InvestingPro’s Fair Value model captures 63% gain in Steelcase ahead of acquisition

inTest Corporation (NASDAQ:INTT) reported declining revenue for the first quarter of 2025 despite year-over-year order growth, according to the company’s quarterly presentation delivered on May 2, 2025. The testing equipment provider highlighted cash generation and debt reduction as bright spots amid challenging market conditions that have impacted its semiconductor business segment.

Quarterly Performance Highlights

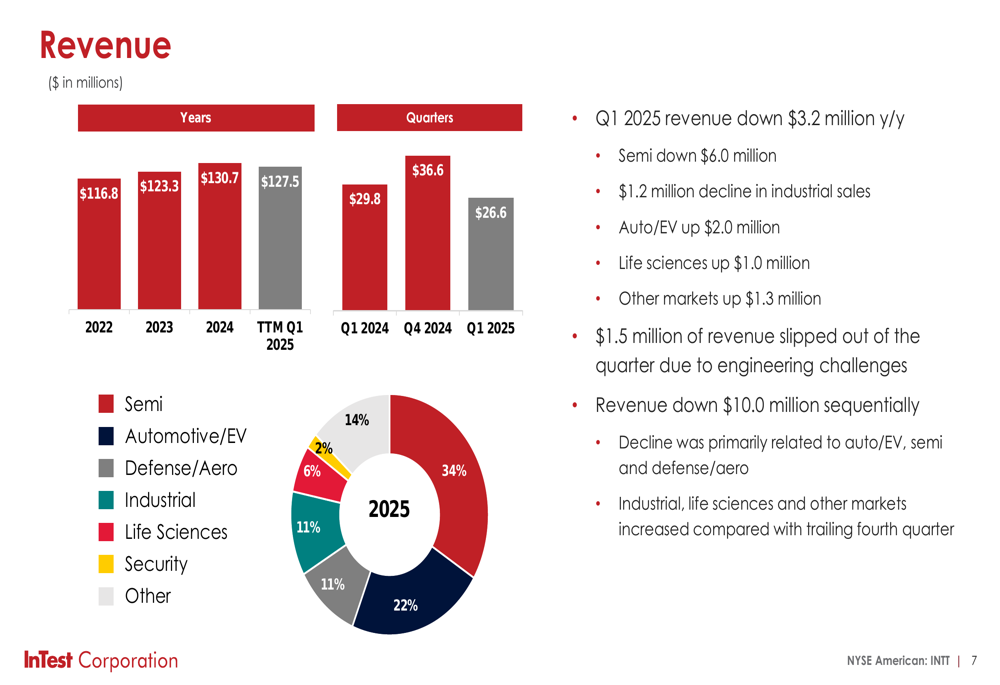

inTest reported Q1 2025 revenue down $3.2 million year-over-year, with particular weakness in the semiconductor sector, which declined by $6.0 million. The company also experienced a $1.2 million decline in industrial sales. These decreases were partially offset by growth in automotive/EV (up $2.0 million), life sciences (up $1.0 million), and other markets (up $1.3 million).

The company noted that $1.5 million of revenue slipped out of the quarter due to engineering challenges, and revenue was down $10.0 million sequentially from Q4 2024.

As shown in the following revenue breakdown by sector:

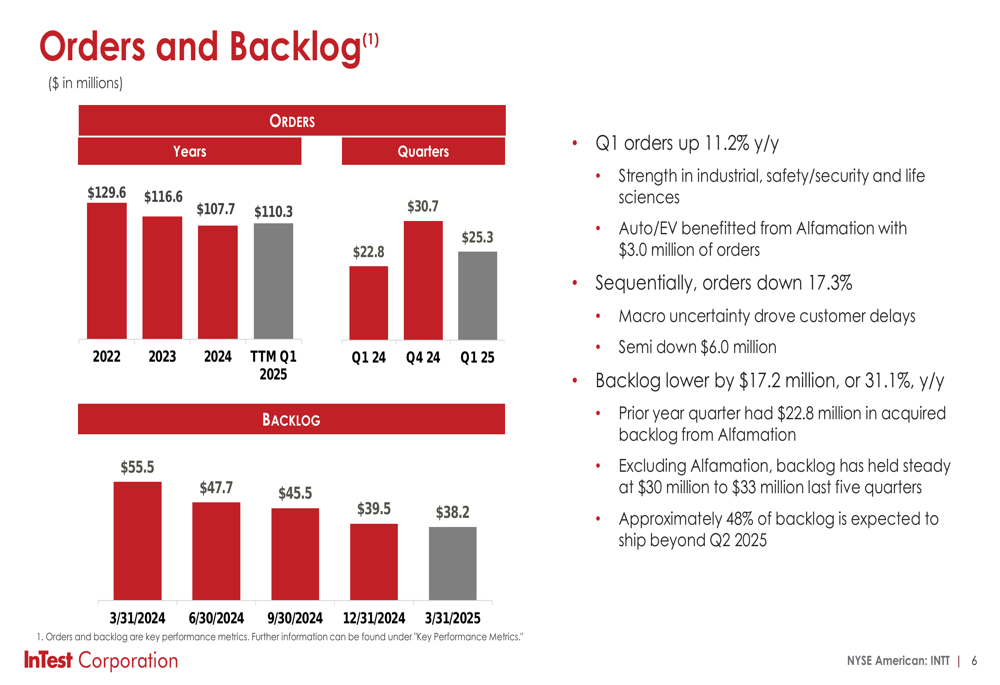

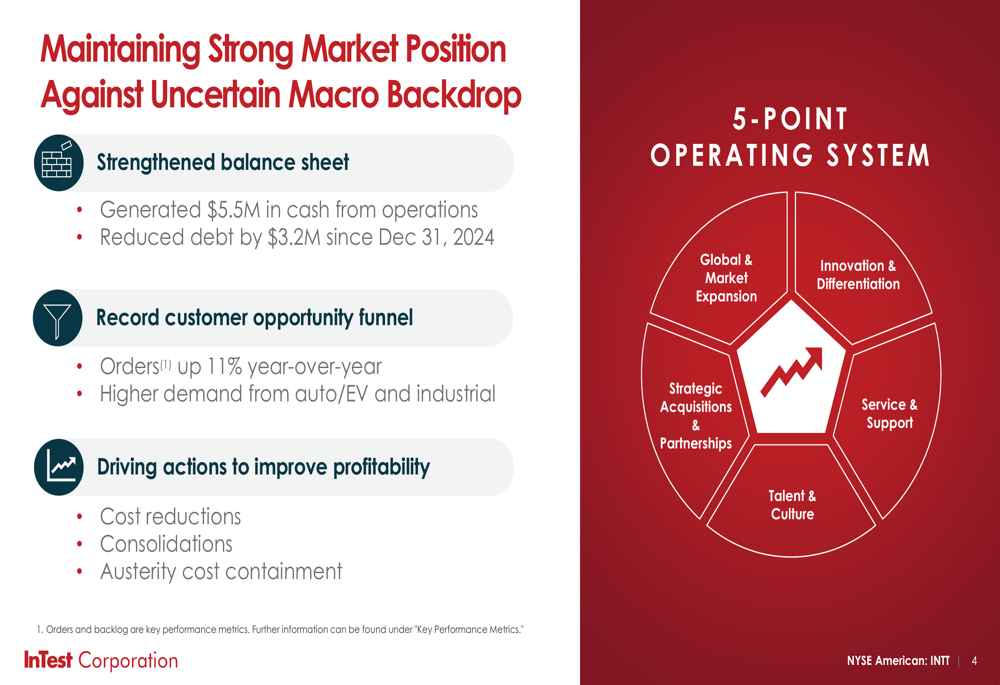

On a more positive note, orders increased 11.2% year-over-year, with strength in industrial, safety/security, and life sciences sectors. The automotive/EV segment benefited from the Alfamation acquisition, contributing $3.0 million in orders. However, orders declined 17.3% sequentially, which management attributed to macro uncertainty driving customer delays, with the semiconductor segment down $6.0 million.

The company’s backlog trends illustrate both the year-over-year decline and recent stabilization:

Detailed Financial Analysis

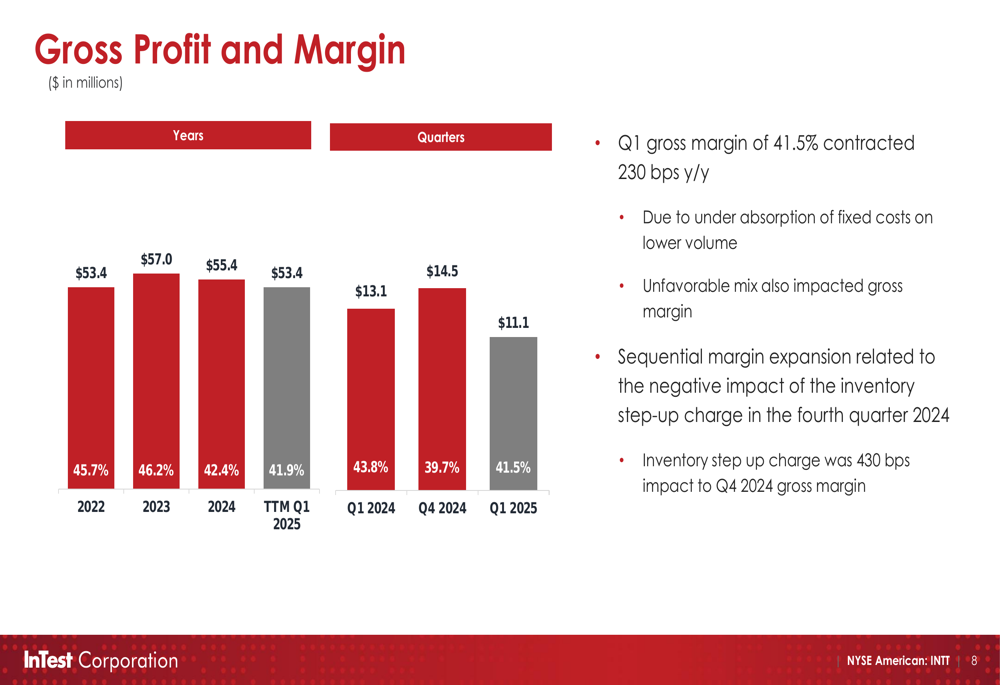

Gross margin contracted to 41.5% in Q1 2025, down 230 basis points year-over-year. Management attributed this decline to under-absorption of fixed costs on lower volume and unfavorable product mix. However, the margin showed sequential improvement from Q4 2024, which had been negatively impacted by a 430 basis point inventory step-up charge.

The following chart illustrates the gross profit and margin trends:

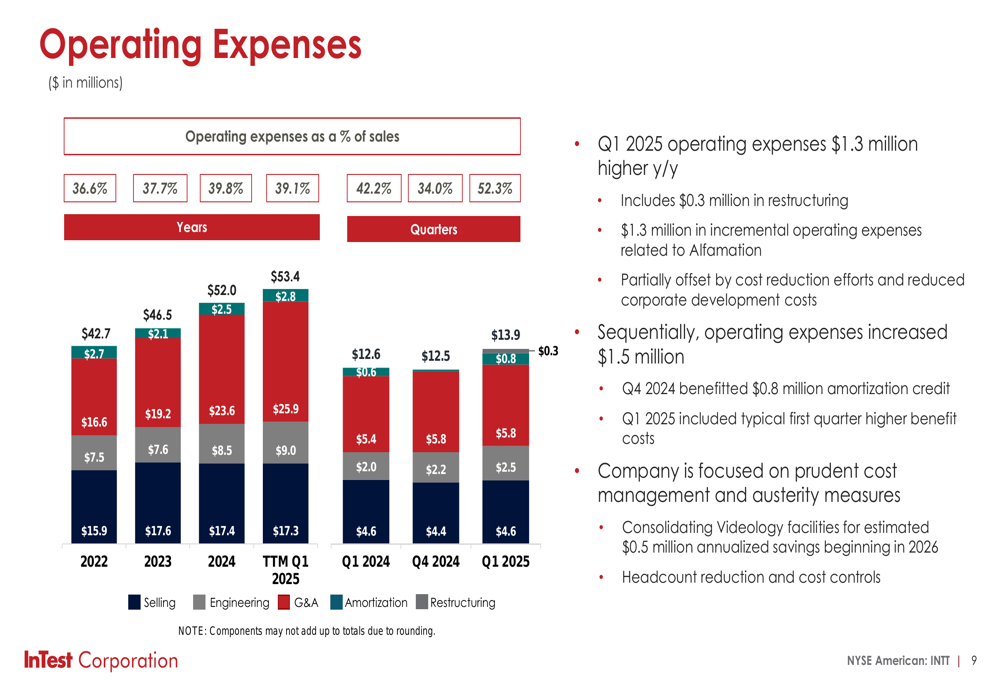

Operating expenses increased by $1.3 million year-over-year, including $0.3 million in restructuring costs and $1.3 million in incremental expenses related to the Alfamation acquisition. These increases were partially offset by cost reduction efforts and reduced corporate development costs.

