Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Ingram Micro Holding Ltd (NYSE:INGM) reported strong first-quarter 2025 results on May 8, with revenue growth significantly outpacing expectations. The global technology distributor’s shares closed at $19.01, up 3.52% on the day, reflecting positive market reaction to the results. The company’s presentation highlighted its ongoing transformation into a platform business for the global technology ecosystem.

Following a relatively stable Q4 2024 that saw 2.5% year-over-year revenue growth, Ingram Micro has accelerated its momentum in Q1 2025, delivering double-digit growth across multiple metrics while continuing to strengthen its balance sheet.

Quarterly Performance Highlights

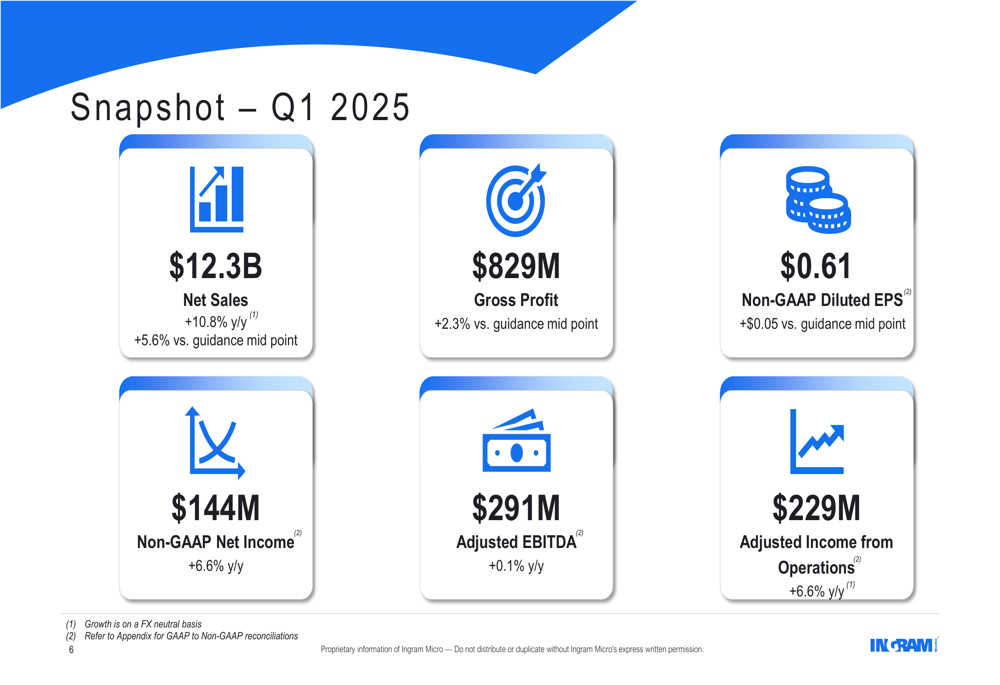

Ingram Micro reported Q1 2025 net sales of $12.3 billion, representing a 10.8% year-over-year increase on an FX neutral basis. This performance significantly exceeded guidance, coming in 5.6% above the midpoint of the company’s projections.

As shown in the following financial snapshot from the presentation, the company delivered solid bottom-line results as well:

Non-GAAP diluted EPS reached $0.61, exceeding guidance by $0.05, while non-GAAP net income grew 6.6% year-over-year to $144 million. Adjusted income from operations also increased by 6.6% to $229 million, though adjusted EBITDA remained essentially flat at $291 million.

