IonQ CRO Alameddine Rima sells $4.6m in shares

Introduction & Market Context

InvenTrust Properties Corp (NYSE:IVT) released its Q1 2025 investor presentation on May 1, highlighting strong quarterly performance and continued execution of its Sun Belt-focused retail strategy. The company’s stock closed at $28.18, up 1.15% on the day, reflecting positive investor sentiment following the earnings announcement.

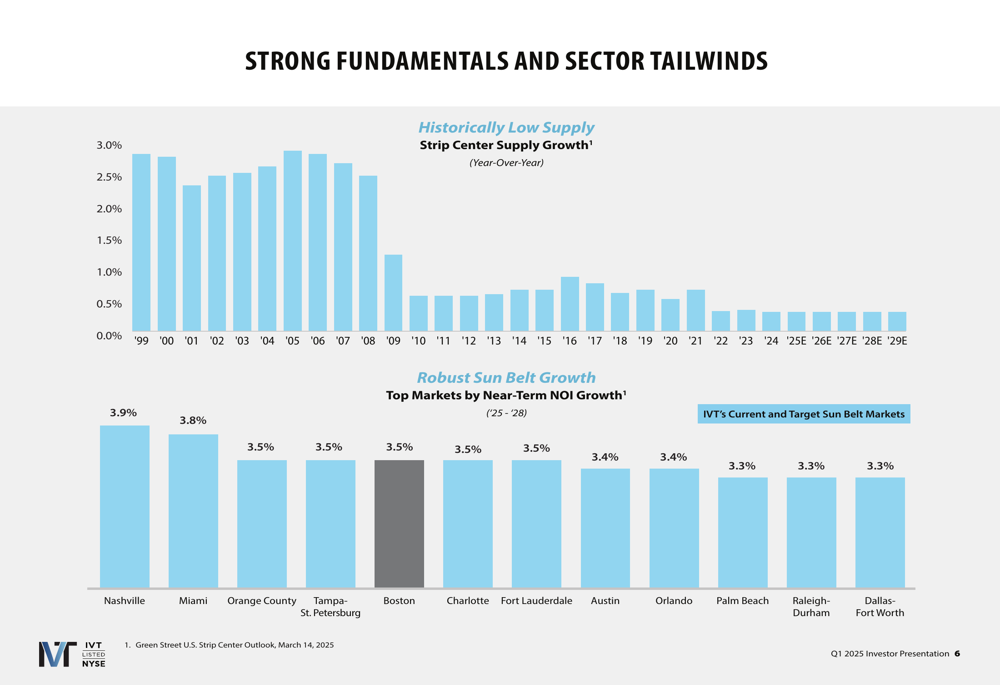

The REIT operates in a favorable market environment characterized by historically low supply growth in the strip center sector, combined with robust projected NOI growth in Sun Belt markets. This market dynamic has created tailwinds for IVT’s portfolio, which consists of 68 retail properties with 97% located in the Sun Belt region.

As shown in the following chart illustrating the supply constraints in the retail market:

Quarterly Performance Highlights

InvenTrust delivered strong financial and operational results in Q1 2025, exceeding analyst expectations. The company reported earnings per share of $0.09, surpassing the forecasted $0.07 by 28.6%, while revenue reached $73.77 million, slightly above the anticipated $73.25 million.

Same Property Net Operating Income (SPNOI) grew by 6.1% year-over-year, demonstrating the strength of the company’s portfolio and leasing strategy. Core FFO per diluted share was $0.46, representing a 4.5% increase from the previous year.

The following slide summarizes the company’s first quarter performance metrics:

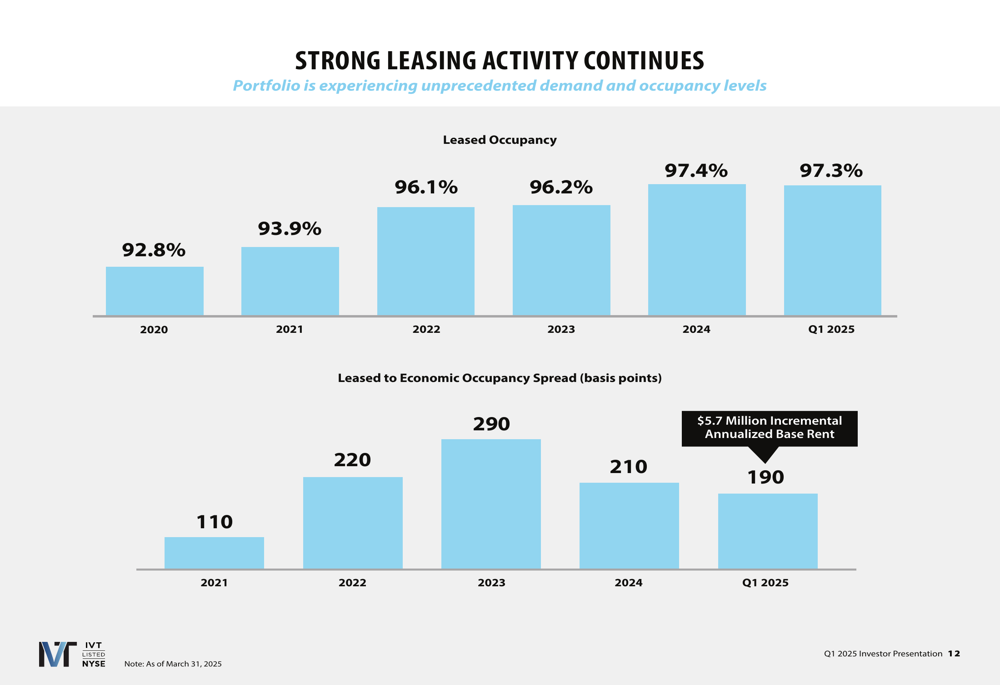

Occupancy metrics remained robust, with leased occupancy at 97.3% and an impressive 90.0% tenant retention rate. Anchor tenant leased occupancy reached 99.5%, while small shop tenant leased occupancy stood at 93.4%. The company achieved comparable leasing spreads of 9.6%, indicating strong demand for its retail spaces.

The presentation highlighted the company’s consistent occupancy growth trajectory since 2020:

Strategic Initiatives and Portfolio Positioning

InvenTrust’s strategy centers on three key pillars: Sun Belt geographic focus, grocery-anchored retail concentration, and maintaining an investment-grade balance sheet. The company’s portfolio is heavily weighted toward essential retail, with 86% of NOI derived from grocery-anchored centers.

The following slide illustrates the company’s investment thesis and strategic focus:

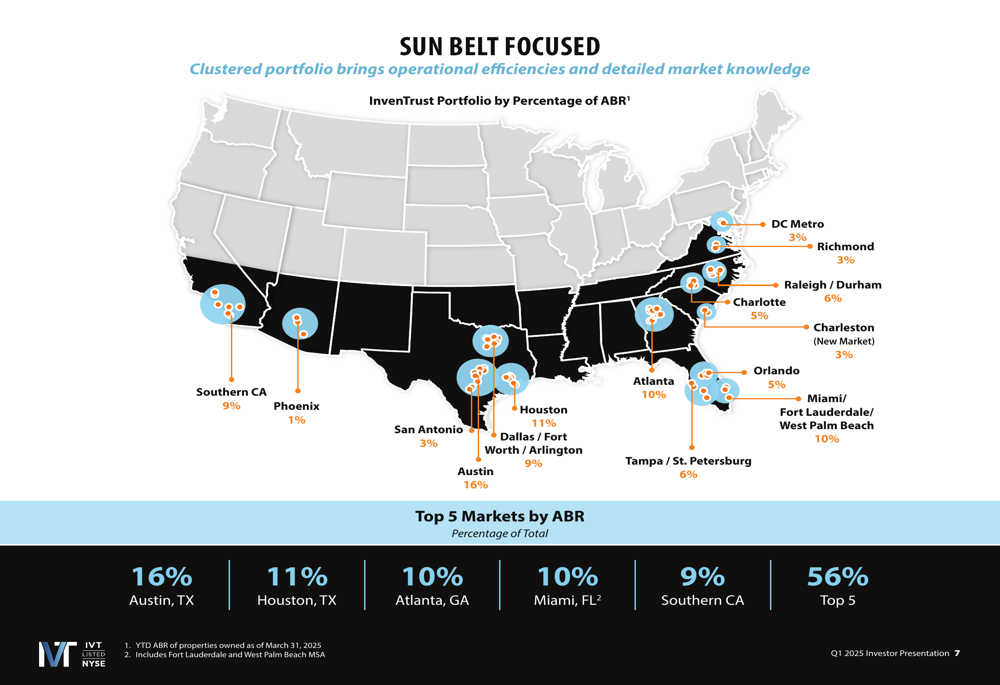

Geographic distribution remains concentrated in high-growth Sun Belt markets, with top locations including Austin (16% of ABR), Houston (11%), Atlanta (10%), and Miami (10%). During the earnings call, management revealed plans to exit California investments by 2025, redirecting capital to higher-growth markets.

The company’s geographic footprint is visualized in this map:

InvenTrust continues to grow through strategic acquisitions in target markets. Recent additions include Carmel Village in Charlotte and Plaza Escondida in Tucson (both acquired in Q2 2025), as well as Market at Mill Creek and Nexton Square in Charleston (acquired in Q4 2024). These properties feature strong ABR per square foot ranging from $16.53 to $27.18 and high occupancy rates between 91.0% and 100%.

The following slide details these recent acquisitions:

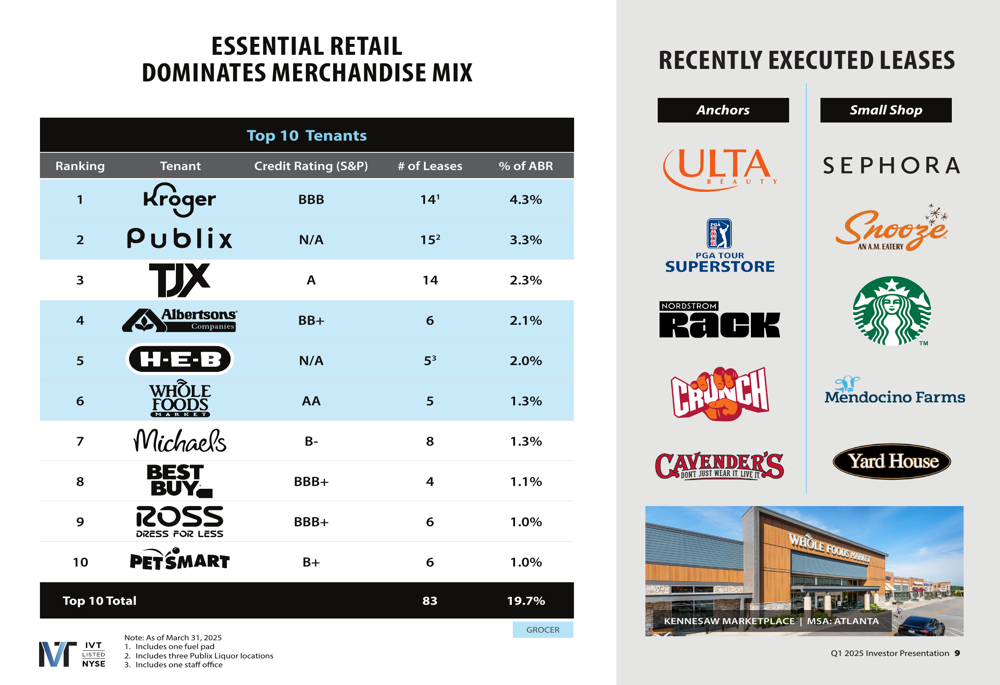

The company’s tenant mix is dominated by essential retail, with top tenants including Kroger (NYSE:KR) (4.3% of ABR), Publix (3.3%), and TJX (NYSE:TJX) (2.3%). This focus on necessity-based retailers provides stability and resilience to the portfolio.

A key competitive advantage for InvenTrust is its limited exposure to retailers on industry watch lists. The company has significantly lower exposure to potentially troubled tenants compared to its peer average, reducing risk in its portfolio.

