Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

Insight Enterprises, Inc. (NASDAQ:NSIT) presented its second quarter 2025 earnings results on July 31, 2025, revealing a modest revenue decline offset by stable margins and continued strategic investments. The company’s stock traded down 1.41% in the previous session, with premarket activity showing an additional 1.1% decline to $143 following the earnings release. The presentation comes as the IT solutions provider navigates a challenging macroeconomic environment while positioning itself as a "Solutions Integrator" rather than a traditional reseller.

Quarterly Performance Highlights

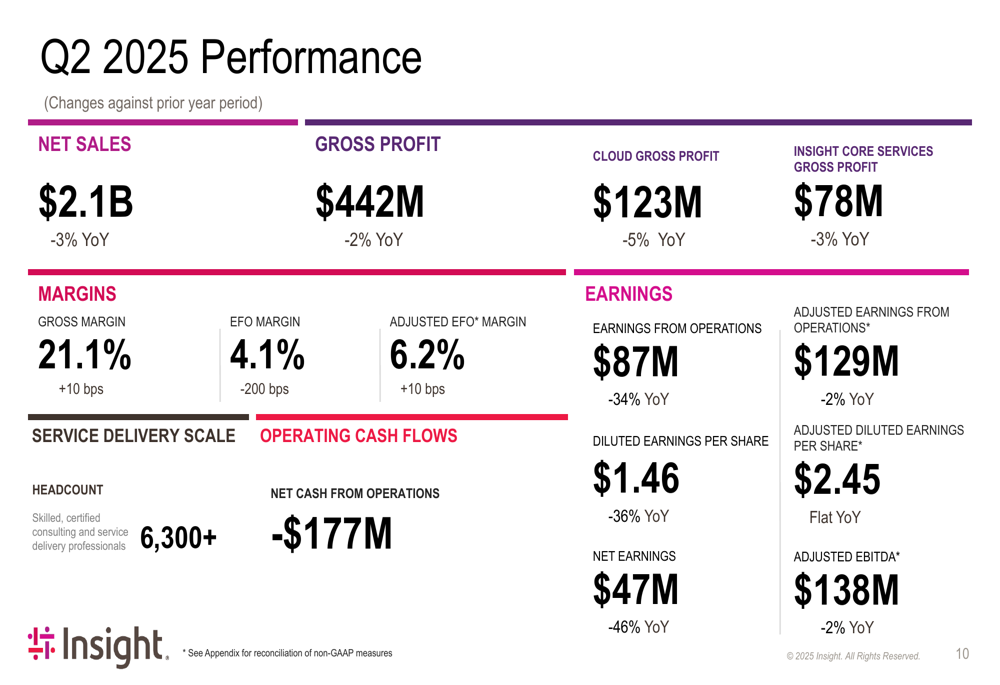

Insight reported second quarter net sales of $2.1 billion, representing a 3% year-over-year decline, while maintaining a gross profit of $442 million, down just 2% compared to the same period last year. Notably, the company improved its gross margin to 21.1%, a 10 basis point increase year-over-year.

As shown in the following financial performance summary:

The results show a significant divergence between GAAP and non-GAAP metrics. While earnings from operations declined 34% year-over-year to $87 million, adjusted earnings from operations showed a much more modest 2% decline to $129 million. Similarly, adjusted EBITDA of $138 million represented only a 2% year-over-year decrease.

