Street Calls of the Week

Introduction & Executive Summary

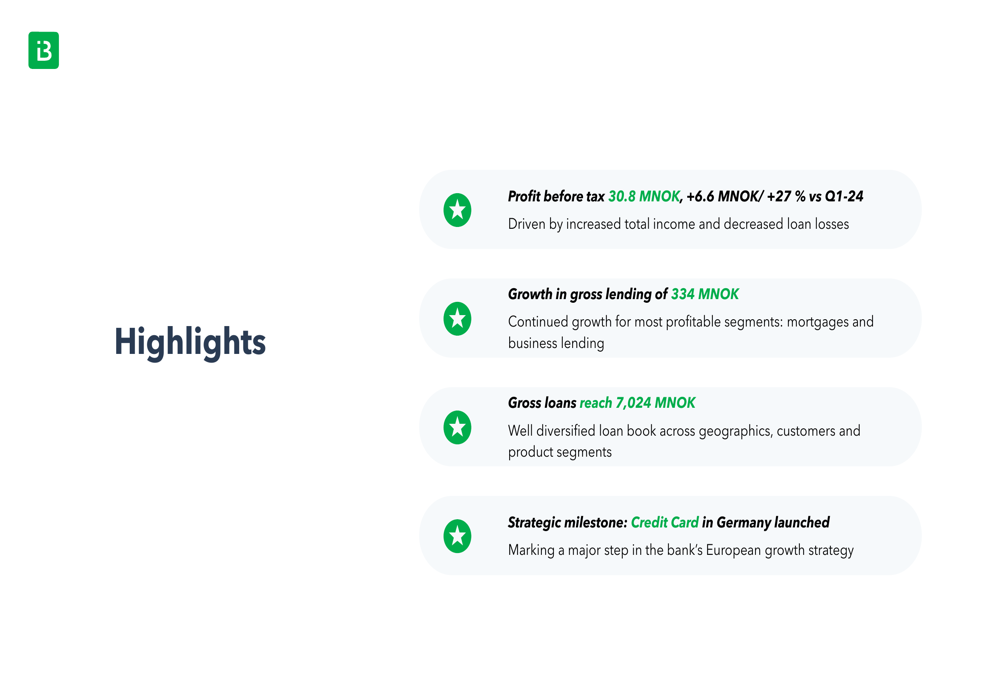

Instabank ASA (EURONEXT:INSTA) reported a strong start to 2025, with profit before tax increasing 27% year-over-year to 30.8 million Norwegian kroner (MNOK) in its Q1 2025 presentation. The Nordic challenger bank highlighted continued growth in its most profitable segments and marked a strategic milestone with the launch of a credit card offering in Germany.

The bank’s shares have responded positively to its consistent performance, currently trading at a 52-week high of 2.35 NOK, up 1.73% on the day of the presentation.

Quarterly Performance Highlights

Instabank’s Q1 2025 results demonstrated solid growth across key metrics. Profit before tax reached 30.8 MNOK, an increase of 6.6 MNOK or 27% compared to Q1 2024, driven by increased total income and decreased loan losses.

As shown in the following chart of quarterly highlights:

Total (EPA:TTEF) income for the quarter amounted to 134.5 MNOK, up by 18.0 MNOK from the same quarter last year. This growth was primarily driven by a 16.1 MNOK increase in total interest income, while interest expenses increased only marginally by 0.7 MNOK despite deposit volume growth of 521 MNOK.

The detailed breakdown of income growth is illustrated in this chart:

Operating expenses reached 62.1 MNOK, representing a modest increase of 0.9 MNOK from the previous quarter. These expenses were impacted by costs associated with the Finnish banking license application process and the new credit card offering in the German market. Despite these strategic investments, the bank maintained a healthy cost-to-income ratio between 41% and 48%.

