Missed the webinar? Here are Investing.com’s top 10 stock picks for 2026

Introduction & Market Context

Insperity Inc (NYSE:NSP) presented its second quarter 2025 results on August 1, revealing a company navigating significant profitability challenges despite modest growth in its core business metrics. The human resources services provider reported a substantial decline in earnings while maintaining a slight increase in its worksite employee base, prompting a 1.37% drop in aftermarket trading following the announcement.

The company's stock, which has declined 43.6% over the past six months, continues to trade near its 52-week low of $44.14, reflecting ongoing investor concerns about profitability despite management's confidence in future growth prospects.

Quarterly Performance Highlights

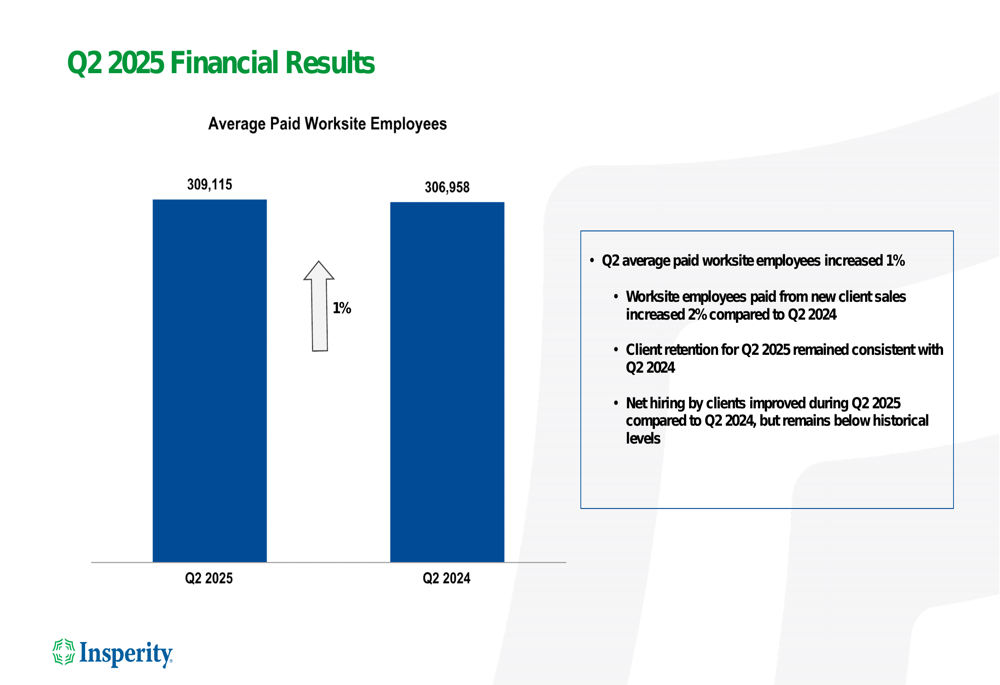

Insperity reported modest growth in its worksite employee base, a key operational metric for the company's PEO (Professional Employer Organization) business model. Average paid worksite employees increased to 309,115 in Q2 2025, representing a 1% year-over-year growth compared to 306,958 in Q2 2024.

As shown in the following chart of worksite employee growth:

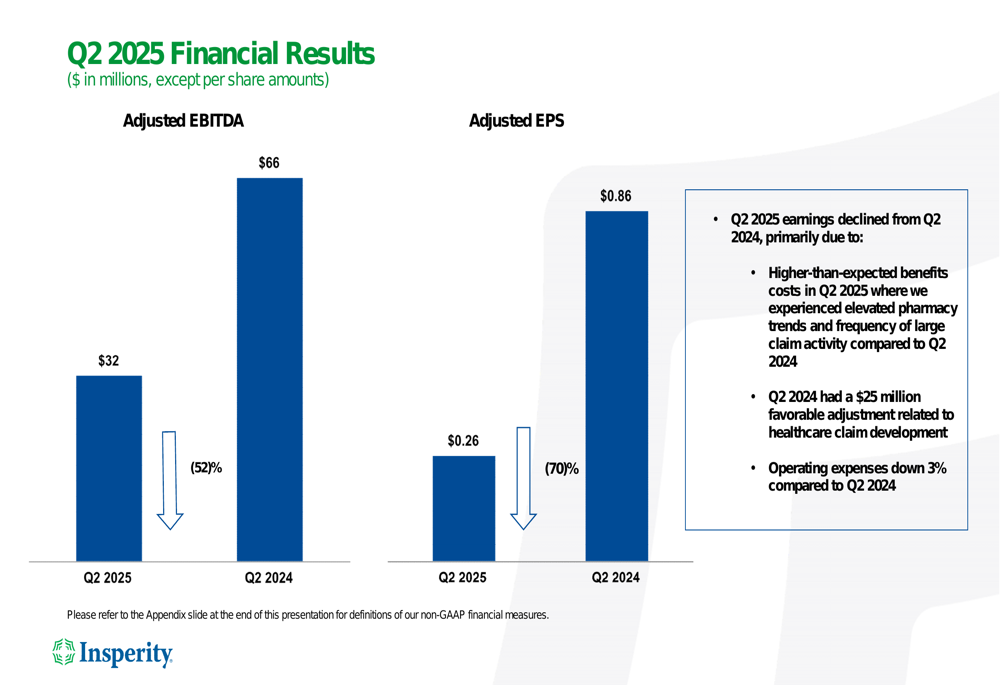

While worksite employee growth remained positive, the company's financial performance deteriorated significantly. Adjusted EBITDA fell 52% to $32 million in Q2 2025 from $66 million in the same period last year. Similarly, adjusted earnings per share dropped 70% to $0.26 from $0.86 in Q2 2024.

The following chart illustrates this substantial decline in profitability metrics:

Detailed Financial Analysis

The primary driver behind Insperity's earnings decline was higher-than-expected benefits costs. The company noted that in Q2 2024, it had recorded a $25 million favorable adjustment related to healthcare claim development, which created a challenging year-over-year comparison. Additionally, operating expenses decreased by 3% compared to Q2 2024, indicating management's efforts to control costs amid profitability pressures.

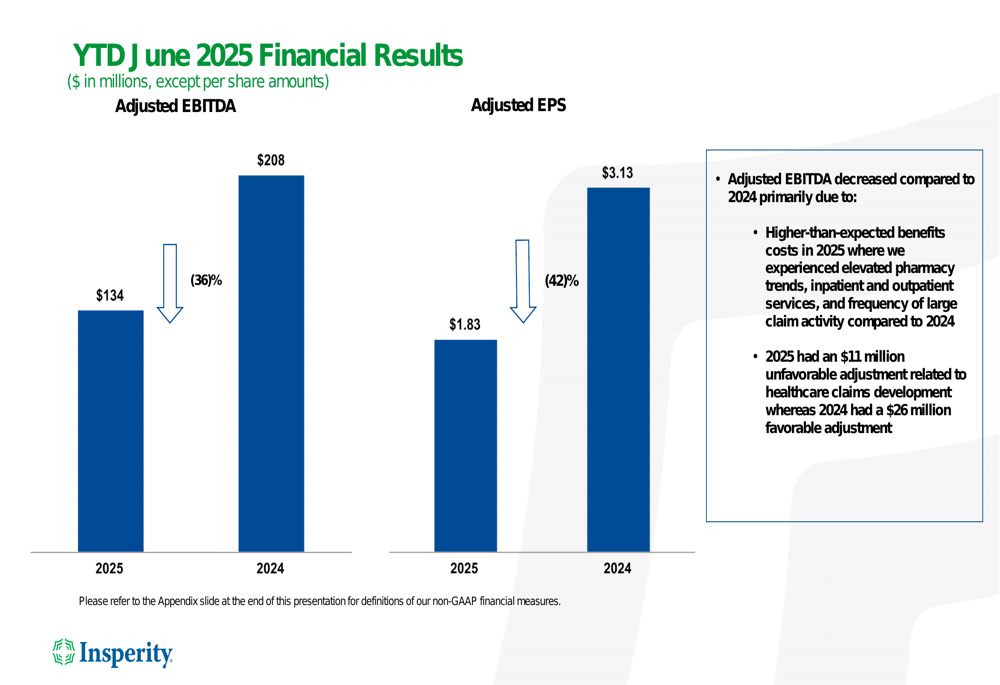

Year-to-date financial results through June 2025 showed similar trends, with worksite employees increasing by 1% while adjusted EBITDA fell 36% to $134 million from $208 million in the comparable period of 2024. Adjusted EPS for the first half of 2025 declined 42% to $1.83 from $3.13 in 2024.

