Gold prices steady ahead of Fed decision, Trump’s tariff deadline

Introduction & Market Context

Insight Enterprises Inc (NASDAQ:NSIT) released its first quarter 2025 earnings presentation on May 1, 2025, revealing a significant decline in revenue and earnings as the company continues to navigate a challenging IT spending environment. The company’s stock reacted negatively to the results, with shares down 3.1% in premarket trading to $134.00, extending a downward trend that has seen the stock fall from its 52-week high of $228.07.

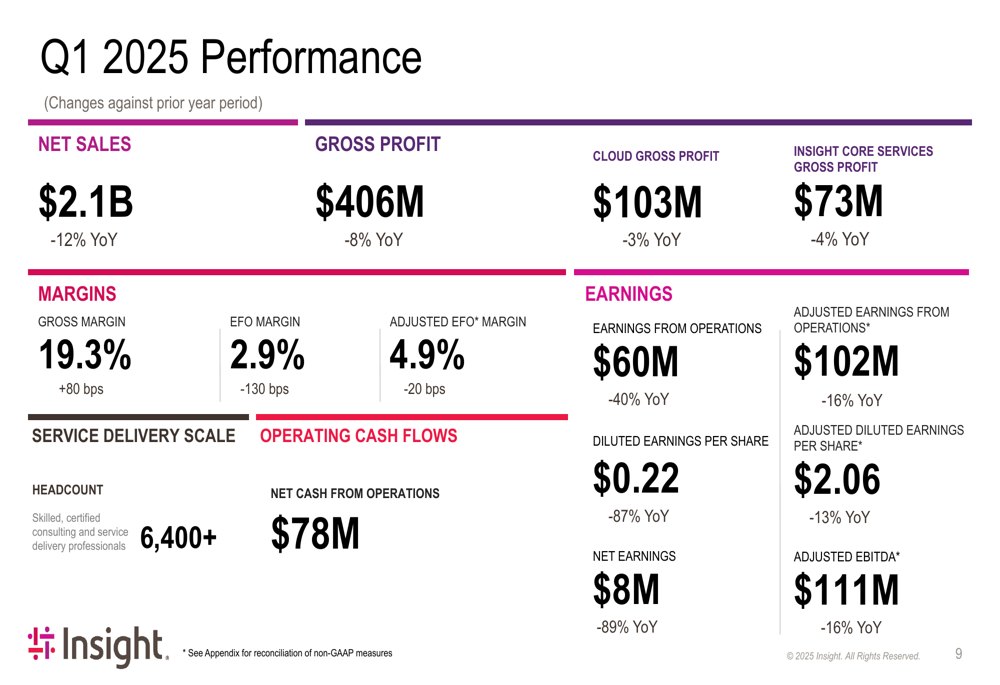

The results continue a pattern of weakness seen in previous quarters, as the company reported a 12% year-over-year decline in net sales to $2.1 billion, while net earnings plummeted 89% to $8 million. Despite these challenges, Insight maintained its strategic focus on transforming into what it calls a "Solutions Integrator" with emphasis on cloud services and core services.

Quarterly Performance Highlights

Insight’s Q1 2025 financial results showed broad-based declines across most key metrics. The company reported net sales of $2.1 billion, representing a 12% year-over-year decrease. Gross profit fell 8% to $406 million, though gross margin improved by 80 basis points to 19.3%.

As shown in the following comprehensive performance summary:

The earnings decline was particularly steep, with earnings from operations dropping 40% to $60 million and diluted earnings per share plunging 87% to $0.22. On an adjusted basis, which excludes certain non-recurring items, earnings from operations fell 16% to $102 million, while adjusted diluted EPS decreased 13% to $2.06.

The company’s services business showed more resilience than product sales, with services net sales declining 5% year-over-year to $396 million, while services gross profit fell 7% to $231 million. Cloud gross profit decreased 3% to $103 million, and Insight Core Services gross profit dropped 4% to $73 million.