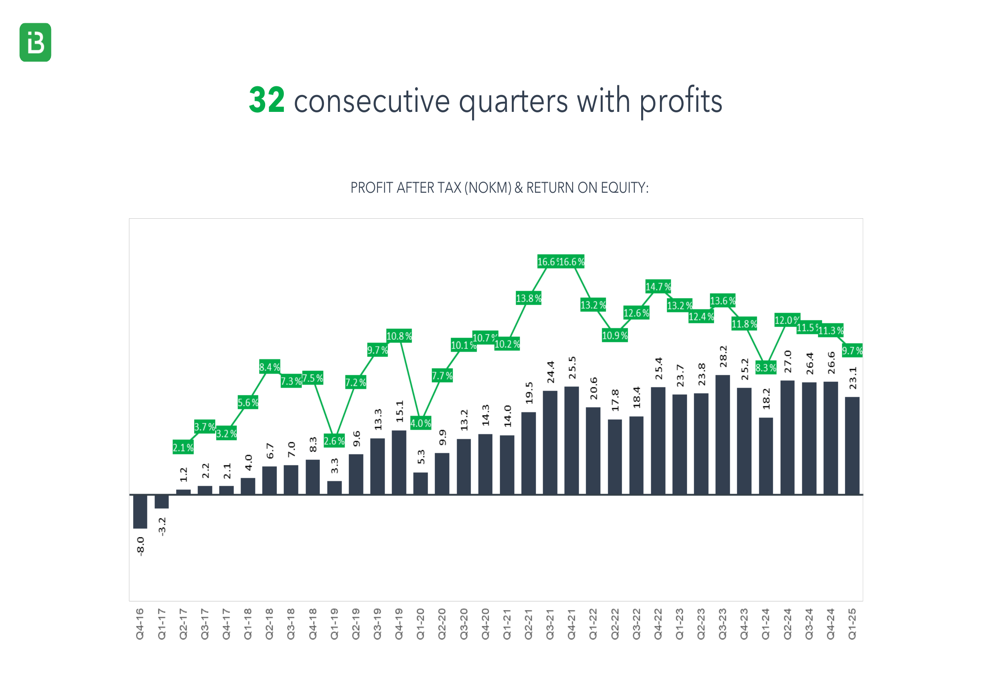

Notably, Instabank has now achieved 32 consecutive quarters of profitability, demonstrating consistent performance since its founding in 2016:

Loan Portfolio Diversification

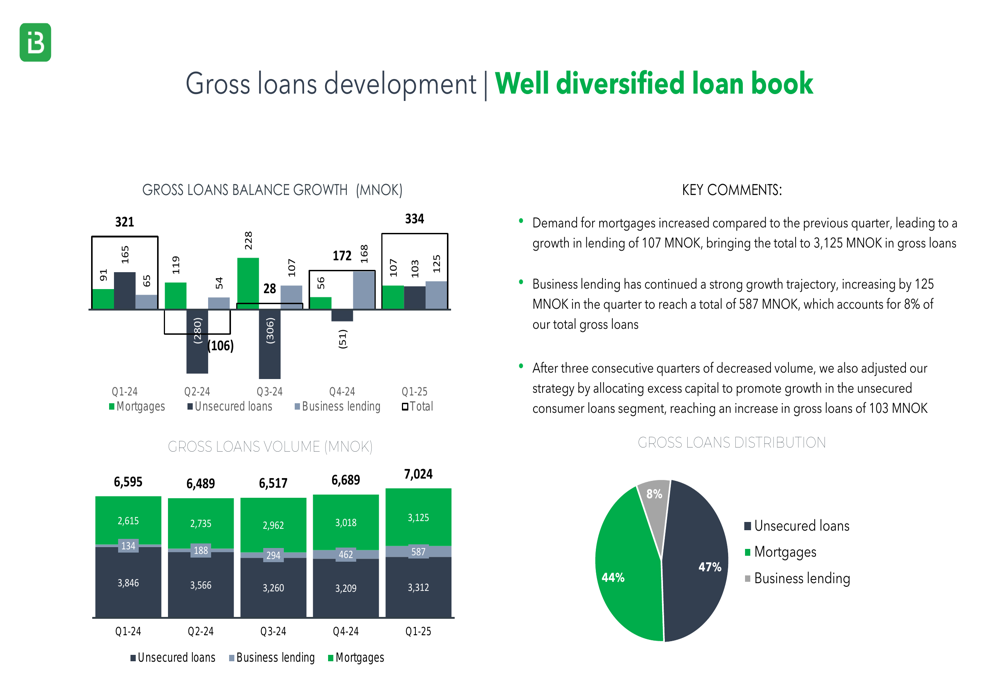

Gross loans reached 7,024 MNOK in Q1 2025, representing growth of 334 MNOK during the quarter. This growth accelerated from the 168 MNOK increase seen in Q4 2024, returning to levels similar to Q1 2024 when the bank added 321 MNOK in gross loans.