Financial Position and Outlook

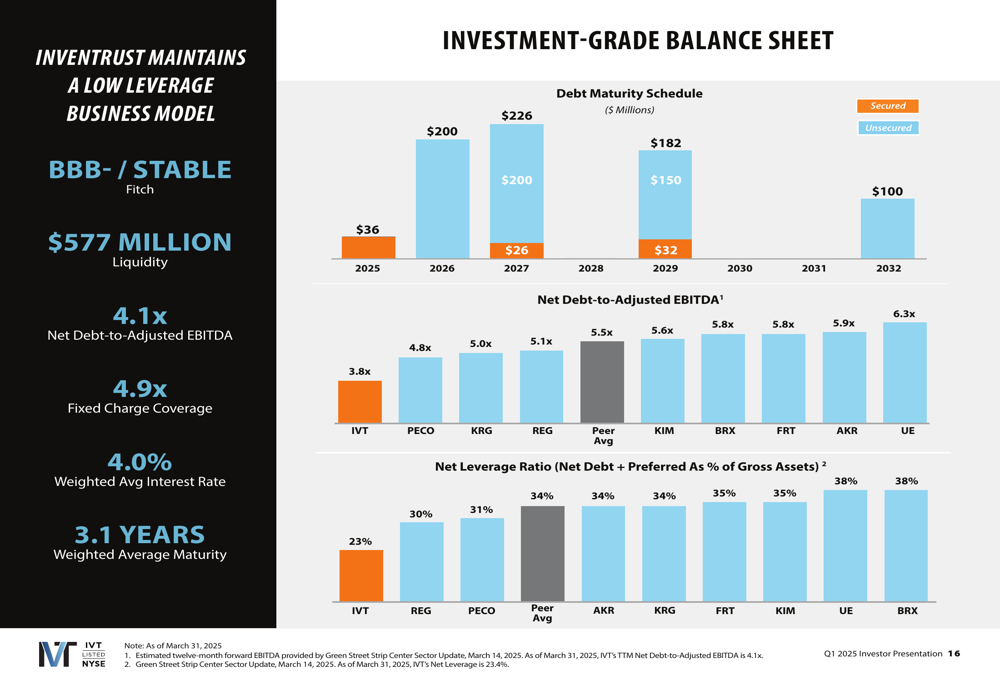

InvenTrust maintains a strong balance sheet with a Net Debt-to-Adjusted EBITDA ratio of 4.1x, well below its long-term target range of 5.0x-6.0x. The company’s net leverage ratio stands at 23.4%, with total liquidity of $577 million providing ample flexibility for future investments.

The debt maturity schedule and key balance sheet metrics are illustrated here:

For full-year 2025, InvenTrust projects core FFO per diluted share of $1.79-$1.83, representing growth of 3.5% to 5.8%. Same Property NOI growth is expected to range between 3.5% and 4.5%. The company has established a 2025 annualized dividend rate of $0.95, continuing its track record of sustainable dividend growth.

The company’s dividend growth trajectory is shown in the following chart:

Competitive Industry Position

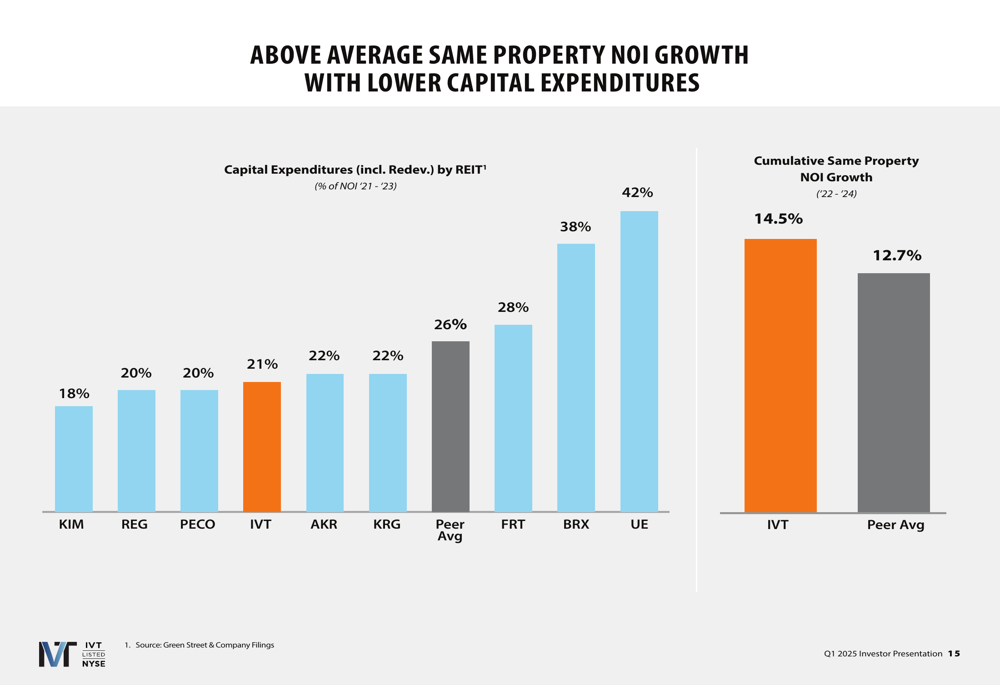

InvenTrust has outperformed its peer group in Same Property NOI growth over recent years. The company’s cumulative SPNOI growth from 2022-2024 exceeded the peer average, positioning it as one of the stronger performers in the strip center REIT sector.

This competitive performance is illustrated in the following comparison:

CEO DJ Bush emphasized the company’s strategic advantages during the earnings call, stating: "Our focus on essential retail positions us well to navigate these challenges." He highlighted the importance of long-term leasing strategies and expressed confidence in the company’s acquisition pipeline.

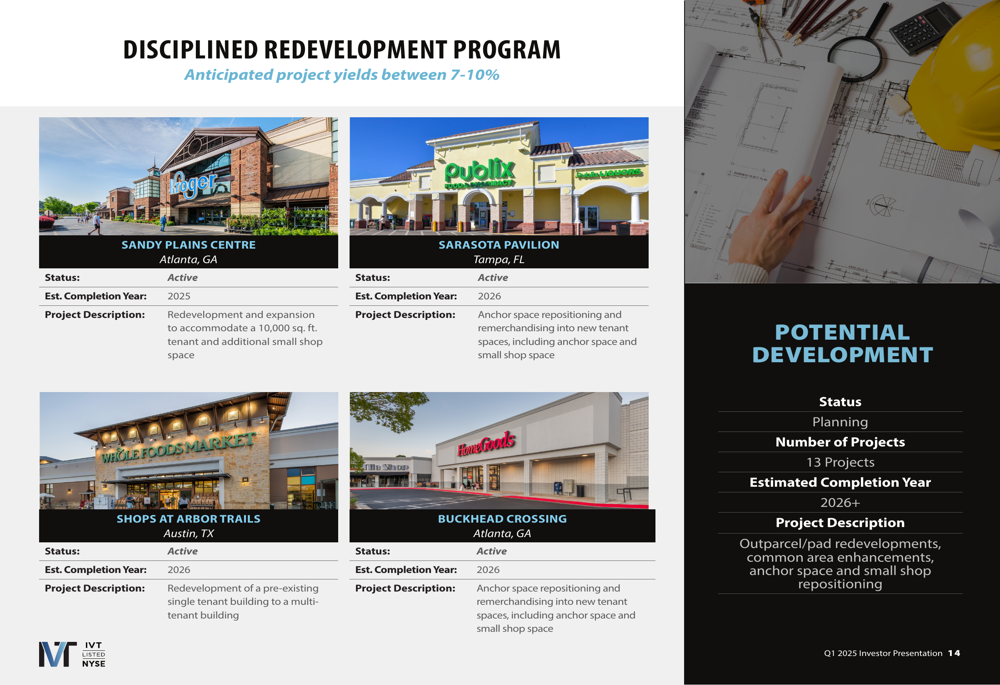

The company’s disciplined redevelopment program includes active projects in Atlanta, Tampa, and Austin, with 13 additional projects in the planning stage for 2026 and beyond. These initiatives focus on outparcel/pad redevelopments, common area enhancements, and space repositioning to drive future growth.

With its focused Sun Belt strategy, high-quality grocery-anchored portfolio, and strong balance sheet, InvenTrust appears well-positioned to continue delivering above-average growth in the retail REIT sector. The company’s Q1 2025 results demonstrate the effectiveness of this approach, with metrics exceeding analyst expectations and providing a solid foundation for the remainder of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.