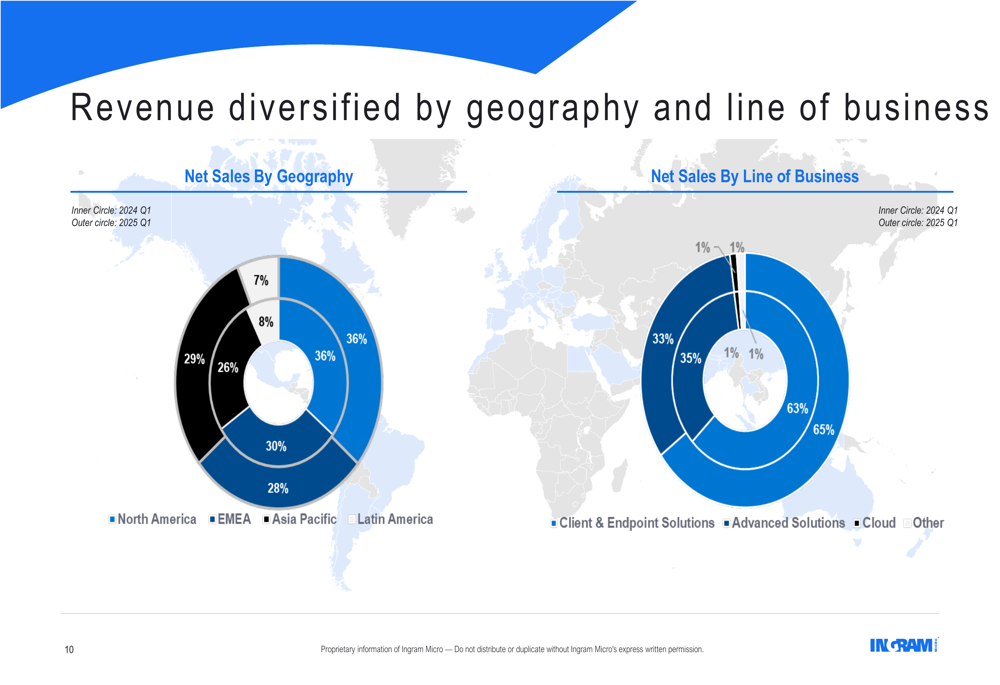

The company’s revenue growth was broad-based across geographies, with particular strength in the Client and Endpoint Solutions segment, alongside solid growth in Advanced Solutions and Cloud businesses. The following chart illustrates the company’s revenue diversification:

North America’s contribution to total revenue increased from 26% to 29% year-over-year, while Asia Pacific grew from 28% to 30%. From a business line perspective, Advanced Solutions increased its share from 33% to 35% of total revenue, reflecting the company’s strategic focus on higher-value segments.

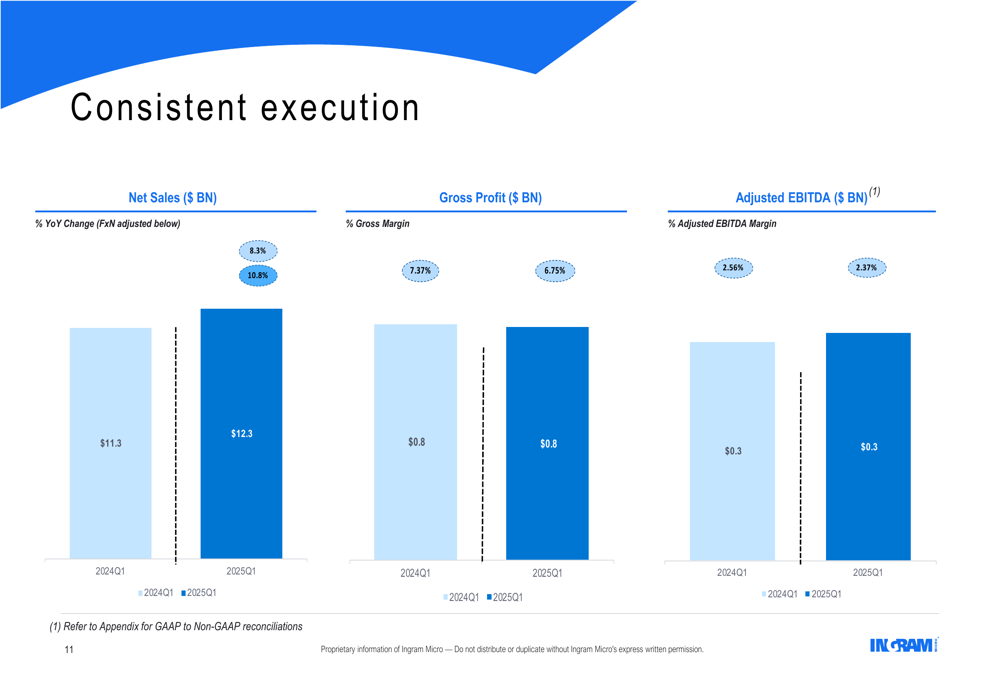

Despite the strong top-line growth, the company’s gross margin contracted from 7.37% in Q1 2024 to 6.75% in Q1 2025, as shown in this comparison of key metrics:

Digital Transformation Strategy

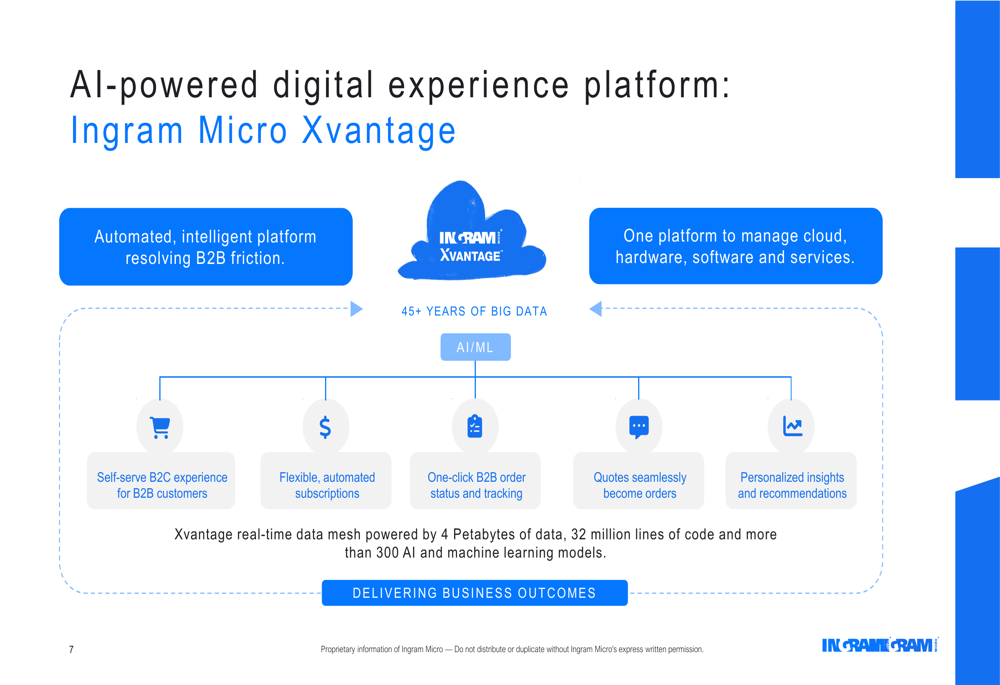

A key element of Ingram Micro’s growth strategy is its Xvantage digital platform, which the company describes as an "AI-powered digital experience platform" designed to resolve B2B friction points. The platform integrates cloud, hardware, software, and services management in a single interface.

The following slide details the capabilities and scale of the Xvantage platform:

The platform’s adoption has accelerated significantly, with self-serve orders more than tripling year-over-year in Q1 2025. The company reported that the platform processed 12 million searches for hardware, software, cloud, and services, while also reactivating thousands of previously dormant customers.

Ingram Micro’s digital transformation efforts have received external validation, with the company winning three 2025 iF Design Awards in the User Experience category for various Xvantage solutions. Industry analysts have also recognized the platform’s effectiveness, with an IDC Research VP highlighting how "Ingram Micro’s Xvantage platform and new Xvantage Integrations Hub demonstrate the balance required between integrations and interactions."

