Bank of America, Morgan Stanley, Nvidia and Dollar Tree rise premarket

Introduction & Market Context

Invesco Mortgage Capital Inc. (NYSE:IVR) reported second-quarter 2025 results on July 25, revealing a challenging period marked by market volatility and negative returns. The mortgage REIT faced significant headwinds as trade policy concerns triggered market turbulence, particularly in April, leading to strategic portfolio adjustments.

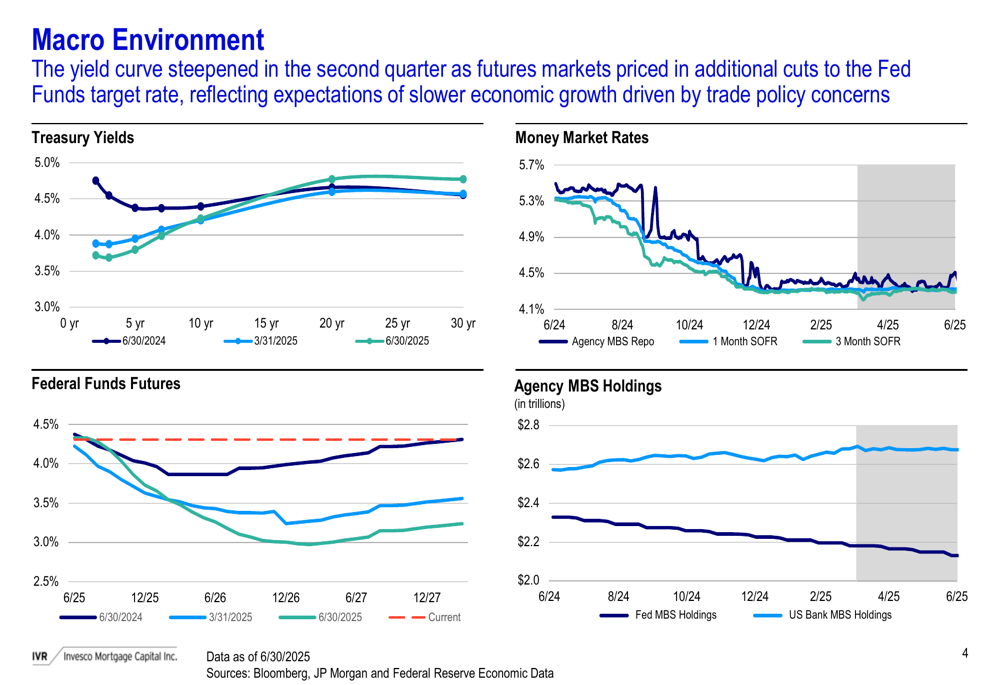

According to the company’s presentation, the yield curve steepened during the quarter as futures markets priced in additional cuts to the Federal Reserve’s target rate, reflecting expectations of slower economic growth driven by trade policy concerns. This macroeconomic backdrop created a volatile environment for mortgage-backed securities.

