S&P 500 falls on pressure from retail stocks, weak jobless claims

Introduction & Market Context

Insteel Industries Inc (NYSE:IIIN), the nation’s largest manufacturer of steel wire reinforcing products, presented its Q2 2025 investor update on April 17, 2025, revealing a significant earnings beat and strong demand recovery. The company reported earnings per share of $0.52, exceeding analyst expectations of $0.29 by 79.3%, while revenue reached $160.7 million, surpassing forecasts by 7.2%.

Following the earnings announcement, Insteel’s stock surged 13.8% to close at $30.41, reflecting investor optimism about the company’s performance and outlook. This positive market reaction came despite mixed signals from broader construction industry indicators.

Quarterly Performance Highlights

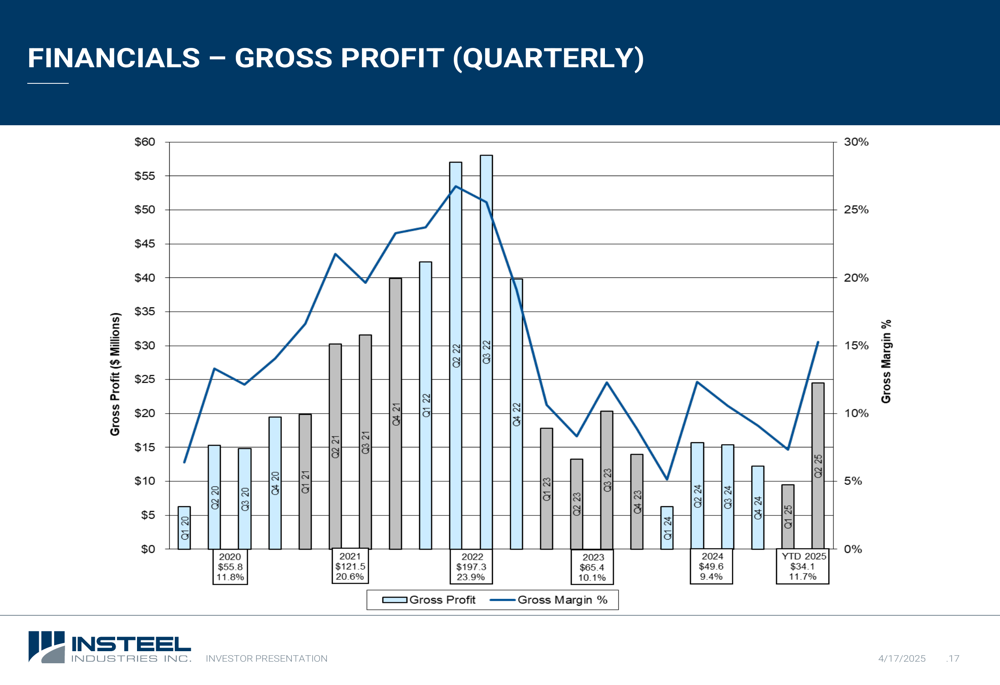

Insteel’s Q2 2025 performance marked a substantial improvement over the same period last year, with shipments increasing 28.9% year-over-year and 17.9% sequentially from Q1. The company’s gross margin expanded to 15.3% from 12.3% in the prior-year period, driven by higher sales volume and improved operational efficiencies.

During the earnings call, CEO H. Waltz expressed confidence in the company’s trajectory, stating, "We’re blowing and going." He emphasized that the current business conditions reflect "much more solid" underlying fundamentals compared to the post-COVID recovery period.

