Missed the webinar? Here are Investing.com’s top 10 stock picks for 2026

Introduction & Market Context

Intact Financial Corporation (TSX:IFC) presented its second quarter 2025 results on July 30, highlighting solid performance across most business segments despite facing challenges in specific markets. The company's stock closed at $259.41 following the presentation, representing a modest 0.86% increase, as investors responded positively to the company's continued operational strength and strategic initiatives.

The presentation, led by CEO Charles Brindamour and CFO Ken Anderson, showcased Intact's resilience in a competitive insurance landscape, with performance metrics generally exceeding industry averages. The company continues to outperform the broader insurance sector, maintaining its position as a market leader in Canada while strategically expanding its global footprint.

Quarterly Performance Highlights

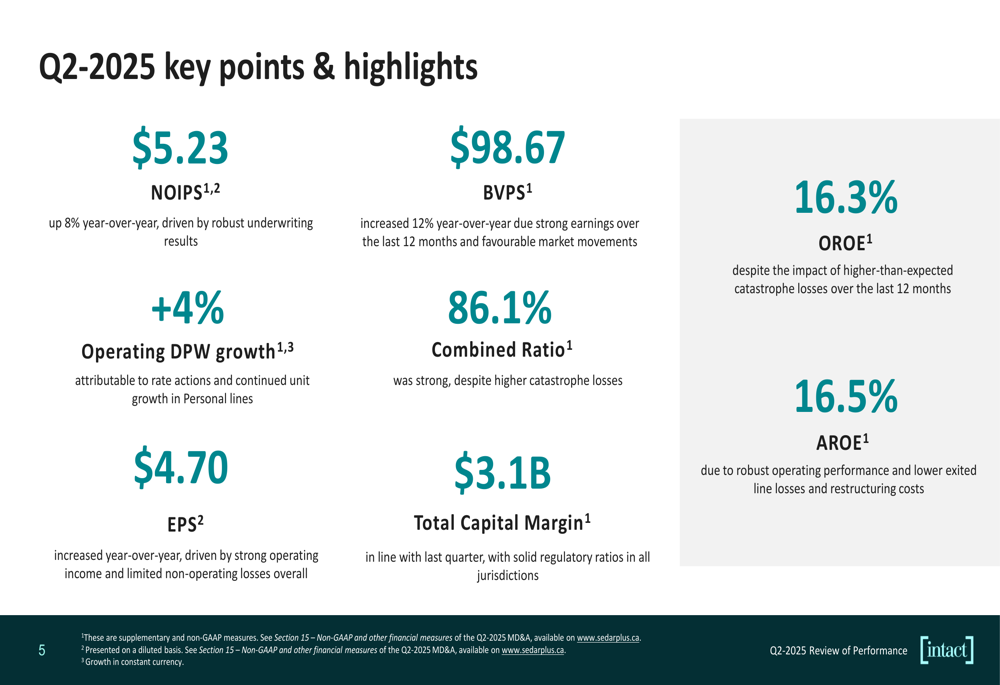

Intact delivered strong financial results for Q2 2025, with net operating income per share (NOIPS) reaching $5.23, an 8% increase year-over-year. The company's book value per share (BVPS) grew impressively by 12% year-over-year to $98.67, reflecting solid capital generation.

The insurer reported an operating return on equity (OROE) of 16.3% and an all-in return on equity (AROE) of 16.5%, both significantly outperforming industry averages. Overall operating direct premium written (DPW) growth was 4%, while the company achieved a strong combined ratio of 86.1%, improving by 1 percentage point compared to the same period last year.

As shown in the following key financial metrics summary:

Segment Performance Analysis

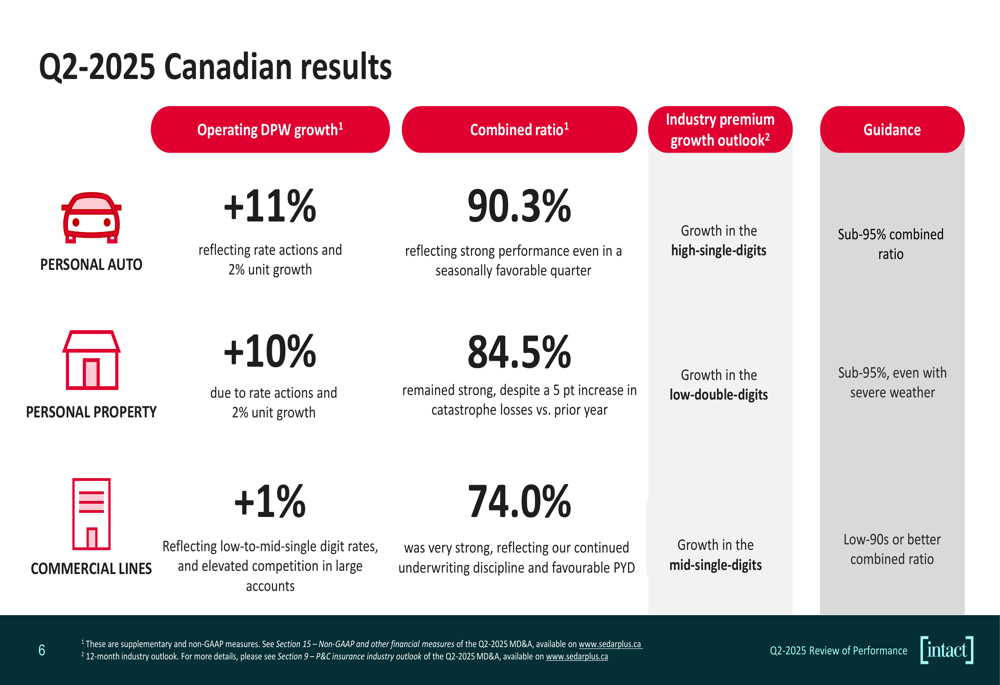

Intact's Canadian operations delivered mixed but generally strong results. Personal Auto showed robust growth with operating DPW increasing by 11% and a combined ratio of 90.3%. Personal Property similarly performed well with 10% DPW growth and an 84.5% combined ratio. Commercial Lines, while posting a stellar 74.0% combined ratio, saw more modest growth at just 1%, reflecting some of the challenges mentioned in the earnings call regarding softening in this segment.

The Canadian segment performance breakdown illustrates these trends:

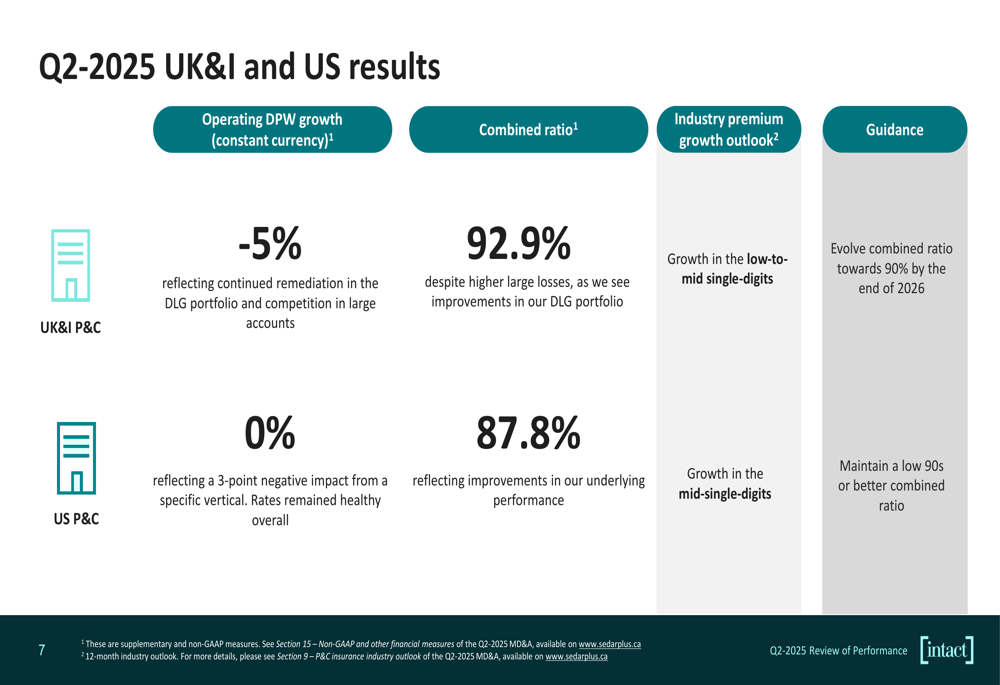

The company's international operations presented more challenges. The UK and Ireland segment experienced a 5% decline in operating DPW at constant currency, though it maintained a reasonable 92.9% combined ratio. The US P&C business showed flat premium growth (0%) but delivered a solid combined ratio of 87.8%. Management indicated plans to evolve the UK&I combined ratio towards 90% by the end of 2026, while maintaining a low-90s or better ratio in the US.