Financial Position & Outlook

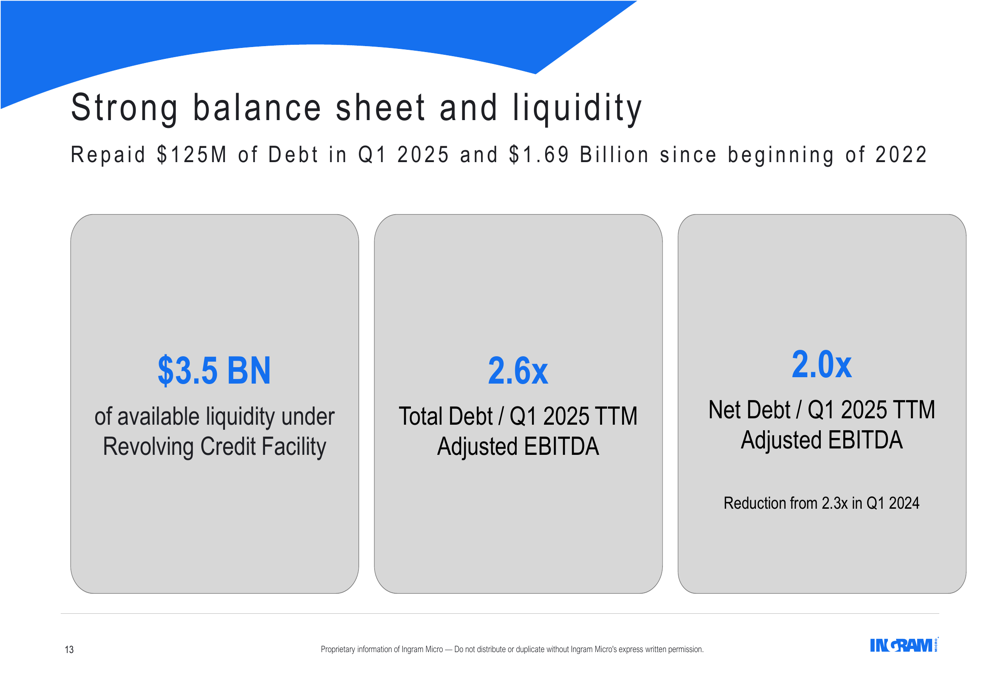

Ingram Micro continued to strengthen its balance sheet in Q1 2025, paying down an additional $125 million of term loan debt. This brings the company’s total debt repayment to $1.69 billion since 2022, reducing its leverage ratio to 2.0x from 2.3x in Q1 2024.

The following slide highlights the company’s improved financial position:

The company also initiated its dividend program, paying its first quarterly dividend and announcing an increased dividend for the second fiscal quarter. This move signals confidence in sustainable cash flow generation despite reporting negative adjusted free cash flow of $159 million for Q1 2025, compared to negative $67 million in the same period last year.

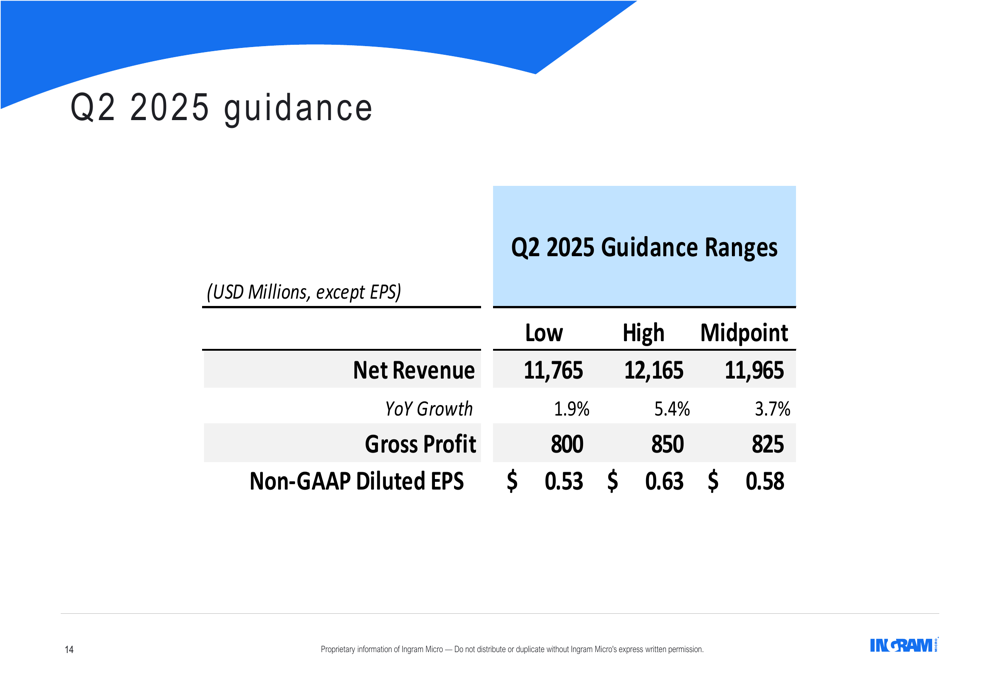

Looking ahead, Ingram Micro provided the following guidance for Q2 2025:

The company expects Q2 2025 net revenue between $11.77 billion and $12.17 billion, representing year-over-year growth of 1.9% to 5.4%. Non-GAAP diluted EPS is projected to be between $0.53 and $0.63, with a midpoint of $0.58.