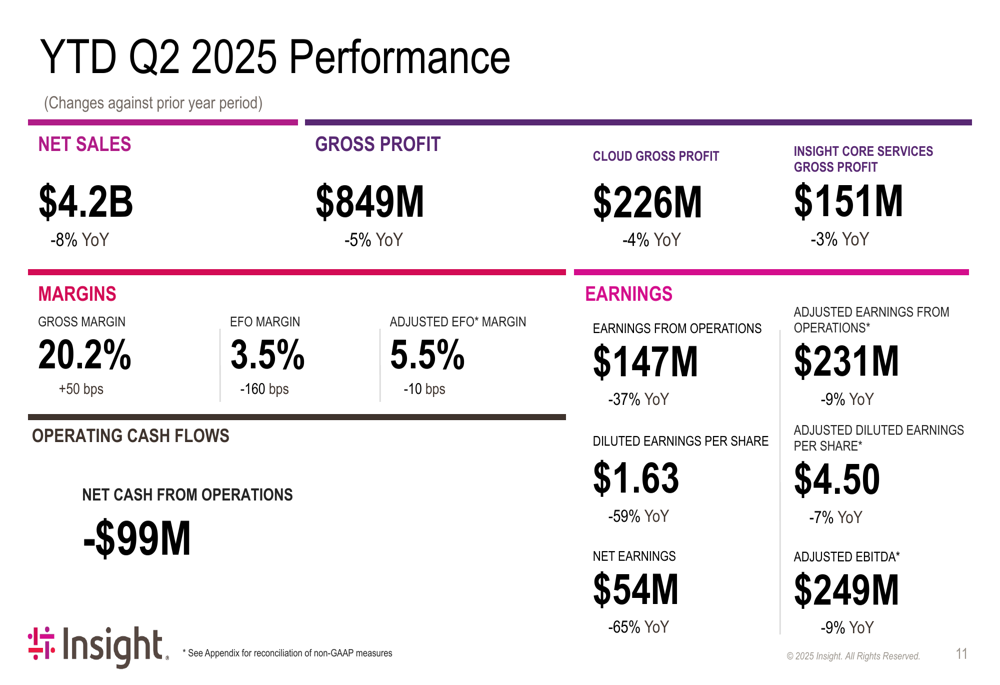

For the first half of 2025, the company’s performance showed more pronounced challenges, with year-to-date net sales of $4.2 billion representing an 8% decline compared to the same period in 2024. However, the gross margin for this period improved by 50 basis points to 20.2%.

Strategic Initiatives

Insight continues to position itself as a "Solutions Integrator" rather than a traditional systems integrator or reseller. This strategic focus is built on four key pillars: putting clients first, delivering differentiation, championing company culture, and driving profitable growth.

The company highlighted two case studies demonstrating its solutions-focused approach. In one example, Insight deployed an AI-powered document review solution leveraging Microsoft (NASDAQ:MSFT) Azure OpenAI Service, projecting annual savings of $7.5 million for the client. In another case, the company implemented comprehensive security solutions using Palo Alto Networks (NASDAQ:PANW) technology across multiple countries.

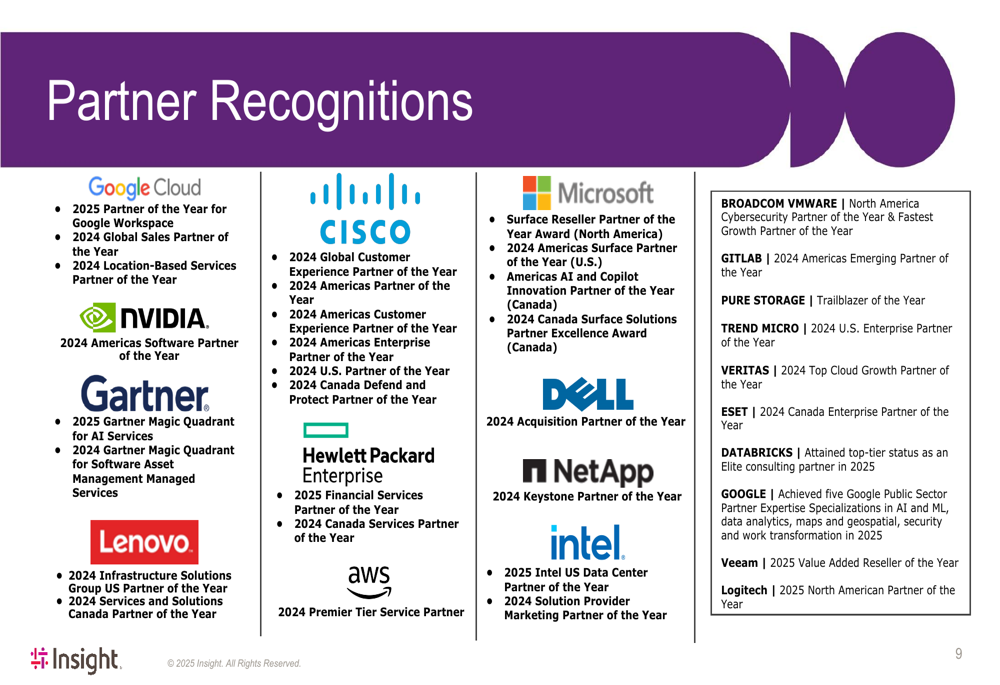

Insight’s market position is reinforced by numerous industry recognitions. The company has received partner awards from major technology providers including Google (NASDAQ:GOOGL) Cloud Partner of the Year, Cisco (NASDAQ:CSCO) Global Customer Experience Partner of the Year, and Microsoft Surface Reseller Partner of the Year.