The loan portfolio is well-diversified across different segments, with unsecured loans representing 47%, mortgages 44%, and business lending 8% of the total portfolio. This distribution reflects the bank’s strategic shift toward lower-risk segments such as mortgages and business lending.

The following chart illustrates the growth and distribution of the loan portfolio:

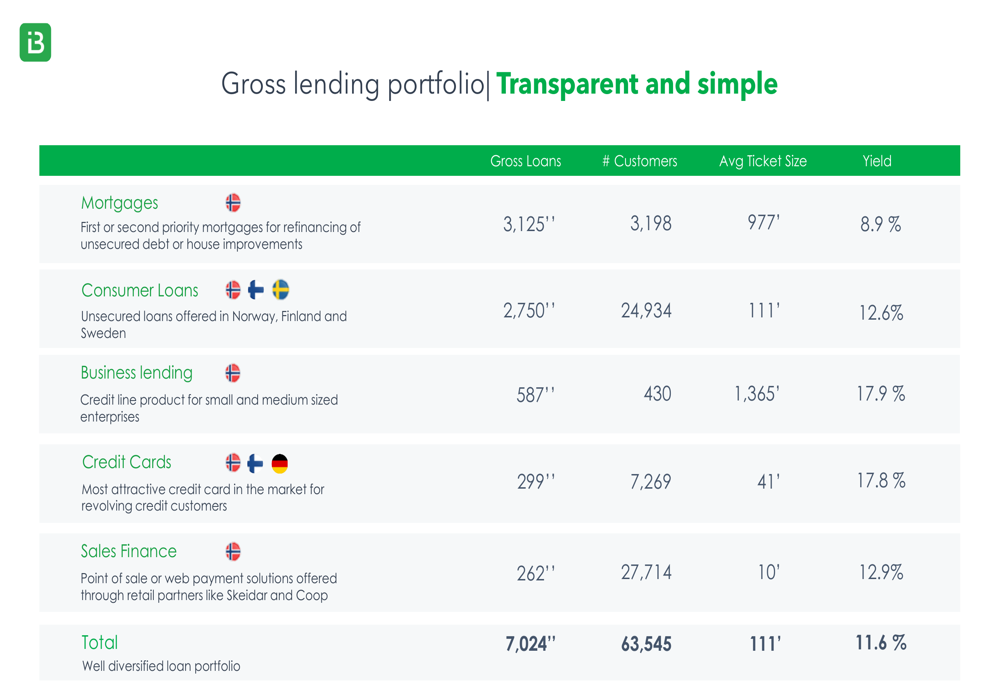

Instabank’s transparent approach to its lending portfolio provides clear visibility into each segment’s performance. The bank’s mortgages segment, which represents 44% of the portfolio, carries a lower yield of 8.9% but also represents significantly lower credit risk with a loan loss ratio under 1%. In contrast, business lending offers the highest yield at 17.9% while maintaining a manageable risk profile.

The detailed breakdown of the lending portfolio is shown here:

Loan losses amounted to 41.7 MNOK or 2.4% of the portfolio, down by 4.7 million NOK from the same quarter last year. This decrease in loan losses is attributed to the strategic shift in lending toward lower-risk segments such as mortgages and business lending.

Strategic Initiatives

Instabank’s European expansion strategy took a significant step forward with the launch of a fully digital credit card in Germany during Q1 2025. This launch represents a key milestone in the company’s European growth strategy, building on its Scandinavian values of trust, simplicity, and transparency.

