Jamaica’s outlook revised to stable by Fitch after hurricane

Instalco Intressenter AB (STO:INSTAL) shares fell 7.32% following its Q3 2025 earnings presentation on October 24, as investors reacted to declining sales despite the company's strategic shift toward profitability over volume growth.

Quarterly Performance Highlights

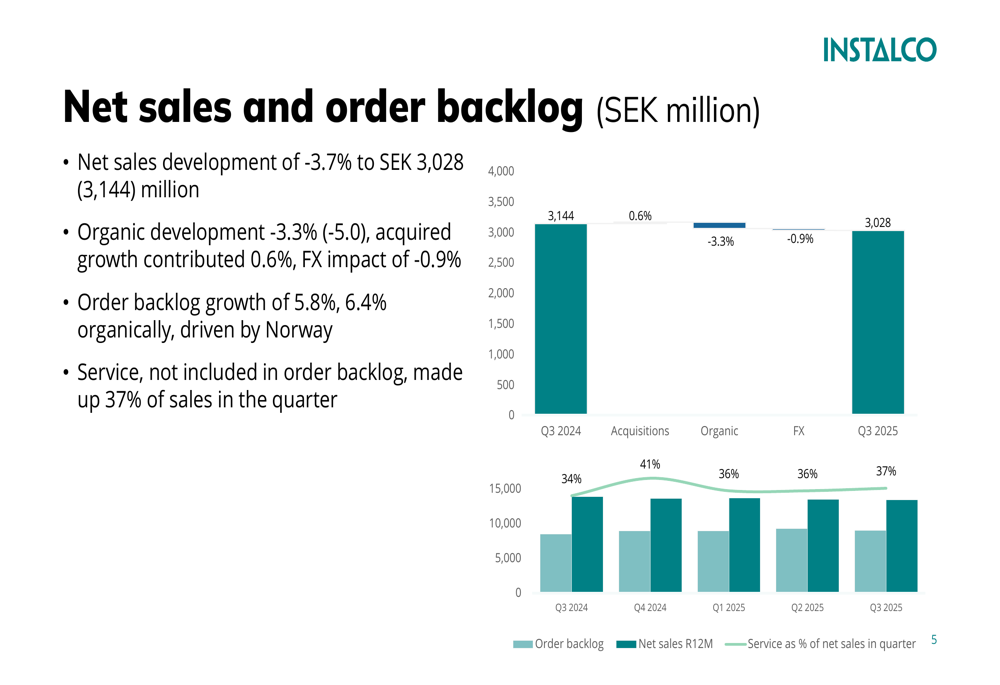

The Nordic installation services provider reported net sales of SEK 3,028 million for Q3 2025, down 3.7% compared to SEK 3,144 million in the same period last year. Organic development decreased by 3.3%, while acquired growth contributed just 0.6% and currency effects had a negative 0.9% impact.

"Financial development not being good enough," the company acknowledged in its quarterly summary, emphasizing that "margin improvement is the highest priority."

Despite the revenue decline, Instalco maintained its EBITA margin at 6.0%, generating EBITA of SEK 180 million compared to SEK 188 million in Q3 2024.

As shown in the following chart of net sales and order backlog:

Performance varied by region, with the Swedish segment showing particular weakness. Sweden, which accounts for approximately two-thirds of total revenue, saw net sales decline to SEK 2,060 million from SEK 2,166 million, with organic development down 5.7%. The segment's EBITA margin contracted to 5.1% from 5.5% in the prior year.

The Rest of Nordics segment demonstrated more resilience, with a slight sales decrease to SEK 968 million from SEK 978 million, but an improved EBITA margin of 7.7% compared to 6.9% in the previous year.