Quarterly Performance Highlights

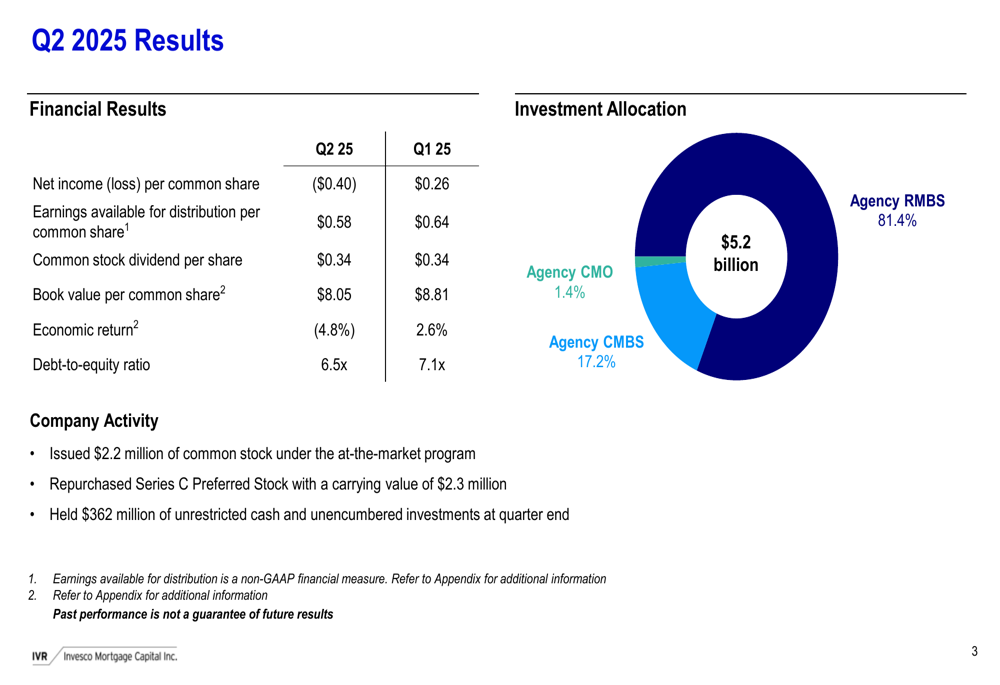

Invesco Mortgage Capital reported a net loss of $0.40 per common share for Q2 2025, a significant deterioration from the $0.26 income per share in the previous quarter. Earnings available for distribution, a non-GAAP measure the company uses to assess its ability to generate income for shareholders, declined to $0.58 per share from $0.64 in Q1.

The company’s book value per common share fell to $8.05 as of June 30, 2025, down from $8.81 at the end of March, representing an 8.6% decline. This contributed to a negative economic return of 4.8% for the quarter, a stark contrast to the positive 2.6% return achieved in Q1.

Despite these challenges, Invesco maintained its quarterly dividend at $0.34 per common share, resulting in an annualized dividend yield of 17.3% based on the quarter-end share price of $7.84.

Portfolio Composition and Strategy

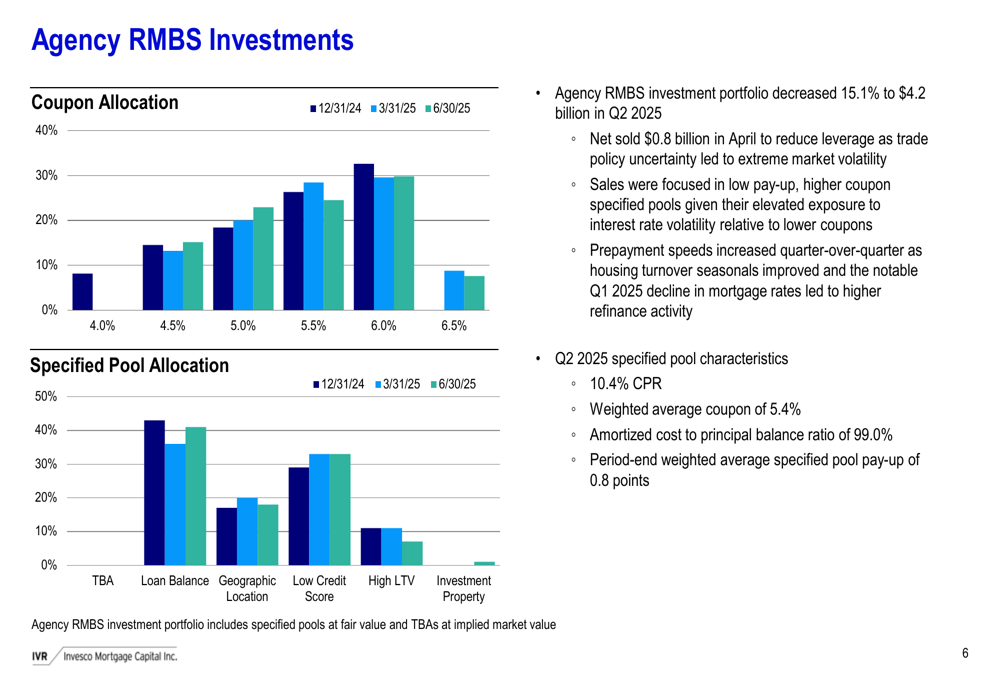

In response to market volatility, Invesco Mortgage Capital strategically reduced its Agency RMBS (Residential Mortgage-Backed Securities) portfolio by 15.1% to $4.2 billion during the quarter. The company disclosed that it net sold $0.8 billion in April to reduce leverage as trade policy uncertainty led to extreme market volatility.

The company’s investment allocation at quarter-end consisted of 81.4% in Agency RMBS, 17.2% in Agency CMBS (Commercial Mortgage-Backed Securities), and 1.4% in Agency CMO (Collateralized Mortgage Obligations), with a total investment portfolio of $5.2 billion.

As shown in the following chart detailing the Agency RMBS investments by coupon and pool allocation, the company focused its sales on low pay-up, higher coupon specified pools due to their elevated exposure to interest rate volatility relative to lower coupons:

The Agency RMBS portfolio had a constant prepayment rate (CPR) of 10.4%, a weighted average coupon of 5.4%, and an amortized cost to principal balance ratio of 99.0%. The period-end weighted average specified pool pay-up was 0.8 points.