Detailed Financial Analysis

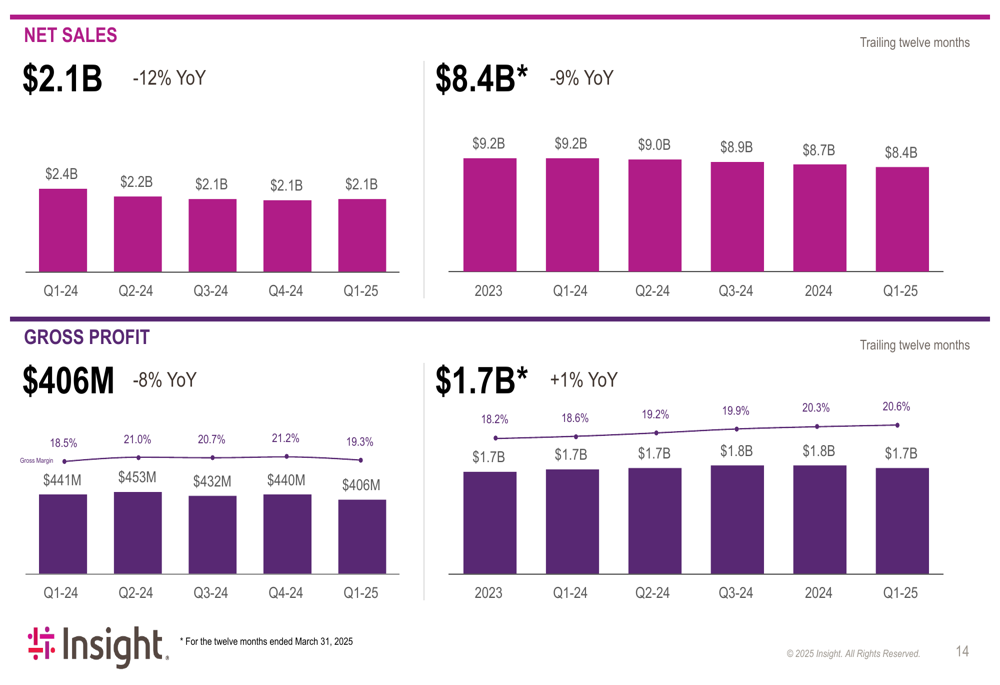

Looking at longer-term trends, Insight’s trailing twelve months (TTM) performance shows a 9% decline in net sales to $8.4 billion, while TTM gross profit increased slightly by 1% to $1.7 billion. The following chart illustrates these trends:

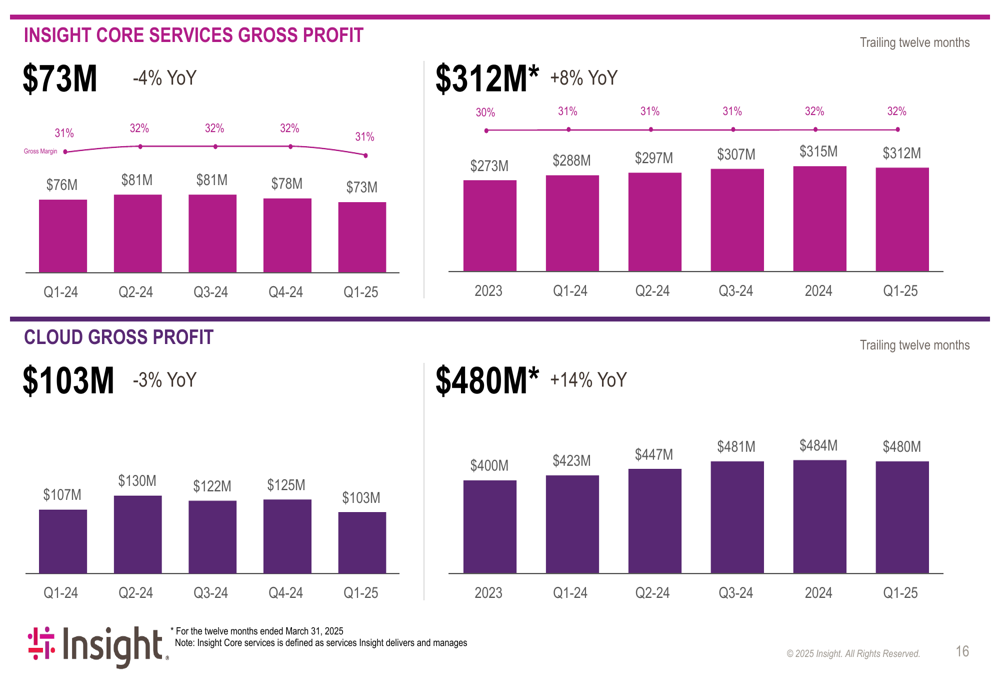

Despite current challenges, the company’s strategic focus areas of cloud and core services have shown better performance on a TTM basis. Cloud gross profit for the TTM period increased 14% to $480 million, while Insight Core Services gross profit grew 8% to $312 million, as shown in this chart:

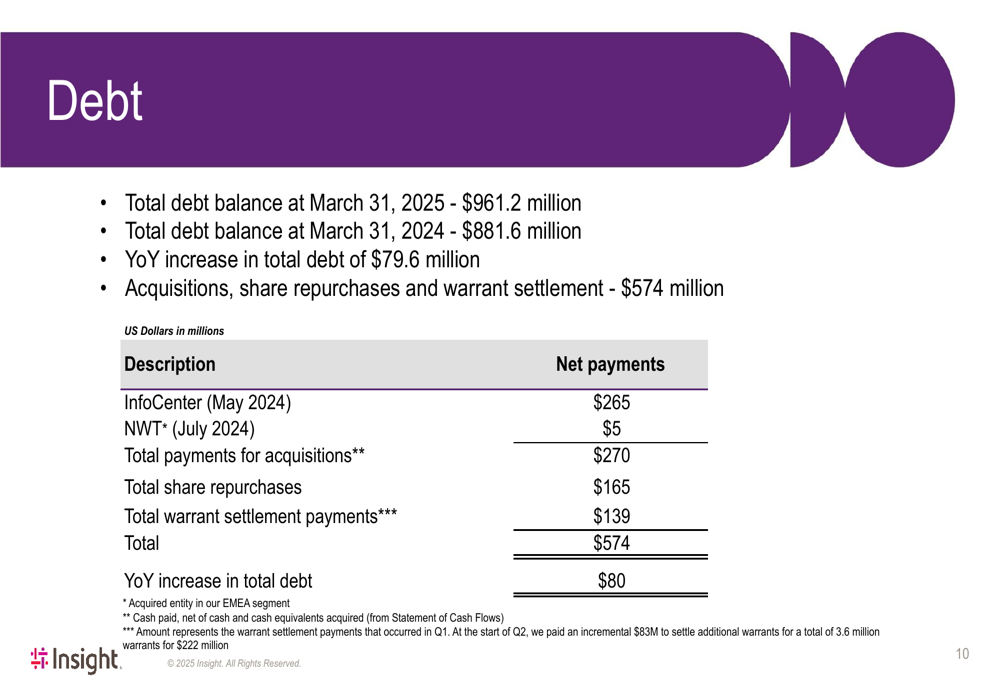

The company’s debt position has increased significantly, with total debt at $961.2 million as of March 31, 2025, up from $881.6 million a year earlier. This $79.6 million increase was primarily driven by acquisitions, share repurchases, and warrant settlements totaling $574 million.

From a regional perspective, all major geographic segments experienced revenue declines, with North America down 11%, EMEA (Europe, Middle East, and Africa) down 15%, and only APAC (Asia-Pacific) showing slight growth of 1%. Gross profit declined across all regions as well.

Strategic Initiatives

Despite the challenging financial results, Insight continues to position itself as a "Solutions Integrator" rather than a traditional systems integrator, reseller, or distributor. The company outlined four strategic pillars: Put Clients First, Deliver Differentiation, Champion Our Culture, and Drive Profitable Growth.

As illustrated in the company’s strategic framework:

The company showcased case studies demonstrating its capabilities in implementing AI solutions and data integration. One example featured The Sherlock Company, where Insight implemented an AI pipeline using Vertex (NASDAQ:VRTX) AI and Gemini to automate content selection, reducing processing time from days to minutes. Another highlighted Boyne Resorts, where Insight helped implement a Customer 360 integration project to unify customer data across multiple systems.

Insight also emphasized its industry recognition, including being named 2025 Google (NASDAQ:GOOGL) Partner of the Year for Google Workspace, Intel (NASDAQ:INTC) US Data Center Partner of the Year, and receiving a perfect score on the Human Rights Campaign Foundation’s 2025 Corporate Equality Index.