The following chart details the year-to-date financial performance:

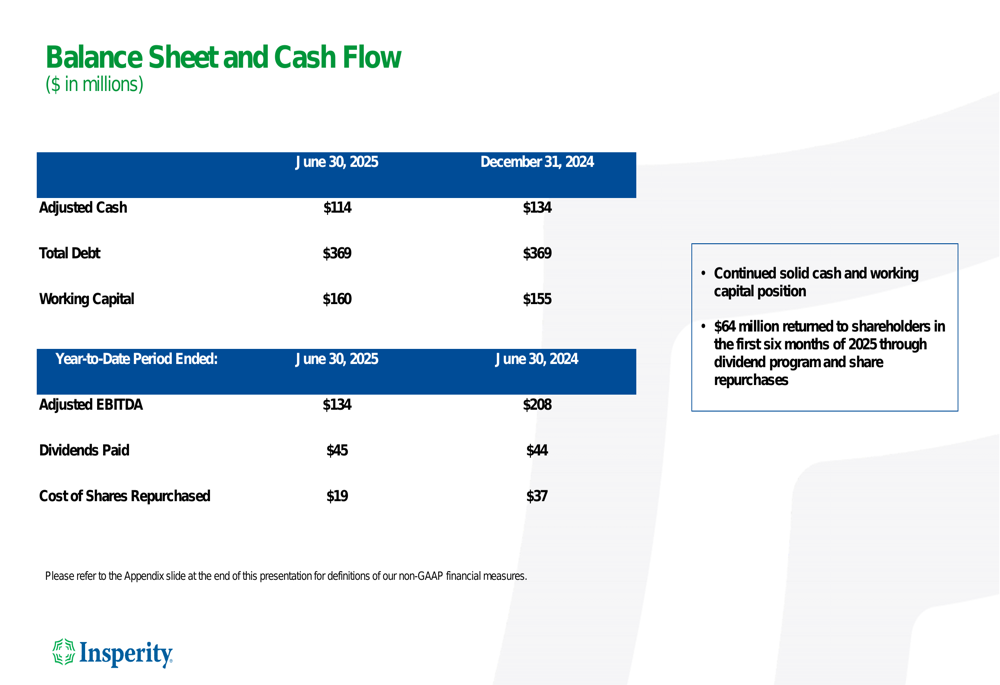

Despite earnings challenges, Insperity maintained a solid balance sheet with $114 million in adjusted cash and $160 million in working capital as of June 30, 2025. The company continued to prioritize shareholder returns, paying $45 million in dividends and repurchasing $19 million in shares during the first half of 2025.

The balance sheet and cash flow highlights are shown in the following slide:

Strategic Initiatives

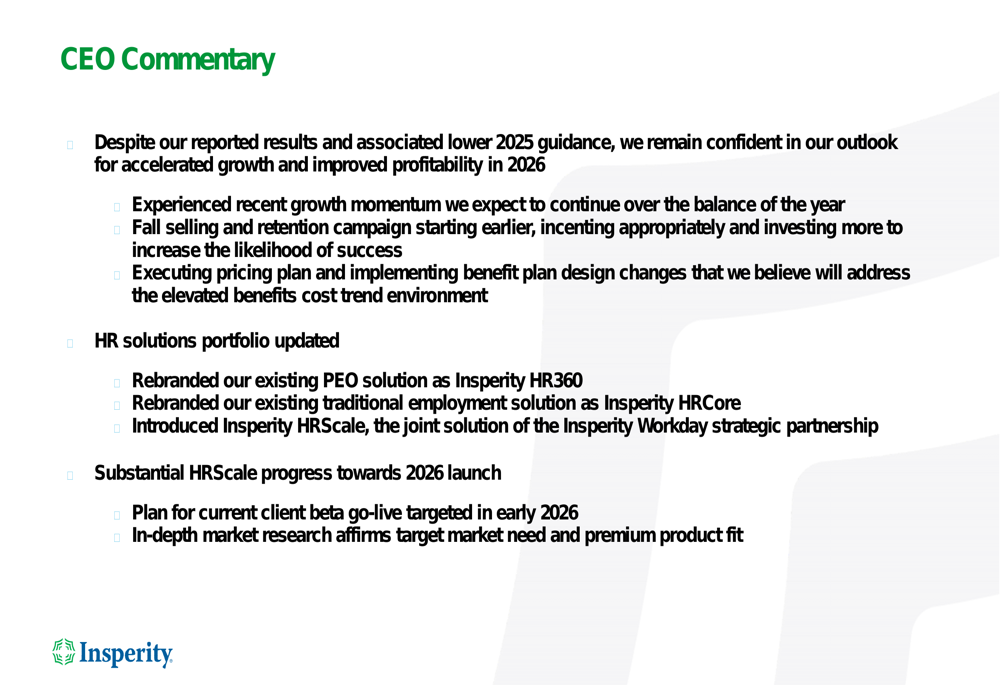

CEO Paul Sarvadi expressed confidence in the company's future trajectory despite near-term challenges. According to the CEO commentary slide, management remains focused on executing several strategic initiatives:

Key strategic priorities include executing the company's pricing plan to address benefits cost pressures, updating the HR solutions portfolio with rebrands of PEO and traditional employment solutions, and introducing Insperity HRScale. Management highlighted "substantial HRScale progress towards 2026 launch" and "positive market research" supporting these initiatives.

The company's partnership with Workday was also mentioned as a potential growth driver, though specific details about implementation timelines were not provided in the presentation.

Forward-Looking Statements

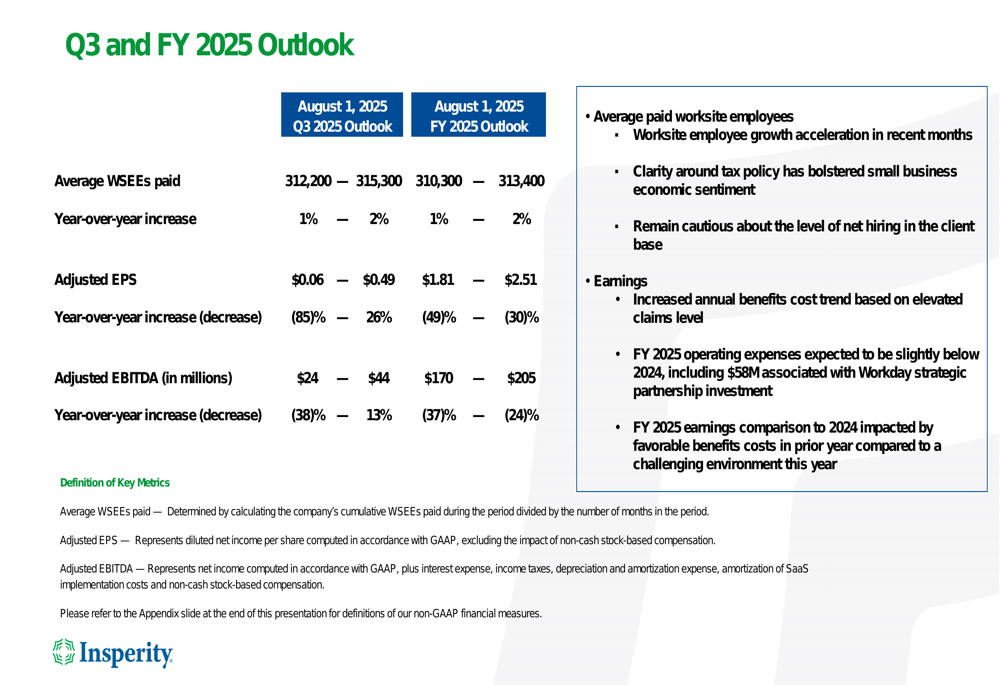

Insperity provided guidance for both Q3 and full-year 2025, projecting continued modest growth in worksite employees while acknowledging ongoing profitability challenges. For Q3 2025, the company expects average worksite employees to range between 312,200 and 315,300, representing a 1-2% year-over-year increase. Adjusted EPS is projected between $0.06 and $0.49, while adjusted EBITDA is expected to range from $24 million to $44 million.

For the full year 2025, Insperity forecasts average worksite employees between 310,300 and 313,400 (1-2% growth), adjusted EPS between $1.81 and $2.51, and adjusted EBITDA between $170 million and $205 million.

The following slide details the company's outlook:

While management expressed confidence in "accelerated growth and improved profitability in 2026," the near-term outlook suggests continued pressure on earnings as the company works to implement pricing adjustments and plan design changes to address benefits cost challenges.

The wide range in the earnings guidance reflects uncertainty about healthcare cost trends and the effectiveness of the company's mitigation strategies in the coming quarters. Investors will likely focus on the company's ability to execute its pricing plan and control benefits costs as key indicators of future performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.