The company has also garnered significant employer awards, ranking #447 on the Fortune 500 list and #37 in IT on Forbes’ 2024 World’s Best Employers list.

Debt and Capital Allocation

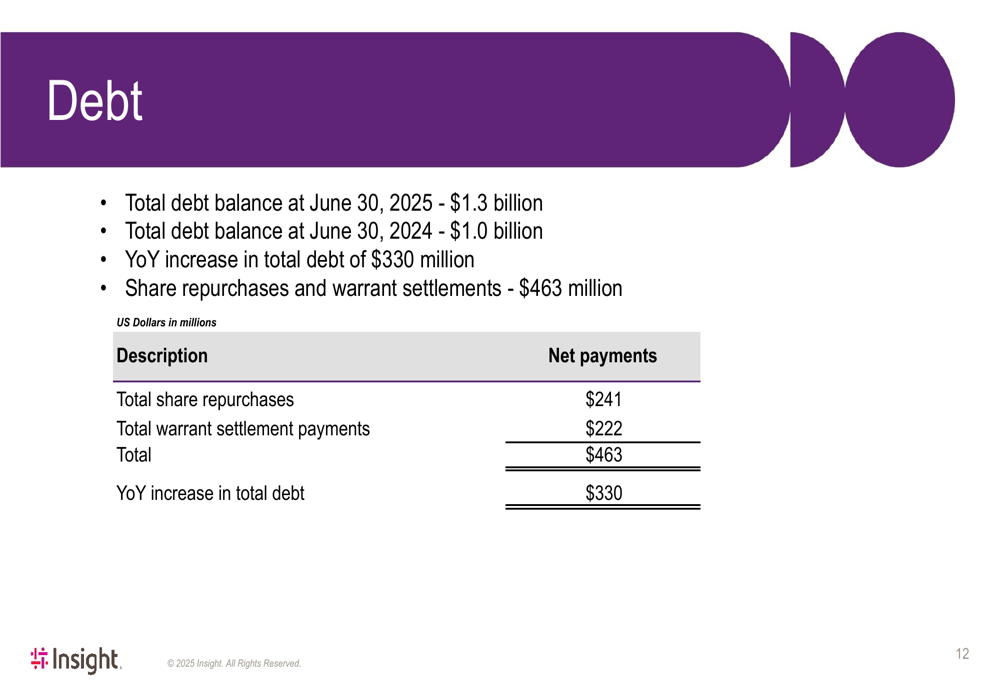

Insight’s total debt balance increased to $1.3 billion as of June 30, 2025, up from $1.0 billion a year earlier. This $330 million increase in debt was primarily driven by the company’s aggressive share repurchase program and warrant settlements, which totaled $463 million.

The company’s capital allocation strategy appears focused on returning value to shareholders through buybacks, even as revenue growth faces headwinds. This approach aligns with the 14% free cash flow yield mentioned in the previous quarter’s earnings report, demonstrating management’s commitment to shareholder returns despite challenging market conditions.