Competitive Industry Position

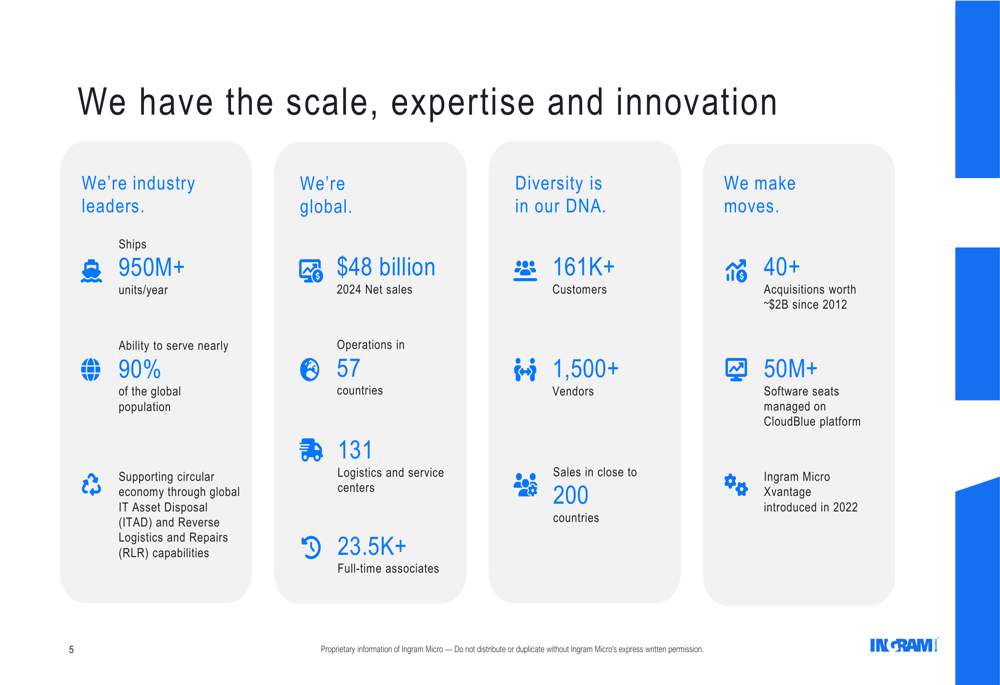

Ingram Micro’s scale and global reach continue to be key competitive advantages. The company highlighted its impressive operational footprint in the presentation:

With $48 billion in 2024 net sales, operations in 57 countries, and 131 logistics and service centers, Ingram Micro maintains its position as an industry leader in IT distribution. The company serves over 161,000 customers and works with more than 1,500 vendors, shipping over 950 million units annually.

The company’s acquisition strategy has also contributed to its growth, with more than 40 acquisitions worth approximately $2 billion since 2012. This approach, combined with the ongoing digital transformation initiatives, positions Ingram Micro to continue evolving from a traditional distributor to a technology platform business.

Forward-Looking Statements

Ingram Micro’s Q1 2025 results demonstrate continued execution of its strategic priorities: driving top-line growth, improving operational efficiency through digital transformation, and strengthening its financial position. The Xvantage platform appears to be gaining significant traction, potentially creating a competitive moat through improved customer experience and operational efficiency.

While the company faces some margin pressure, as evidenced by the year-over-year decline in gross margin percentage, its ability to grow adjusted income from operations suggests effective cost management. The initiation of a dividend program, combined with ongoing debt reduction, reflects management’s confidence in sustainable cash generation despite the seasonal negative free cash flow in Q1.

As Ingram Micro continues its transformation into a platform business, investors will likely focus on the company’s ability to maintain revenue growth while improving margins and cash flow generation in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.