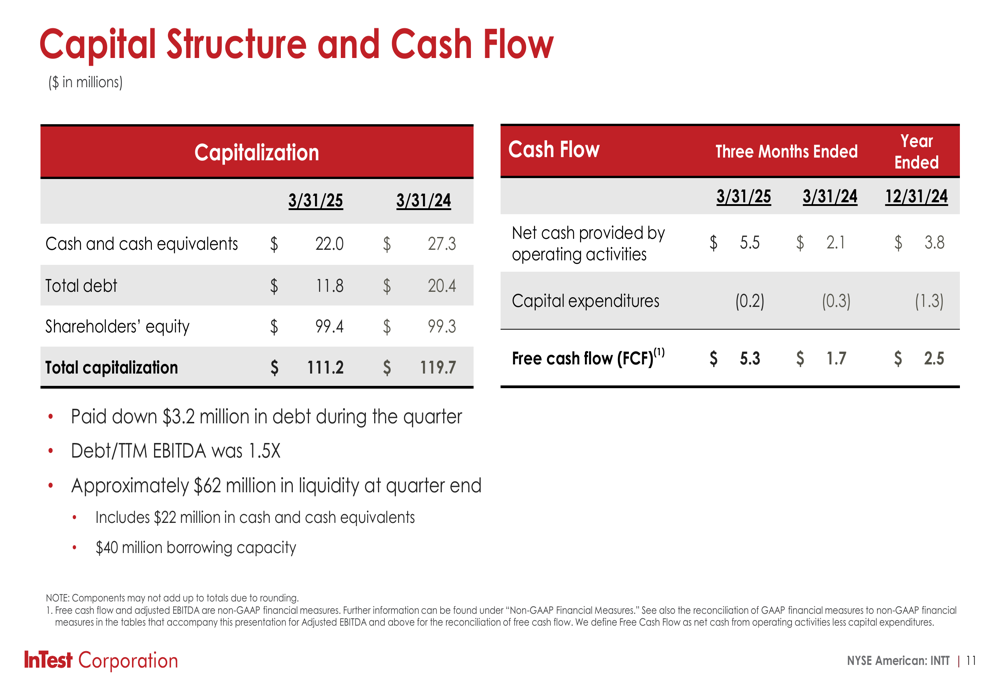

Despite revenue challenges, inTest maintained a strong balance sheet, generating $5.5 million in cash from operations during Q1 and reducing debt by $3.2 million since December 31, 2024. The company reported $62 million in total liquidity at quarter end, including $22 million in cash and cash equivalents and $40 million in borrowing capacity. The debt-to-TTM EBITDA ratio stood at 1.5x.

