Functional Brands closes $8 million private placement and completes Nasdaq listing

Introduction & Market Context

Intrum AB (INTRUM) presented its third quarter 2025 results on October 30, showing operational improvements amid ongoing restructuring efforts. The credit management company’s stock fell 9.7% following the announcement, closing at SEK 46.1, reflecting investor concerns despite some positive operational trends.

The presentation, led by CEO Johan Åkerblom and CFO Masih Yazdi, highlighted progress in cost reduction initiatives and organic growth in the servicing business, while acknowledging significant one-off impairments that impacted bottom-line results.

Executive Summary

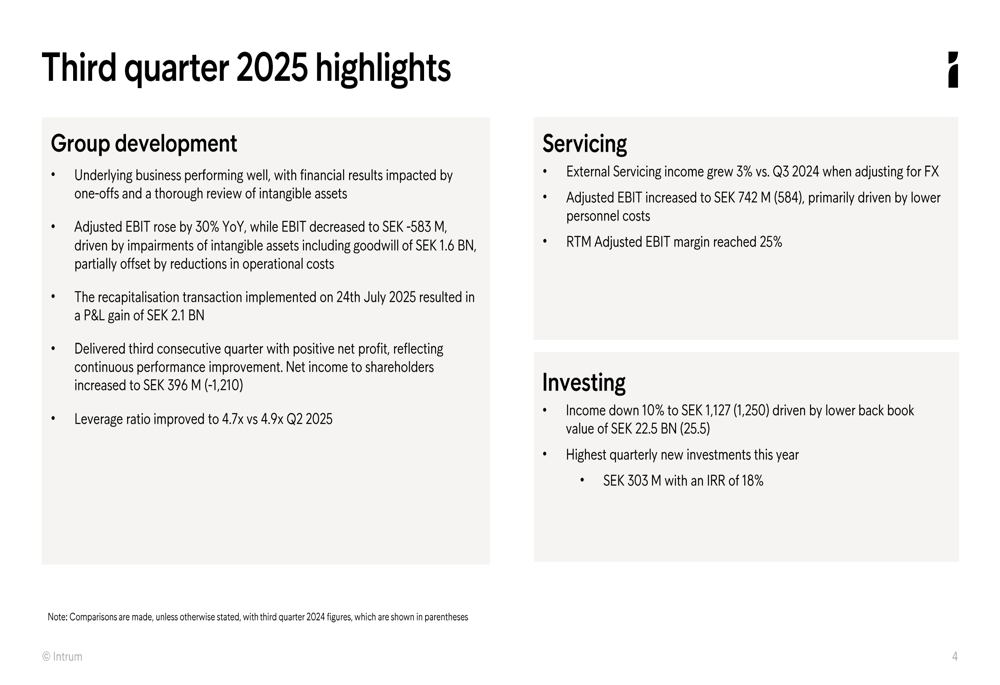