Forward-Looking Statements

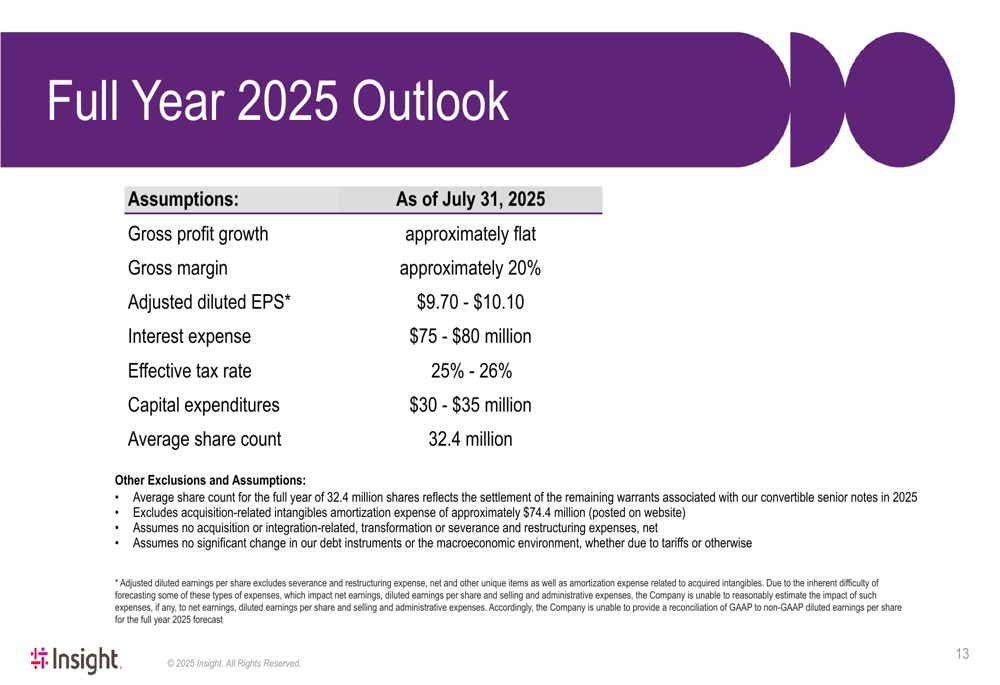

For the full year 2025, Insight maintained its previous guidance, projecting approximately flat gross profit growth with a gross margin of around 20%. The company expects adjusted diluted earnings per share between $9.70 and $10.10, with an effective tax rate between 25% and 26%.

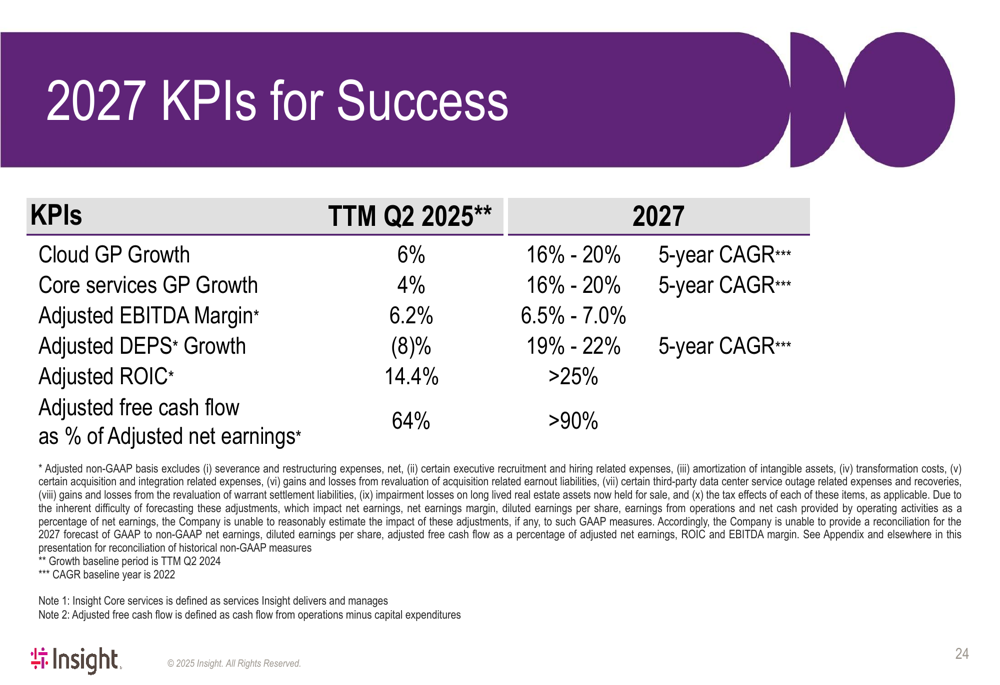

Looking further ahead, Insight outlined ambitious targets for 2027, including 16-20% growth in both cloud gross profit and core services gross profit (measured as 5-year CAGR), an adjusted EBITDA margin between 6.5-7.0% (compared to 6.2% currently), and adjusted diluted EPS growth of 19-22% (compared to -8% currently).

These long-term targets represent a significant acceleration from current performance levels, suggesting management expects substantial improvement in market conditions or significant benefits from the company’s strategic initiatives in the coming years.

Conclusion

Insight Enterprises’ Q2 2025 presentation reveals a company navigating revenue headwinds while maintaining margins and investing in strategic positioning as a solutions integrator. The significant gap between GAAP and adjusted earnings metrics highlights the impact of restructuring and transformation costs as the company pursues its strategic vision. Meanwhile, the increased debt load reflects a strong commitment to shareholder returns through buybacks despite the challenging revenue environment. Investors will be watching closely to see if the company can achieve its ambitious 2027 targets while managing the current market challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.