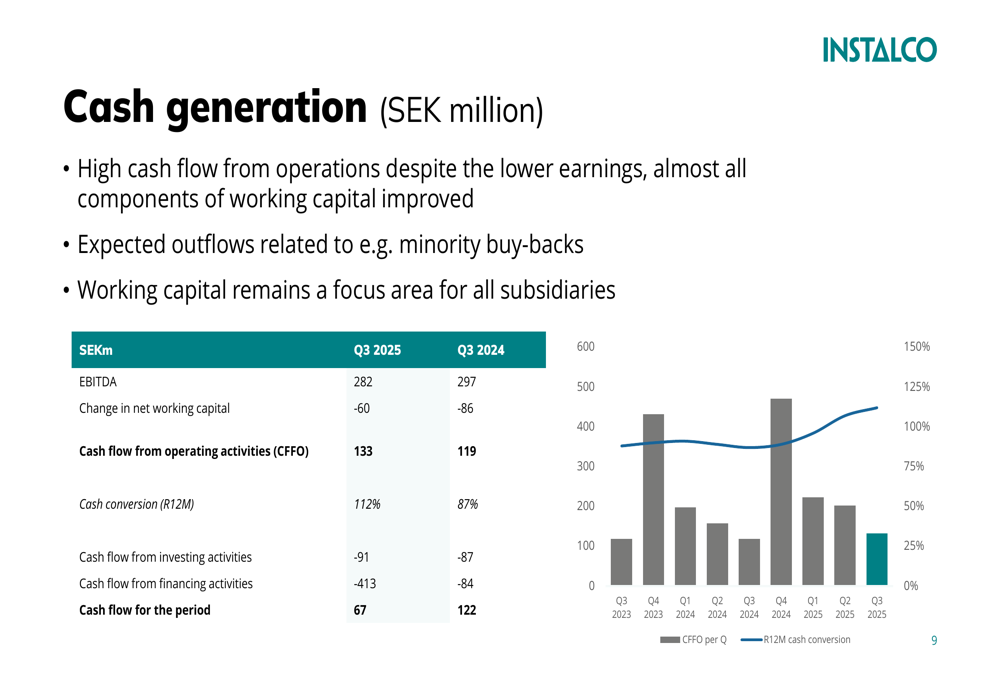

Cash Generation and Order Backlog

Despite lower earnings, Instalco reported strong cash flow from operations of SEK 133 million, up from SEK 119 million in Q3 2024, with improvements in nearly all working capital components. The company's cash conversion rate on a trailing twelve-month basis reached 112%, compared to 87% in the prior year.

The following chart illustrates Instalco's cash generation performance:

The company's order backlog grew by 5.8% to SEK 9,026 million, with organic growth of 6.4% primarily driven by Norway. Service components, which are not included in the order backlog, represented 37% of sales in the quarter.

Strategic Initiatives: Instalco 2.0

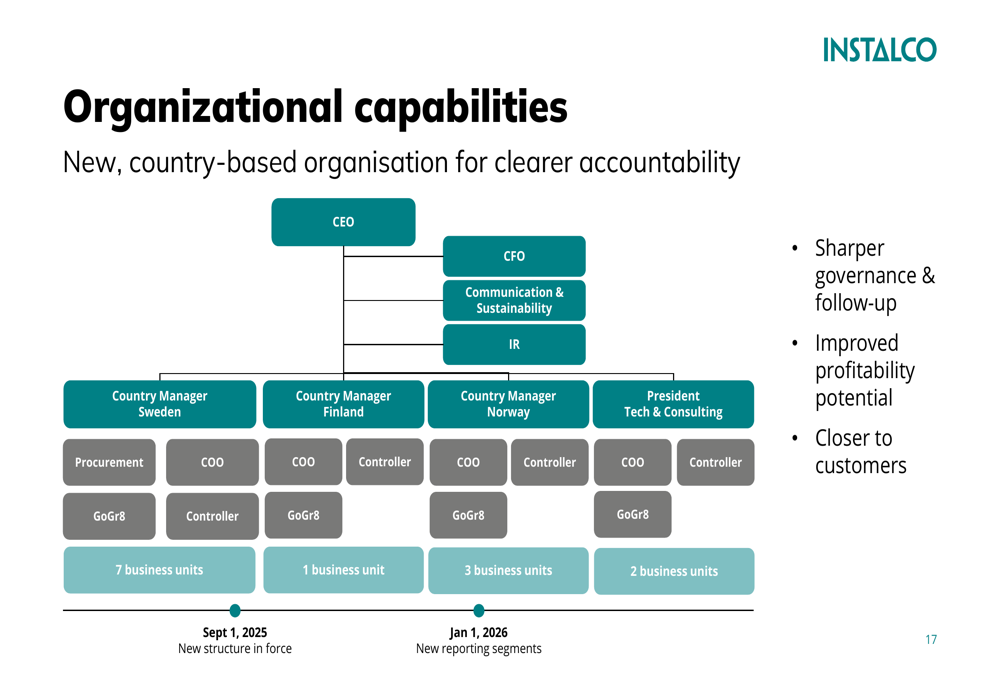

CEO Per Sjöstrand introduced "Instalco 2.0," a strategic initiative featuring a new country-based organizational structure implemented on September 1, 2025. The reorganization aims to create clearer accountability and improve profitability.

The new organizational structure is illustrated below:

"Margin is the No1 priority, closely followed by working capital management," the company emphasized in its presentation summary. This focus on profitability over volume reflects a strategic shift in response to challenging market conditions.

To improve margins, Instalco outlined a three-pronged approach:

The company is particularly focused on addressing underperforming business units through a structured framework that categorizes units based on operational excellence and financial results, providing tailored support where needed.