Forward-Looking Statements

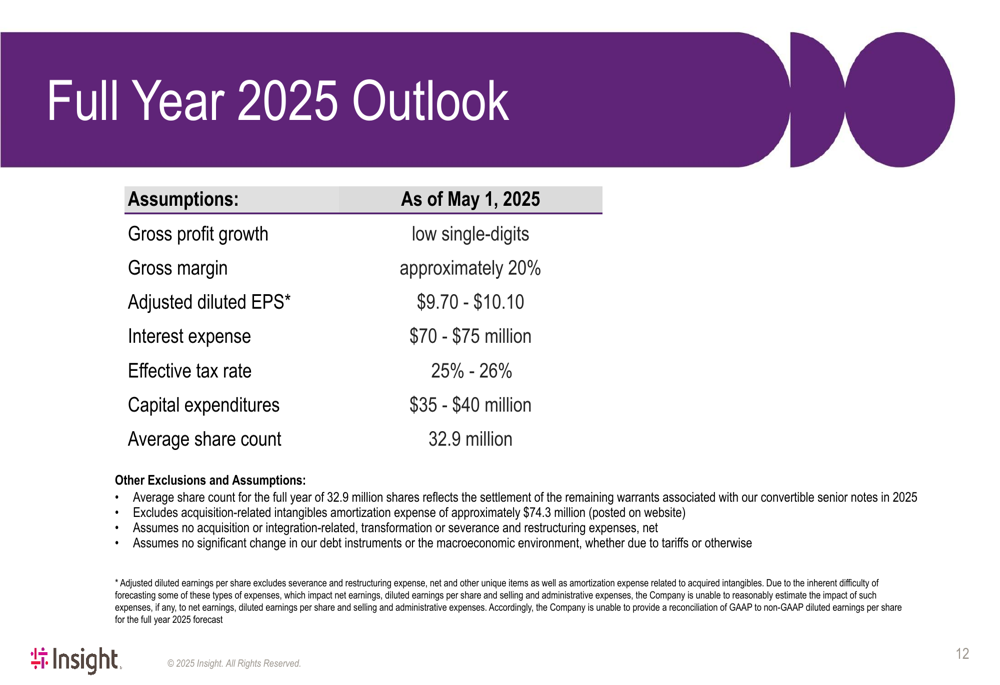

Looking ahead, Insight provided its outlook for the full year 2025, projecting low single-digit gross profit growth and a gross margin of approximately 20%. The company expects adjusted diluted EPS between $9.70 and $10.10.

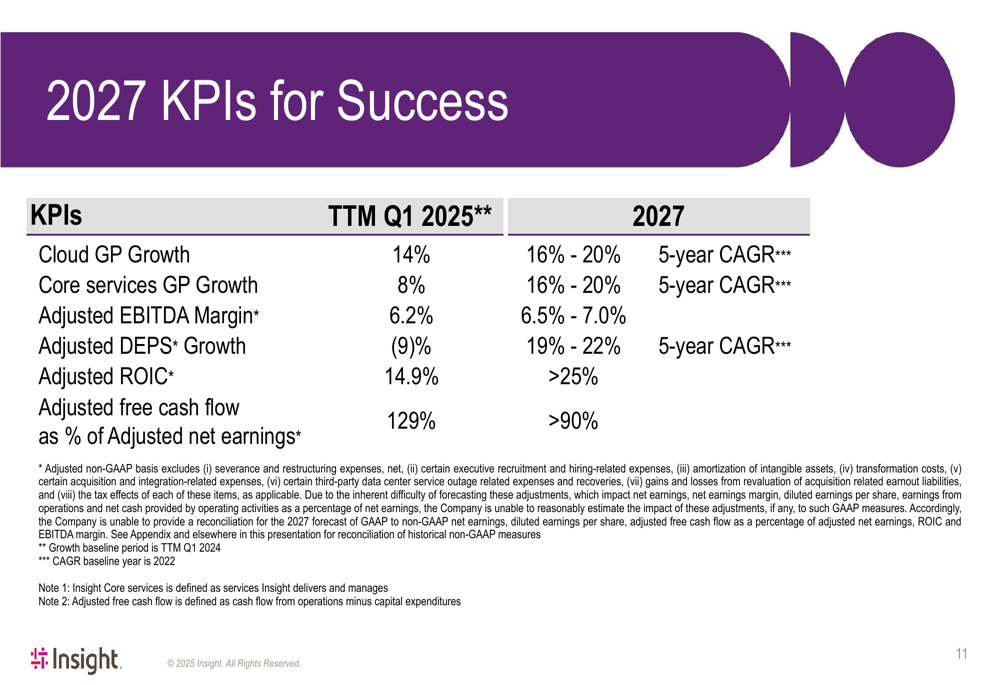

For the longer term, Insight outlined ambitious targets for 2027, including 16-20% compound annual growth rates for both cloud gross profit and core services gross profit, adjusted EBITDA margin of 6.5-7.0%, and adjusted diluted EPS growth of 19-22%.

However, there remains a significant gap between current performance and these long-term targets. For the trailing twelve months ending Q1 2025, cloud gross profit growth was 14% (vs. target of 16-20%), core services gross profit growth was 8% (vs. target of 16-20%), and adjusted diluted EPS growth was negative 9% (vs. target of 19-22%).

The continued challenges in IT spending, particularly in hardware and on-premises software, echo the trends reported in the company’s Q3 2024 results, suggesting that the recovery in these areas remains elusive. While Insight maintains its strategic focus on higher-margin cloud and services businesses, the near-term headwinds appear to be persisting longer than anticipated.

As Insight navigates these challenges, investors will be watching closely to see if the company can reverse the negative trends in revenue and earnings while continuing to make progress toward its ambitious 2027 targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.