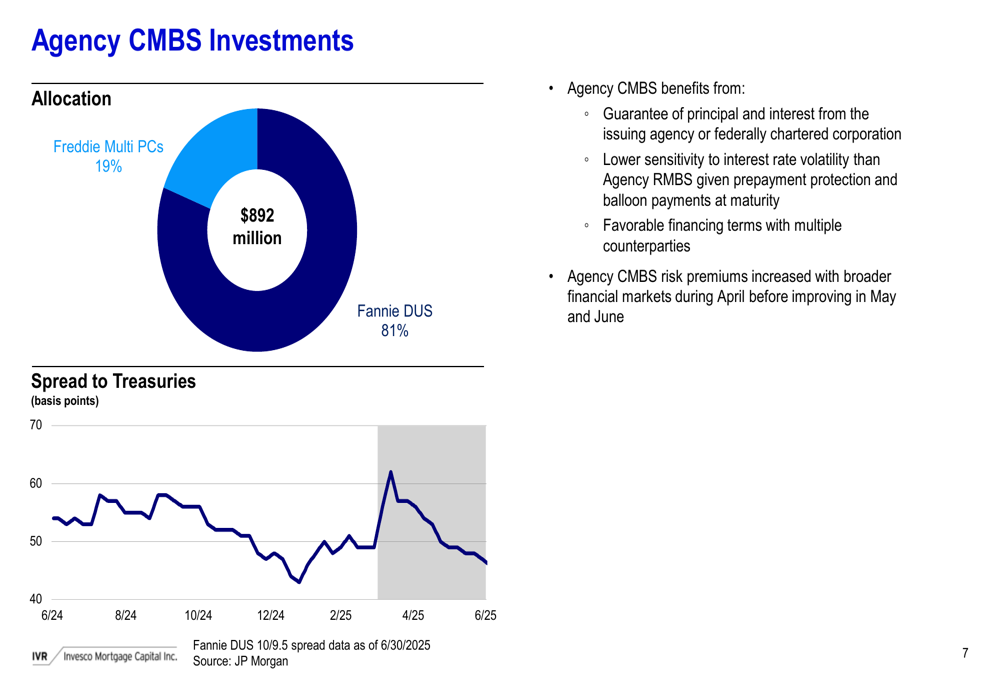

Complementing its RMBS holdings, Invesco maintained $892 million in Agency CMBS investments, which offer lower sensitivity to interest rate volatility than Agency RMBS due to prepayment protection and balloon payments at maturity. The allocation was primarily in Fannie DUS (81%) and Freddie Multi PCs (19%).

