its target level of approximately 12.5%. This robust capital position enables the bank to continue returning value to shareholders through both dividends and share buybacks.

The following chart illustrates the development of ING’s CET1 ratio during the quarter:

In Q2 2025, ING distributed €2,152 million to shareholders, consisting of €1,205 million in share buybacks and €947 million in cash dividends. The bank’s shareholder return stood at 15.3% for the quarter, reflecting its commitment to delivering value to investors while maintaining a healthy capital position.

Outlook and Targets

ING has improved its outlook for 2025 while maintaining its ambitious 2027 targets. The bank now expects fee income to grow at the higher end of the 5-10% range for 2025, while expenses are projected to be at the lower end of the €12.5-€12.7 billion range. The return on equity outlook has been increased from >12% to approximately 12.5% for full-year 2025.

The following chart compares ING’s updated 2025 outlook with its 2027 targets:

For the remainder of 2025, ING expects commercial NII to remain stable in Q3 before increasing in Q4. The bank anticipates its CET1 ratio to be between 12.8-13.0% by year-end 2025, continuing to provide a solid foundation for business growth and shareholder returns.

Looking further ahead, ING remains committed to its 2027 targets, including annual growth of 1 million mobile primary customers, total income CAGR of 4-5% for 2024-2027, fee income of €5 billion, a cost/income ratio of 52-54%, and a return on equity of 14%.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.