Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

International Paper (NYSE:IP) reported first-quarter 2025 adjusted operating earnings per share of $0.23, marking a significant improvement from the previous quarter’s negative results. The company’s earnings presentation, delivered on April 30, revealed that despite facing softer market demand, International Paper remains on track to meet its 2025 earnings targets, bolstered by the recent DS Smith acquisition and ongoing cost reduction initiatives.

Quarterly Performance Highlights

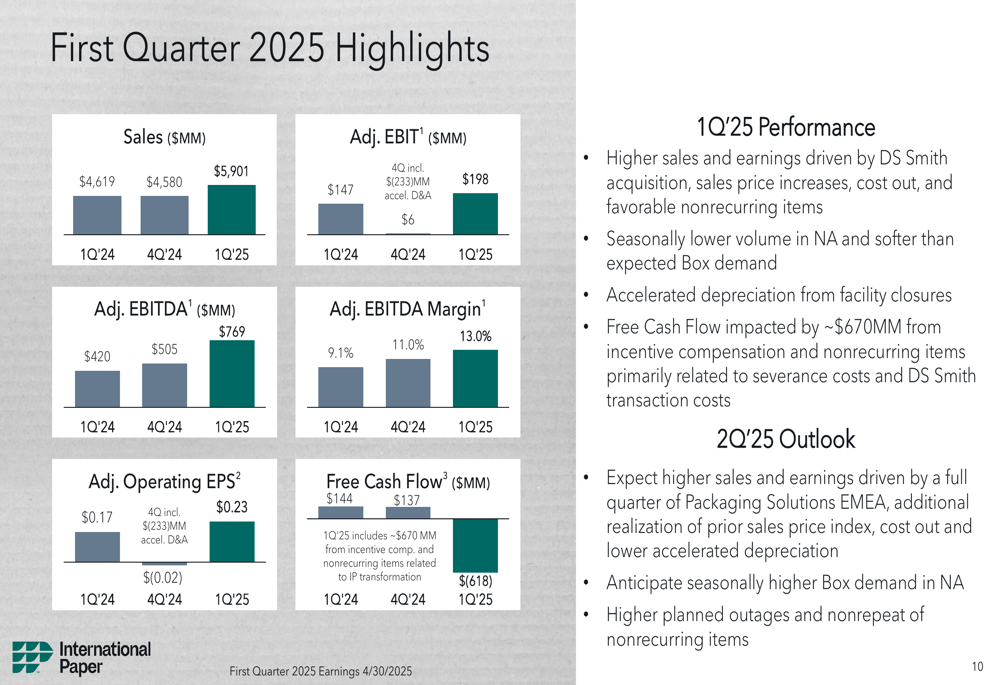

International Paper posted Q1 2025 sales of $5,901 million, with adjusted EBITDA reaching $769 million (13.0% margin). The company’s free cash flow was negative $618 million, impacted by accelerated depreciation related to mill closures.

"Our transformation is underway with a focus on safety, talented team, 80/20 performance system, customer focus, cost reduction, building execution muscle and DS Smith integration," noted CEO Andy Silvernet in the presentation, highlighting the company’s first year of strategic transformation.

As shown in the following chart of quarterly financial highlights:

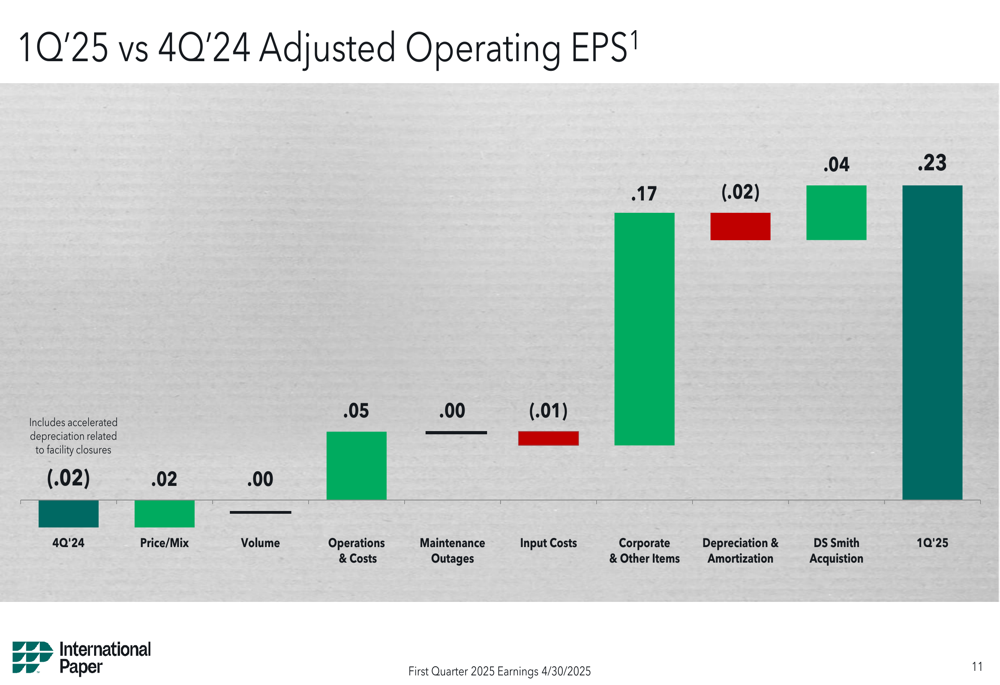

The quarter-over-quarter improvement in adjusted operating EPS was driven by several factors, including favorable nonrecurring items, the DS Smith acquisition contribution of $0.04 per share, and corporate and other items adding $0.17 per share. These positive factors offset the impact of seasonally lower volumes in North America and softer box demand.

The following waterfall chart illustrates the components of the EPS change from Q4 2024:

Segment Performance

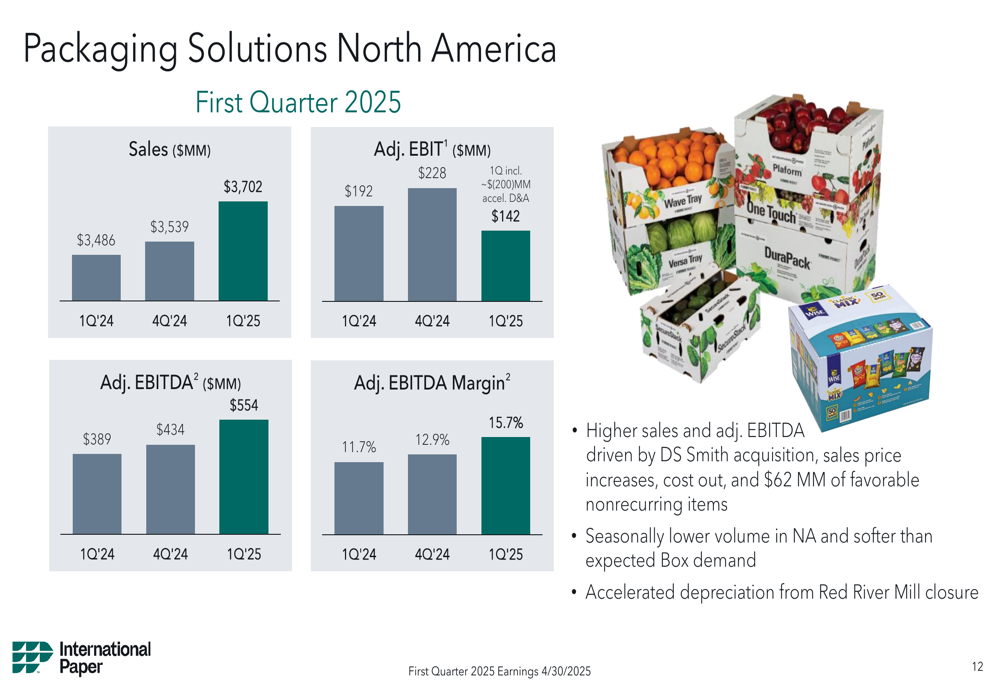

International Paper’s three business segments showed mixed results in the quarter. Packaging (NYSE:PKG) Solutions North America, the company’s largest segment, generated sales of $3,702 million and adjusted EBITDA of $554 million (15.7% margin).

As illustrated in the segment performance chart:

The Packaging Solutions EMEA segment, now operating as DS Smith following the acquisition, contributed $1,550 million in sales and $153 million in adjusted EBITDA (9.9% margin). The Global Cellulose Fibers segment reported $643 million in sales and $68 million in adjusted EBITDA (10.6% margin), with long-term improvement trends despite including $222 million of accelerated depreciation related to the Georgetown Mill closure.