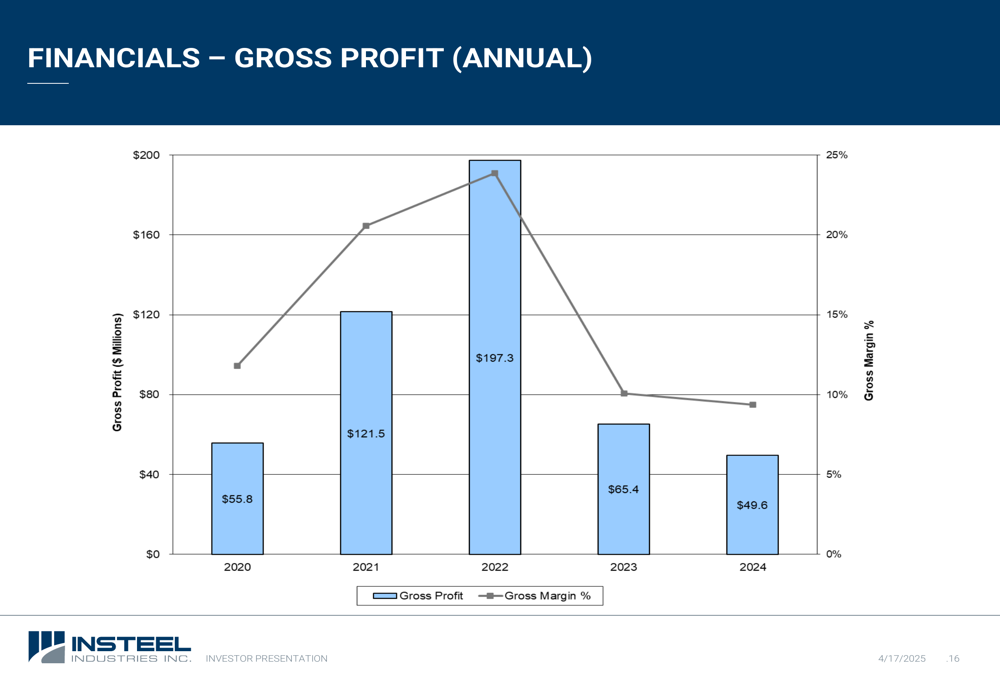

As shown in the following quarterly gross profit chart, Insteel has begun to reverse the margin compression experienced throughout 2023 and 2024:

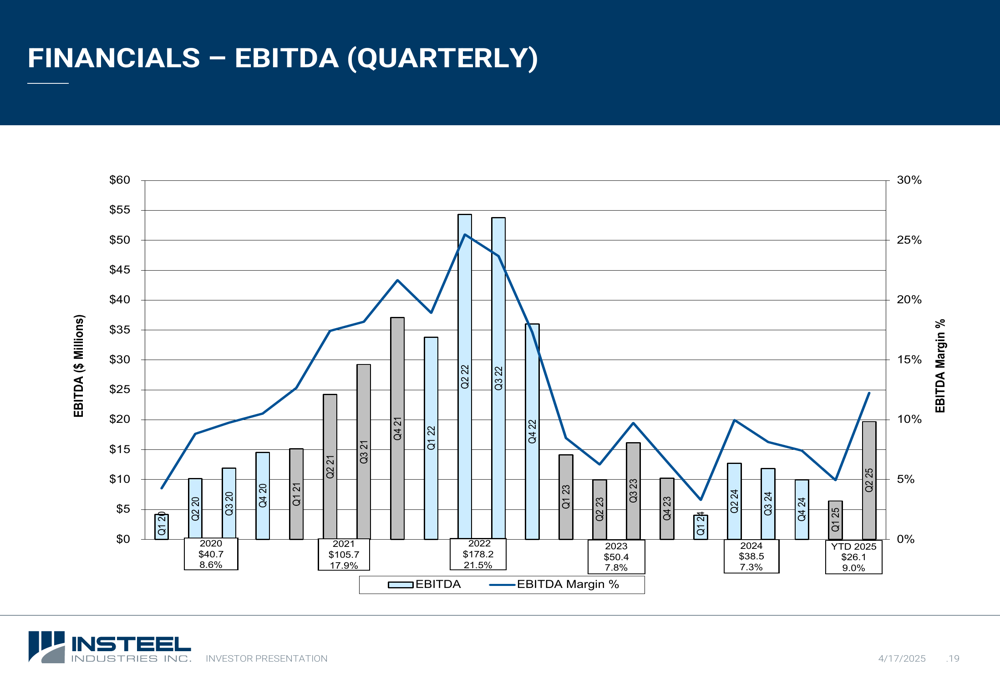

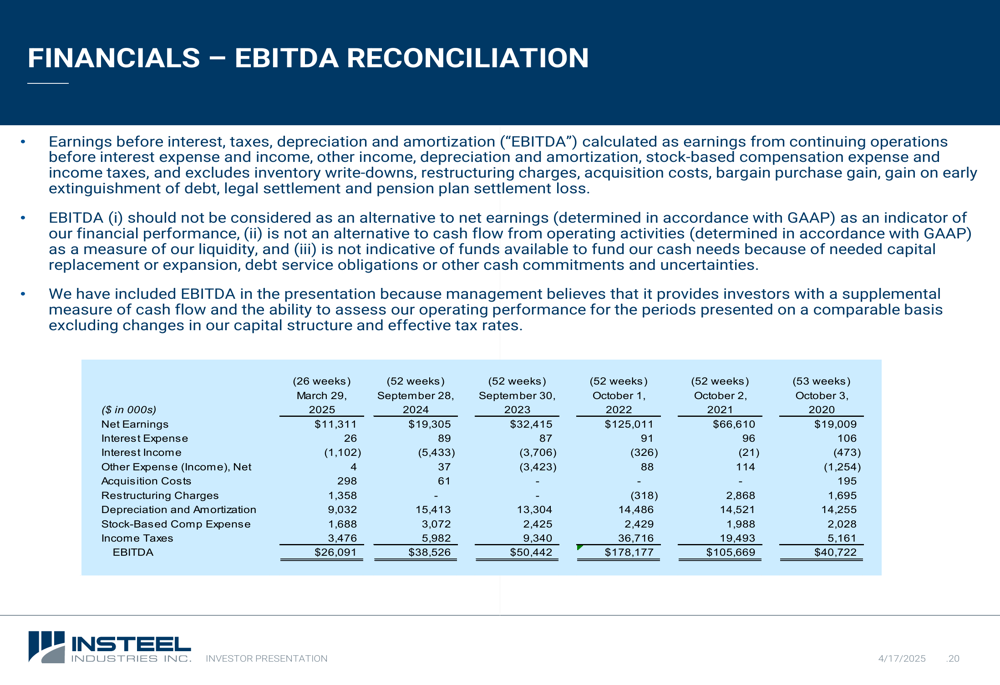

The company’s EBITDA has also shown signs of recovery in the first half of fiscal 2025, with year-to-date EBITDA margin improving to 9.0% from 7.3% for the full year 2024:

Business Overview & Strategic Position

Insteel Industries operates 11 manufacturing facilities across the United States, producing two main product lines: Welded Wire Reinforcement (WWR) and Prestressed Concrete Strand (PC Strand). In fiscal 2024, WWR accounted for 58% of sales, while PC Strand represented 42%.

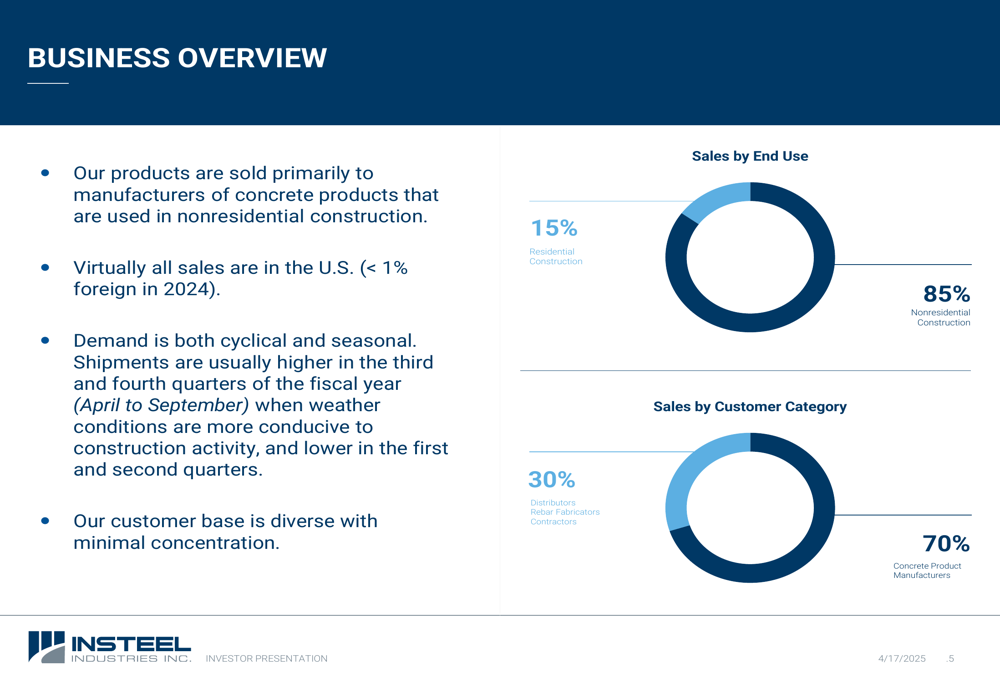

The company’s sales breakdown by end market and customer category provides insight into its market focus:

With 85% of sales coming from nonresidential construction and virtually all sales within the U.S. market, Insteel is heavily exposed to domestic infrastructure and commercial construction trends. The company’s customer base is diverse, with 70% of sales going to concrete product manufacturers and 30% to distributors, rebar fabricators, and contractors.

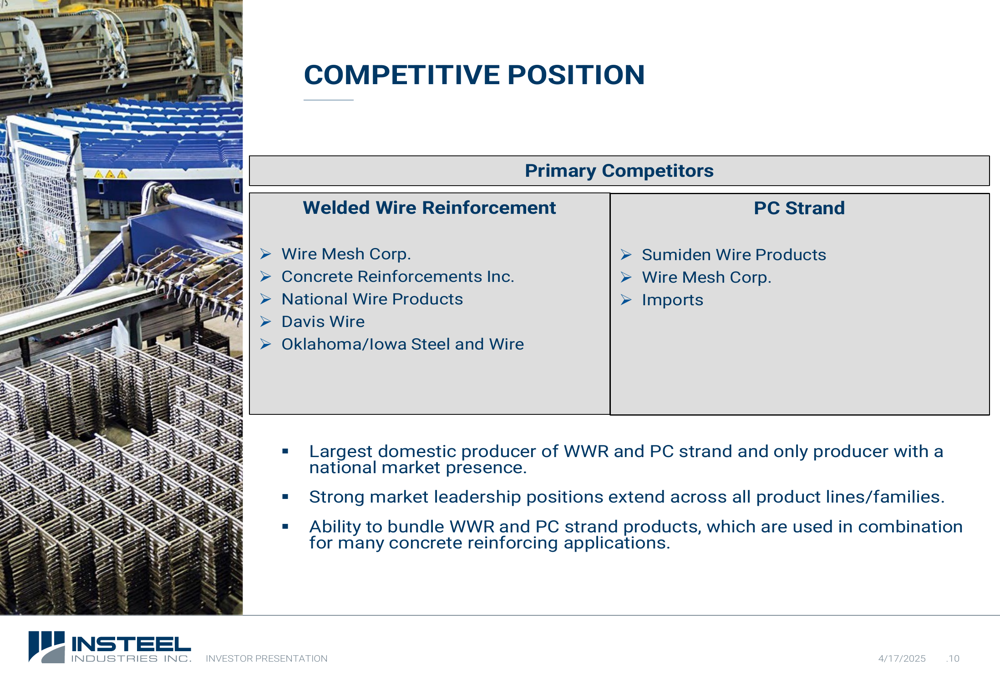

Insteel maintains a strong competitive position as the only producer with a national market presence in both WWR and PC Strand products:

Growth Strategy & Recent Acquisitions

A key element of Insteel’s growth strategy is the conversion of rebar users to Engineered Structural Mesh (ESM) for cast-in-place applications. This approach leverages the company’s manufacturing and engineering capabilities while providing cost savings and accelerating the construction process for customers.

The company has also been active in strategic acquisitions, with recent additions including Engineered Wire Products and O’Brien Wire Products in late 2024:

During the earnings call, Waltz noted that the integration of these acquisitions is "complete and successful," with operational and freight synergies already being realized. The Upper Sandusky, Ohio facility, acquired as part of these transactions, was specifically highlighted for its positive contribution.