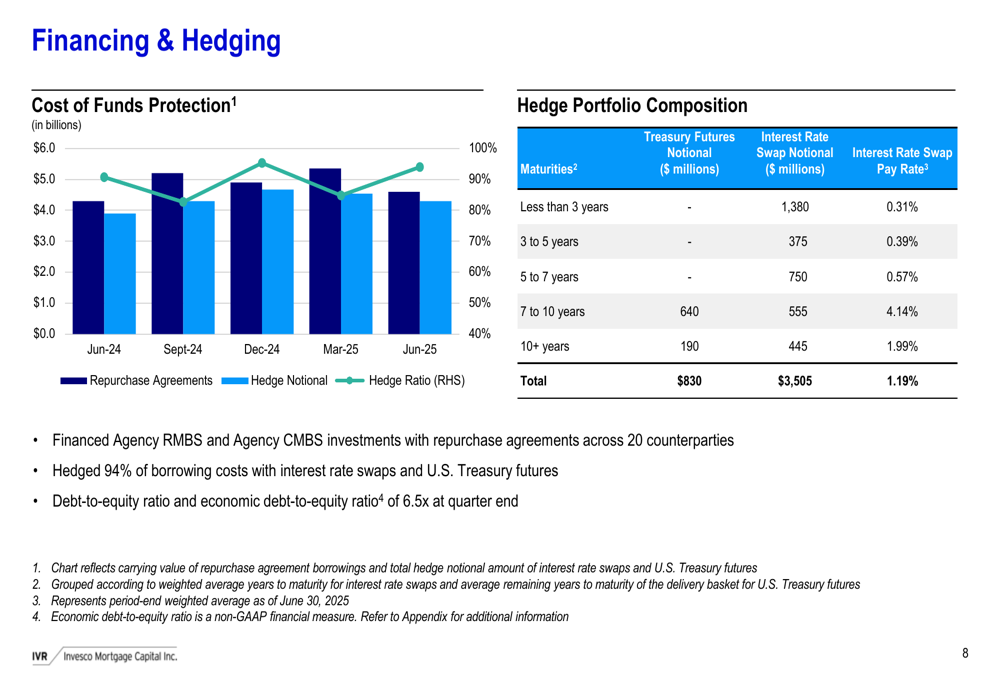

Financing and Risk Management

Invesco Mortgage Capital improved its leverage profile during the quarter, with the debt-to-equity ratio decreasing to 6.5x from 7.1x in Q1 2025. The company financed its Agency RMBS and CMBS investments with repurchase agreements across 20 counterparties.

To manage interest rate risk, the company hedged 94% of its borrowing costs with interest rate swaps and U.S. Treasury futures. The hedge portfolio consisted of $3.5 billion in interest rate swap notional amount with a weighted average pay rate of 1.19%, and $830 million in U.S. Treasury futures notional.

The following chart illustrates the company’s financing and hedging strategy, showing the relationship between repurchase agreements, hedge notional, and hedge ratio:

At quarter-end, Invesco reported holding $362 million of unrestricted cash and unencumbered investments, providing substantial liquidity to navigate market conditions.

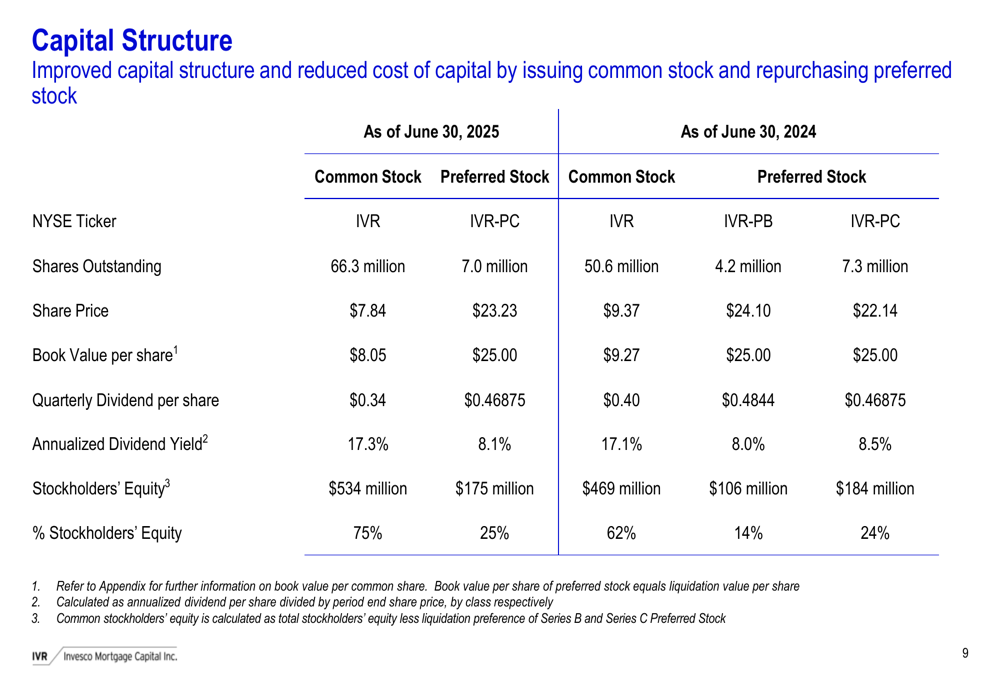

Capital Structure and Outlook

Invesco Mortgage Capital’s capital structure as of June 30, 2025, included $534 million in common stockholders’ equity (75% of total equity) and $175 million in preferred equity (25%). The company issued $2.2 million of common stock under its at-the-market program during the quarter and repurchased Series C Preferred Stock with a carrying value of $2.3 million.

Looking forward, the company faces continued challenges from market volatility but appears positioned to navigate the environment with its reduced leverage, substantial liquidity, and hedged portfolio. The maintenance of the dividend despite lower earnings suggests management confidence in the portfolio’s ability to generate sufficient income in the coming quarters.

However, investors should note that the negative economic return and declining book value in Q2 2025 represent a significant deterioration from the previous quarter’s performance. The company’s ability to stabilize book value and return to positive economic returns will be crucial for long-term shareholder value.

The stock closed at $7.63 on July 25, 2025, up 0.92% for the day, and trades at a slight discount to its reported book value of $8.05 per share.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.