Strategic Initiatives & Cost Reduction

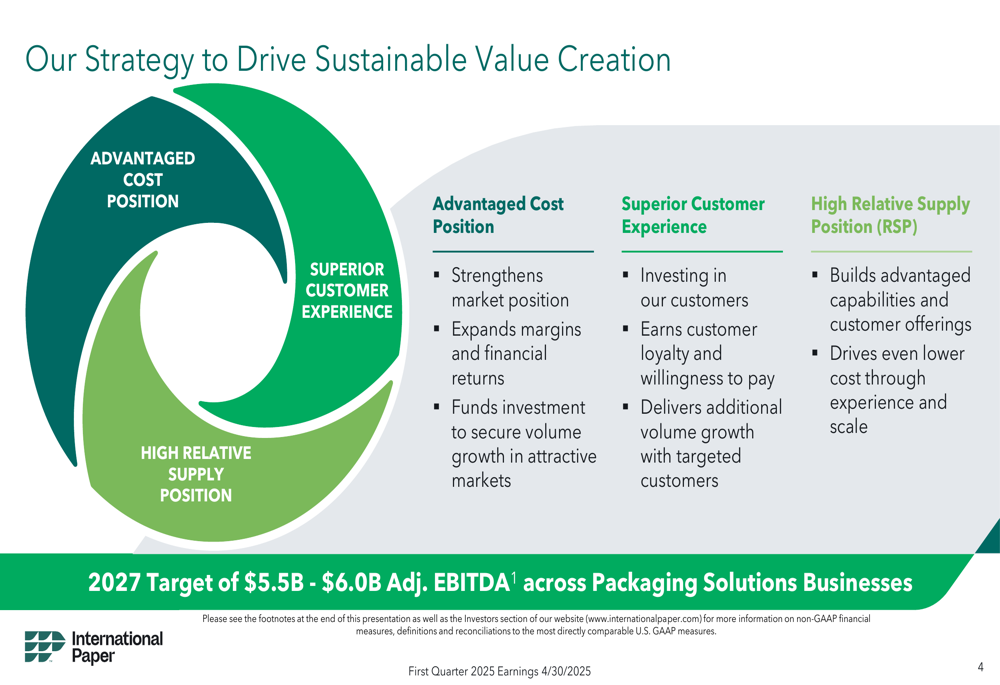

International Paper outlined an ambitious strategy to drive sustainable value creation, focusing on three pillars: advantaged cost position, superior customer experience, and high relative supply position (RSP).

The company’s strategic framework is illustrated in this diagram:

Cost reduction initiatives are targeting approximately $0.6 billion in adjusted EBITDA run-rate benefits by the end of 2025. Actions already taken include enterprise overhead reduction (~$120 million), plant closures (~$70 million), and mill closures (~$170 million). The company is ultimately targeting $1.9 billion in net cost reduction by 2027.

In parallel, commercial excellence initiatives are targeting another $0.6 billion in adjusted EBITDA run-rate benefits by the end of 2025. These include reducing the North American gap to market, implementing price increases (~$500 million), and increasing the sales force by 25%.