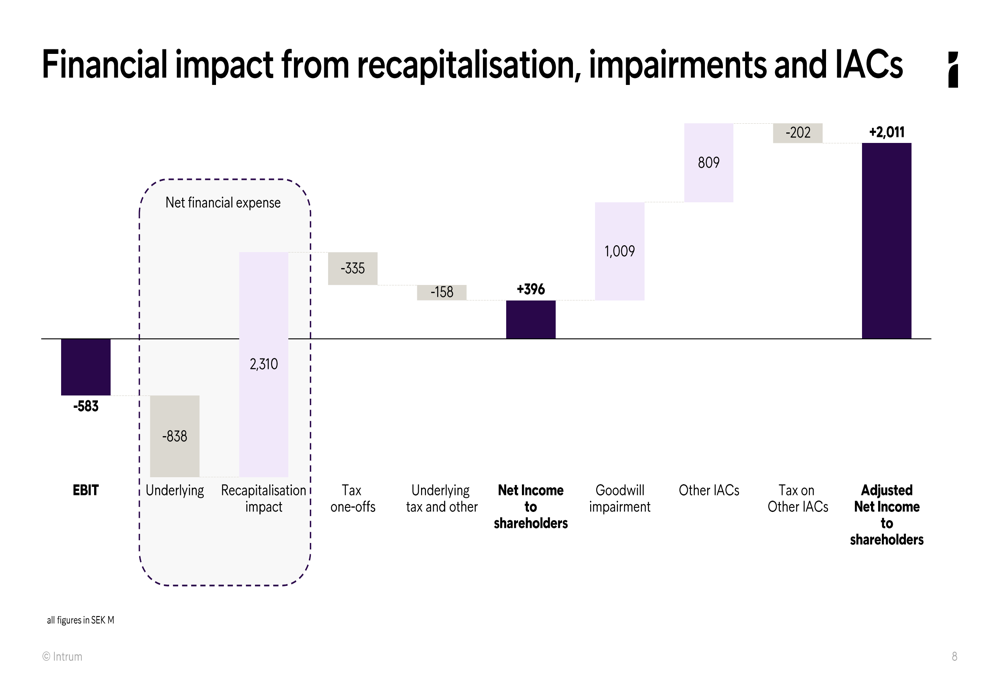

Intrum’s Q3 2025 results revealed a mixed performance with underlying business improvements overshadowed by one-off charges. The company reported a negative EBIT of SEK 583 million due to impairments of intangible assets, including goodwill of SEK 1.6 billion. However, adjusted EBIT rose 30% year-over-year, reflecting operational efficiencies and cost discipline.

The recapitalization transaction implemented in July 2025 resulted in a P&L gain of SEK 2.1 billion, contributing to a positive net income to shareholders of SEK 396 million, compared to a loss of SEK 1,210 million in the same period last year.

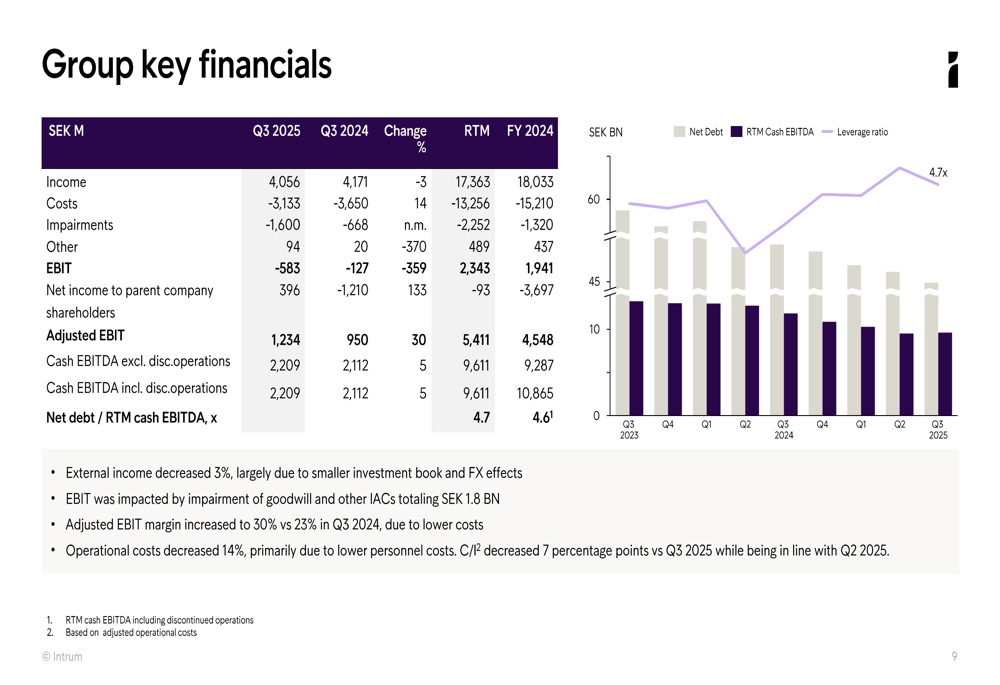

As shown in the following comprehensive overview of the quarter’s performance:

Quarterly Performance Highlights

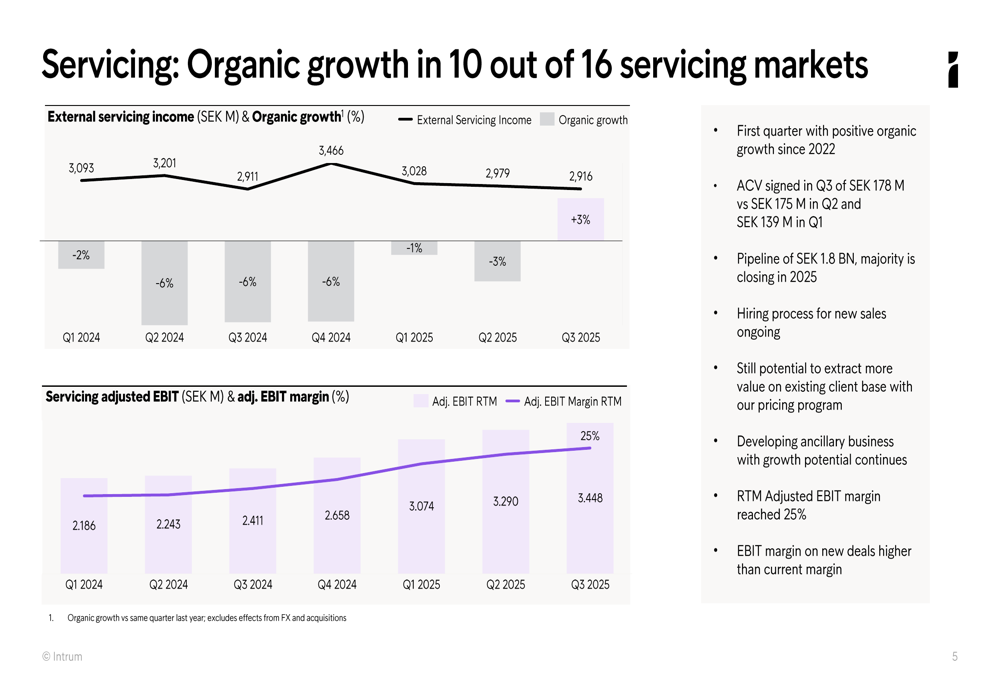

The Servicing segment showed encouraging signs with external servicing income growing 3% year-over-year when adjusting for foreign exchange effects. This marks the first quarter with positive organic growth since 2022. The segment’s adjusted EBIT increased to SEK 742 million from SEK 584 million in Q3 2024, primarily driven by lower personnel costs.

The following chart illustrates the improving trend in external servicing income and adjusted EBIT margin:

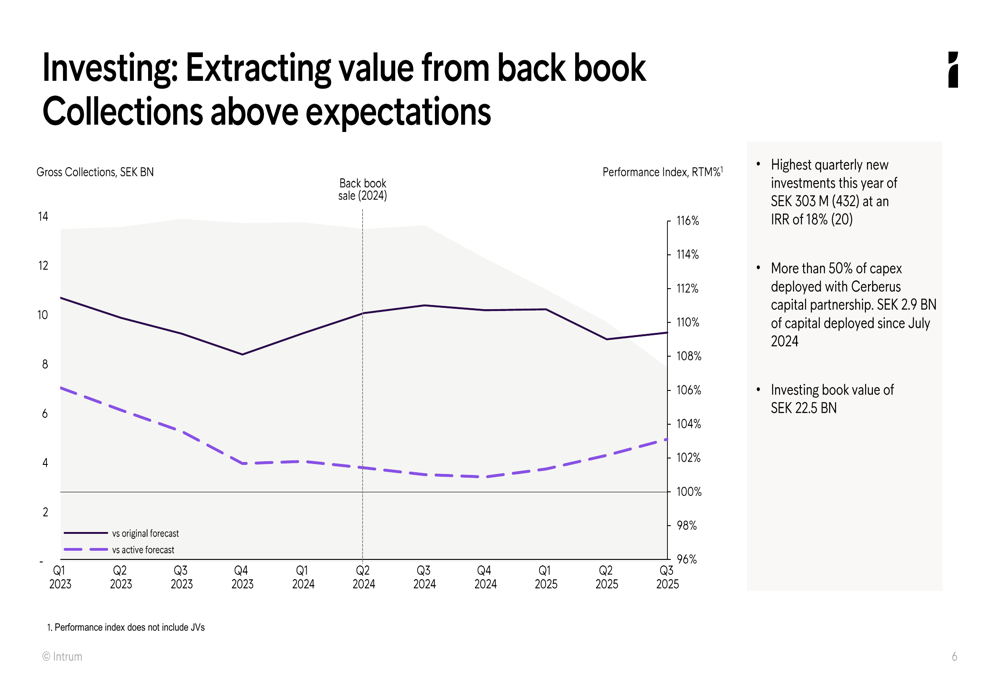

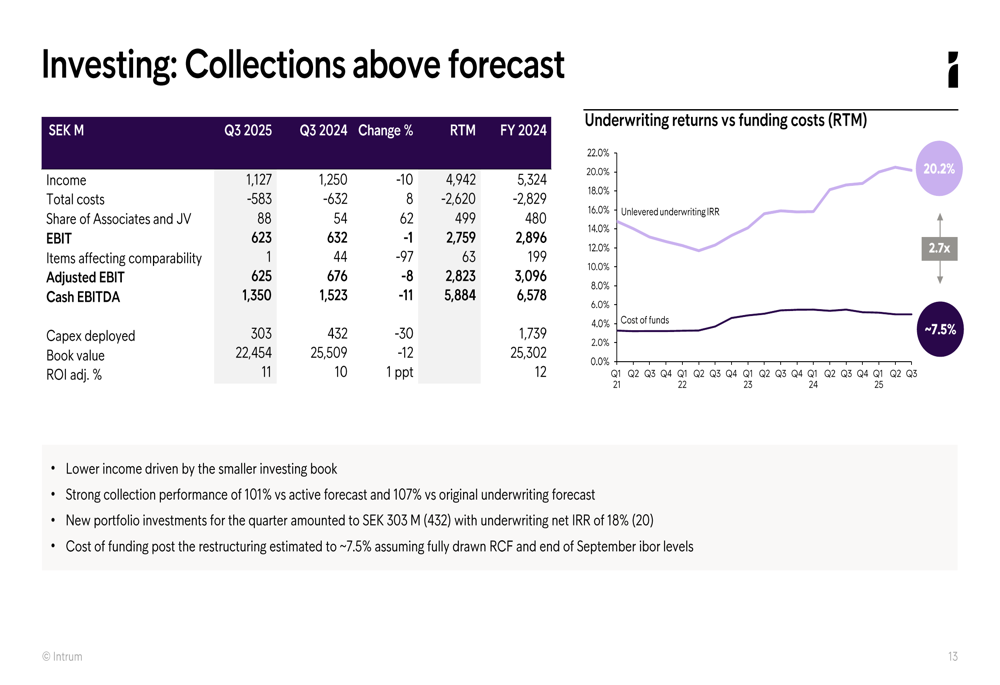

Meanwhile, the Investing segment saw income decline by 10% to SEK 1,127 million, largely due to a smaller back book value of SEK 22.5 billion compared to SEK 25.5 billion in Q3 2024. Despite this, collection performance remained strong at 101% versus active forecast and 107% versus original underwriting forecast.

The following visualization shows collections consistently exceeding expectations:

Detailed Financial Analysis

Intrum’s financial results were significantly impacted by one-off charges related to the recapitalization process and impairments. The following breakdown illustrates how these factors affected the company’s bottom line:

Group key financials show that while income decreased by 3% year-over-year, the adjusted EBIT margin improved to 30% compared to 23% in Q3 2024, primarily due to lower costs. Operational costs decreased by 14%, mainly from reduced personnel expenses.