The international segment performance is detailed in the following chart:

Strategic Initiatives

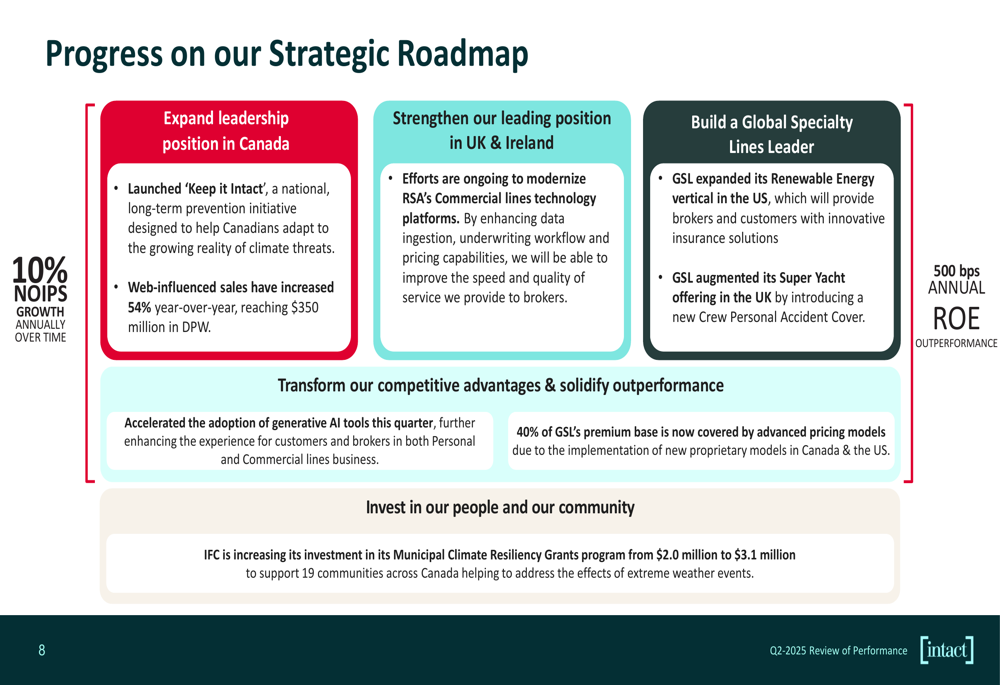

Intact outlined significant progress on its strategic roadmap, focusing on three key pillars: expanding leadership in Canada, strengthening its position in the UK & Ireland, and building a Global Specialty Lines (GSL) leader. The company launched "Keep it Intact," a customer retention initiative, while modernizing RSA's Commercial lines technology platforms.

In the specialty segment, Intact expanded its Renewable Energy vertical in the US market and implemented advanced pricing models across 40% of GSL's premium base. The company also increased its investment in the Municipal Climate Resiliency Grants program from $2.0 million to $3.1 million, reinforcing its commitment to sustainability.

These strategic initiatives align with Intact's long-term targets of 10% annual NOIPS growth and 500 basis points of annual ROE outperformance, as illustrated in the strategic roadmap:

Detailed Financial Analysis

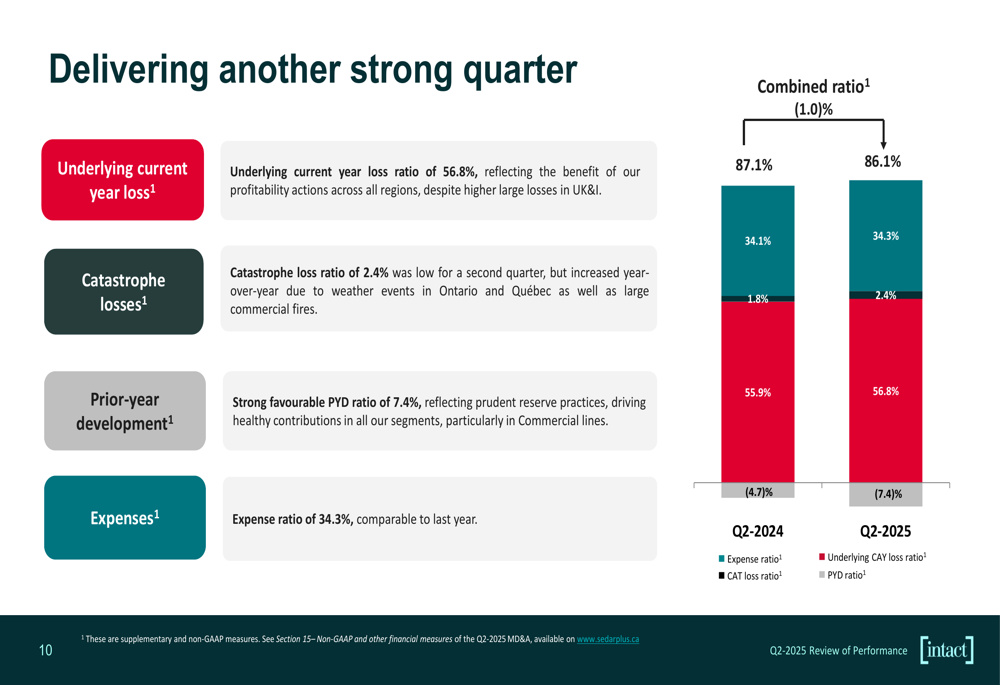

The presentation provided a comprehensive breakdown of underwriting performance factors. Intact's combined ratio improved to 86.1% in Q2 2025 from 87.1% in Q2 2024. This improvement came despite a slight increase in the catastrophe loss ratio (2.4% vs 1.8%) and underlying current year loss ratio (56.8% vs 55.9%). The positive variance was largely driven by favorable prior-year development, which contributed 7.4% in Q2 2025 compared to 4.7% in the same period last year.

The expense ratio remained relatively stable at 34.3%, compared to 34.1% in Q2 2024, demonstrating the company's continued operational efficiency despite inflationary pressures.

The following chart illustrates the components of Intact's combined ratio performance:

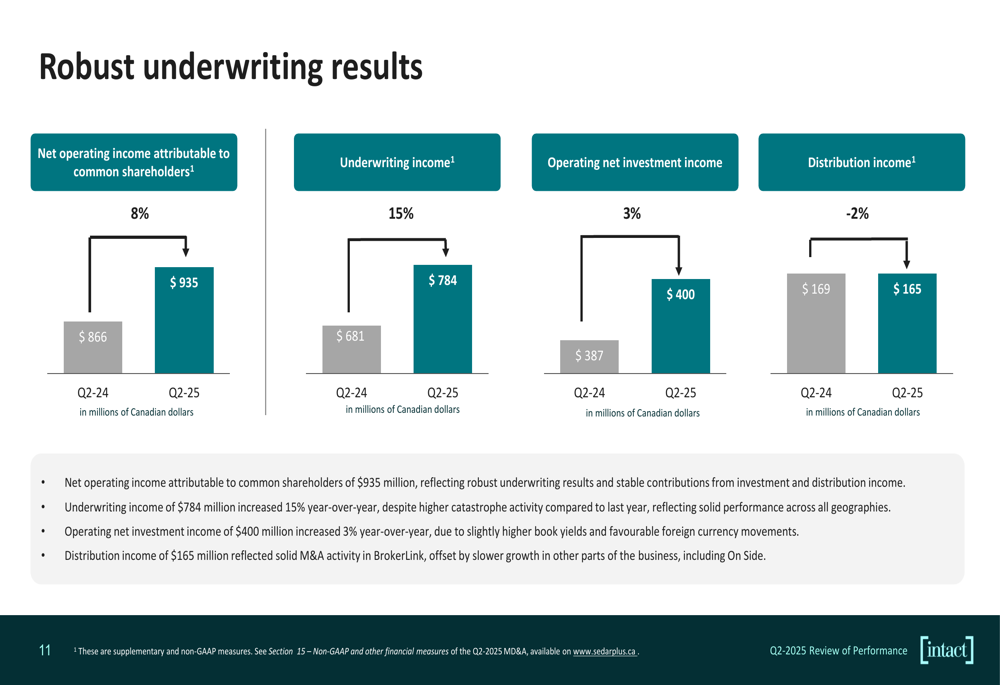

Net operating income attributable to common shareholders increased from $866 million in Q2 2024 to $935 million in Q2 2025, representing an 8% improvement. This growth was primarily driven by stronger underwriting income, which rose from $681 million to $784 million. Operating net investment income also saw modest growth from $387 million to $400 million.

Distribution income, however, declined slightly from $169 million to $165 million, confirming the challenges in this segment mentioned during the earnings call.

Financial Position & Outlook

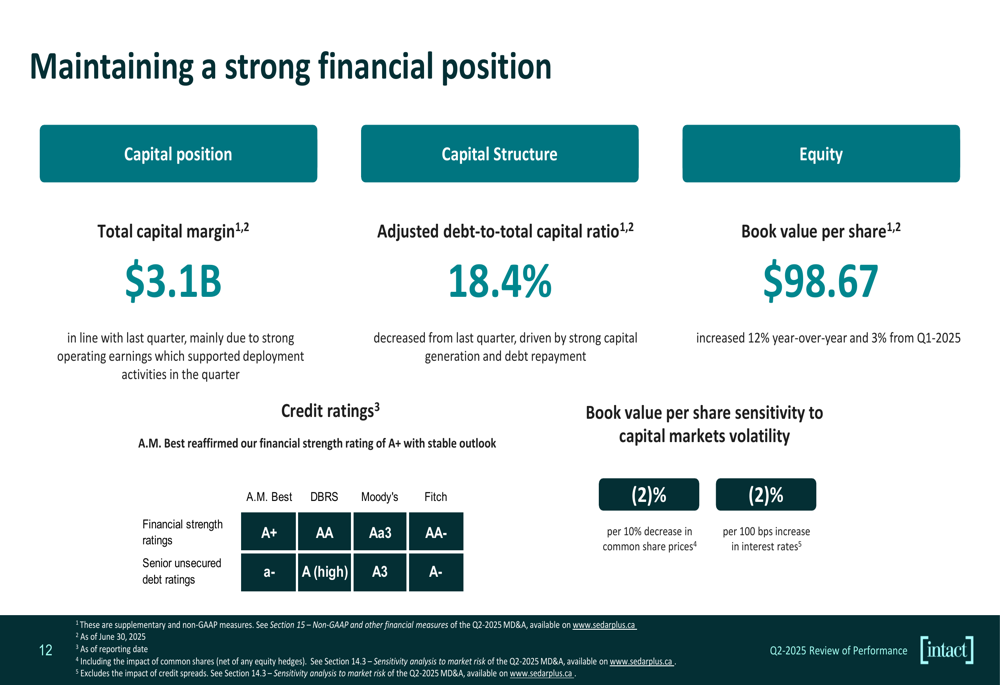

Intact maintains a strong financial position with a total capital margin of $3.1 billion and an adjusted debt-to-total capital ratio of 18.4%. The company's financial strength is further validated by solid ratings from major agencies: A+ from A.M. Best, AA from DBRS, Aa3 from Moody's, and AA- from Fitch.

The company's book value per share sensitivity indicates a potential 2% impact from market fluctuations, suggesting a relatively stable capital position even under stress scenarios.

Looking ahead, Intact remains focused on achieving its target of 10% annual growth in net operating income per share over time. The company continues to invest in technology and strategic expansion, particularly in the US market, while maintaining its commitment to outperforming industry ROE by approximately 500 basis points.

Industry premium growth outlook varies by segment, with Canadian Personal Auto and Property expected to see high-single-digit to low-double-digit growth, while Commercial Lines and international segments are projected to experience mid-single-digit growth. These forecasts align with the company's strategic focus on maintaining strong combined ratios across all business segments.

Despite challenges in certain areas such as commercial lines growth, distribution income, and the Alberta auto market, Intact's diversified business model and strong capital position provide resilience and flexibility to navigate market conditions while pursuing strategic growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.