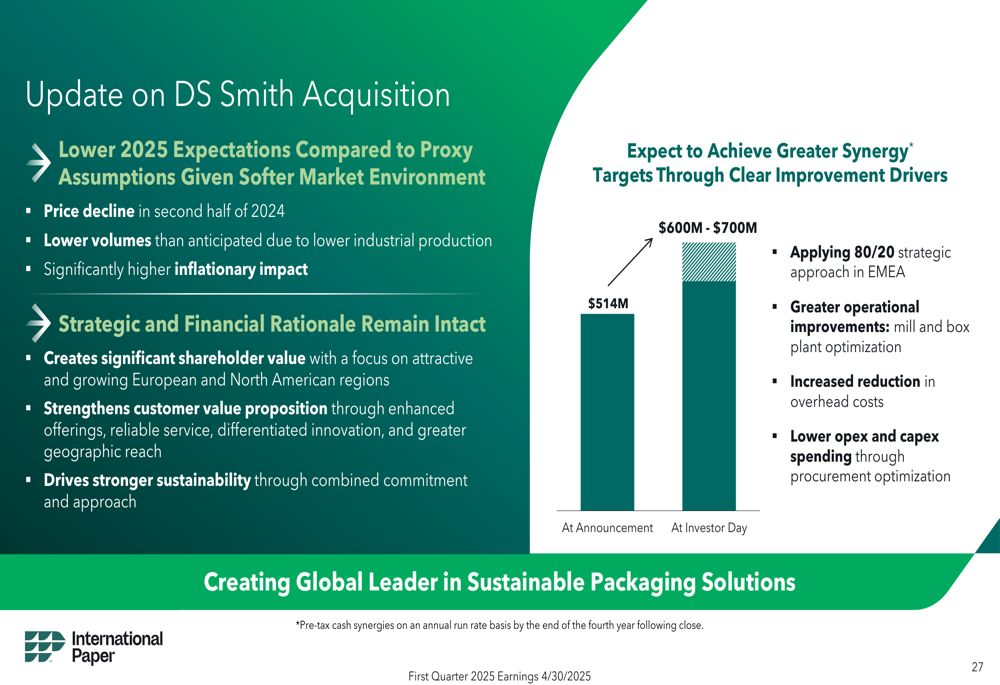

DS Smith Integration

The DS Smith acquisition, while facing lower 2025 expectations compared to proxy assumptions due to softer market conditions, remains strategically sound according to management. The company is targeting $600-700 million in synergies, consistent with previous investor day guidance.

The following chart shows the synergistic value expected from the DS Smith acquisition:

"We have intense focus on DS Smith integration and 80/20 deployment with synergy ramp up," management noted in the presentation, emphasizing the importance of this acquisition to the company’s long-term strategy.

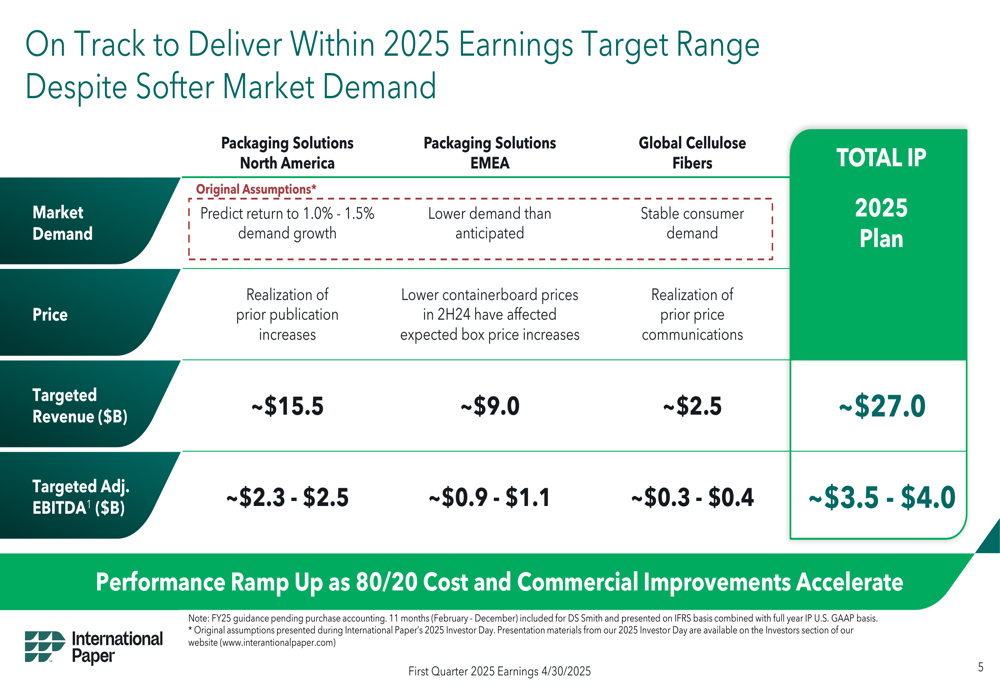

Forward Outlook

Despite macroeconomic uncertainties, International Paper maintains its 2025 adjusted EBITDA target range of $3.5-$4.0 billion. The company acknowledges softer industrial production and flat to down market demand compared to its original plan but has identified mitigation strategies including adjusting supply, accelerating cost reductions, and optimizing capital expenditure.

As shown in the following comparison of original assumptions versus current expectations:

For Q2 2025, the company expects higher sales and earnings driven by increased box demand in North America, though this will be partially offset by planned outages and the non-recurrence of favorable one-time items from Q1.

The company’s stock was trading at $46.68 in premarket trading, down 1.99% following the earnings release, reflecting investor concerns about the negative free cash flow and softer demand environment despite the positive adjusted earnings.

Looking further ahead, International Paper is targeting $5.5-$6.0 billion in adjusted EBITDA across its Packaging Solutions businesses by 2027, with a healthy balance sheet enabling continued investment. The company expects to reduce its debt/adjusted EBITDA ratio to the 2.5x-2.8x range while generating $2.0-$2.5 billion in cash flow by 2027.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.