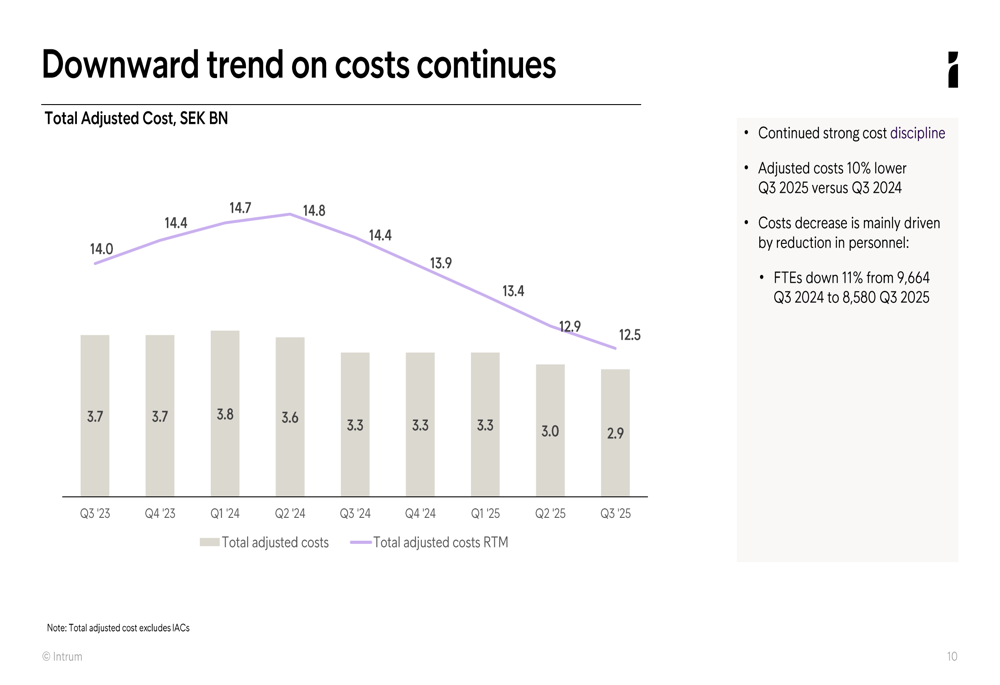

The company’s cost discipline remains a key focus area, with adjusted costs 10% lower in Q3 2025 compared to Q3 2024. Full-time employees decreased by 11% from 9,664 in Q3 2024 to 8,580 in Q3 2025, contributing significantly to the cost reduction.

As demonstrated in the following chart showing the downward trend in costs:

Strategic Initiatives

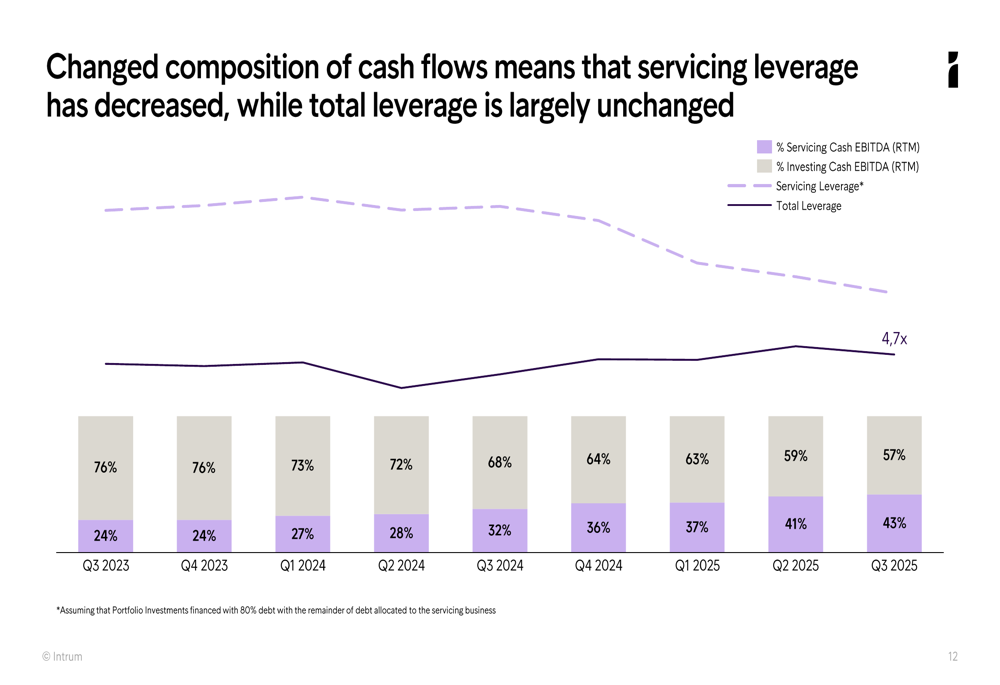

Intrum’s business mix continues to evolve, with Investing segment gaining importance relative to Servicing. The composition of cash flows shows that Servicing cash EBITDA decreased from 68% to 57% of total over the past year, while Investing increased from 32% to 43%.