Financial Performance & Outlook

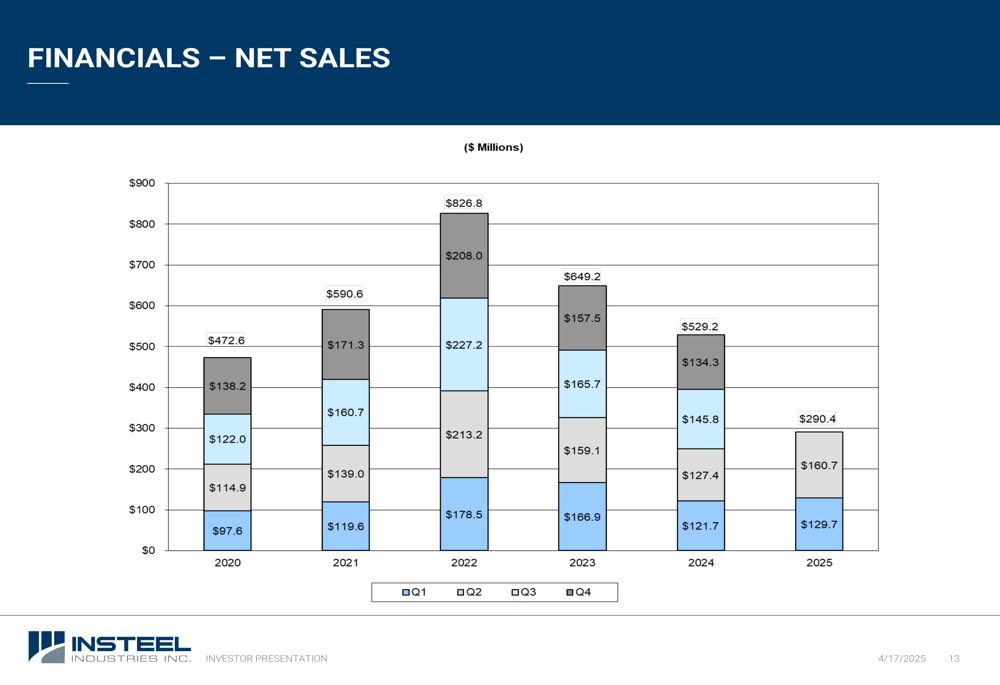

Insteel’s financial performance has shown volatility over recent years, with net sales peaking at $826.8 million in 2022 before declining to $529.2 million in 2024. However, Q1 and Q2 2025 results suggest a recovery is underway:

The company’s gross profit and margins have followed a similar pattern, with a significant compression from the peak levels of 2022:

A detailed reconciliation of EBITDA provides further insight into the company’s profitability drivers:

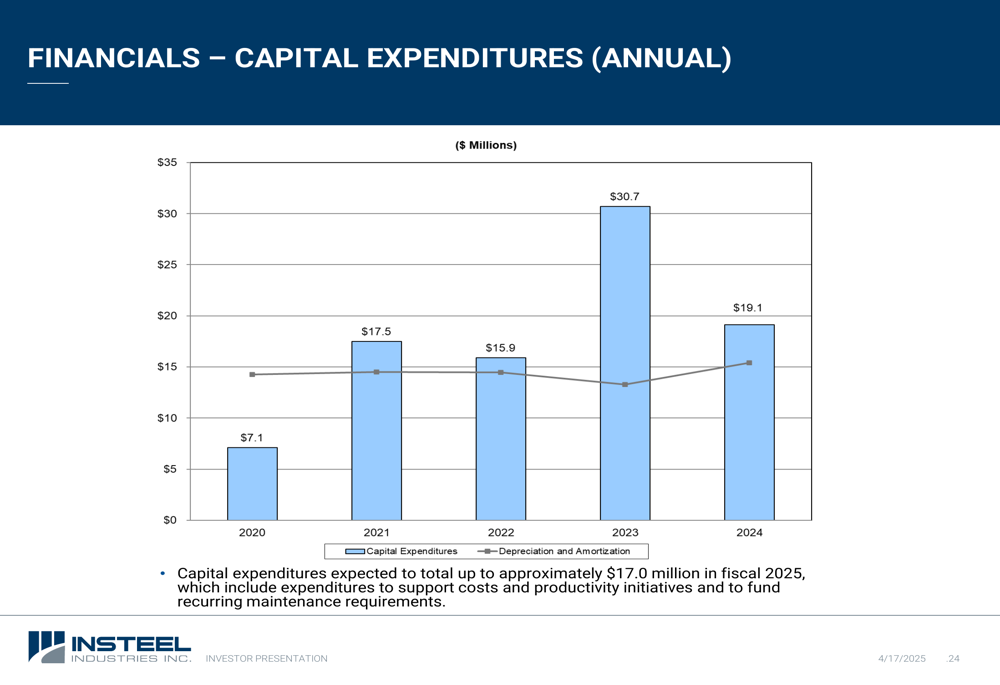

As of March 29, 2025, Insteel maintained a strong balance sheet with no debt and $28.4 million in cash. The company has revised its capital expenditure forecast for fiscal 2025 downward to $17 million from the previously communicated $22 million, reflecting resources devoted to acquisitions and integration activities rather than project cancellations.