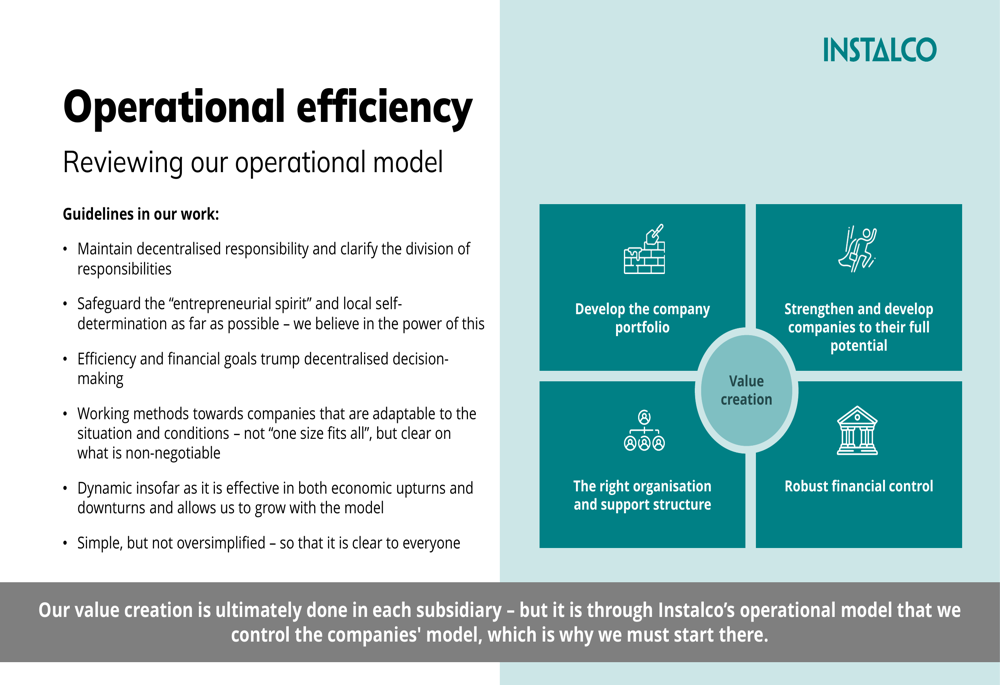

Operational Efficiency and Expansion

Instalco emphasized that while it maintains its decentralized approach and entrepreneurial spirit, it is implementing more disciplined financial controls and performance management.

The operational efficiency principles are shown below:

Meanwhile, the company continues to expand internationally. Its Fabri subsidiary announced three new acquisitions in Germany: I&H Elektrotechnik-Meisterbetrieb GmbH, Adolf Kindler GmbH, and Geuppert Elektrotechnik GmbH & Co.KG, with a combined 99 employees and estimated sales of EUR 18.7 million. This expands Fabri's German platform to 20 local companies.

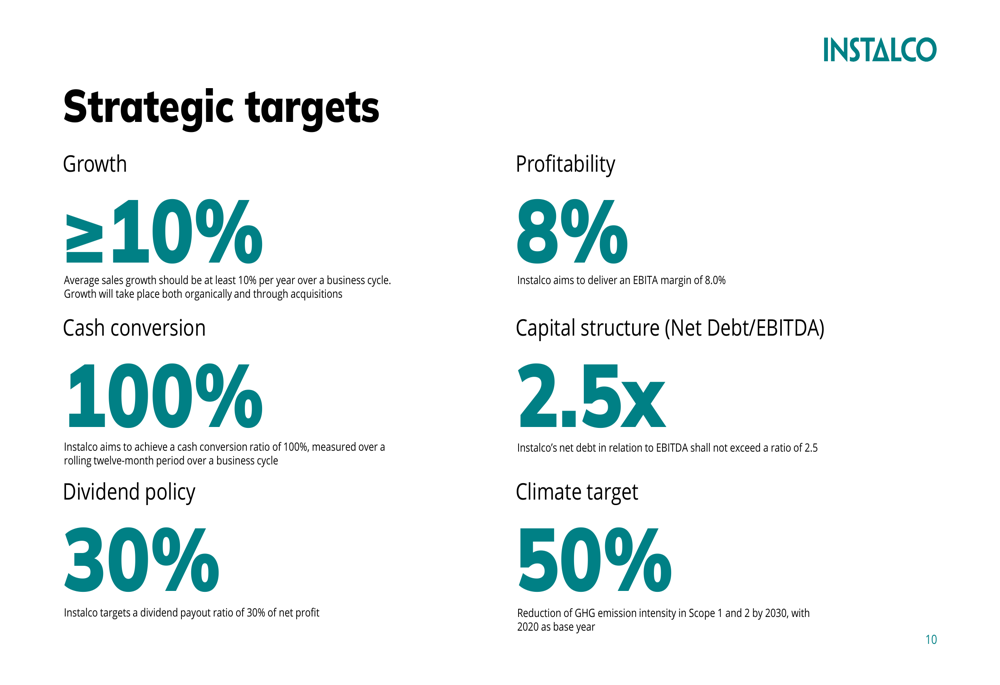

Outlook and Strategic Targets

Instalco maintains ambitious strategic targets despite current challenges, including growth of at least 10% per year over a business cycle, an EBITA margin of 8% (compared to the current 6.4% on a last twelve months basis), and a cash conversion target of 100%.

The company's strategic targets are outlined below:

"Seasonality and market pressure are visible in the numbers – market activity has picked up," noted the company, suggesting potential improvement ahead. However, the 7.32% drop in share price following the presentation indicates investor skepticism about the company's near-term prospects.

According to the earnings call transcript, Instalco expects market stabilization in 2026, with management focusing on operational excellence in the interim. The company trades at an EV/EBITDA of 13.3x and a P/E ratio of 24.5x, moderate multiples relative to peers, while maintaining impressive gross profit margins of 53%, significantly above industry averages.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.