The Investing segment, despite lower overall income, showed strong collection performance and completed its highest quarterly new investments this year at SEK 303 million with an IRR of 18%. The company has deployed more than 50% of capex with the Cerberus capital partnership, totaling SEK 2.9 billion since July 2024.

The following breakdown provides further insight into the Investing segment’s performance:

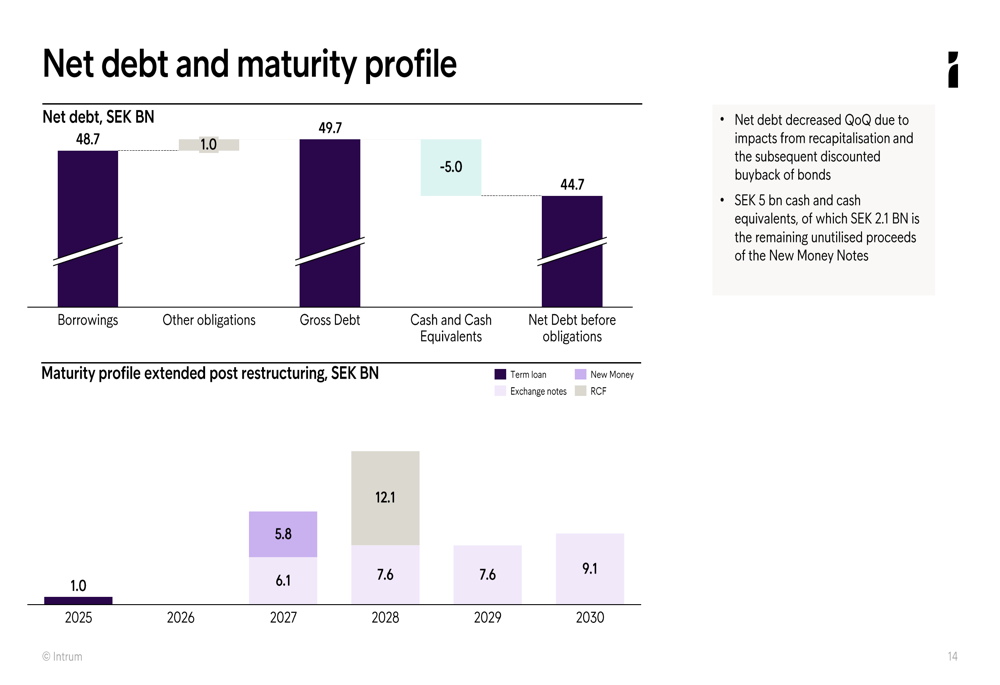

Intrum’s debt profile has also improved following the recapitalization, with net debt decreasing quarter-over-quarter. The company reported SEK 5 billion in cash and cash equivalents, of which SEK 2.1 billion represents remaining unutilized proceeds from the New Money Notes.

Forward-Looking Statements

Looking ahead, Intrum plans to present a strategic review and updated financial targets with its full-year 2025 results. The company highlighted several areas of focus, including continued servicing top-line growth, maintaining margin discipline, and extracting more value from the existing client base through its pricing program.

The pipeline for new servicing contracts stands at SEK 1.8 billion, with the majority expected to close in 2025. The company is also developing ancillary businesses with growth potential and notes that the EBIT margin on new deals is higher than the current margin.

As summarized in the third quarter overview:

While Intrum’s presentation emphasized operational improvements and the third consecutive quarter with positive net profit, investors appeared concerned about the significant impairment charges and ongoing restructuring efforts. The stock’s 9.7% decline following the earnings release suggests the market may require more evidence of sustainable performance improvement before regaining confidence in the company’s turnaround strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.