The German credit card launch is detailed here:

Further expanding its European footprint, Instabank plans to submit a banking license application to the Finnish Financial Supervisory Authority during Q2 2025. The application process is expected to take approximately one year. The bank cited Finland’s regulatory stability and alignment with EU banking standards as key factors in this decision, noting that the Norwegian regulatory environment for niche banks is considered more restrictive and less stable than those in Sweden and Finland.

The Finnish banking license will support Instabank’s strategy of scaling across European markets, complementing its recent product launches in Germany and planned business lending expansion in Finland:

Instabank’s product strategy shows a clear evolution from a specialized consumer finance bank to a focused commercial bank. The timeline illustrates the bank’s methodical expansion across markets and product categories:

Financial Outlook and Guidance

Looking ahead, Instabank provided clear financial guidance for 2025 and mid-term strategic ambitions. For 2025, the bank expects profit after tax of approximately 125 million NOK, return on equity exceeding 12%, and gross loans of around 8.5 billion NOK.

The bank’s mid-term strategic ambitions are even more ambitious, targeting profit after tax exceeding 200 million NOK, return on equity above 15%, and gross loans exceeding 10 billion NOK.

These financial targets are summarized in the following guidance:

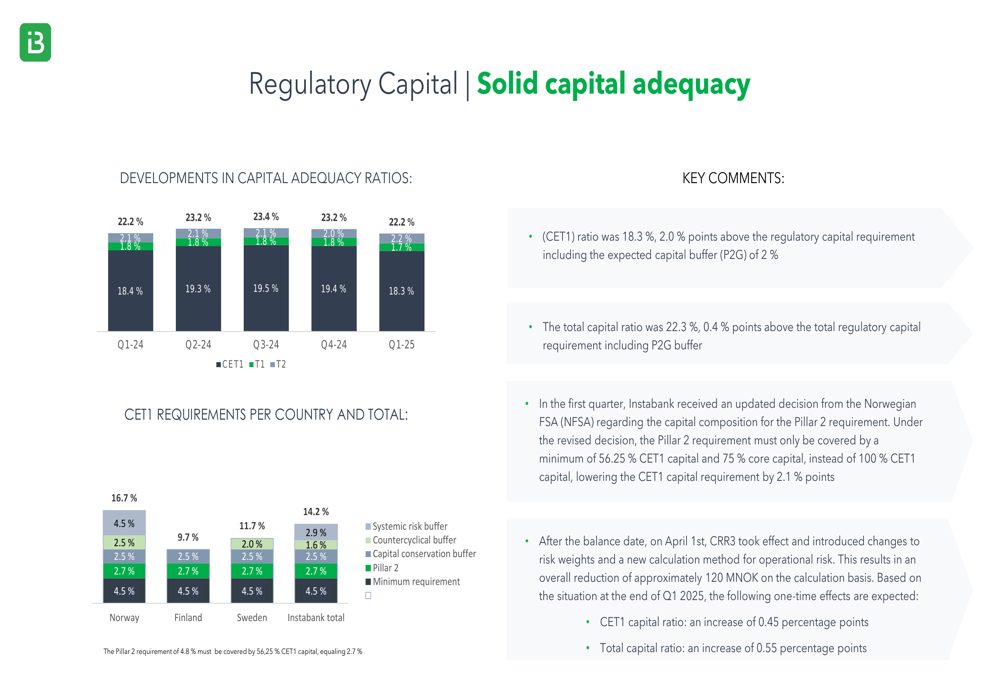

Instabank’s capital position remains solid, with a CET1 ratio of 18.3%, which is 2.0 percentage points above the regulatory capital requirement including the expected capital buffer of 2%. The total capital ratio was 22.3%, 0.4 percentage points above the total regulatory capital requirement including the P2G buffer.

In the first quarter, Instabank received an updated decision from the Norwegian Financial Supervisory Authority regarding the capital composition for the Pillar 2 requirement, further solidifying its regulatory standing.

With its consistent profitability, diversified loan portfolio, and clear strategic direction for European expansion, Instabank appears well-positioned to achieve its financial targets while continuing to build its presence as a Nordic challenger bank with growing European operations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.