Strategic Initiatives & Outlook

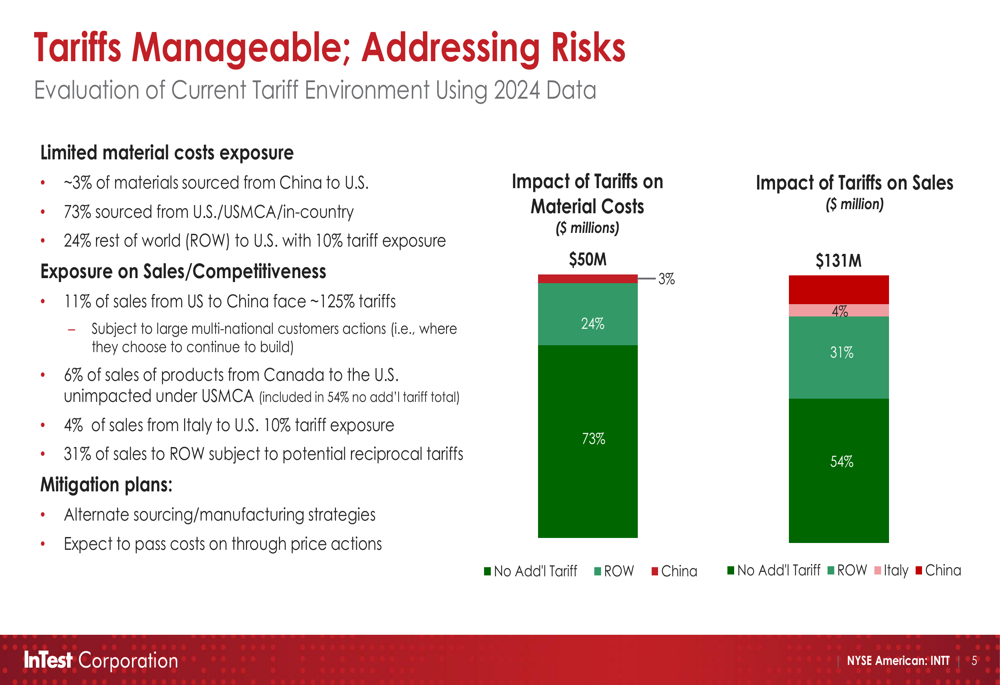

inTest provided a detailed analysis of tariff impacts on its business, showing limited material cost exposure with only about 3% of materials sourced from China to the U.S. However, 11% of sales from the U.S. to China face approximately 125% tariffs, presenting a more significant challenge. The company outlined mitigation plans including alternate sourcing and manufacturing strategies, as well as passing costs through price actions.

The following chart breaks down the company’s tariff exposure:

To improve profitability, inTest is implementing cost reduction initiatives, including consolidating Videology facilities for an estimated $0.5 million in annualized savings beginning in 2026, as well as headcount reductions and other cost controls.

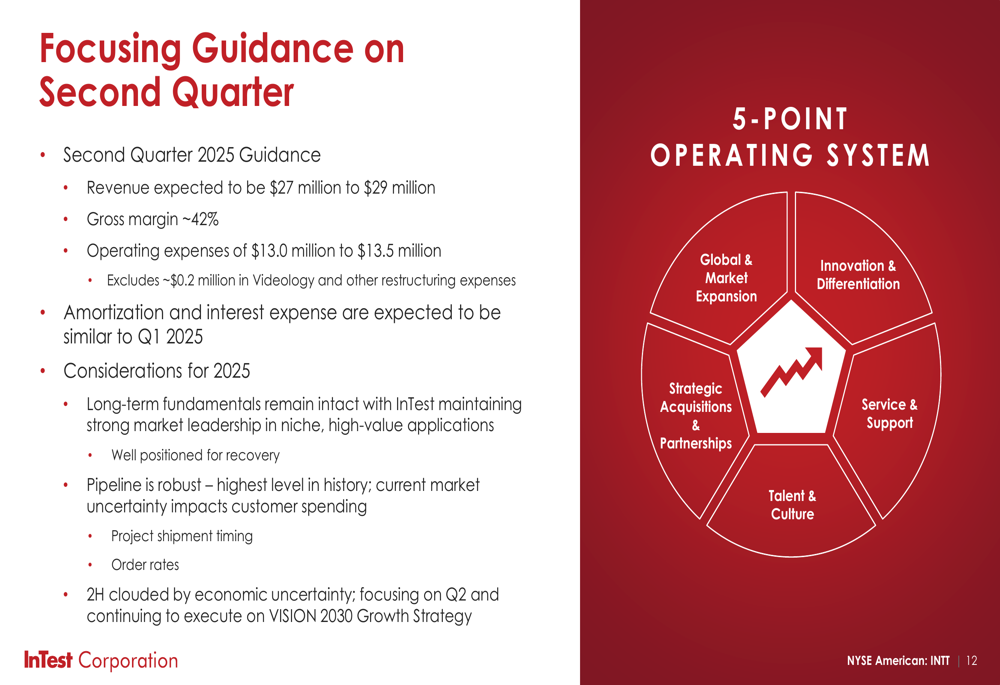

For Q2 2025, inTest provided guidance of $27-29 million in revenue with gross margin of approximately 42%. Operating expenses are expected to be $13.0-13.5 million, excluding about $0.2 million in Videology and other restructuring expenses.

The company emphasized its focus on operational excellence while maintaining its long-term VISION 2030 Growth Strategy:

Market Reaction

inTest’s stock fell sharply in premarket trading following the earnings release, down 13.34% to $5.39, suggesting investors were disappointed with the results and outlook. This reaction contrasts with the previous quarter’s performance, when the stock jumped 18.1% after Q4 2024 results exceeded analyst expectations.

The market response likely reflects concerns about the sequential decline in orders and revenue, as well as ongoing challenges in the semiconductor sector. While management highlighted the company’s cash generation and debt reduction as positives, investors appear focused on the near-term revenue and profitability outlook.

inTest’s management remains confident in the company’s long-term strategy despite current headwinds, citing a robust project pipeline and well-positioned products. However, they acknowledged macroeconomic and geopolitical uncertainties, including potential tariff impacts, as factors affecting near-term performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.