Market Outlook & Tariff Impact

A significant positive development for Insteel has been the expansion of the Section 232 steel tariff to derivative products, including PC Strand. This change eliminates what the company described as a "significant competitive disadvantage" it has faced since 2018, when tariffs were applied to its raw materials but not to imported finished products.

During the earnings call, Waltz emphasized that while this tariff expansion is beneficial, it’s "not a panacea" since the world market price of hot-rolled steel remains $300-400 per ton lower than U.S. prices. Nevertheless, it makes Insteel’s competitive position more tenable in markets affected by imports, which represent approximately 10% of the company’s revenues.

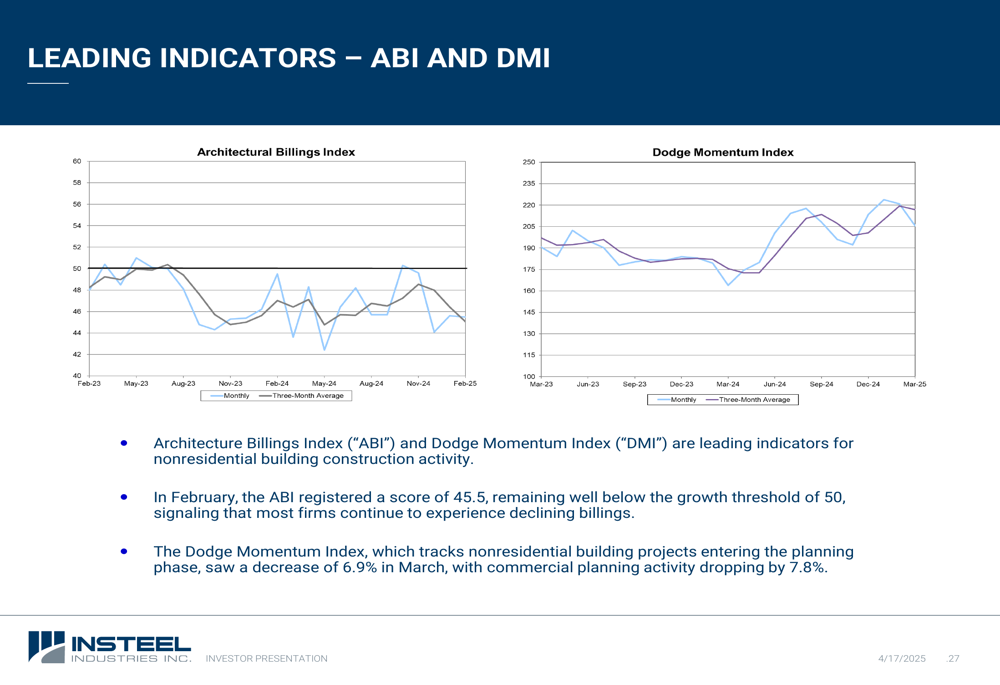

Looking ahead, Insteel remains cautiously optimistic about market conditions through the end of fiscal 2025, despite concerning signals from leading indicators. The Architectural Billings Index registered 45.5 in February, remaining below the growth threshold of 50, while the Dodge Momentum Index decreased 6.9% in March:

Investment Considerations

Insteel highlighted several factors that support its investment case, including strong cash flow generation, national market presence, financial flexibility, and experienced management:

Key challenges facing the company include supply chain constraints, with Waltz noting "serious concerns about adequate domestic supplies of wire rod going forward." This has led Insteel to commit to importing substantial quantities of raw materials despite the inherent risks of longer lead times.

The company also faces ongoing uncertainties related to tariff policies and their potential impact on the U.S. economy. Labor market challenges continue to affect operational capacity, with Waltz mentioning difficulties in hiring personnel to support increased production hours.

Despite these challenges, Insteel’s strong Q2 2025 performance and improving market conditions suggest the company is well-positioned to capitalize on infrastructure spending and construction activity in the coming quarters, particularly with its strengthened competitive position following recent acquisitions and favorable tariff developments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.